New York Rep. Alexandria Ocasio-Cortez’s recent suggestion that individual income exceeding $10 million should be taxed at a rate of 70 percent has inspired outrage among anti-tax lawmakers and activists. Their responses vary from oversimplifying her suggestion to pretending a 70 percent top marginal rate would affect people struggling to get by.

The uproar deliberately steers clear of any real policy discussion about what a significantly higher marginal tax rate would mean. Her critics are mostly the same lawmakers who enacted a massive tax cut for the rich last year that was not debated seriously or supported by serious research. Meanwhile, multiple scholarly studies conclude a 70 percent top tax rate would be an optimal way to tax the very rich. Ocasio-Cortez has brought more attention to the very real need to raise revenue and do it in a progressive way.

Let’s Start with a Reminder About How Marginal Tax Rates Work

Most of the racket over Ocasio-Cortez’s proposal is ridiculous on its face. For example, Rep. Steve Scalise (R-LA) tweeted that Democrats want to “[t]ake away 70% of your income and give it to leftist fantasy programs,” to which Ocasio-Cortez replied, “You’re the GOP Minority Whip. How do you not know how marginal tax rates work?”

Good question. The top marginal income tax rate applies only to income in the top tax bracket, which, under the approach Ocasio-Cortez describes, would only consist of taxable income exceeding $10 million. The proposal would not affect taxpayers with income less than $10 million. A taxpayer with income of, say, $10.1 million would have $100,000 of taxable income in the top bracket and pay 70 percent of it, or $70,000, in income tax (as opposed to $37,000 under the current top rate of 37 percent). The rest of the taxpayer’s income would be subject to lower marginal rates.

Someone with taxable income of $10.1 million typically has a much higher total income because taxable income is total income minus deductions. Most rich people claim significant deductions.

In contrast with marginal tax rates, the effective tax rate is tax liability as a percentage of income. Let’s assume this proposal was in effect in 2018 and that a married couple had taxable income of $10.1 million that year. Let’s keep things simple by assuming the taxpayer claims only the standard deduction and has no other tax breaks. So, the household’s 2018 income is $10,124,000, and they claim a standard deduction of $24,000, leaving them with taxable income of $10.1 million. (In real life, most millionaires claim significant deductions and thus taxable income would be much smaller than total income.)

Under current law, the taxpayer’s federal income tax is $3,676,379, which is 36.3 percent of her total income. If Congress enacted the top marginal rate of 70 percent but made no other changes to the tax code, the taxpayer would pay $33,000 more, or $3,709,379, which would be 36.6 percent of her total income. In other words, this proposal would boost her effective tax rate from 36.3 percent to 36.6 percent.

We Need Higher Effective Tax Rates, Not Just Higher Statutory Tax Rates, for the Rich

Most people with more than $10 million in income currently pay effective tax rates that are much lower than 36 percent because of all the special breaks and loopholes they can use. Ocasio-Cortez did not suggest that a high marginal tax rate on the very rich would, by itself, fix our tax system, and I would strongly caution anyone against thinking that alone would be sufficient. In fact, if we don’t solve the other problems with our tax code, a higher marginal tax rate on the rich simply will not work because they will be able to use loopholes and special breaks to avoid it and keep their effective tax rates low.

High-income individuals behave like corporations. Both have the resources to arrange their affairs to exploit whatever loopholes or special breaks are available to them. The top statutory income tax rate for corporations was, until 2018, 35 percent, but few corporations paid 35 percent of their profits in federal income taxes. (ITEP found Fortune 500 corporations that were consistently profitable from 2008 through 2015 paid an average effective rate of 21 percent during that period, and several paid nothing.)

Similarly, until 2018, the top statutory income tax rate for individuals was 39.6 percent, but few rich people paid even close to 39.6 percent of their income in federal income taxes. The IRS reported that the richest 400 taxpayers paid an effective tax rate of just 23 percent in 2014. This is especially striking given that the vast, vast majority of their taxable income would likely be in the top income tax bracket.

The Special Breaks and Loopholes

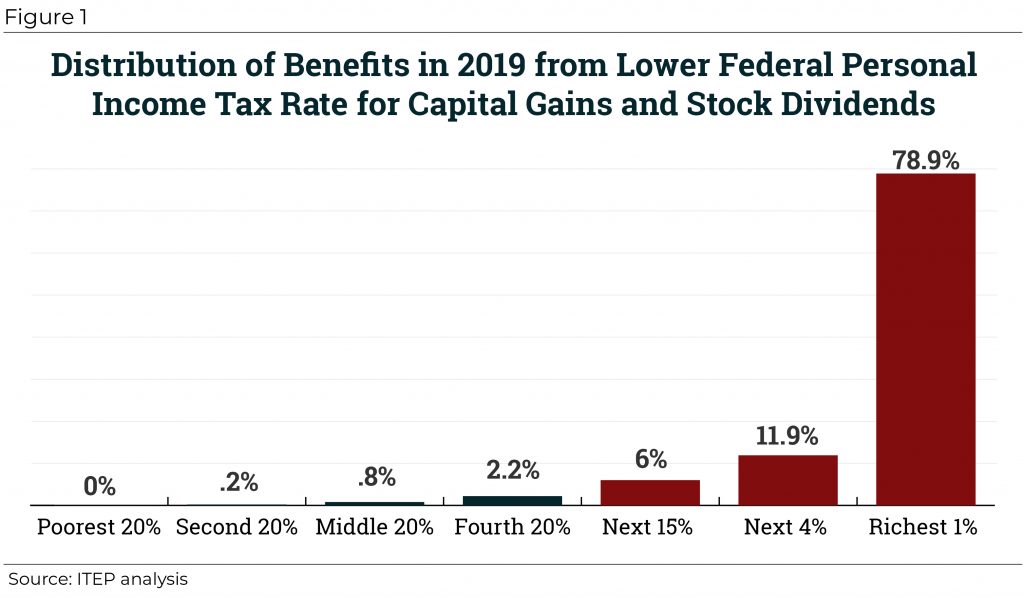

One way that high-income individuals pull this off is by using several breaks for income in the form of capital gains. The most familiar is the lower income tax rates that apply to capital gains and stock dividends. Another is the rule that exempts any capital gains on assets that are left to heirs.

If Congress imposed a top marginal rate of 70 percent but left in place special rates and other breaks for capital gains, then wealthy people could avoid the tax increase by using schemes to characterize more of their income as capital gains. A recent ITEP paper explains what Congress needs to do to shut down these breaks.

Another special break Congress needs to shut down is the 20 percent deduction for income from pass-through businesses (businesses not subject to the corporate income tax) that was enacted as part of the Tax Cuts and Jobs Act (TCJA). Congress can also find a way to limit the numerous itemized deductions in the code that disproportionately benefit the wealthy. (An ITEP report explores ways to do this that would be fairer than TCJA’s $10,000 cap on deductions for state and local taxes.)

The details may seem arcane, but reforms of this sort would raise significant revenue, and the vast majority of it would come from income that the richest 1 percent of taxpayers currently shields from taxation. A real tax reform plan would include these changes, which experts refer to as “base broadening.” Once lawmakers understand how far they can go in raising revenue in this way, they can figure out what exactly the tax rates should be, given that they have eliminated the ability of rich people to circumvent tax increases.

This is born out in some of the scholarly research that supports the type of tax rate Ocasio-Cortez is talking about. For example, a 2014 paper from Thomas Piketty, Emmanuel Saez and Stefanie Stantcheva concluded that the optimal marginal tax rate for the very rich would be 71 percent. But that assumed base-broadening measures like eliminating the preferential rates for capital gains.

Tax experts may debate what is the optimal top tax rate on various types of income. For example, government analysts have believed that the revenue-maximizing rate for capital gains was somewhere around 28 to 32 percent, meaning rates higher than that would lead to so much tax avoidance that revenue would actually fall. But, as explained in the ITEP paper on capital gains, this assumes Congress leaves in place all the avenues that rich people have right now to avoid paying higher rates on capital gains (like the rule exempting gains on assets left to heirs). The revenue-maximizing rate or optimal top rate on various types of income will be much higher once such special breaks and loopholes are closed.

The debate about optimal top tax rates may be a long one, but it is a debate worth having given the importance of raising revenue in a progressive way.