See the 2016 Updated Brief Here

Read this Policy Brief in PDF Form

Low- and middle-income working parents frequently spend a significant portion of their income on child care. As an increasing number of single parents take jobs, and as the number of two-earner families continues to rise, child care expenses are an unavoidable and increasingly unaffordable expense for these families. This policy brief looks at one way of making child care more affordable: the dependent care tax credit offered by the federal government and many states.

How the Federal Dependent Care Credit Works

The federal government allows an income tax credit to help off set childcare expenses. In 2010, single working parents (and two-earner married couples) with children under 14 could claim a credit to partially off set up to $6,000 of child care expenses. Low-income taxpayers can receive a credit of up to 35 percent of these expenses. In 2010, this meant a maximum credit of $2,100. The credit percentage gradually falls from 35 to 20 percent of expenses for higher-income taxpayers. Taxpayers with incomes over $43,000 can claim the minimum credit of 20 percent of child care expenses. This “sliding scale” approach helps to target tax relief somewhat more effectively to low-income taxpayers, although the credit is available to even the wealthiest taxpayers.

Options for State Dependent Care Tax Relief

More than half of the states now offer some form of state income tax break for families with dependent care expenses. This section looks at the various approaches states have taken—and assesses the usefulness of each approach in reducing the cost of low-income child care.

More than half of the states now offer some form of state income tax break for families with dependent care expenses. This section looks at the various approaches states have taken—and assesses the usefulness of each approach in reducing the cost of low-income child care.

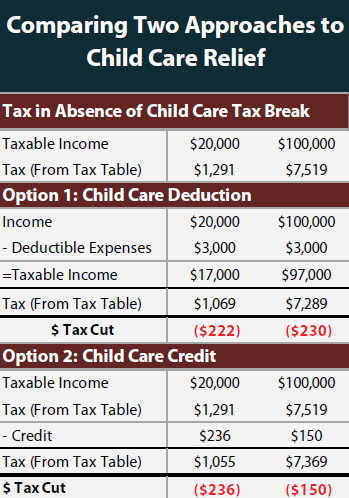

The most basic choice to make in implementing dependent care tax relief is between a tax credit and a tax deduction. Almost all of the states that currently provide dependent care tax breaks use tax credits, which reduce taxes on a dollar-for-dollar basis. However, a few states allow income tax deductions for child care expenses. Deductions reduce taxable income on a dollar-for-dollar basis. In states with graduated income taxes (that is, income taxes that apply higher rates to higher-income taxpayers), deductions will be a better deal for wealthier taxpayers than for low-income parents. As shown in the hypothetical examples below, a $3,000 child care deduction will be worth slightly more to a family earning $100,000 than to a family earning $20,000, while a tax credit based on the federal “sliding scale” rules will give a larger tax break to the lower-income family than to the wealthier taxpayer.

Lawmakers must also choose whether to impose income eligibility limits. While the federal credit is available to taxpayers at all income levels, some states have chosen to restrict their credits to low- and middle-income taxpayers. Ten states currently have such an income limit, ranging from $30,160 in New Mexico to $100,000 in California and Oklahoma. By imposing income limits, states can reduce the cost of dependent care tax relief while targeting the benefits to those lower- and middle-income taxpayers for whom child care expenses are most burdensome.

As noted above, all states with child care credits use a “sliding scale,” modeled after the federal credit, that gives lower-income families a larger credit. But some states take additional steps to target tax relief more precisely to low-income families. For example, the Nebraska credit is calculated as 100 percent of the federal credit at low income levels and 25 percent of the federal credit at higher income levels. This approach targets the benefits of the Nebraska credit much more efficiently to low- and middle-income parents than does the federal credit.

For states allowing tax credits, possibly the most important policy choice is whether the credit should be refundable or nonrefundable. A non-refundable tax credit can only be used to reduce income taxes to zero. A refundable credit, by contrast, does not depend on the amount of income taxes paid: if the credit amount exceeds your income tax liability, the excess amount is given as a refund. Refundability is an especially valuable feature in state credits for two reasons: first, low-income parents with substantial child care expenses and little or no income tax liability will receive little or no benefit from a non-refundable credit, and second, the non-refundability of the federal child care credit means that the state credit may be the only tax relief available for these families.

States must also decide whether to preserve the real value of these tax breaks by tying their value to inflation (See ITEP Brief, “Indexing Income Taxes for Inflation: Why It Matters” for more information). The impact of inflation means that (for example) the maximum $2,100 federal credit is worth slightly less every year. This problem affects both the income eligibility limits and the maximum credit amount. Very few states have taken steps to avoid this problem—which means that the value of this credit in reducing the cost of child care falls every year.

Are Tax Breaks the Best Approach to Making Child Care Affordable?

Income tax breaks for dependent care are now an established practice. A majority of states now follow the federal government’s lead in providing income tax credits or deductions to make child care more affordable. As this policy brief has noted, some states do a better job than others in targeting this tax relief to the low- and middle-income taxpayers for whom child care represents a substantial expense. States seeking to provide targeted dependent care relief can do this most effectively by enacting a refundable tax credit with relatively low income limits.

However, even the best designed tax credit may not be an appropriate way to reduce child care costs. Even the most generous credits can be claimed only when income taxes are filed—often long after the costs of child care are incurred. Moreover, reducing the cost of child care is only one of many spending priorities that the public may favor. By enshrining these tax breaks in the tax code, lawmakers grant child care subsidies an unfair advantage in the annual scramble for adequate funding. A more even-handed and timely approach to reducing the cost of child care would be to provide direct subsidies to families incurring these costs, and to determine the appropriate amount of state funding for these subsidies as part of the regular budget process.