Carl Davis

Research Director, Institute on Taxation and Economic Policy

Thank you for the opportunity to speak today. My name is Carl Davis and I am the Research Director at the non-partisan Institute on Taxation and Economic Policy, or ITEP. We are a research group that works on both federal and state tax policy issues, including the areas where they intersect such as the one we’re discussing right now.

ITEP views this proposal as a sensible improvement, and one that is actually overdue, to the way the charitable deduction is administered. At the end of my remarks I will discuss a few ways that the regulation could be improved. But the core point I want to emphasize is that the general approach taken here, where quid pro quo rules are applied in a broad-based fashion to all significant state and local tax credits, is the correct one.

Recommendation 1: Reject Requests for a Carveout

Many of today’s commenters are here to ask for special exceptions from this regulation, either for tax credits that existed before 2018 or for programs benefiting private charities. It is enormously important that those requests for special treatment be rejected. Fair and effective administration of the tax law demands that this regulation be applied broadly, not in a scattershot fashion.

ITEP opposes carveouts for any charitable credit above the 15 percent de minimis threshold. But in my remarks today I’m going to focus largely on tax credits for donations that support private K-12 scholarships, also known as school vouchers. Among the preexisting credits, those private school programs tend to offer the highest reimbursement percentages and are therefore among the most problematic as SALT cap workarounds.

My written comments explained in detail how two-thirds of existing private school voucher tax credits can — and will — be used for SALT cap avoidance unless this regulation is implemented. This is not a small or isolated issue. A dozen states are offering hundreds of millions of dollars in high-percentage private school tax credits that can be used to circumvent the SALT cap – and the size of these credits is growing every year.

Some of the private school groups seeking special treatment are insisting that their credits couldn’t possibly be viewed as SALT cap workarounds because they were enacted before the SALT cap was even created. This narrative is misleading.

Limitations on the SALT deduction, and avoidance of those limitations via state tax credits, is nothing new. Previously, this avoidance was confined largely to the Alternative Minimum Tax – or AMT.

In my written comments I explained that South Carolina lawmakers knew that their credit was being used to avoid SALT deduction limits under the AMT as far back as 2013, and yet did nothing to prevent it. Those comments also walk through a similar story in New Hampshire, which expanded its private school credit this year despite significant publicity around the federal tax shelter it facilitated.

Rather than retell those stories here, I’m going to focus on Georgia because some important new data on that state’s credit were released just one week ago.

According to researchers at Georgia State University who have access to official Department of Revenue data, nearly one in five dollars paid out under the state’s private school voucher tax credit in 2015 went to AMT payers – meaning taxpayers that would have received a federal tax cut on top of their 100 percent state tax credit, and therefore would have come out ahead on their so-called “donations.”

These data confirm the claims of a financial planner who wrote that the credit enjoyed “a loyal base of high income parents who benefitted from the AMT tax savings.”

And the data also suggest that the aggressive advertisements pushed by private schools and accountants in Georgia were effective. In Georgia and around the country, we’ve extensively documented instances where words like “profit” and “make money” were used to describe the fact that AMT payers were receiving tax cuts larger than their donations.

And to be frank with you, Georgia is far from being the worst-case scenario here. In Georgia, the credit is capped at $2,500 per individual, meaning that the tax rewards of donating max out at a few hundred dollars per year for individuals.

That’s not the case in Louisiana, or Alabama, or New Hampshire, or South Carolina, or Pennsylvania, or various other states where there is either no cap, or there is a very high cap, on tax-credit-eligible donations per taxpayer. In these states, very-high-income taxpayers who are guaranteed to face the SALT cap can transform massive amounts of nondeductible SALT payments into deductible charitable contributions by using these credits unless this regulation is implemented.

Louisiana’s credit is particularly noteworthy. That state offers a 95 percent tax credit for donations to fund private K-12 school vouchers, and there is no cap at either the taxpayer level or the statewide level. Simply put, a taxpayer interested only in tax avoidance would much rather have access to Louisiana’s 95 percent private school credit than to New York’s brand-new 85 percent credit for public school donations.

Viewed through the eyes of taxpayers, the Louisiana credit that some of today’s commenters would like to see given a free pass is unquestionably the more powerful tool for avoiding the SALT deduction cap.

Viewed through the eyes of state lawmakers, both programs are efforts to steer state funding toward the education of children. In Louisiana that education happens to be taking place in private and religious schools. In New York it’s happening in local public-school districts. But the fact remains that these are both K-12 education programs and treating the Louisiana program more favorably, simply because it outsources teaching responsibilities to private schools, would be a mistake and would offer a wide-open avenue for even more states to begin facilitating SALT cap avoidance.

Given all the attention that this regulation has received, if a carveout for private school voucher credits is added to this regulation there is no doubt that many of these state credits – including existing ones and ones yet to come – will become immensely popular as SALT cap workarounds. We’ve already seen evidence of this in Arizona, for example, where a credit that took 6-months to reach its statewide cap last year lasted all of 2 minutes – literally 2 minutes – this year after the SALT cap was implemented and private school groups began describing the federal tax avoidance benefits on local TV news programs and elsewhere.

Given that the goal of this project is to end the use of state and local charitable tax credits as ways to dodge the $10,000 SALT deduction cap, it is essential that these types of preexisting programs be included within the regulation’s scope.

We know that these credits were used to dodge SALT limits under the AMT for many years.

We know that these credits were used to dodge the new $10,000 SALT deduction cap during the first half of 2018.

And we know that they will become even more popular as SALT cap dodges in the years ahead unless this regulation puts a stop to it.

With my last couple minutes, I’ll just briefly outline the other recommendations from my written comments.

Recommendation 2: End Tax Avoidance by Investors Who Donate Appreciated Property in Exchange for Tax Credits

My second recommendation is that the regulation should clarify that taxpayers donating appreciated property in exchange for large tax credits must recognize a gain.

Several states with private school voucher credits allow taxpayers to receive state tax credits on donations of property, including marketable securities.

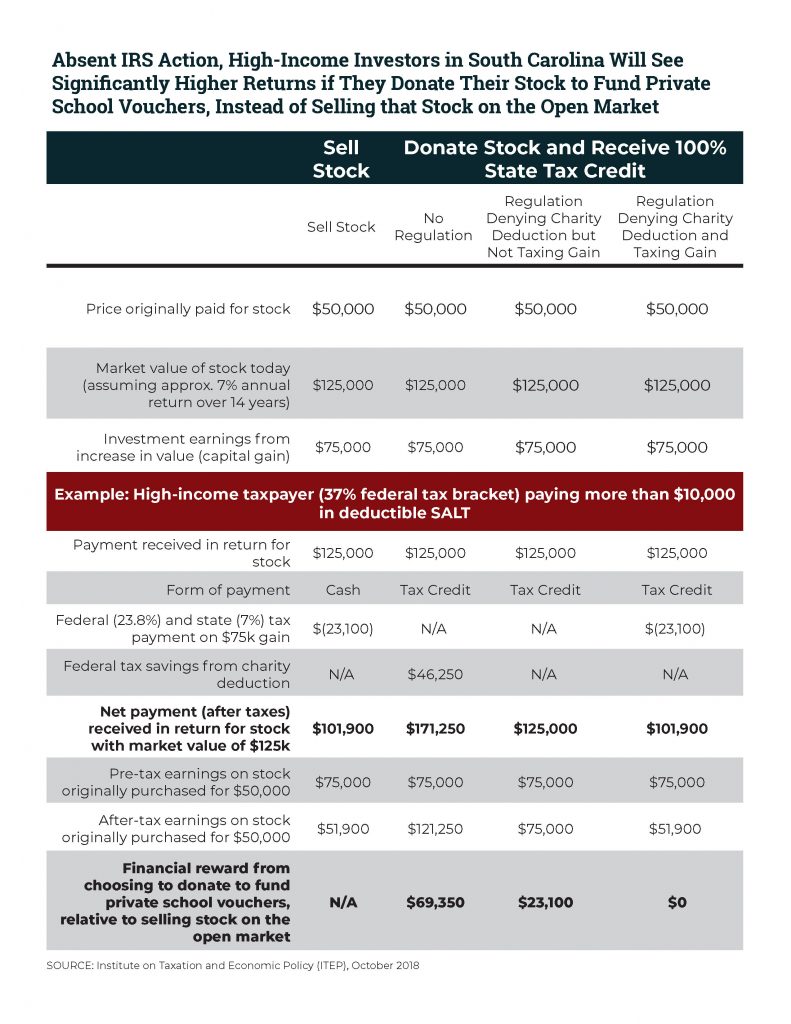

In South Carolina this is especially problematic because an investor can receive a 100 percent tax credit for their donation of appreciated property, meaning that their state government will effectively pay them the same price that they could have received by selling on the open market. The key difference, though, is if South Carolina’s government pays for the stock with tax credits, then depending on the outcome of this regulation, there might not be a taxable gain.

My written comments walk through an example in which a high-income investor would come out ahead by $23,000 by agreeing to donate stock under the state’s credit program. That’s relative to simply selling the stock. And that even assumes that this regulation is implemented without a carveout, and that the donation therefore doesn’t trigger a section 170 charitable deduction.

Unless the regulation requires recognition of gain, we’ll be left with a hugely distortionary policy where investors seeking to make the best financial move for their own families will be forced to donate stock under state tax credit programs rather than simply sell the stock on the open market.

Recommendation 3: Revisit Stacking of State Tax Credits and Business Expense Deductions

My third recommendation is that additional scrutiny be given to businesses that seek to combine state tax credits and federal business expense deductions to yield tax rewards larger than the amounts contributed to public or private charities.

The IRS’s September 5th clarification for business taxpayers has been widely interpreted as allowing pass-through businesses to use state and local tax credits as tools to convert nondeductible SALT payments into deductible business expenses.

Some firms have even begun to discuss how credit programs could be modified to make it easier for contributing businesses to secure a business expense deduction, such as through public advertising of the contributions being made.

There is significant uncertainty surrounding this aspect of the federal tax code’s treatment of contributions benefiting from state tax credits. I urge you to give more consideration to the business expense deduction in this context, with an eye toward ensuring that businesses contributing to state tax credit programs cannot reap a net positive financial return because of the tax rewards alone.

Recommendation 4: Apply Third Party Quid Pro Quo Rules More Broadly

My fourth and final recommendation is to adopt an excellent suggestion made by Professor Larry Zelenak of Duke University, who noted that the regulation may be on stronger legal footing if it considers third-party benefits of all forms to be potential quid pro quos, rather than treating them as such only when they take the form of tax credits. There is no mandate either in statute or from the courts that third party benefits must be ignored by the IRS when determining what constitutes a quid pro quo. Because of this, it is more sensible to begin considering third party benefits in general rather than only considering those benefits when they take the form of tax credits.

Conclusion

In sum, this regulation would represent a major improvement over the status quo, particularly because it takes a broad approach to state and local tax credits. There are certain refinements that should be made to improve the regulation’s consistency and to close down related tax shelters, but these changes can be made while keeping the broad outlines of the proposed regulation very much intact.

And with that I’ll conclude my remarks. Thank you for your time.

************************

Mr. Davis’s written comments, which provide more detail and citations, are available online at:

https://itep.org/itep-comments-reg-112176-18/