When thinking of tax havens, one generally pictures notorious zero-tax Caribbean islands like the Cayman Islands and Bermuda. However, we can also find a tax haven a lot closer to home in the state of Delaware – a choice location for U.S. business formation. A loophole in Delaware’s tax code is responsible for the loss of billions of dollars in revenue in other U.S. states, and its lack of incorporation transparency makes it a magnet for people looking to create anonymous shell companies, which individuals and corporations can use to evade an inestimable amount in federal and foreign taxes. The Internal Revenue Service estimated a total tax gap of about $450 billion with $376 billion of it due to filers underreporting income in 2006 (the most recent tax year for which this data is available).[i] While it is impossible to know how much underreported income is hidden in Delaware shell companies, the First State’s ability to attract the formation of anonymous companies suggests that it could rival the amount of income hidden in more well-known offshore tax havens.

Delaware ranks 46th in population among the 50 states with roughly 935,000 residents. Yet more than 1.1 million companies incorporated there as of 2014, including 65 percent of Fortune 500 parent companies.[ii] Additionally, 85 percent of Fortune 500 companies reported having at least one subsidiary in Delaware in 2014. In total, these companies reported more than 19,000 Delaware subsidiaries. In sum, 58 percent of all reported U.S. subsidiaries and 30 percent of total reported subsidiaries are housed in Delaware. In contrast, the two states that account for the largest contribution to the nation’s Gross Domestic Product, California and Texas, have 1,160 and 1,540 Fortune 500 subsidiaries, respectively.[iii] Delaware is also favored by foreign companies as a location for incorporating subsidiaries. A 2011 analysis of FTSE 100 companies (the largest businesses on the London Stock Exchange) found that they collectively had more than 2,000 subsidiaries registered in Delaware, which is more than double the number of subsidiaries the FTSE 100 has in the Netherlands, the second most used tax haven.[iv]

Why are so many businesses drawn to incorporate in Delaware? The most popular answer is the state’s “business-friendly climate.” It has a dedicated corporate court system (the Chancery Court) producing a steady stream of case law, an enormous network of corporate lawyers, and laws that favor management over shareholders. The legal benefits are likely a large draw for parent companies, but this cannot explain the disproportionate number of subsidiaries that choose Delaware over other states, since subsidiaries don’t have the same types of legal and corporate governance issues.[v] Another part of the appeal is the ease and rapidity with which a business entity can be formed there. Business entities can be set up in a number of hours. But the tax haven features of the state are a critical draw for individuals and corporations looking to engage in tax avoidance as well as illicit activities such as tax evasion and money laundering.

It is worth noting that there are a few other states that have similar tax haven features as Delaware, most notably Nevada, Wyoming, and South Dakota. However, this report focuses on Delaware due to the volume of business entities incorporated there. For example, in comparison to Delaware’s 19,000 Fortune 500 subsidiaries, Nevada, Wyoming, and South Dakota have less than 1,000 combined.

What Makes a Jurisdiction a Tax Haven?

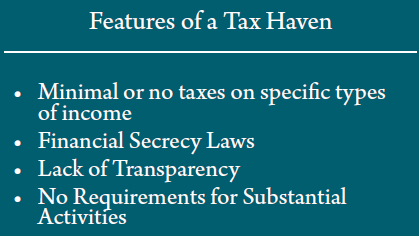

The Organisation for Economic Cooperation and Development (OECD) has identified four key tax haven features.[vi] First, and most obvious, a tax haven levies no or minimal taxes on specific types of income. Second, tax havens have laws or practices that encourage financial secrecy and inhibit an effective exchange of information about taxpayers to tax and law enforcement authorities. A third feature is the general lack of transparency in legislative, legal, or administrative practices, and fourth is the lack of a requirement that activities be “substantial,” suggesting that a jurisdiction is trying to attract investment or transactions that are driven primarily by tax considerations.

The “Delaware Loophole”

Delaware is not a typical zero-tax jurisdiction, nor is it one of the states with no corporate income tax (Nevada, Wyoming, and South Dakota). However, its tax code does contain a glaring loophole; it collects zero tax on income relating to intangible assets held by a “Delaware Holding Company,” or a “Passive Investment Company (PIC).” This includes interest and investment income as well as income related to intellectual property, such as trademarks and patents. Sometimes called the “Delaware loophole” or the “Passive Investment Company (PIC) loophole,” this allows corporations to set up holding companies in Delaware that the parent company or other subsidiaries then pay for the use of intellectual property. This income is not taxed in Delaware, while the payments can be deducted as a business expense from the parent company’s tax liability in its home state. In effect, states where corporations are actually operating can lose millions of dollars in revenue as a result of the Delaware loophole. A 2012 New York Times article estimated that the loophole had cost states approximately $9.5 billion over a decade in lost revenues.[vii] One econometric study analyzing Delaware’s role as a domestic tax haven (using data from over 2,500 firms between 1995 and 2009) estimated that firms using the Delaware PIC strategy reduced their state income tax liability by 15 to 24 percent, with the average firm saving an estimated $3.2 to $4.2 million annually.[viii]

One prominent example of a company’s use of the Delaware PIC strategy is Toys R Us, as it resulted in a significant South Carolina Supreme Court decision in 1993.[ix] Toys R Us, Inc. has a Delaware subsidiary, Geoffrey LLC, which on paper owns the company’s trademarks and trade names (such as its mascot, “Geoffrey the Giraffe”). Retail Toys R Us stores in other states pay royalties to Geoffrey LLC for the use of these intangible assets, which are not taxed in Delaware, and then deduct the royalties on their state tax returns. For example, in 1990, Geoffrey LLC received $55 million in royalty income, and Toys R Us was able to avoid an estimated $2.75 million in state taxes as a result of this strategy.

One prominent example of a company’s use of the Delaware PIC strategy is Toys R Us, as it resulted in a significant South Carolina Supreme Court decision in 1993.[ix] Toys R Us, Inc. has a Delaware subsidiary, Geoffrey LLC, which on paper owns the company’s trademarks and trade names (such as its mascot, “Geoffrey the Giraffe”). Retail Toys R Us stores in other states pay royalties to Geoffrey LLC for the use of these intangible assets, which are not taxed in Delaware, and then deduct the royalties on their state tax returns. For example, in 1990, Geoffrey LLC received $55 million in royalty income, and Toys R Us was able to avoid an estimated $2.75 million in state taxes as a result of this strategy.

It is impossible to know how widely the PIC strategy is used, but litigation by other states attempting to recover revenues has often brought this issue to light. A 2002 Wall Street Journal article identified nearly 50 companies that had been involved with litigation with states relating to their use of PICs.[x] While the PIC strategy is often used with Delaware subsidiaries, it can also be used in states that have no corporate income tax.

In addition to using PICs to shift profits between affiliated companies, corporations can also use them in “asset isolation” strategies, where external income can be shielded from taxes.[xi] This strategy, often used by financial institutions, involves investing in interest-yielding assets which are transferred to PICs in Delaware or other states that do not tax interest income. Even though that interest income is not taxed by any state, the parent company and other subsidiaries can access it by taking out loans from the PIC and deduct the interest paid to the PIC from their state tax liability.

Another use of PICs to facilitate state tax avoidance is pairing them with a “captive Real Estate Investment Trust (REIT)” strategy, which helped Wal-Mart save about $350 million in state taxes between 1998 and 2001, according to the Wall Street Journal.[xii] In this scenario, a corporation sets up a Delaware PIC subsidiary which has 99 percent ownership of a REIT. The company then transfers its real estate assets to the REIT and makes tax-deductible rent payments to the REIT, which are tax-free to the REIT if it pays out at least 90 percent of its profits in dividends to investors (i.e. the Delaware PIC). The PIC is not taxed on those dividends due to the Delaware loophole, and the PIC can pay dividends back to the parent company tax-free since corporations are not taxed on dividend payments from subsidiaries.[xiii] Again, this strategy can also be used in other states that do not tax investment income received from REITs.

Beneficial Ownership Secrecy and Lack of Substantial Activity Requirements

Another feature that Delaware shares with other tax havens is the ease with which an anonymous company can be created. This provides individuals and businesses with a vehicle for avoiding taxes or laundering income from illegal activities since it is very difficult (if not impossible) for authorities to trace the company back to the beneficial owners. While no U.S. state requires disclosure of beneficial ownership information for business entity formation, Delaware is one of the easiest jurisdictions in the world to set up an untraceable shell company. Setting up a company in Delaware requires less information than signing up for a library card.[xiv]

In 2013, the New York Times published an op-ed titled “Delaware, Den of Thieves?” by John Cassara, a former agent with the Treasury Department’s Financial Crimes Enforcement Network (FinCEN), in which Cassara told of the frequency of financial crimes investigations leading to Delaware, as well as Nevada and Wyoming.[xv] He spoke of foreign authorities requesting help from FinCEN when “following the money” brought them to an anonymous Delaware corporation, at which point the investigation would stall because it was impossible to identify the corporation’s true owners. Thus, the laws of Delaware and other so-called “secrecy jurisdictions” prevent both domestic and foreign authorities from prosecuting individuals and businesses that use anonymous shell companies to launder money or evade taxes at home and abroad.

Delaware law does not require businesses to provide any information on the beneficial owner(s) or to have a business office or any substantial activity in the state. To register a new business entity, only a “registered agent” with a physical Delaware address must be provided, which is often a third-party “company service provider (CSP)” that serves as the formation agent and the owner of record. Registered agents can also provide companies with directors, officers, and employees, as well as accounting and financial reporting services. In 2006, there were around 30,000 registered agents in Delaware, with about 240 that represented 50 or more different companies.[xvi] The New York Times reported that in 2012, one registered agent known as CT Corporation had an office in Wilmington, Delaware that was listed as the address for at least 285,000 companies.[xvii] As the largest registered agent in Delaware, CT Corporation represented about one-third of all the businesses incorporated in the state. A 2006 case study on Delaware conducted by the Financial Action Task Force (FATF) reported that many Delaware registered agents explicitly advertised the anonymity that beneficial owners can enjoy in the state.[xviii] Ultimately, in 2012 the Delaware Secretary of State issued standards prohibiting registered agents from marketing secrecy or anonymity.[xix] Some registered agents, such as Advantage Delaware LLC, still advertise anonymity (along with favorable business regulations and the many tax benefits of incorporating in the state).[xx]

Delaware law does not require businesses to provide any information on the beneficial owner(s) or to have a business office or any substantial activity in the state. To register a new business entity, only a “registered agent” with a physical Delaware address must be provided, which is often a third-party “company service provider (CSP)” that serves as the formation agent and the owner of record. Registered agents can also provide companies with directors, officers, and employees, as well as accounting and financial reporting services. In 2006, there were around 30,000 registered agents in Delaware, with about 240 that represented 50 or more different companies.[xvi] The New York Times reported that in 2012, one registered agent known as CT Corporation had an office in Wilmington, Delaware that was listed as the address for at least 285,000 companies.[xvii] As the largest registered agent in Delaware, CT Corporation represented about one-third of all the businesses incorporated in the state. A 2006 case study on Delaware conducted by the Financial Action Task Force (FATF) reported that many Delaware registered agents explicitly advertised the anonymity that beneficial owners can enjoy in the state.[xviii] Ultimately, in 2012 the Delaware Secretary of State issued standards prohibiting registered agents from marketing secrecy or anonymity.[xix] Some registered agents, such as Advantage Delaware LLC, still advertise anonymity (along with favorable business regulations and the many tax benefits of incorporating in the state).[xx]

In another ostensible effort to increase transparency, Delaware passed a law in 2006 that requires businesses to provide their registered agents with a “communications contact” that is an “officer, director, employee, or designated agent of the company” and requires registered agents to retain that information.[xxi] Similarly, in 2014 the state passed legislation requiring the registered agent to identify a person at the company that has a list of the entity’s legal owners.[xxii] However, the only way this information can be accessed is via a subpoena on the registered agent. So, this beneficial ownership information remains unavailable to the public and can only be obtained by authorities after cutting through several layers of red tape. In addition, the company’s legal owners may actually be other companies with hidden ownership.

Another issue is that many registered agents do not verify the identities of beneficial owners prior to company formation. FATF, which is an international intergovernmental body dedicated to preventing money laundering and terrorism financing, recommends that countries require CSPs to obtain identification documentation before setting up a business entity.[xxiii] However, in a random experiment where researchers attempted to set up anonymous shell companies, sometimes for risky-sounding purposes, Delaware CSPs were among the most likely to offer shell companies without asking for identification.[xxiv] Delaware ranked the second easiest state in which to form an anonymous shell corporation, trailing only Nevada. Due to the lax requirements in Delaware, Nevada, and a few other states, the researchers found that it was easier to set up an anonymous company in the United States than in most of the well-known tax havens like the Cayman Islands, the British Virgin Islands, and Switzerland. When the researchers divided the U.S. sample into CSPs and law firms, American CSPs ranked first of all the sample countries.[xxv]

The strategy of using Delaware shell corporations to hide beneficial ownership information to evade taxes is detailed in a book by Romanian accountant Laszlo Kiss entitled “United States, Tax Heaven – Uncle Sam Will Fight Your Taxes!”[xxvi] In 2010, Kiss was arrested by Romanian authorities in connection with embezzlement, money laundering, and tax evasion using a network of shell companies in Delaware and other offshore locations.[xxvii]

What Can Be Done?

If they wanted to, lawmakers in Delaware could pass legislation eliminating loopholes and various laws that have made their state an infamous onshore tax haven. Unfortunately, the Delaware Legislature appears complacent with its status as a tax haven and has only made minimal gestures in recent years toward change.

The good news is that lawmakers outside the state need not wait for Delaware to act, but instead can take immediate action at the state and national level to mitigate these issues.

Closing the Delaware Loophole

Some states have attempted to prevent revenues lost due to Passive Investment Company loopholes by adopting some variation of an “addback rule,” which requires companies operating in the state to add back into taxable income payments made to related companies for interest or intangible assets. For example, a company in a state passing an addback rule would no longer be able to avoid taxes by deducting payments for the use of a trademark made to a Delaware subsidiary (or a subsidiary in another state where that income would not be taxed). While this strategy may be effective to some extent, most states that have adopted it have exceptions to the rule, and there is a large degree of variation in the policies between states.[xxviii] With partial solutions like addback rules, corporate accountants can usually find other ways to shift income to states where it will be taxed less or not at all.

A more comprehensive solution is for states to adopt “combined reporting,” which is the most effective way to prevent state corporate tax avoidance.[xxix] Under combined reporting, companies are required to report the income and expenses of all out-of-state subsidiaries for the purpose of determining corporate income tax (in contrast to separate accounting, which only requires reporting of the income with a substantial “economic nexus” with the home state). In states that have enacted combined reporting laws, businesses no longer have an incentive to move income to other states, as they will be taxed on the income of all their U.S. subsidiaries. About half of all states have already adopted combined reporting.

Increasing Transparency in Beneficial Ownership

At the federal level, Congress could and should pass legislation requiring states to require beneficial ownership information from businesses. The Incorporation Transparency and Law Enforcement Act, which would mandate that states require the name and address of each beneficial owner of a company at the time of incorporation and after any change in ownership, has been proposed in the last several Congresses but has never come to a vote in either chamber. This legislation has had bipartisan support, being co-sponsored by former Sens. Carl Levin (D-MI) and Chuck Grassley (R-IA) in the Senate and Reps. Carolyn Maloney (D-NY), Peter King (R-NY), and Michael Fitzpatrick (R-PA) in the House. The bill, which is expected to be introduced again in this Congress, would give tax authorities and law enforcement a greater ability to investigate tax evasion and illicit financial flows. One of the biggest challenges the bill has faced is opposition from the Democratic Senators from Delaware, Tom Carper and Chris Coons. The state of Delaware, which gets around one-quarter of its revenues from franchise taxes and other business fees,[xxx] clearly has a vested interest in remaining the state of choice for business formation. Even so, Delaware state legislators are concerned enough about the state’s reputation for attracting shady business dealings that 31 of them signed on to a letter to the Delaware congressional delegation urging support on the Incorporation Transparency and Law Enforcement Act.[xxvii]

Fighting Tax Avoidance and Evasion at Home

U.S. officials often criticize the practices of offshore jurisdictions that facilitate tax avoidance, tax evasion, money laundering, terrorist financing, and other financial crimes. Unfortunately, there are jurisdictions within U.S. borders using similar tactics. It is unreasonable to expect other countries to make changes deterring tax haven abuse and improving transparency without holding U.S. states to the same standards.

[i] Internal Revenue Service, “IRS Releases New Tax Gap Estimates; Compliance Rates Remain Statistically Unchanged from Previous Study,” January 6, 2012. http://www.irs.gov/uac/IRS-Releases-New-Tax-Gap-Estimates;-Compliance-Rates-Remain-Statistically-Unchanged-From-Previous-Study

[ii] Delaware Division of Corporations, 2014 Annual Report. http://delaware.contentdm.oclc.org/cdm/ref/collection/p16397coll14/id/123.

[iii] Subsidiary data is from CTJ staff tabulations of the subsidiaries reported by Fortune 500 companies on their 2014 10-K forms, filed annually with the Securities and Exchange Commission. Some companies may not report all of their subsidiaries or fail to report the locations of subsidiaries, so these numbers are likely underestimated.

[iv] Amy Hamilton, “Report: Delaware is FTSE 100’s ‘Favourite Tax Haven’,” State Tax Notes, October 17, 2011.

[v] Scott D. Dyreng, Bradley P. Lindsey, and Jacob R. Thornock, “Exploring the Role Delaware Plays as a Domestic Tax Haven,” September 2012. http://ssrn.com/abstract=1737937

[vi] Organisation for Economic Co-operation and Development, “Harmful Tax Competition: An Emerging Global Issue,” 1998. http://www.oecd-ilibrary.org/taxation/harmful-tax-competition_9789264162945-en

[vii] Leslie Wayne, “How Delaware Thrives as a Corporate Tax Haven,” New York Times, June 30, 2012. http://www.nytimes.com/2012/07/01/business/how-delaware-thrives-as-a-corporate-tax-haven.html?_r=0

[viii] Scott D. Dyreng, Bradley P. Lindsey, and Jacob R. Thornock, “Exploring the Role Delaware Plays as a Domestic Tax Haven,” September 2012. http://ssrn.com/abstract=1737937

[ix] Ibid.

[x] Glen R. Simpson, “A Tax Maneuver in Delaware Puts Squeeze on Other States,” Wall Street Journal, August 9, 2002. http://www.wsj.com/articles/SB1028846669582427320

[xi] Michael Mazerov, “State Corporate Tax Shelters and the Need for Combined Reporting,” State Tax Notes, November 26, 2007.

[xii] Jesse Drucker, “Wal-Mart Cuts Taxes by Paying Rent to Itself,” Wall Street Journal, February 1, 2007. http://www.wsj.com/articles/SB117027500505994065

[xiii] Michael Mazerov, “State Corporate Tax Shelters and the Need for Combined Reporting,” State Tax Notes, November 26, 2007.

[xiv] Financial Transparency Coalition, “Who’s in your backyard? Looking at anonymous companies and their ownership of London Property,” March 4, 2015. http://financialtransparency.org/whos-in-your-backyard-looking-at-anonymous-companies-and-their-ownership-of-london-property/

[xv] John Cassara, “Delaware, Den of Thieves?” New York Times, November 1, 2013. http://www.nytimes.com/2013/11/02/opinion/delaware-den-of-thieves.html?_r=0

[xvi] Financial Action Task Force, “Third Mutual Evaluation Report on Anti-Money Laundering and Combating the Financing of Terrorism – United States of America,” June 23, 2006. http://www.fatf-gafi.org/media/fatf/documents/reports/mer/MER%20US%20full.pdf

[xvii] Leslie Wayne, “How Delaware Thrives as a Corporate Tax Haven,” New York Times, June 30, 2012. http://www.nytimes.com/2012/07/01/business/how-delaware-thrives-as-a-corporate-tax-haven.html?_r=0

[xviii] Financial Action Task Force, “Third Mutual Evaluation Report on Anti-Money Laundering and Combating the Financing of Terrorism – United States of America,” June 23, 2006. http://www.fatf-gafi.org/media/fatf/documents/reports/mer/MER%20US%20full.pdf

[xix] Secretaries of State of Delaware, Nevada, and Wyoming, “Encouraging Business While Fighting Fraud: States Focus on Changes Made and Changes to Consider,” White Paper Prepared for the National Association of the Secretaries of State Business Services Committee and Company Formation Task Force, July 2013. http://nvsos.gov/sos/home/showdocument?id=2800

[xx] Advantage Delaware, LLC, “Why Incorporate in Delaware?” https://www.advantage-de.com/information-center/reasons-corp-choice/#

[xxi] Secretaries of State of Delaware, Nevada, and Wyoming, “Encouraging Business While Fighting Fraud: States Focus on Changes Made and Changes to Consider,” White Paper Prepared for the National Association of the Secretaries of State Business Services Committee and Company Formation Task Force, July 2013. http://nvsos.gov/sos/home/showdocument?id=2800

[xxii] Global Financial Integrity, “Delaware Bills ‘Mere Window-Dressing’, Will Do Nothing to Curb Abuse of Anonymous Companies,” June 10, 2014. http://www.gfintegrity.org/press-release/delaware-bills-mere-window-dressing-will-nothing-curb-abuse-anonymous-companies/

[xxiii] Financial Action Task Force, “International Standards on Combating Money Laundering and the Financing of Terrorism & Proliferation – The FATF Recommendations,” February 2012. http://www.fatf-gafi.org/media/fatf/documents/recommendations/pdfs/FATF_Recommendations.pdf

[xxiv] Michael Findley, Daniel Nielson, and Jason Sharman, “Global Shell Games: Testing Money Launderers’ and Terrorist Financiers’ Access to Shell Companies,” 2012. https://www.griffith.edu.au/__data/assets/pdf_file/0008/454625/Oct2012-Global-Shell-Games.Media-Summary.10Oct12.pdf

[xxv] Findley, Michael G., and Daniel L. Nielson. Global Shell Games: Experiments in Transnational Relations, Crime, and Terrorism. March 2014.

[xxvi] Mihai Munteanu, “Kiss: Hiding Ownership Offshore,” Organized Crime and Corruption Reporting Project, November 20, 2010. https://www.reportingproject.net/offshore/index.php/kiss-how-to-hide-ownership

[xxvii] Mihai Munteanu, “Kiss: Police Arrest Kiss,” Organized Crime and Corruption Reporting Project, November 20, 2010. https://www.reportingproject.net/offshore/index.php/kiss-the-downfall-and-arrest-of-kiss; Mihai Munteanu, “Laszlo Kiss: The Offshore Master,” Organized Crime and Corruption Reporting Project, November 20, 2010. https://www.reportingproject.net/offshore/index.php/laszlo-kiss-undercover-with-a-master

[xxviii] Charles F. Barnwell, Jr., “Addback: It’s Payback Time,” State Tax Notes, November 17, 2008.

[xxix] For a more detailed look at combined reporting see Institute on Taxation and Economic Policy “Combined Reporting of State Corporate Income Taxes: A Primer,” August 1, 2011. https://itep.org/itep_reports/2011/08/combined-reporting-of-state-corporate-income-taxes-a-primer.php#.VdS5frJViko

[xxx] Scott D. Dyreng, Bradley P. Lindsey, and Jacob R. Thornock, “Exploring the Role Delaware Plays as a Domestic Tax Haven,” September 2012. http://ssrn.com/abstract=1737937

[xxxi] Americans for Democratic Action, Delaware Chapter, “Joint Legislator Letter re: Anonymous Companies Delivered to Congressional Delegation,” July 24, 2014. http://delawareada.org/2014/07/24/jointlegislatoritleaaletter/