See the 2016 Updated Brief Here

Read this Policy Brief in PDF Form

Sales taxes are one of the most important revenue sources for state and local governments—and are also one of the most unfair taxes. In recent years, policymakers nationwide have struggled to find ways of making sales taxes more equitable while preserving this important source of funding for public services. This policy brief discusses the advantages and disadvantages of two approaches to progressive sales tax relief: broad-based exemptions and targeted sales tax credits.

The Problem: Sales Taxes Are Unfair

State and local sales taxes are inherently regressive because the lower a family’s income, the more of its income the family must spend on things subject to the tax. According to estimates produced by ITEP based on Consumer Expenditure Survey data, low-income families typically spend three-quarters of their income on things subject to the sales tax, middle-income families spend about half of their income on items subject to sales tax, and the richest families spend only about a sixth of their income on sales-taxable items. Lawmakers seeking to provide relief for low-income taxpayers have two choices:

- They can provide general sales tax exemptions for items such as groceries and utilities that constitute a larger share of income for poorer taxpayers.

- They can provide targeted low-income tax credits instead of exemptions.

Exemptions and Credits: How They Work

Exemptions are the most popular approach to progressive sales tax relief. Exemptions eliminate all sales taxes on particular retail items. For example, thirty one states exempt groceries from their state sales tax, and almost all states exempt prescription drugs. Many states also exempt sales of residential utilities such as electricity or natural gas.

Targeted tax credits are an innovative alternative to exemptions. Usually administered through the income tax, these credits generally provide a flat dollar amount for each member of a family, and are available only to taxpayers with income below a certain threshold. These credits are usually refundable, meaning that the value of the credit does not depend on the amount of taxes a claimant pays and that credit is given even if it exceeds the amount of income tax a claimant owes.

Disadvantages of Exemptions

The main disadvantage of sales tax exemptions is that they make the sales tax base (that is, the total dollar amount spent on taxable items) much narrower, and reduce the yield of the tax. Economists generally argue that the sales tax base should be as broad as possible, for several reasons:

- Exemptions are poorly targeted. The poorest 40 percent of taxpayers typically receive only about 25 percent of the benefit from exempting groceries. The rest goes to wealthier taxpayers who can more easily afford to pay the sales tax on groceries.

- While exemptions can make the sales tax less regressive, they also create a new source of unfairness: differential treatment of taxpayers at a given income level. By exempting food while taxing other retail sales, lawmakers are discriminating against taxpayers who spend more of their money on non-food items.

- Exemptions tend to make sales tax collections fluctuate more, because changes in particular economic sectors can affect tax collections. A broader tax base will allow tax revenues to be less sensitive to sudden swings in retail purchases of particular items since those swings will generally be off set by changes in purchases of other items.

- Because they offer tax relief to everyone regardless of their individual need, exemptions are very costly. Exempting groceries, for example, has the potential to reduce the revenue yield of each penny of sales tax by nearly twenty percent. This requires that lawmakers increase tax rates in order to off set the reduction in the tax base.

- Exemptions are an administrative challenge to policymakers, tax administrators, and retailers because any exemption requires a way of distinguishing between taxable and exempt products. For example, in some states a food item may be taxable based only on whether or not the seller provides eating utensils with the item. Exemptions require policymakers and tax administrators to make countless decisions of this sort, and retailers must be familiar with all of these rules.

- In states that allow local sales taxes, lawmakers must decide whether sales tax exemptions should apply to local taxes as well. Doing so can be costly to local governments, but failing to do so creates more complication for retailers and tax administrators.

Credits: A Better Alternative

Sales tax credits offer several advantages over sales tax exemptions, among them: credits can be targeted to state residents only, and they can be designed to apply to whichever income groups are deemed to be in need of tax relief.

The precise targeting of credits means that they can be much less expensive than exemptions. Credits do not affect the sales tax base, so the long-term growth of sales tax revenue is more stable. And credits are easier for tax administrators to manage.

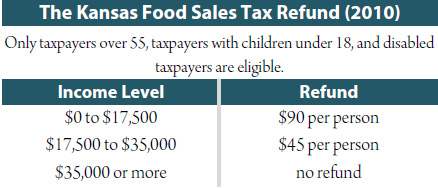

Several states offer an income tax credit to assist in off setting some of the sales and excise taxes that low- income families pay. Some of the credits are specifically intended to off set some of the impact of sales taxes on groceries. The chart on this page shows the details of one such program, the Kansas food sales tax refund.

However, sales tax credits do have disadvantages. The main drawback of credits as an alternative to exemptions is the added administrative responsibility on taxpayers. All of the states that currently allow sales tax credits require taxpayers to file an application form, usually in conjunction with state income tax forms. Eligible taxpayers who do not know about the credit, or who do not have to file an income tax form, may not claim the credit. This means that an effective outreach program is a critical part of any effort to provide sales tax credits of this sort. By contrast, exemptions are given automatically at the cash register—so consumers don’t need to apply or even to know about them.

Many states interested in mitigating the regressive effects of the sales tax have decided to rely on a state Earned Income Tax Credit (EITC) in lieu of a formal sales tax credit (described in ITEP Policy Brief, “Rewarding Work Through the Earned Income Tax Credit”). While this approach offers state lawmakers less flexibility in deciding on the credit’s eligibility criteria and amount, it is preferable from a tax simplicity perspective. This is because state EITCs are based on the federal credit which enhances the ease with which taxpayers can claim the credit.

Sales Tax Relief: Only Part of the Solution

Exemptions and credits are both progressive options for low-income tax relief—but neither is sufficient to off set the basic regressivity of sales taxes. Sales tax exemptions and credits should each be part of a broader strategy for tax fairness that includes a progressive, graduated personal income tax, but sales tax breaks are likely to be insufficient on their own to eliminate the unfairness of state and local taxes.