President Biden’s proposal to eliminate the lower income tax rate on capital gains (profits from selling assets) and stock dividends for millionaires would affect less than half of 1 percent (0.4 percent) of U.S. taxpayers if it goes into effect in 2022. The share of taxpayers affected would be less than 1 percent in every state.

The capital gains and stock dividend income subject to the tax increase (all of which goes to millionaires) would account for around 5 percent of total adjusted gross income (AGI) in the United States in 2022. This varies from a low of less than 2 percent in North Dakota, Iowa, Mississippi, Alaska, and West Virginia to a high of more than 7 percent in Massachusetts, Connecticut, New York, Florida, Nevada and Wyoming.

ITEP produced these figures with its microsimulation model.[1] Because this data requires unusually specific estimates (about specific types of income going to millionaires in each state), this report provides an appendix demonstrating that rough calculations using IRS data lead to essentially the same conclusions.

Whereas ITEP’s previous analysis examined the changes for ordinary income and capital gains and dividends in combination, this analysis focuses solely on the rate change for capital gains and stock dividends and therefore finds a smaller share of taxpayers affected.

Background

The two most prominent parts of the president’s plan to raise taxes on individuals are his proposals to restore the top personal income tax rate to 39.6 percent and end breaks in the personal income tax for capital gains and stock dividends going to millionaires.[2]

The first of these proposals would return the top income tax rate on what our tax laws call “ordinary” income to 39.6 percent, the rate that applied before the Trump tax law was enacted at the end of 2017 and reduced it to 37 percent.

The second of these proposals would end (for millionaires) tax breaks related to capital gains and stock dividends. This itself has two parts. One would address the tax break that privileges these types of income over “ordinary” income by subjecting them to lower income tax rates, with a top rate of just 20 percent. Biden proposes to end this break (but only for millionaires), and this is the focus of this report. (The other part of this proposal would address the break that exempts capital gains exceeding $1 million on assets left to heirs, which would not affect even the wealthiest families in most years.[3])

The lower income tax rate for capital gains and stock dividends is one reason very high-income individuals in the United States sometimes pay lower effective tax rates than middle-income families that work for their income.

To qualify for the lower income tax rates, a capital gain must be a long-term capital gain, which (according to the tax law) means the taxpayer owned the asset for at least a year before selling it. Short-term capital gains, which are a fraction of total capital gains in any year, are taxed as ordinary income.

To qualify for the lower income tax rates, a stock dividend must be a qualified dividend, meaning it meets certain requirements. Most dividends distributed by U.S. corporations are qualified dividends for shareholders who have held stock for a certain period. Dividends paid by real estate investment trusts, partnerships, tax-exempt companies and dividends paid on money market accounts are usually nonqualified, meaning they are taxed as ordinary income.

The president’s plan would increase the top rate for taxable income in excess of $1 million that is long-term capital gains or qualified stock dividends from 20 percent to 39.6 percent. As we understand the proposal, even those with taxable income exceeding $1 million would not pay higher taxes on any capital gains and dividends that account for some or all of their first $1 million of taxable income.[4]

As explained in our previous report, the revenue raised from increased taxes on capital gains can be restricted to some degree by behavioral effects, meaning the ways that high-income individuals respond to a change in tax law to partly avoid a tax increase. As explained in our previous report, the proposal would raise revenue despite these behavioral effects. The figures presented in this report concern the distribution of the tax increase rather than its revenue impact and therefore does not account for behavioral effects, following the standard practice of Congress’s official revenue estimators and analysts.

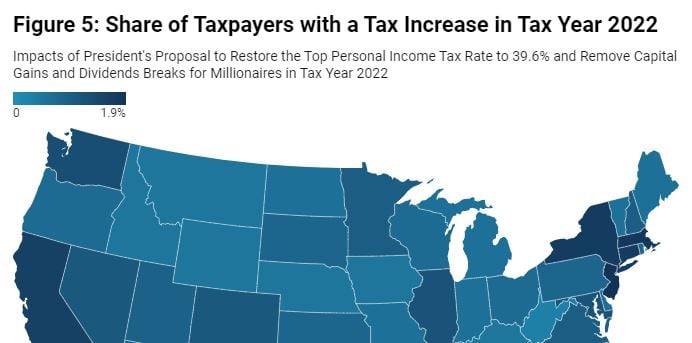

Rate Increase on Capital Gains and Dividends Affects Less than 1 Percent in Every State

Using ITEP’s microsimulation model, we project that just 0.4 percent of taxpayers in the United States would be subject to the income tax rate increase (from 20 percent to 39.6 percent) on capital gains and stock dividends under the president’s plan in 2022.

As illustrated in Figure 1, the states most affected by this proposal are New Jersey, Connecticut and Massachusetts, each with 0.7 percent of their taxpayers facing increased taxes. West Virginia, Mississippi, New Mexico and Hawai’i are the states least affected, each with just 0.1 percent of their taxpayers facing increased taxes.

A Small Share of Income Is Affected in Most, But Not All, States

The share of taxpayers facing a tax increase is one way to think about how each state is affected. Another is the share of the state’s income that is made up of the type of income subject to a tax increase.

Using the ITEP model, we project that just 5.3 percent of the total adjusted gross income (AGI) in the United States would be subject to this tax increase. In other words, just 5.3 percent of AGI in the U.S. is long-term capital gains or qualified dividends that is taxed at a rate of 20 percent under current law but would be taxed at a rate of 39.6 percent under the president’s plan. (As already explained, all of this is income going to those with taxable income of more than $1 million.)

In most states, the share of AGI subject to the tax increase is similarly low, with the smallest share (1.2 percent) in West Virginia. However, in three states, Florida, Nevada, and Wyoming, around 10 percent of total AGI is subject to the tax increase, as illustrated in Figure 2.

These three states apparently have a great deal of inequality so that a particularly large portion of total income in these states is going to millionaires who are mostly paying personal income taxes at a rate of just 20 percent, a lower rate than many pay on their earned income.

APPENDIX

Simple calculations using IRS data come to roughly the same conclusions as our analysis using the ITEP model. This is expected given that the data used by the ITEP model is updated annually to ensure that it reflects the most recent state-by-state IRS data. ITEP uses the Congressional Budget Office’s projections of growth of different types of income to estimate how taxpayers’ income grows in years beyond those covered by the IRS data. The result is that ITEP’s projections are never far off from what one would expect after examining the IRS data. The comparisons provided in this appendix are nevertheless helpful as a simple way to demonstrate how ITEP’s projections line up with publicly available data.

The most recent IRS Statistics of Income (SOI) data broken down by state are for 2018. The number of taxpayers with adjusted gross income (AGI) exceeding $1 million who also have some capital gain or loss could be used as a rough proxy for the number of taxpayers who could face a tax increase in the U.S. and in each state. As illustrated in Figure 3 below, this calculation comes to a very similar conclusion as the ITEP tax model’s projections for the share of taxpayers facing a tax increase from this proposal in 2022.

For example, using ITEP’s tax model we find that 0.4 percent of taxpayers in the US would pay more under this proposal. The share of taxpayers with more than $1 million of AGI who have capital gains or losses in 2018 was 0.3 percent in 2018 according to the IRS SOI data. The figures are similar for each state, as shown in Figure 3.

Of course, this comparison is not perfect. The share of taxpayers in each state with AGI exceeding $1 million who also have capital gains or losses is not exactly the same thing as the share of taxpayers affected by this proposal. The capital gains that are taxed at the lower rate under current law, and that are taxed more under this proposal, are long-term capital gains, defined as gains on assets held for at least a year. A fraction of the capital gains reported in the IRS SOI data for millionaires in each state are short-term capital gains which are not affected by this proposal. Also, capital gains are not the only type of income affected by this proposal—qualified stock dividends are affected as well, although in much smaller amounts. Taxpayers in the IRS SOI data with AGI exceeding $1 million do not all have taxable income exceeding $1 million.

And yet, despite flaws in this rough comparison, the simple calculation using IRS SOI data comes to roughly the same conclusions as the ITEP tax model projections for 2022. For example, using either approach leads to the conclusion that the largest share of taxpayers affected are in California, Connecticut, the District of Columbia, Massachusetts, New Jersey and New York.

The IRS SOI data can also be used to roughly verify our calculation of the income subject to the tax increase in the U.S. and in each state. Figure 4 compares the share of AGI subject to the tax increase according to ITEP’s model in 2022 to the share of AGI that is capital gains going to taxpayers with AGI exceeding $1 million in 2018 according to the IRS SOI data.

Again, this comparison is imperfect. Not all the capital gains going to millionaires in the IRS data would be subject to the tax increase. Some is short-term capital gains and some is taxable income below the $1 million threshold. And capital gains income is not the only income subject to the tax increase.

Nonetheless, this comparison again comes to generally the same conclusions as we do with the ITEP tax model. As illustrated in Figure 4, the least affected state by this measure is West Virginia, and the three most affected states are Florida, Nevada and Wyoming.

[1] ITEP Microsimulation Tax Model Overview. https://www.itep.org/itep-tax-model/

[2] Steve Wamhoff and Matthew Gardner, “Income Tax Increases in the President’s American Families Plan,” April 29, 2021. https://itep.org/income-tax-increases-in-the-presidents-american-families-plan/

[3] Under current law, the personal income tax excludes capital gains on assets left to heirs, which is a subsidy provided through the tax code for families that pass appreciated assets from one generation to the next. The president would end this break only for gains exceeding $1 million ($2 million for married couples) on assets left to heirs. For more detail, see Steve Wamhoff and Matthew Gardner, “Income Tax Increases in the President’s American Families Plan,” April 29, 2021. https://itep.org/income-tax-increases-in-the-presidents-american-families-plan/

[4] For example, a taxpayer with taxable income made up of $500,000 of ordinary income and $1.5 million of long-term capital gains and qualified dividends would have $1 million of income subject to the tax increase proposed by the president.