Read this Policy Brief in PDF Form

Sales taxes are an important revenue source, comprising close to half of all state revenues in 2012. But sales taxes are also inherently regressive because the lower a family’s income, the more of its income the family must spend on things subject to the tax. Lawmakers in many states have enacted “sales tax holidays” (at least 17 states will hold them in 2013) , providing a temporary break on paying the tax on purchases of clothing, computers and other items. While these holidays may seem to lessen the regressive impacts of the sales tax, in fact they do not. This policy brief examines the many problems associated with using sales tax holidays as a tax reduction device and concludes that they have more political than policy benefits.

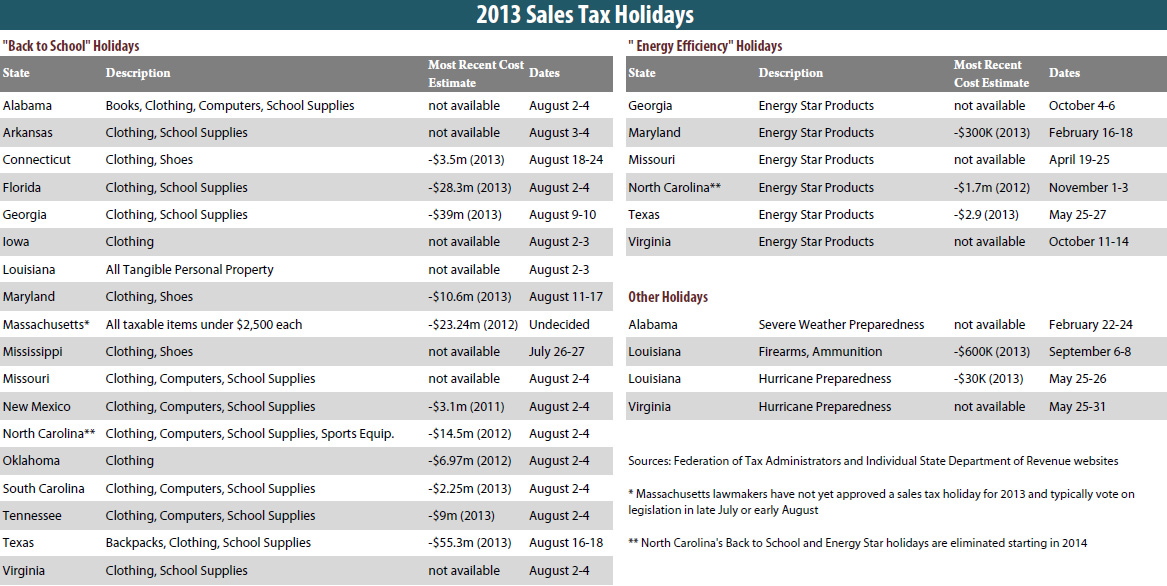

How Sales Tax Holidays Work

Sales tax holidays are temporary sales tax exemptions, usually applying to a finite number of taxable items for a very limited period of time. Since New York experimented with the first sales tax holiday in 1996, well over a dozen other states have passed similar legislation (New York no longer offers a holiday). These holidays are typically timed to take place in August, during the traditional “back to school” shopping season and offer breaks on school-related items like clothing, school supplies, and computers. Yet, a few states exempt all taxable goods during the holiday. Separate holidays for energy efficient appliances and storm preparation materials are becoming increasingly common as well. Most sales tax holidays last only two or three days, and almost all holidays apply only to items below some specified price (e.g. clothing items worth over $100 are generally not exempted).

Problems with Sales Tax Holidays

Justifications for sales tax holidays come in a variety of forms: they make a state’s tax structure more fair, spur economic activity, and come with little cost to the states in terms of revenue and administrative difficulties. These justifications don’t hold up under closer examination.

Sales Tax Holidays are Poorly Targeted

- Sales tax holidays are advertised as a way to give people a break from paying the sales tax . On the surface, this sounds good given that sales taxes are regressive, meaning they take a larger share of income from low-and middle-income families than from wealthy families. However, a two to three day sales tax holiday for selected items does nothing to provide relief to low-and moderate-income taxpayers during the other 362 days of the year. In the long run, sales tax holidays leave a regressive tax system basically unchanged.

- Because wealthier taxpayers can benefit from sales tax holidays, they offer less “bang for the buck” from a progressivity perspective than more targeted tax breaks such as low-income sales tax credits (described in ITEP Policy Brief, “Options for Progressive Sales Tax Relief ”) or Earned Income Tax Credits.

- In fact, wealthier taxpayers are often best positioned to benefit from the holidays, since they have more flexibility to shift the timing of their purchases to take advantage of the tax break –an option that isn’t available to families living paycheck to paycheck. Many low-income taxpayers spend most or all of their income just getting by—which means that they have less disposable income than wealthier taxpayers to spend when the holiday arrives.

- One recent study found that while households with earners above $30,000 were likely to increase their clothing purchases over a sales tax holiday weekend, households earning less than $30,000 were not.1

- The benefits of sales tax holidays are not limited to state residents, but instead extend to anybody that happens to be within the state’s borders at the time of the holidays including tourists and individuals who live close to the border.

Sales Tax Holidays Offer No Significant Retail Boost

- One popular rationale for sales tax holidays is that they increase local consumer spending and boost local retail, but this has not been demonstrated. Rather, increased sales during sales tax holidays have been shown to be primarily the result of consumers’ shifting the timing of their planned purchases.

Some Retailers Exploit Sales Tax Holidays

- Unscrupulous retailers can take advantage of the shift in the timing of consumer purchases by increasing their prices or watering-down their sales promotions during the tax holiday. One study of retailers’ behavior during a sales tax holiday in Florida found evidence of precisely that: up to 20 percent of the price cut consumers thought they were receiving from the state’s sales tax holiday was actually reclaimed by retailers. 2

Sales Tax Holidays Create Administrative Difficulties

Sales tax exemptions create administrative difficulties for state and local governments, and for the retailers who must collect the tax. For example, exempting groceries requires a sheaf of government regulations to police the border between non-taxable groceries and taxable snack food. A temporary exemption for clothing (or for any other back-to-school item) requires retailers and tax administrators to wade through a similar quantity of red tape for an exemption that lasts only a few days. Further complexity can arise in states with local sales taxes when some localities opt not to participate in the holiday and consumer unexpectedly end up paying local sales taxes on their purchases.

Sales Tax Holidays Cost Revenue

Revenue lost through sales tax holidays will ultimately have to be made up somewhere else, either through painful spending cuts or increasing other taxes. For this reason, many states have either repealed or temporarily suspended sales tax holidays in recent years. Lawmakers in Florida, Georgia, Maryland and Massachusetts canceled holidays during the height of the recent economic recession. Holidays in Illinois, the District of Columbia, West Virginia and Vermont were either short-lived or repealed. If the long-term consequence of sales tax holidays is a higher sales tax rate, low income taxpayers may ultimately be worse off as a result of these policies.

Conclusion

Sales tax holidays are poorly targeted and too temporary to meaningfully change the regressive nature of a state’s tax system. Lawmakers must understand that they can not resolve the unfairness of sales taxes simply by offering a short break from paying these taxes. Policymakers seeking to achieve greater tax fairness would do better to provide a permanent refundable low-income sales tax credit or Earned Income Tax Credit (EITC) to offset the impact of the sales tax on low- and moderate-income taxpayers.

1 Marwell, Nathan and Leslie McGranahan (2010), The Effect of Sales Tax Holidays on Household Consumption Patterns. Federal Reserve Bank of Chicago

2 Harper, R. K., Hawkins, R. R., Martin, G. S. and Sjolander, R. (2003), Price Effects around a Sales Tax Holiday: An Exploratory Study. Public Budgeting & Finance, 23: 108–113.