On the last day of their legislative session, Oklahoma lawmakers finalized a $6.8 billion budget bill that was later signed by Gov. Mary Fallin. In the governor’s statement on the bill, she noted that state agencies will be hard hit by the agreement–“it leaves many agencies facing cuts for the sixth year in a row”–and that while it does include some recurring revenue, it does not address the state’s long-run structural budget challenges.

These are valid concerns that make this a disappointing budget agreement for the Sooner State especially since Oklahoma was off to such a good start this year.

Most notably, in April lawmakers wisely repealed the second of two automatic cuts to the state’s top personal income tax rate. The cut, which would have lowered the top tax rate from 5 to 4.85 percent, could have been triggered as early as this year despite the state’s $878 million revenue shortfall. Had the cut been allowed to take effect, nearly 70 percent of the benefits would have flowed to the wealthiest 20 percent of Oklahoma households.

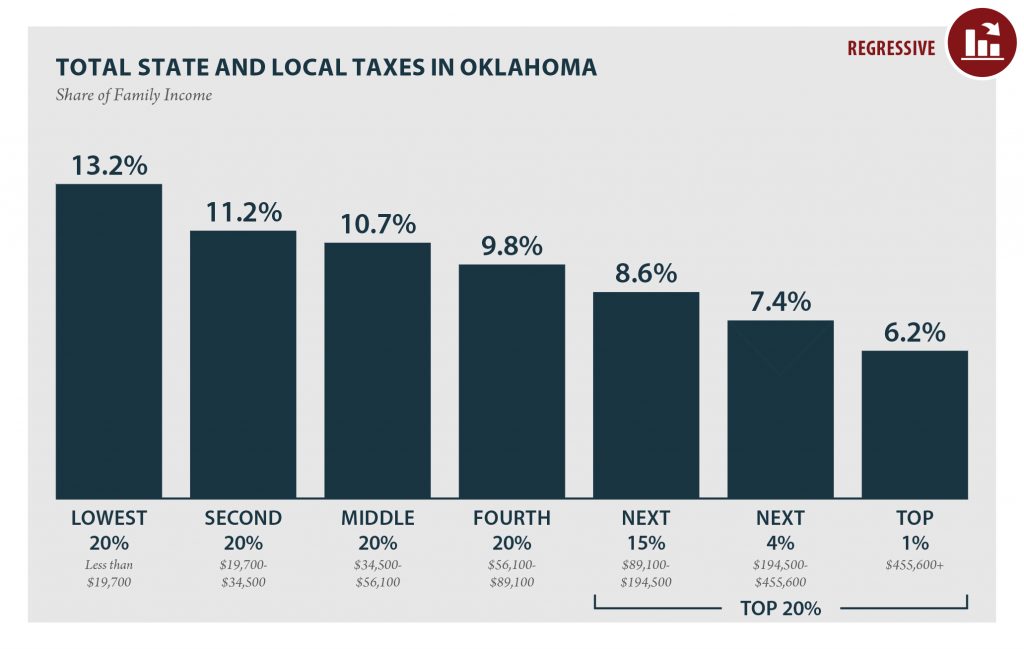

Also, more progressive alternatives considered by the legislature failed to gain enactment. Oklahoma has a regressive tax code that asks more of its low- and middle-income families than of wealthy Oklahomans. In a move that would have helped lessen this unfairness, the House passed a measure that would have capped the amount of itemized deductions that Oklahomans can claim. But the proposal did not gain support from the Senate.

Lawmakers ultimately settled on spending cuts and a mix of regressive and low-yield revenue increases. The spending cuts range far and wide, with 51 state agencies experiencing some type of cut. The Department of Education, which has been under particular stress, will see a slight increase in funding, but not enough to avoid drastic measures such as four-day school weeks. Revenue increases include a $1.50/pack cessation fee on cigarettes, partial repeal of sales tax exemption on purchases of motor vehicles, raising the tax rate on some horizontal drilling wells, sunsetting rebates and exemptions on the state’s gross production tax, a handful of compliance initiatives, and eliminating vendor discounts. Lawmakers also prevented the state’s standard deduction from growing alongside inflation, a move that would decouple Oklahoma from any future federal changes to the standard deduction. Lawmakers also appropriated funds from the state’s constitutional Rainy Day Reserve Fund.

It is important to note, however, that many of the revenue provisions may soon be challenged in court because the state constitution prohibits revenue bills from passing during the last five days of session, and requires that such bills receive a three-fourths vote in both chambers. Further, the bill enacting the new fee on cigarettes is expected to require proof that its primary purpose was not to raise revenue.

While budget discussions in Oklahoma have concluded for the session, Gov. Fallin was correct in stating that the state’s structural budget challenges have not yet been addressed. Oklahoma lawmakers need to start looking toward the long-run in their budget decisions and, moving forward, should more seriously consider the impact of tax changes on the fairness of the state’s tax code.