Sen. Susan Collins (R-ME) indicated that she will not vote for the tax bill being debated in the Senate unless it is amended to include a deduction for up to $10,000 in annual property taxes, similar to what the House included in the bill it passed last month. Currently, the Senate bill would end the ability of individuals to write-off any of their state and local income, sales, and property taxes.

Adding a property tax deduction back into the Senate bill may sound like a reasonable compromise, but a new analysis performed using the ITEP Microsimulation Tax Model reveals that the amount of state and local taxes deducted by Maine residents would plummet by 90 percent under this change, from $2.58 billion to just $262 million in 2019. In short, this change is much more symbolic than substantive.

Among ITEP’s other findings:

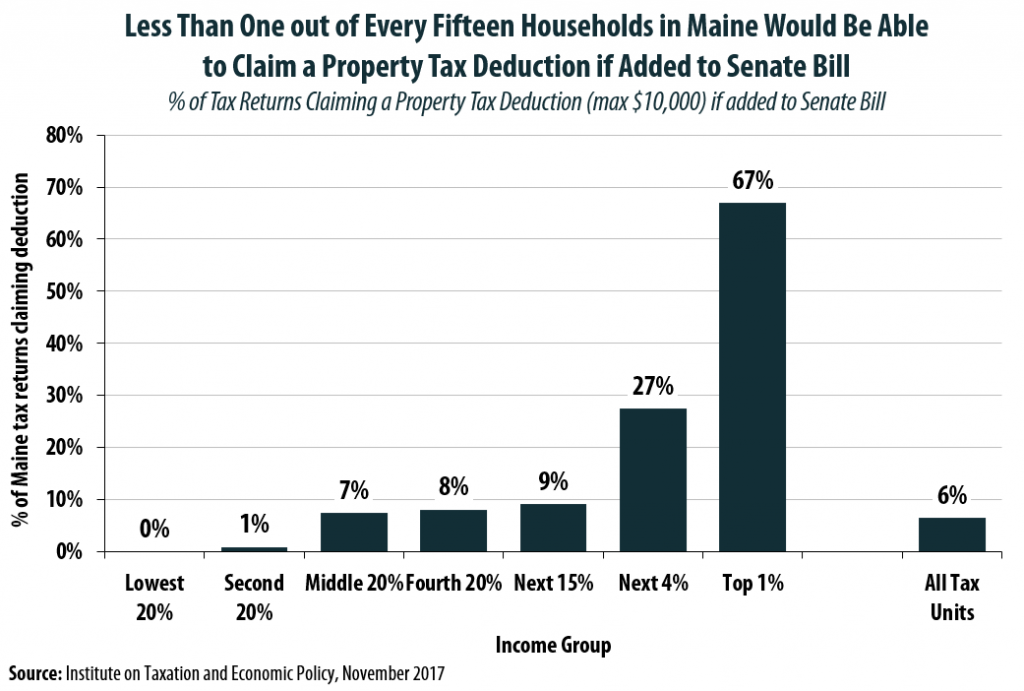

- Very few Mainers would benefit from a $10,000 property tax deduction under the type of tax code envisioned in the Senate bill. Less than 1 in 15 households (6.4 percent) would receive a property tax deduction in this scenario.

- Three out of every four Maine households deducting their property taxes today would lose the deduction. While 173,000 households in Maine are expected to deduct their property taxes in 2019 under current law, that figure would fall to just 44,000 under a version of the Senate bill in which a $10,000 property tax deduction is left in place.

- Higher-income Mainers are disproportionately likely to be able to use the type of deduction proposed by Sen. Collins. Two-thirds (67 percent) of the top 1 percent of Maine earners, for instance, would deduct at least a portion of their property tax bills under this policy.

- Among middle-income Mainers, just 7 percent of households would receive any benefit from this deduction.

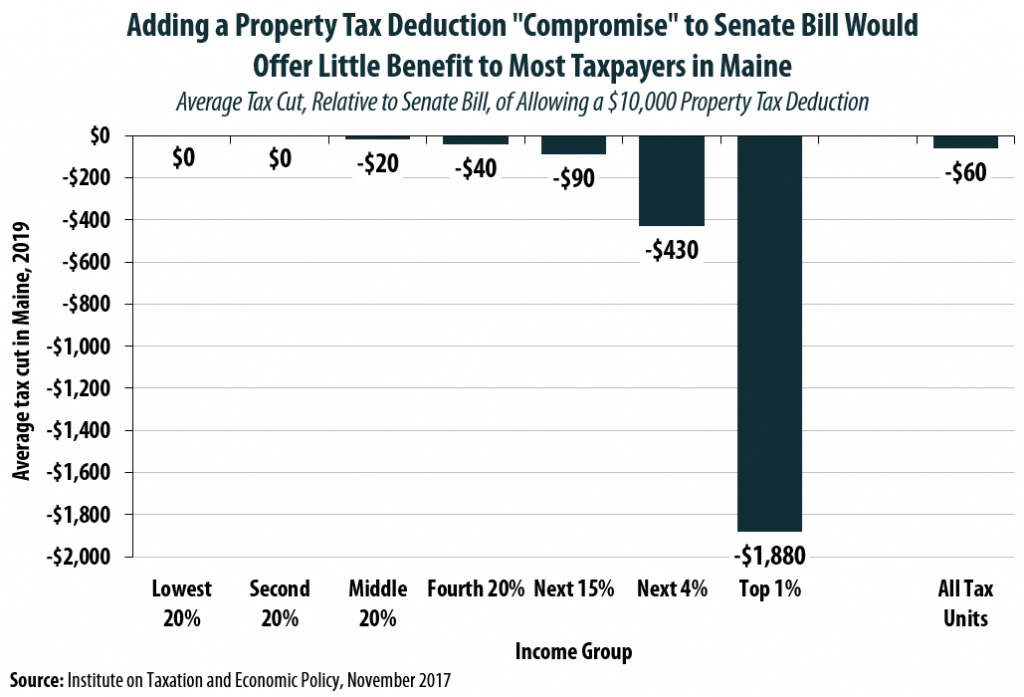

- Because so few Mainers would be able to use the deduction, the average benefit to households in Maine would be exceedingly small, at just $60 per year. And even this modest figure is skewed upward by the average tax cut of $1,880 that high-income Mainers could expect to receive. For middle-income families, the average benefit would be just $20 per year.

- Even looking just at the small fraction of Mainers able to claim a property tax deduction in this scenario, the average benefit for middle-income earners would amount to just $270 per year—or $23 per month. Meanwhile, for high-income Mainers able to use such a deduction, the average benefit would be $2,810 annually, or $234 per month.

Under the Senate bill, many taxpayers would find that, without the ability to deduct their state income tax payments, they would not have enough ‘itemized deductions’ left to warrant itemizing. Others would find that the enhanced standard deduction proposed by the Senate would exceed their itemized deductions—though the benefits of this change would be blunted by the repeal of personal exemptions.

The complicated reshuffling of tax breaks proposed in the Senate bill can make it difficult for ordinary taxpayers, and their elected officials, to understand how any single change might impact them. While a $10,000 property tax deduction might sound like a good deal relative to full repeal of the deduction for state and local taxes, the reality is that interactions with other components of the bill would render the deduction useless for the vast majority of taxpayers.