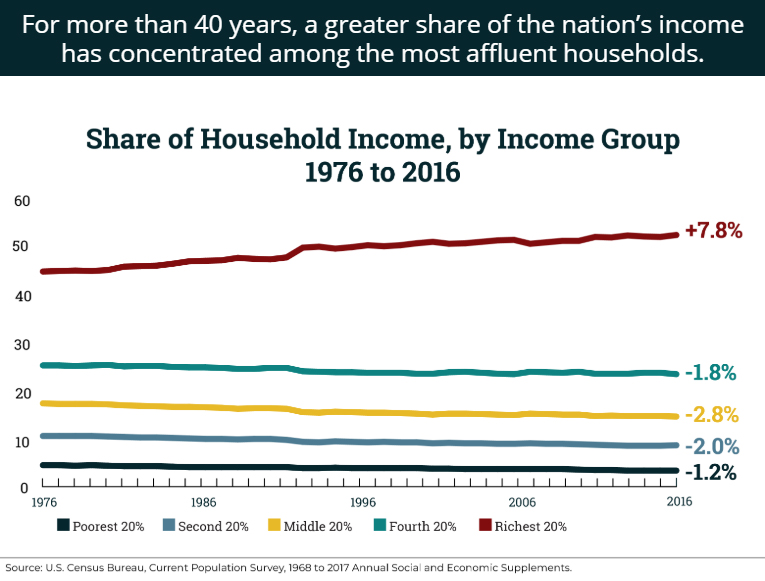

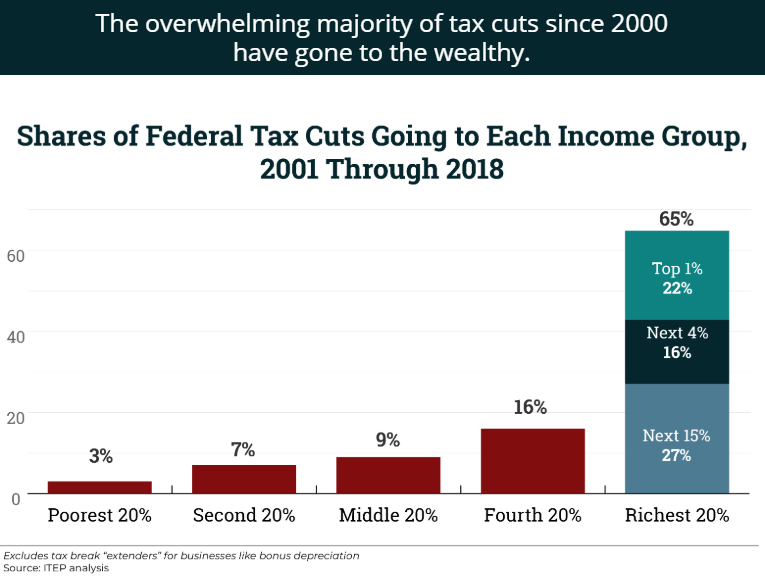

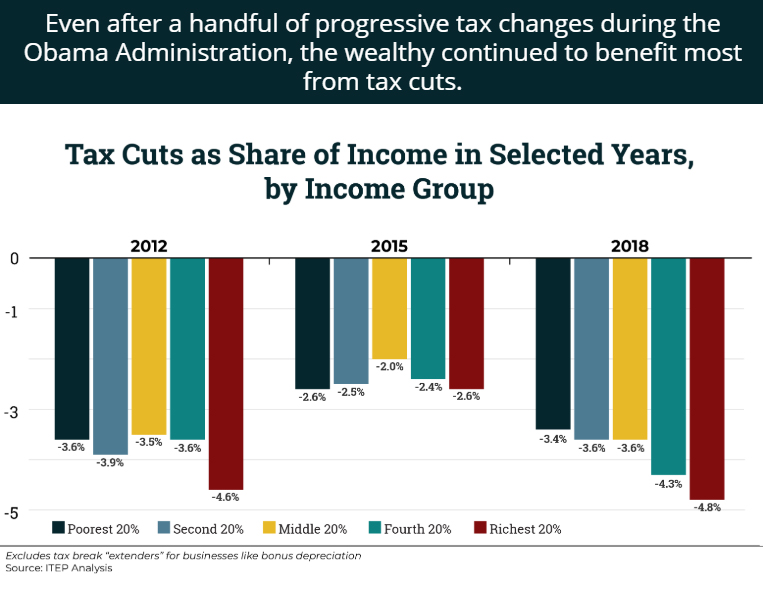

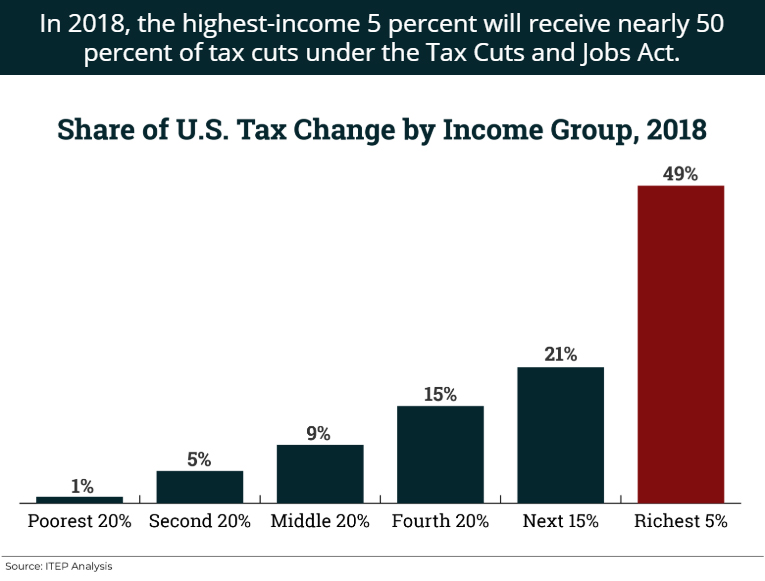

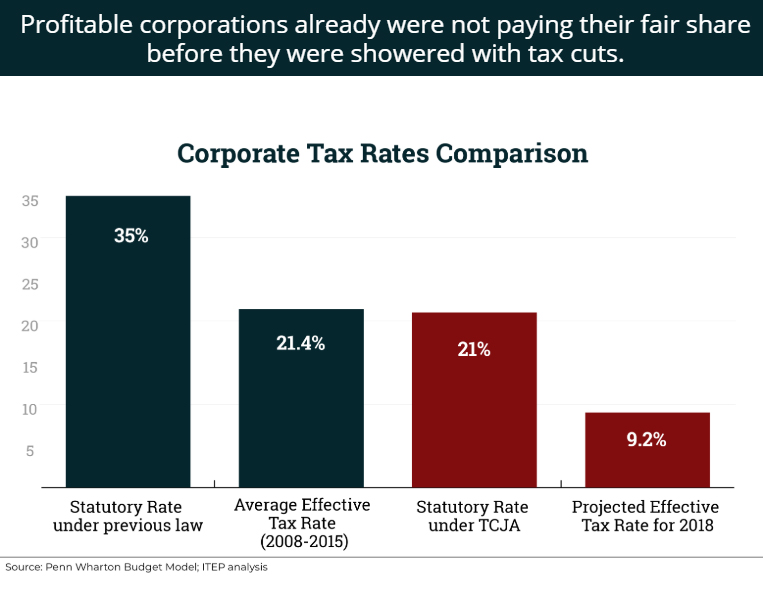

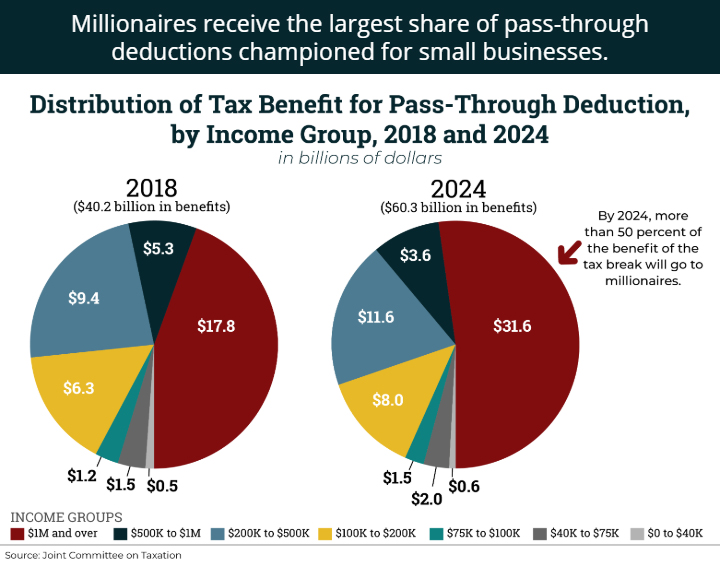

In this illustrated breakdown of the Tax Cuts and Jobs Act (TCJA) and Tax Cuts 2.0, ITEP staff examine TCJA’s role in growing income inequality, broken promises from corporations pledging to invest tax savings into workers and wages, and the embarrassment of riches flowing to the wealthiest Americans as a result of these “middle-class tax cuts.”