Read this Policy Brief in PDF Form

One of the thorniest problems in administering state corporate income taxes is how to distribute the profits of multi-state corporations among the states in which they operate. Ultimately, each corporation’s profits should be taxed in their entirety, but some corporations pay no tax at all on a portion of their profits. This problem has emerged, in part, due to recent state efforts to manipulate the “apportionment rules” that distribute such profits. This policy brief explains how apportionment rules work and assesses the effectiveness of special apportionment rules such as “single sales factor” as economic development tools.

Why Apportionment is Necessary

Most large corporations do business in more than one state and, as a result, are typically subject to the corporate income tax in multiple states. However, each state faces two important limits on how much of these corporations’ profits it can tax.

- First, if a corporation does not conduct at least a minimal amount of business in a particular state, that state is not allowed to tax the corporation at all. Corporations that have sufficient contact in a state to be taxable are said to have “nexus” with that state.

- Second, each state where a corporation has nexus must devise rules for dividing the corporation’s profits into an in-state portion and an out-of-state portion — a process known as “apportionment.” The state can then only tax the in-state portion.

These limits exist for a good reason: if every state taxed all of the income of all corporations operating within the state’s borders, businesses could find their profits taxed multiple times. Indeed, when state corporate income taxes were first adopted, there were no agreed-upon rules for dividing corporate profits among states. As a result, some businesses found that nationally, more than 100 percent of their profits were subject to state taxes. In the 1950s, legal reformers worked to set up a fair, uniform way of allocating income among states that would result in multi-state businesses’ profits being taxed exactly once. The result was the Uniform Division of Income for Tax Purposes Act (UDITPA), a piece of model legislation that about half the states with a corporate income tax have adopted.

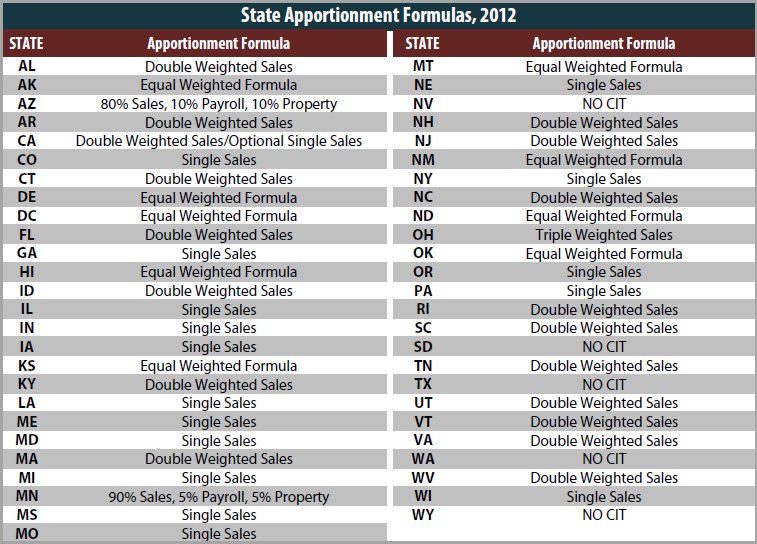

How States Apportion Income

UDITPA recommends an apportionment rule that relies equally on three different factors in determining the share of a corporation’s profits that can be taxed by a state. These factors are:

- The percentage of a corporation’s nationwide property that is located in a state.

- The percentage of a corporation’s nationwide sales made to residents of a state.

- The percentage of a corporation’s nationwide payroll paid to residents of a state.

The main rationale for using these three factors to determine taxable income is that it is impossible to determine with any accuracy the specific parts of a company that generate a given dollar of profit, let alone the states in which those parts may be located. These three factors are viewed as reasonable approximations of the share of a company’s profit that arises from doing business in a state, based on both the demand for company output in the state (the sales factor) and the production activity in which it engages in that state (the property and payroll factors), since profits are a function of both supply and demand. UDITPA’s recommendation was to assign each of these three factors an equal weight in distributing a company’s business income among the states in which it operates. If every state used the apportionment rule UDITPA recommends, it would be an important step towards ensuring that all corporate profits are subject to taxation.

However, over the past twenty years, many states have chosen to reduce the importance of the property and payroll factors and increase the importance of the sales factor. The majority of states now use apportionment formulas that give “double-weight” or greater to the sales factor. This means a corporation’s in-state sales are at least twice as important as each of the other factors. At the extreme, more than a dozen states now rely entirely on the sales factor (and therefore do not use the property or payroll factors at all) in determining at least some corporations’ tax liabilities. This approach is known as the “single sales factor” or SSF.

Advantages and Disadvantages of Increasing the Sales Factor

Single sales factor (SSF) is typically enacted for two reasons. First, it is argued that SSF makes a state a more attractive place for businesses to expand their property and payroll: if the property and payroll factors are ignored in calculating a state’s corporate tax, then a business can hire employees or build a plant in a state without incurring any additional corporate profits tax. Second, SSF is sometimes enacted in response to threats from companies that already have substantial in-state employment and property. For example, Massachusetts adopted SSF in response to threats from Raytheon that it would reduce its employment in the state unless it was adopted.

These arguments overlook several disadvantages of heavily weighting the sales factor:

- While some companies will benefit from SSF, other companies will actually pay more taxes under SSF. Manufacturing companies that have more of their property and payroll in-state (and sell more of their products to customers in other states) will benefit from SSF, but companies with little in-state employment and property that sell proportionately more of their products in-state will be hurt by SSF. Whether SSF will reduce, or increase, a state’s corporate income tax revenue depends on the importance of the state for the purposes of producing goods and services relative to its importance as a market for those goods and services.

- When SSF is enacted in response to the threats of in-state corporations to relocate in other states, there is no guarantee that these corporations will not “take the money and run.” For example, after the passage of SSF, Raytheon cut thousands of Massachusetts jobs.

- SSF creates harmful incentives for some businesses. A company that sells products in an SSF state, but does so only by shipping products into the state (and therefore has no nexus) will not have to pay any income tax to the state. But if such a company makes even a small investment of employees or property in the state, it will immediately have much of its income apportioned to the state because the sales factor counts so heavily. Thus, SSF gives these companies a clear incentive not to invest in the state. Even worse, SSF gives companies with in-state employees an incentive to move all of their employees out of state to eliminate their nexus with the state—thus zeroing out their tax.

- By discriminating against some companies and in favor of others, SSF makes corporate income taxes less fair—and can result in profitable companies paying no state income tax. For example, under the Illinois SSF rules, a corporation that has all of its employees and property in Illinois—but makes all of its sales to customers in other states—will pay no Illinois income tax, no matter how profitable it is. This unfairness reduces public confidence in the tax system.

The use of SSF has created a lack of uniformity in corporate tax rules. As a result, corporations now face the same inequitable treatment that prompted the UDITPA rules sixty years ago: some multi-state businesses find their income taxed more than once, while others are not taxed at all. This inequitable treatment undermines the perceived legitimacy of the tax system by arbitrarily discriminating in favor of certain corporations and creates perverse tax incentives that can deter corporations from moving to, or remaining in, some states. Returning to a more uniform set of apportionment rules is an important first step in preventing widespread tax avoidance and ensuring that state corporate income taxes are applied fairly.