Read this Policy Brief in PDF

The Tax Cuts and Jobs Act (TCJA) was enacted just weeks before many state legislatures began their sessions, leaving state lawmakers, tax officials, and the public scrambling to understand how the bill affects their states and how they should react. The TCJA has many important implications for both the fairness and adequacy of state tax codes and this report aims to summarize those implications and provide guidance on the key decisions facing state policymakers going forward.

Most states piggy-back on federal law to some extent for their own taxes, especially personal and corporate income taxes. These states in particular must understand what the federal changes mean for their own tax codes and decide whether to remain “coupled” to the changes in the TCJA, decouple from them, or take other action in response. But all states are affected by the federal tax cuts and the funding cuts to important public priorities that will inevitably result. Every state therefore has crucial choices to make this year and in coming years, including whether to adopt the federal tax changes, how much to rely on the federal tax code going forward, and how to maintain adequate services in the face of impending federal funding cuts.

As with all tax policy decisions, state policymakers should determine their responses to the federal tax bill with an eye toward maintaining adequate revenue, promoting tax fairness, and ensuring stability and sustainability in the tax code. And given the high stakes and significant uncertainty surrounding these debates, a broad view of each of these considerations is particularly crucial. When considering the full picture of state funding needs, who is most affected, and what is to be expected in the long term, a few key lessons come to light.

When choosing which provisions of the federal bill to adopt or reject, and what other steps to take in response, state policymakers should:

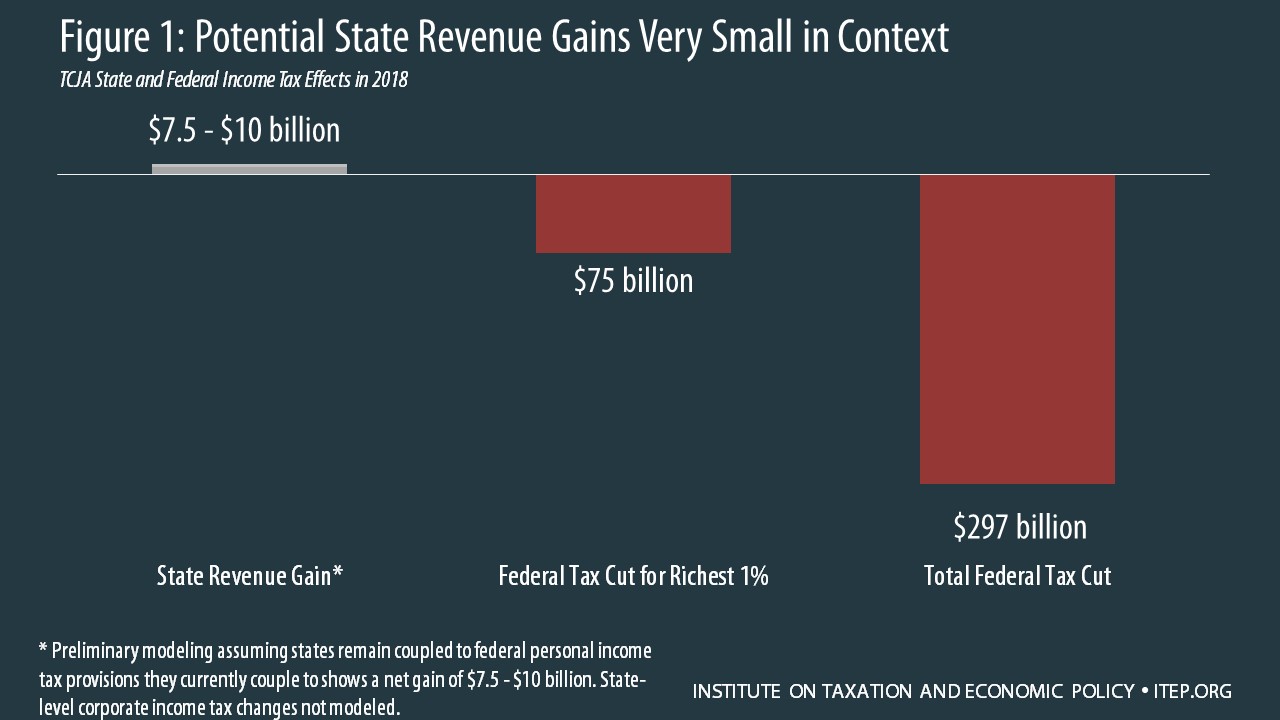

- Protect and enhance revenues to fund vital services, and reject any efforts to worsen their budget outlooks through tax cuts. Existing budget shortfalls, underfunded services, inadequate rainy day funds, and looming federal budget cuts all indicate a large and growing need for revenue in most states. What is more, there is a great deal of uncertainty surrounding the effects of the TCJA because it was passed in haste, is ridden with loopholes and complexity, and also contains major business tax provisions such as a switch to a “territorial” corporate tax system whose effects on states no one can currently predict. And in the vast majority of affected states, the need far outweighs any minor revenue bump they may get as an indirect effect of the federal tax changes. At the least, states should reject the characterization of these revenue gains as “windfalls” and resist the temptation to direct the revenues toward tax cuts that will further undermine their ability to sufficiently fund public services.

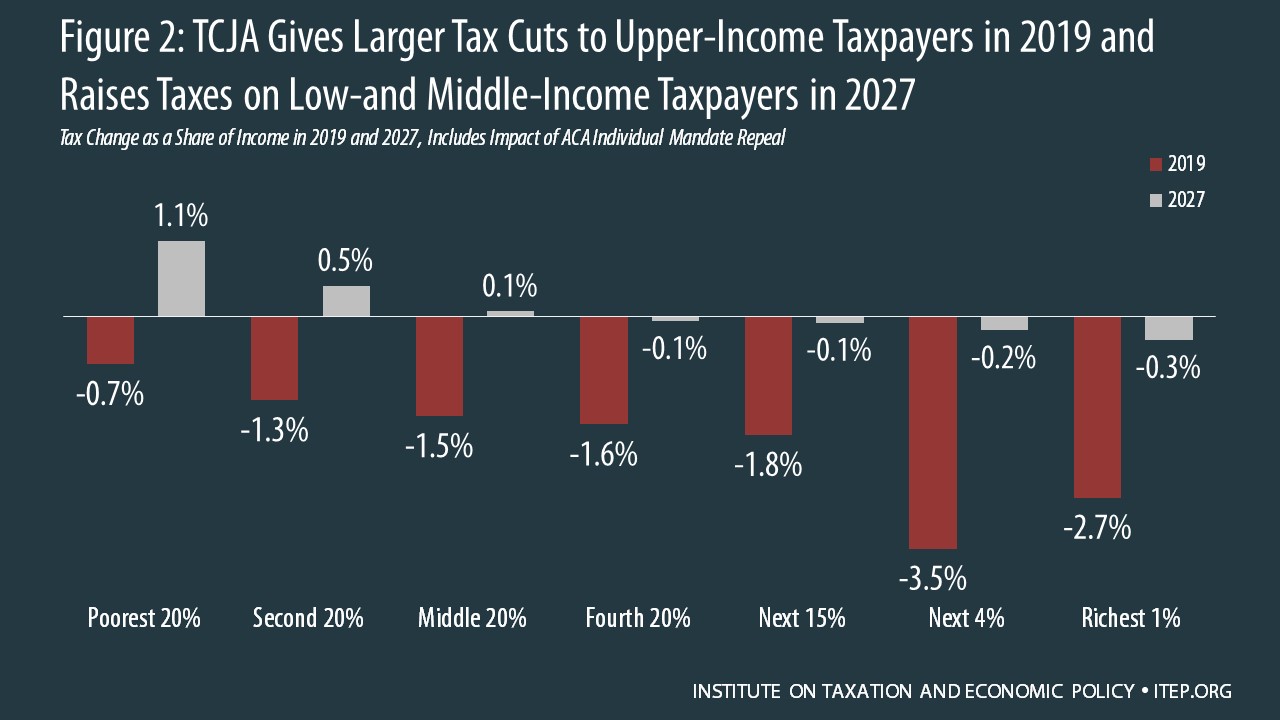

- Mitigate – not exacerbate – the regressive nature of federal tax changes that overwhelmingly benefit the highest-income Americans. While each state tax code’s relationship to the federal code is unique and the state-level effects vary substantially, the highest-income residents of every state receive significant federal tax cuts that far exceed the cuts going to low- and middle-income families and easily outweigh any state-level tax increases they might see as an effect of those federal changes (Figure 1). Moreover, at the state and local level, these wealthy households already pay lower effective tax rates than those in all other income groups. State reactions to the TCJA should work in the opposite direction: although the revenue gains some states will experience are generally small, if state lawmakers are determined to give back some of the increased revenue to taxpayers, those measures should take the form of targeted tax cuts for the low- and middle-income families most likely to see state-level tax increases; and to the extent that additional revenue is needed, states should raise the revenue by asking more of those wealthy groups that are set to receive major cuts in their federal taxes.

- Remember that trickle-down economics and Kansas-style tax competition do not work. The TCJA and many proposed reactions to it are based on disproven economics asserting that tax cuts for corporations and wealthy individuals at the expense of public priorities like education and infrastructure are a recipe for growing state and national economies. States should not buy into this approach by cutting taxes even further in hopes of economic growth. In fact, states can explicitly reject the new law’s misguided economics by recouping part of the tax windfall that it gives to corporations and wealthy families, and investing it in families and needed infrastructure. This approach should both promote more broadly shared prosperity and protect states from the impact of potential budget cuts in federal support for important state services.

- Focus permanent responses on the long-term good of their states, not short-sighted tax-cut temptations or political maneuvering. Most of the TCJA provisions directly affecting families and individuals are temporary, expiring after 2025. But a provision that slowly raises people’s taxes by reducing cost-of-living adjustments is permanent, as are major tax cuts that primarily help high-income investors by slashing taxes on corporations. In other words, a broad tax cut heavily skewed toward the wealthy eventually becomes a permanent tax cut for those wealthy households and a tax increase for most Americans (Figure 2). This makes the idea, already touted in some states, of using temporary state revenue gains to pay for permanent income tax rate cuts particularly unconscionable, as such cuts would benefit those same wealthy households even further. State policymakers should feel no need to cut taxes on those households at all, much less to make permanent regressive changes to their tax codes that will persist even when their low- and middle-income residents face federal tax hikes down the road. While states can take the current climate as an opportunity to meaningfully reform their tax codes, such reforms should focus on strengthening the progressive aspects and revenue performance of state tax codes for the long term, not weakening them through permanent or regressive tax cuts. Finally, states should also avoid politically driven gimmicks and overreactions such as converting taxes to charitable contributions, or converting income taxes to payroll taxes.