Read Senate testimony as a PDF

Testimony for the House Committee on Ways and Means

Hearing on Long-Term Financing of the Highway Trust Fund

Carl Davis, Research Director

Institute on Taxation and Economic Policy (ITEP)

June 17, 2015

The federal Highway Trust Fund (HTF) is the single most important mechanism for funding maintenance and improvements to the nation’s transportation infrastructure. Absent Congressional action, however, the HTF will face insolvency at the end of July. Unfortunately, despite the critical importance of infrastructure to the U.S. economy, the condition of the HTF has been allowed to deteriorate to the point that imminent insolvency has become entirely normal.

Since 2008, Congress has dealt with recurring shortfalls in the HTF through a series of short-term patches that have collectively transferred $65 billion in outside funding to the account. While these transfers have played an important role in funding the nation’s transportation network, they also represent a failure to deal with the root cause of these recurring shortfalls: an outdated and poorly designed gasoline tax.

Increasing and reforming the gas tax could adequately and sustainably fund the HTF for decades to come. New funding sources such as a vehicle miles traveled tax (VMT tax), on the other hand, hold some long-term promise but cannot address the fund’s current shortfall and are not necessarily a panacea for the HTF’s revenue sustainability problem. Finally, other high profile funding options such as a repatriation holiday or deemed repatriation of corporate profits are problematic from a tax policy perspective, and entirely unsustainable as revenue raising options.

Gas Tax Design is Flawed but Fixable

The HTF is currently facing insolvency because the federal gas tax is poorly designed. On October 1st, the nation’s 18.4 cent per gallon federal gas tax rate will become 22 years old. As a result, drivers have been paying roughly $3 in federal gas taxes on every tank of gas they have bought over the last two decades. But as drivers’ contributions have stagnated, the cost of asphalt, steel, and machinery has risen by roughly 60 percent.[1] This growing disconnect between the cost of the roads that drivers use, and the price they pay to use them, has played a large role in causing HTF revenues to consistently fall short of infrastructure needs.

Simply put, the 18.4 cent federal gas tax rate is outdated. Federal funding for the nation’s transportation infrastructure would be on a much more sustainable course if the rate had been allowed to rise alongside inflation in the same manner that numerous income tax provisions did over this time period (e.g., personal exemptions, standard deductions, tax brackets, and the Earned Income Tax Credit).

But a lack of planning for inflation is not the only challenge facing the federal gas tax. According to the Federal Highway Administration, the average fuel-efficiency of a passenger vehicle on America’s roadways has increased by roughly 12 percent over the last two decades—from 19.3 to 21.6 miles per gallon.[2] For a vehicle with a 15 gallon gas tank, this means that the average driver is able to wear down the roadways with 35 extra miles of driving before they have to stop, refuel, and pay anything in gas taxes. The result has been reduced gas tax collections, and less revenue with which to maintain and improve the nation’s transportation network.

In late 2013, ITEP examined the impact of both inflation and fuel-efficiency growth in significant detail and concluded that inflation has, by far, played the larger role in contributing to the HTF funding shortfalls of recent years:

Over three-fourths (78 percent) of the current gasoline tax revenue shortfall is a result of Congress’ failure to plan for inevitable growth in the cost of building and maintaining the nation’s infrastructure. The remainder (22 percent) is due to improvements in vehicle fuel-efficiency.[3]

This does not need to be the case. Immediately increasing the gas tax and allowing the rate to rise each year alongside a formula that considers both inflation and fuel-efficiency gains would put the HTF on a sustainable course for decades to come. Had this reform been implemented in the late 1990s, there would be no question as to the HTF’s solvency as the fund would have ran a surplus in every subsequent year, thereby facilitating as much as $215 billion in additional transportation investments. Today, the cost to drivers associated with this reform would be roughly 11 cents per gallon in additional gas taxes—an amount equal to less than $5 per month for the average driver.[4]

Diverse Group of States Shows the Way Forward

While federal gas tax increases and reforms have long been viewed as politically impossible, the progress being made in the states shows that there is a practical way forward. Since February 2013, sixteen politically and geographically diverse states stretching from Idaho to Massachusetts have enacted meaningful gas tax increases or reforms.[5]

Partially as a result of these changes, there are now nineteen states that levy a reformed, variable-rate gas tax where the tax rate can automatically grow over time alongside factors such as inflation, gas prices, or fuel-efficiency.[6] Some states, such as Florida and North Carolina, have used these smarter, variable-rate structures for a number of years. Others, such as Pennsylvania and Utah, are more recent additions to this group.

But of all the states with variable-rate gas taxes, Georgia is arguably the leader. In May 2015, Governor Nathan Deal signed a reform that addresses both of the major challenges to the sustainability of the state’s gas tax. In addition to a flat, one-time increase in the tax, Georgia’s gas tax rate will now be allowed to rise each year to keep pace with both inflation and vehicle fuel-efficiency gains. While the inflation component of this formula is not unusual (similar formulas exist in Florida, Maryland, Rhode Island, and Utah), the fuel-efficiency inflator is the first of its kind.

Issues with Vehicle Miles Traveled Taxes

As electric and highly efficient vehicles have grown in popularity, increased attention has been paid to proposals that would transition the nation’s system of transportation finance away from taxes on motor fuel and toward taxes directly on the number of miles driven. On July 1, Oregon will take a significant first step in this direction by allowing 5,000 volunteer drivers to permanently exempt themselves from the state’s gasoline tax in exchange for paying a 1.5 cent tax on each mile that they drive.[7] While this experiment is a welcome example of forward thinking, there are at least three important caveats to keep in mind.

First, VMT taxes are not a solution to the immediate funding challenges facing the HTF, or to the broader infrastructure funding needs that exist right now. Recent opinion polling shows that VMT taxes are unpopular among the American people, though this may change as people become more familiar with these types of taxes.[8] Moreover, installing the devices needed to track and report vehicle mileage is a costly and time consuming endeavor that could take years or even decades to fully implement, depending on whether efforts are made to retrofit current vehicles with the technology.

Second, even if a VMT tax could be implemented immediately, these types of taxes are not inherently better than gas taxes at weathering the gradual effects of inflation on their purchasing power. Oregon’s flat VMT tax of 1.5 cents per mile, for example, is exactly as vulnerable to inflation as the state’s flat gas tax of 30 cents per gallon. As we explained in a recent report on this subject:

Transitioning from a pay-per-gallon gas tax to a pay-per-mile VMT tax will not necessarily put federal and state transportation revenues on a sustainable course. If the tax rate levied under a VMT tax is not allowed to grow alongside the inflation rate, revenues will quickly begin to lag behind the cost of building and maintaining the nation’s infrastructure—much as gas tax revenues have for decades. Lawmakers interested in adequately funding transportation on an ongoing basis should immediately index their gas tax rates to inflation, and should be aware that such indexing will also be needed under any VMT tax they might enact.[9]

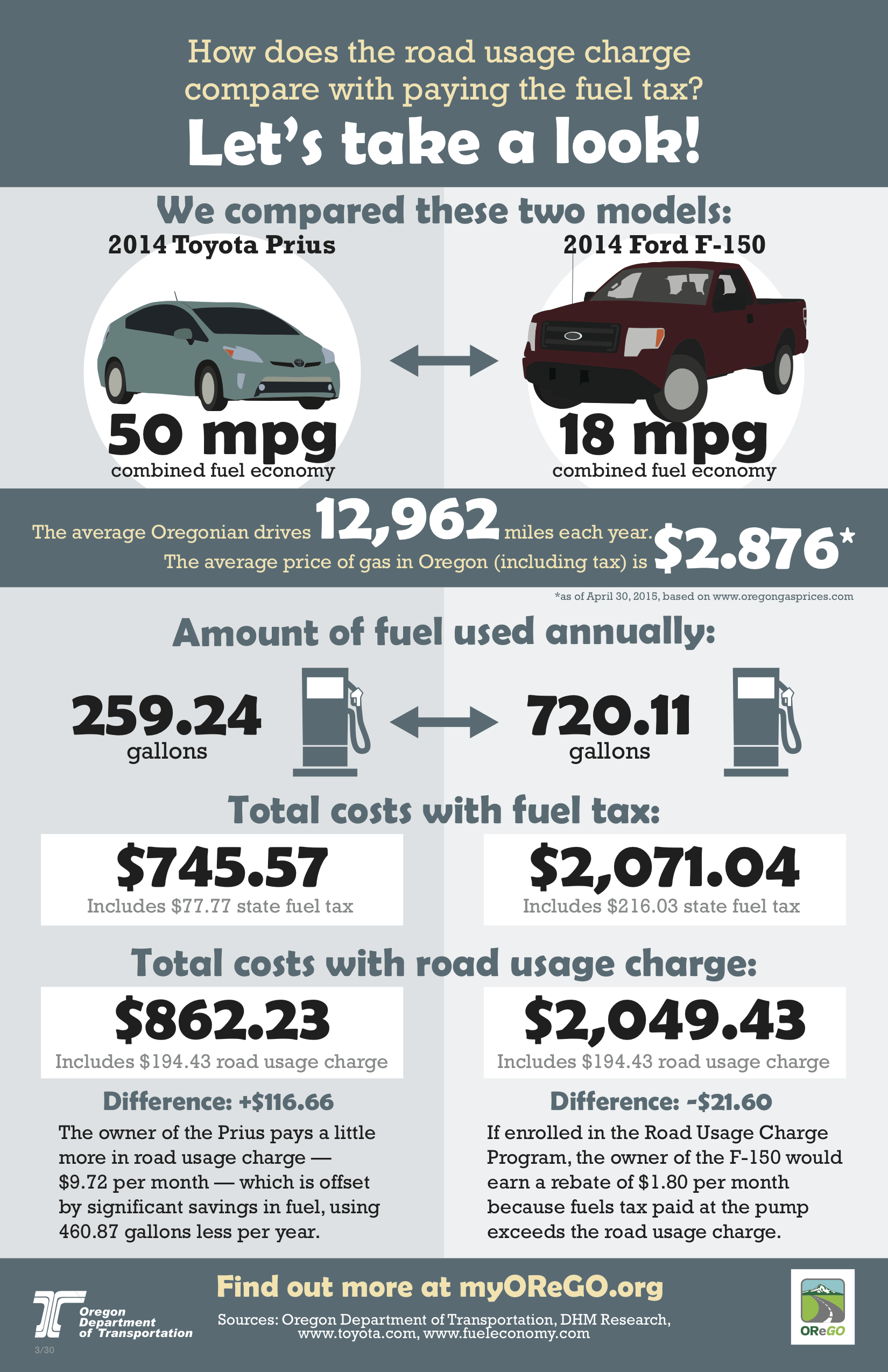

Third and finally, many VMT tax proposals come with worrisome environmental implications. Oregon’s upcoming experiment, for example, is expected to be very popular among owners of fuel-inefficient cars who purchase larger volumes of gasoline (and pay higher gas taxes) relative to their neighbors. Paying by the mile, rather than by the gallon, will be of such great benefit to these drivers that lawmakers put a firm cap on the number of inefficient cars allowed into the experiment (only 1,500 slots are reserved for vehicles rated at 17 miles per gallon or less). Hybrid and electric vehicle owners, by contrast, will fare quite poorly under this program. The Oregon Department of Transportation calculates that a Toyota Prius owner could see their taxes rise by as much as $117 per year under this tax.[10] While some of this disparity could be alleviated by reducing the tax rate for vehicles that get better gas mileage, this option has not been a central part of most VMT tax discussions thus far.

Repatriation: An Ineffective Band-Aid

Rather than deal with the gas tax flaws at the heart of the HTF’s current shortfall, some lawmakers have proposed patching the HTF with either a voluntary or mandatory tax on profits held offshore by corporations. These proposals would reward and encourage offshore tax avoidance, while at best only providing a temporary fix to the gap in funding.

The most problematic proposal in this category is known as a repatriation holiday. Under a repatriation holiday, multinational corporations could voluntarily bring back profits held offshore by paying tax on those profits at a rate much lower than the 35 percent rate they would normally owe (one such proposal would set the repatriation rate as low as 6.5 percent).

But repatriation holidays are not a sustainable funding source for the HTF because they would actually lose revenue in the medium- and long-term. In fact, the Joint Committee on Taxation (JCT) found that a repatriation holiday could cost as much as $96 billion in just 10 years.[11] This is because the holiday would encourage companies to hoard even more of their future profits in offshore tax havens in anticipation of another holiday, and because much of the money repatriated under a holiday would have been eventually repatriated at a higher tax rate if the holiday were not enacted.

Aside from a voluntary repatriation holiday, consideration has also been given to enacting a mandatory, or deemed, repatriation tax on corporate profits held offshore. For example, President Barrack Obama has proposed paying for infrastructure with a 14 percent mandatory tax on unrepatriated profits as part of a broad corporate tax reform that would include a 19 percent minimum tax on foreign profits moving forward.

As with a voluntary repatriation holiday, however, this form of mandatory repatriation would reward companies for their current offshore tax dodging with a special lower rate, and would incentivize companies to shift more of their operations offshore in order to enjoy the lower rate.

In addition, while both proposals would raise revenue in the short-term, they are not sustainable solutions. If the HTF is simply patched with a repatriation tax, the fund will inevitably face insolvency yet again in the very near future. The result would be a quick return to the same debate that has been rehashed repeatedly from at least 2008 to the present, and a continued lack of certainty for the agencies responsible for maintaining and enhancing the nation’s infrastructure.

Conclusion

The root cause of the Highway Trust Fund’s looming insolvency is that its primary revenue source—the federal gas tax—is poorly designed. Specifically, the tax’s stagnant and outdated rate contains no mechanism for growing with inflation, or for dealing with the more recent rise in vehicle fuel-efficiency.

In an effort to address these same flaws in their own gas taxes, state-level lawmakers have increasingly been moving forward with gas tax increases and reforms that could serve as models for federal action on this issue. Rather than focusing on short-term solutions, a growing group of states have transitioned toward a reformed, variable-rate gas tax that can finance economically vital transportation investments in both the short- and long-terms.

Unlike the gas tax, a new tax on the number of miles that drivers travel is not a realistic funding option in the short-term. Moreover, this type of vehicle miles traveled tax (VMT tax) will be unsustainable in the long-term as well if its tax rate is calculated as a flat amount per mile, regardless of changes in inflation.

Of all the proposals under consideration, repatriation is among the most problematic. A repatriation holiday could offer a short-term revenue boost but would provide no funding for transportation in medium- or long-term, and would actually reduce federal revenues overall. Additionally, any repatriation plan comes with the added downside of encouraging corporations to conduct more of their operations offshore (either on paper or in reality).

The gas tax has been the cornerstone of transportation finance for nearly sixty years. As the states have shown, this tax could continue to play this valuable role for decades to come if its rate is simply updated and reformed. Done correctly, the result could be an end to the HTF’s perpetual funding crises for decades to come, and the beginning of hugely valuable investments in the nation’s transportation infrastructure.

[1] This covers the 1993-2013 period in order to be consistent with the fuel-efficiency figures cited below. To be clear, this does not suggest that construction costs have grown in an unprecedented or unexpected way. Prices in the broader economy, as measured by the Consumer Price Index, rose by 61 percent over this same period.

[2] See Table VM-1 from the Federal Highway Administration’s Highway Statistics series. 1993 data for “passenger cars” and “2-axle, 4-tire trucks” are available at: http://www.fhwa.dot.gov/ohim/1994/section5/vm-1.pdf and 2013 data for “all light duty vehicles” are available at http://www.fhwa.dot.gov/policyinformation/statistics/2013/vm1.cfm.

[3] Institute on Taxation and Economic Policy. “A Federal Gas Tax for the Future.” September 22, 2013. Available at: https://itep.org/itep_reports/2013/09/a-federal-gas-tax-for-the-future.php.

[4] Ibid.

[5] Davis, Carl. “Sweet Sixteen: States Continue to Take On Gas Tax Reform.” Tax Justice Blog. May 20, 2015. Available at: http://www.taxjusticeblog.org/archive/2015/05/sweet_sixteen_states_continue.php.

[6] Institute on Taxation and Economic Policy. “Most Americans Live in States with Variable-Rate Gasoline Taxes.” May 20, 2015. Available at: https://itep.org/itep_reports/2015/02/most-americans-live-in-states-with-variable-rate-gas-taxes-1.php.

[7] See Senate Bill 810 of Oregon’s 2013 Regular Session. Additional information on the program is available at http://www.myorego.org/.

[8] Agrawal, Asha Weinstein and Hilary Nixon. “How Do Americans Feel About Taxes and Fees to Fund Transportation?” Mineta Transportation Institute. April 2015. Available at: http://transweb.sjsu.edu/PDFs/research/1428-tax-survey-2015-top-line-results.pdf.

[9] Institute on Taxation and Economic Policy. “Pay-Per-Mile Tax is Only a Partial Fix.” May 28, 2014. Available at: https://itep.org/itep_reports/2014/05/pay-per-mile-tax-is-only-a-partial-fix.php.

[10] Oregon Department of Transportation. “How does the road usage charge compare with paying the fuel tax?” May 2015. Available at: http://www.myorego.org/wp-content/uploads/2015/05/orego_odot_cost_comparison.png.

[11] Barthold, Thomas A. Letter to Senator Orrin Hatch. Joint Committee on Taxation. June 6, 2014. Available at: http://www.hatch.senate.gov/public/_cache/files/1b24c4cf-6005-4a4e-bab7-3d9e3820c509/JCT%206-6-14.pdf.

{kind=link}