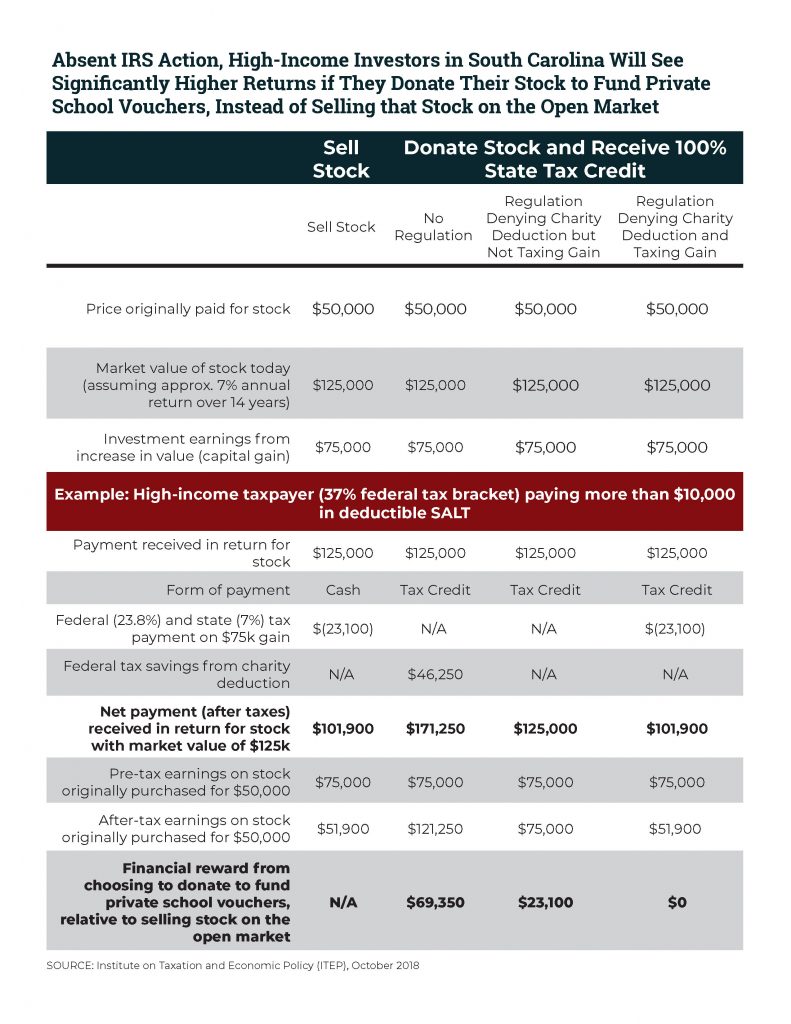

A new IRS proposal could once again allow wealthy business owners to use state charitable tax credits—including tax credits for donating to support private and religious K-12 schools—to dodge the federal government’s $10,000 cap on state and local tax (SALT) deductions.

This week ITEP submitted comments urging that the regulations be clarified to prevent this form of tax avoidance.

The proposal builds on regulations that the IRS finalized last year ending this scheme for individuals. While the details were complicated, the bottom line was simple. Taxpayers who make charitable donations but then see those donations reimbursed (often dollar-for-dollar) with lucrative state tax credits can no longer pretend they did something truly philanthropic and get a federal charitable tax deduction.

Previously, people who donated to certain programs—usually K-12 private and religious school vouchers—could reap combined state and federal tax cuts larger than their so-called “donations.” They were turning a profit at taxpayer expense while making a mockery of the entire concept of charity. And they were dodging the SALT cap in the process because, at its core, the scheme allowed taxpayers to reclassify their nondeductible SALT payments into fully deductible, so-called “charitable donations” instead.

ITEP commented favorably on those regulations and explained that they were needed to prevent new SALT cap workaround proposals that emerged in response to the 2017 Trump tax law, and also a variation of the much older tax scheme that had long been abused by wealthy donors to private K-12 school voucher programs.

But the latest IRS proposal, which builds on the regulations finalized last year, suggests that high-income owners of pass-through businesses may be able to continue their caper in a slightly different form. Specifically, the IRS proposal appears to allow owners of pass-through businesses to dodge the SALT cap and turn a profit for themselves by classifying their payments to private school groups and other entities as deductible business expenses rather than charitable contributions.

ITEP’s newest comments detail how this scheme could work in practice and offer recommendations for shutting it down definitively.

The IRS is accepting public comments through January 31 and will likely finalize a version of these regulations sometime this year.