Idaho: Who Pays? 6th Edition

IDAHO

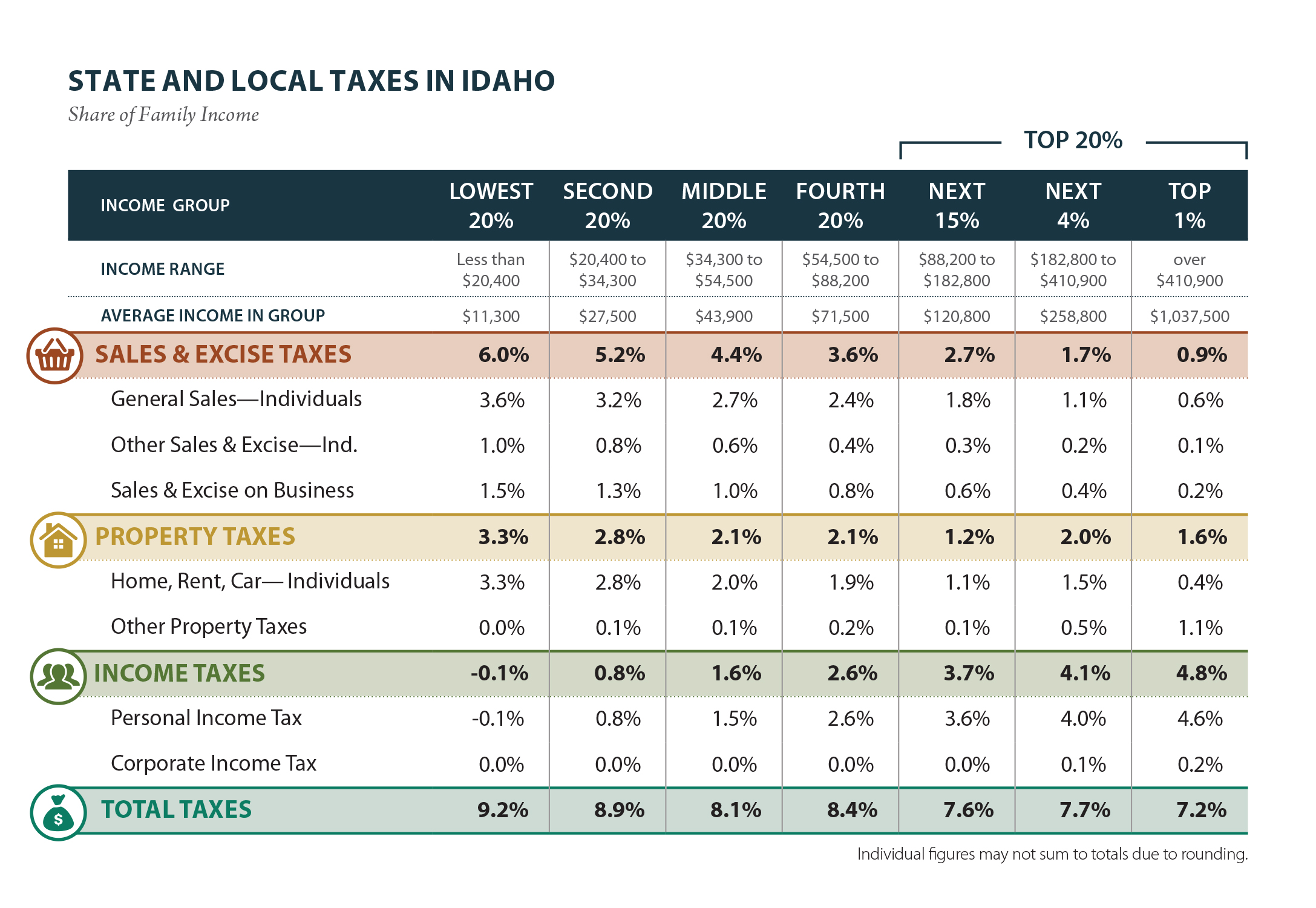

IDAHO STATE AND LOCAL TAXES

Taxes as Share of Family Income

| Top 20% | |||||||

|---|---|---|---|---|---|---|---|

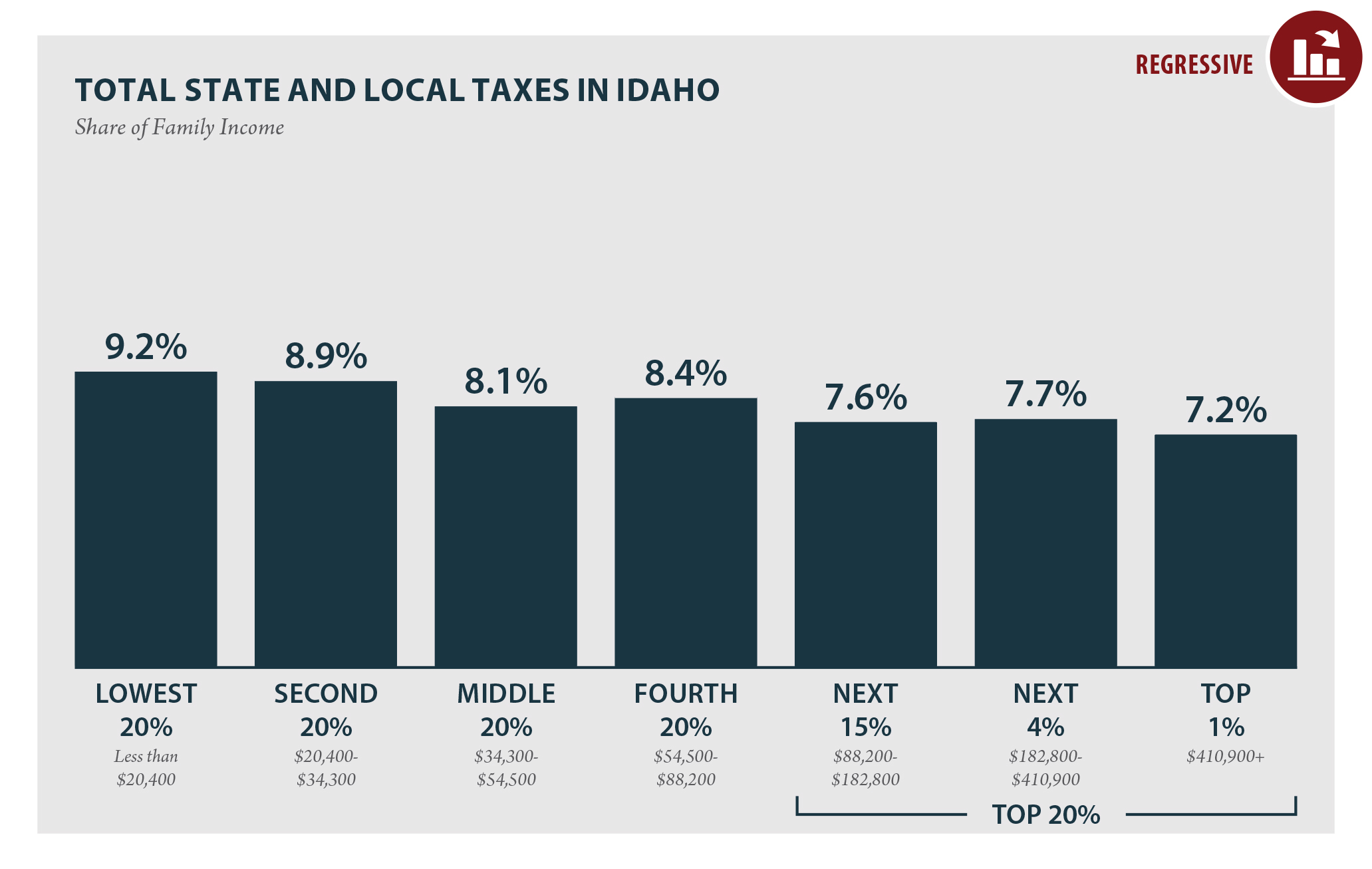

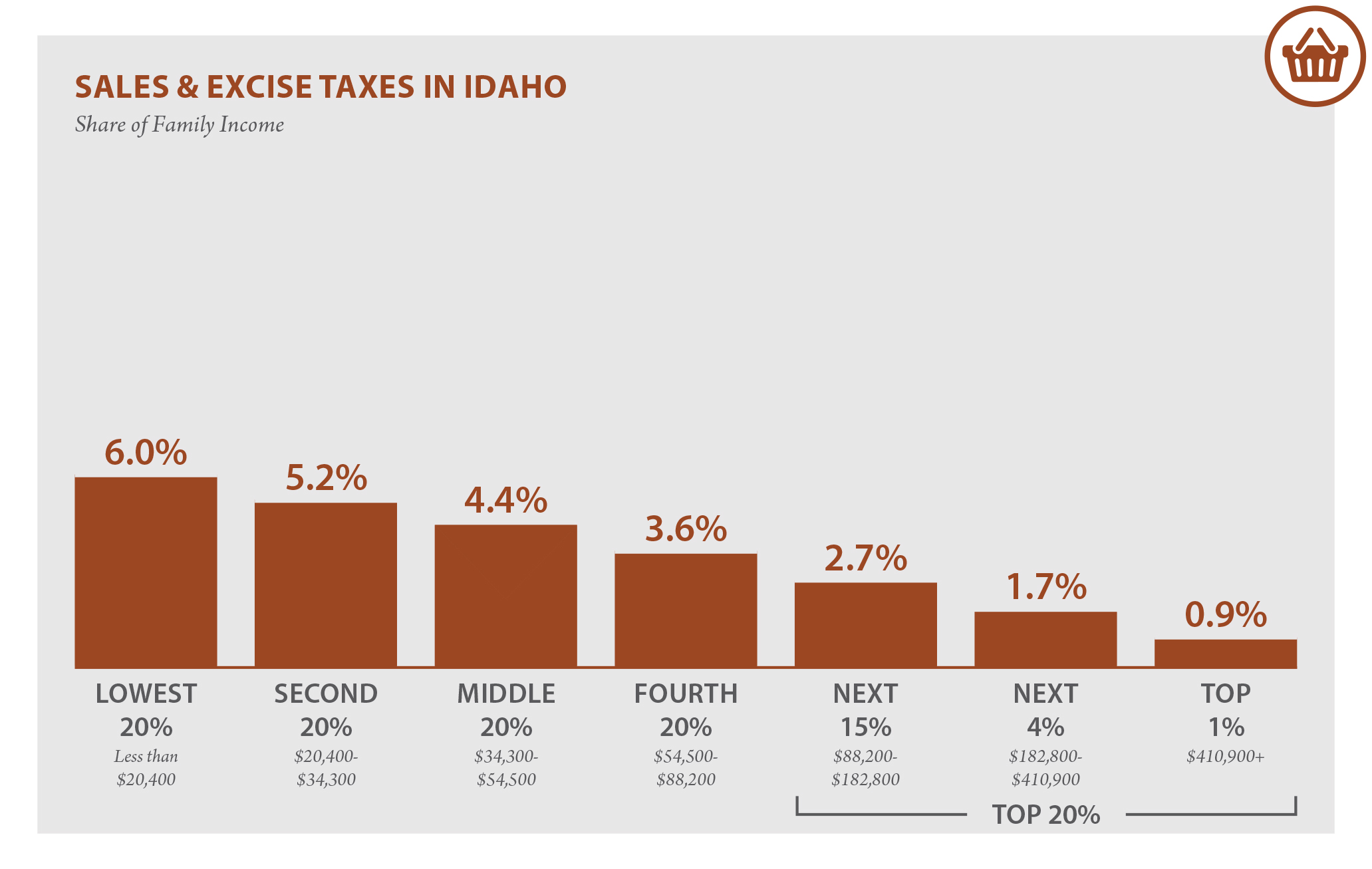

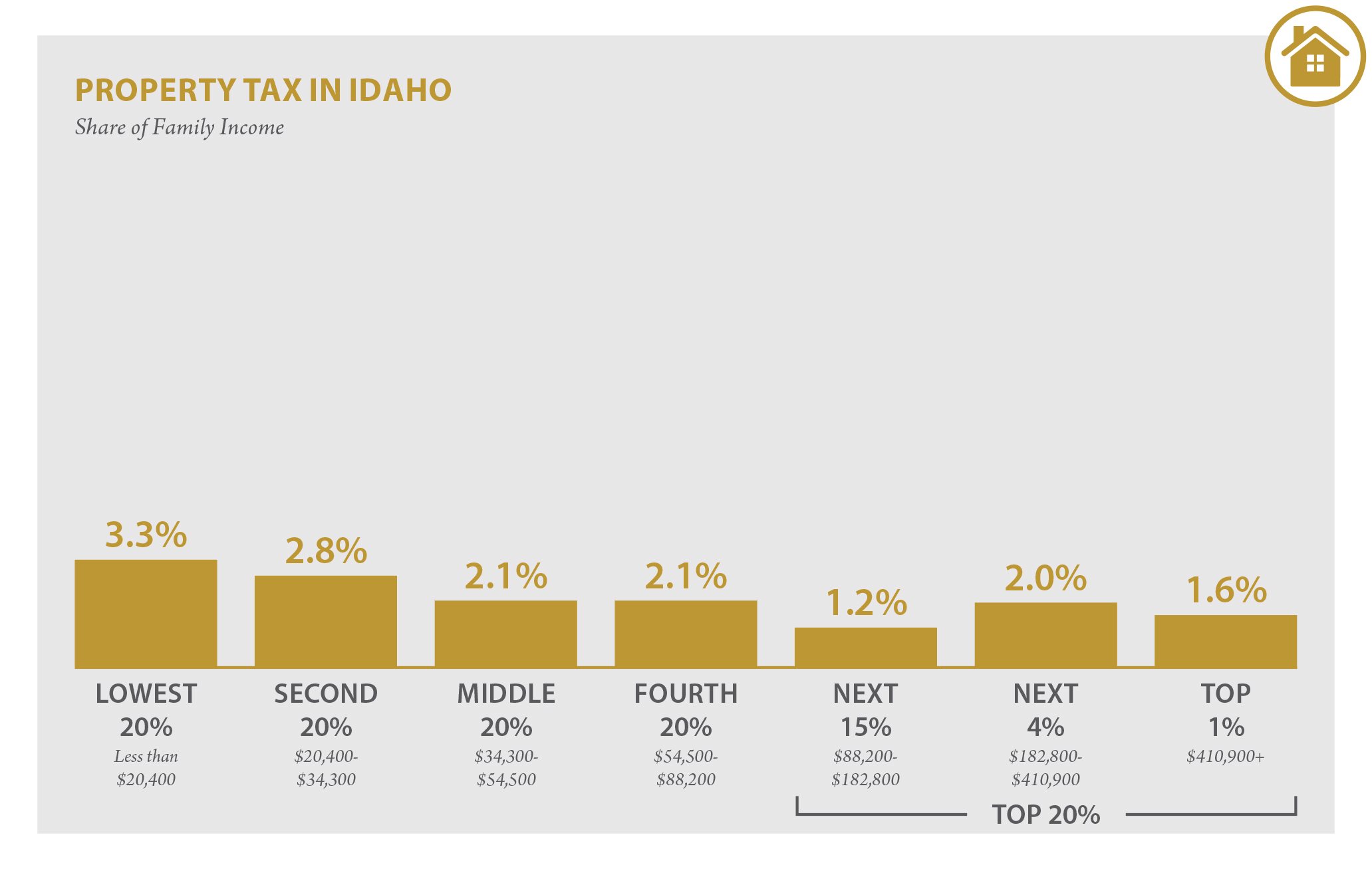

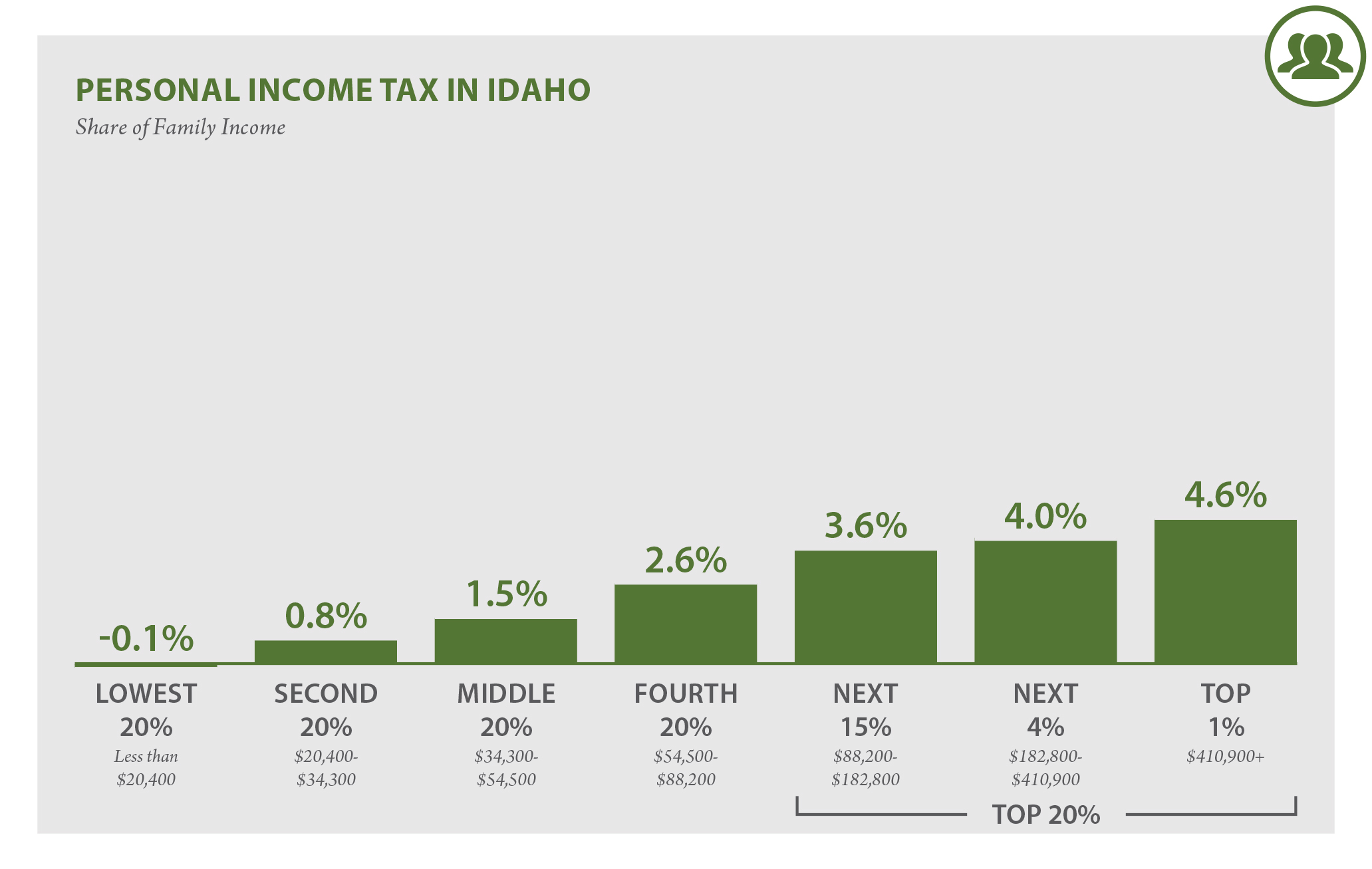

| Income Group | Lowest 20% |

Second 20% |

Middle 20% |

Fourth 20% |

Next 15% |

Next 4% |

Top 1% |

| Income Range | Less than $20,400 |

$20,400 to $34,300 |

$34,300 to $54,500 |

$54,500 to $88,200 |

$88,200 to $182,800 |

$182,800 to $410,900 |

over $410,900 |

| Average Income | $11,300 | $27,500 | $43,900 | $71,500 | $120,800 | $258,800 | $1,037,500 |

| Sales & Excise Taxes | 6.0% | 5.2% | 4.4% | 3.6% | 2.7% | 1.7% | 0.9% |

| General Sales – Individuals | 3.6% | 3.2% | 2.7% | 2.4% | 1.8% | 1.1% | 0.6% |

| Other Sales & Excise – Ind. | 1.0% | 0.8% | 0.6% | 0.4% | 0.3% | 0.2% | 0.1% |

| Sales & Excise on Business | 1.5% | 1.3% | 1.0% | 0.8% | 0.6% | 0.4% | 0.2% |

| Property Taxes | 3.3% | 2.8% | 2.1% | 2.1% | 1.2% | 2.0% | 1.6% |

| Home, Rent, Car – Ind. | 3.3% | 2.8% | 2.0% | 1.9% | 1.1% | 1.5% | 0.4% |

| Other Property Taxes | 0.0% | 0.1% | 0.1% | 0.2% | 0.1% | 0.5% | 1.1% |

| Income Taxes | -0.1% | 0.8% | 1.6% | 2.6% | 3.7% | 4.1% | 4.8% |

| Personal Income Tax | -0.1% | 0.8% | 1.5% | 2.6% | 3.6% | 4.0% | 4.6% |

| Corporate Income Tax | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.1% | 0.2% |

| TOTAL TAXES | 9.2% | 8.9% | 8.1% | 8.4% | 7.6% | 7.7% | 7.2% |

Individual figures may not sum to totals due to rounding. Download the table

{kind=link}

TAX FEATURES DRIVING THE DATA in Idaho

Progressive Features |

Regressive Features |

|---|---|

|

|

ITEP Tax Inequality Index

According to ITEP’s Tax Inequality Index, which measures the impact of each state’s tax system on income inequality, Idaho has the 38th most unfair state and local tax system in the country. Incomes are more unequal in Idaho after state and local taxes are collected than before. (See Appendix B for state-by-state rankings and the methodology section for additional detail on the index.)

Note: Figures show permanent law in Idaho enacted through September 10, 2018, at 2015 income levels. Top figure represents total state and local taxes as a share of non-elderly income. The sixth edition of Who Pays does not include the impact of the federal deduction for state and local taxes (SALT) because policy changes in the 2017 federal Tax Cuts and Jobs Act temporarily limited the extent to which the SALT deduction functions as a generalized offset of state and local taxes.