This piece originally appeared in State Tax Notes.

Race was front and center in a lot of state policy debates this year, from battles over what’s being taught in schools to disagreements over new voting laws. Less visible, but also extremely important, were the racial implications of tax policy changes. What states accomplished this year – both good and bad – will acutely affect people and families of color.

Tax policy is an important tool to mitigate injustices confronting marginalized communities and to advance genuine racial equity. Done well, tax reform can create a dream scenario of equitable taxation and well-funded public services for everyone. It can also create a nightmare of regressive taxation and weak public investment.

More than one-third of states made strides this year to improve their tax systems. This mostly happened through strengthening refundable credits, which offer a proven means of bolstering economic security. In a few states, lawmakers also opted to raise new tax revenue in equitable ways to fund public priorities. Other states, however, prioritized top-heavy tax cuts that will leave fewer resources to respond to the challenges that lie ahead.

Refundable Credits Are a Victory for Racial Equity in States

Policymakers created Child Tax Credits (CTCs) or Earned Income Tax Credits (EITCs) in 11 states and enhanced them in 13 states this year. These are often structured as refundable tax credits, which ensures that people with little to no income tax liability receive a refund to help offset the substantial amounts of sales, excise, and property taxes they pay. Without refundability, the lowest income families are effectively deemed too poor to qualify for the credit.

Refundable credits are a promising way to secure economic justice, advance racial equity, and help communities of color. They can serve as a lifeline to low- and moderate-income families who face food and housing insecurity, and who generally struggle to make ends meet.

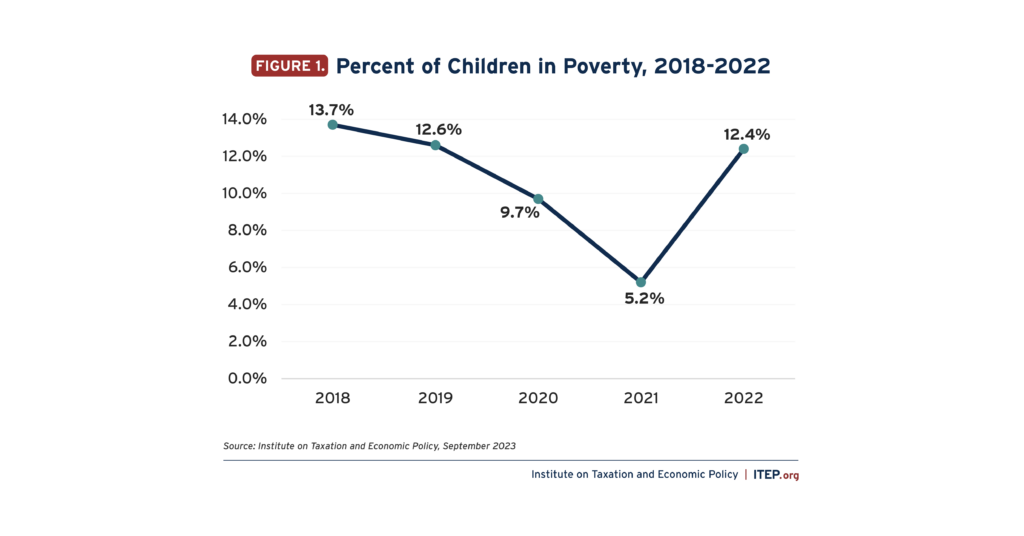

State lawmakers’ interest in refundable credits, and the CTC in particular, has increased largely as a reaction to the federal government’s successful implementation of a larger, fully refundable CTC in 2021. That policy has since lapsed, causing child poverty to more than double. Under the pared-back federal CTC in effect today, 45 percent of Black children, 42 percent of Hispanic children, and 23 percent of white children are denied at least a portion of the federal CTC because their families’ incomes are too low. Fully refundable state CTCs can help make sure that low-income children of all races receive more financial support – help that would be particularly valuable to the Black and Hispanic families that are disproportionately excluded from the full credit.

Minnesota policymakers had a particularly innovative approach in 2023 that will do the most for children with the greatest needs. The state’s new CTC provides a $1,750 per child maximum credit. With a phase-out starting at $29,500 for single filers, the credit is narrowly targeted to those most in need. The state also restructured its EITC and made the credit more inclusive by extending eligibility to immigrants who file without Social Security numbers.

States that created or improved EITCs or CTCs in 2023: Connecticut, Colorado, Hawaii, Indiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Montana, New Jersey, New Mexico, New York, Oregon, Rhode Island, Utah, Vermont, and Washington.

Raising Revenue to Invest in Key Public Programs

Programs that help families of color succeed focus on equity, economic stability, and liberation. This year some states raised revenue to continue investing in those programs. Minnesota, for example, created a new 1 percent tax on high earners’ investment income, becoming the first state with a broad-based income tax to nonetheless choose to tax long-term capital gains income at a higher rate than wages. The state also strengthened taxes on multinational corporations, pared back standard and itemized deductions for high-income families, and implemented a new payroll tax, among other reforms. Some of the new public services being funded by this new revenue are free school meals, guaranteed family and medical leave, and more affordable college tuitions.

Connecticut and New York also raised revenue by extending temporary corporate tax surcharges through 2025 and 2026, respectively. In recent years, stocks have grown to be the largest source of wealth for white families, especially well-off white families. While racial wealth disparities outside of corporate equities have narrowed in recent years, stock values have grown so rapidly they alone have been able to fuel recent increases in inequality. Taxing corporate profits more robustly is an effective way to narrow racial wealth gaps.

Finally, Washington state’s Supreme Court upheld the state’s new tax on capital gains exceeding $250,000. The policy, which recently went into effect, is estimated to bring in approximately $849 million in its first year, much higher than earlier projections. Most of the new revenue will go to education, with any revenue above $500 million going to one-time school construction projects.

States that enacted revenue raising policies in 2023: Connecticut, Delaware, Maine, Minnesota, New York, and Vermont.

Tax Cuts Widen the Economic Advantage of White Households Over Households of Color

Too many states, however, enacted deep tax cuts that, in most cases, will disproportionately help the wealthiest families. Nearly one-third of states cut taxes in 2023. Often touted as a responsible use of the temporary surpluses states had on hand, over time these cuts will drain funding for key programs and services that strengthen the economy, make communities thrive, and help all families, and particularly families of color, flourish. The same people who for centuries have been held back economically and whose communities have lacked adequate investment again saw legislators prioritizing the well-being of high-income households over public goods that benefit everyone.

Kentucky has been on a path of repeated income tax cutting in recent years. What was once a graduated tax with rates ranging up to 6 percent is now a flat tax with a rate that will soon fall to 4 percent. A trigger law on the books could eventually eliminate this tax in its entirety.

Kentucky is already a state with high poverty rates across the board (15.8 percent in 2022 compared to 11.5 percent for the nation), and Black residents are more likely to be poor (24.4 percent) than white residents (15 percent). The state does not have a large wealthy population but 92 percent of Kentuckians in the top 20 percent of total tax returns – those who our data show are getting the bulk of the tax cuts – are white. In contrast, only 4 percent of this group is Black, despite Black Kentuckians making up 8 percent of households overall.

The beneficiaries of Kentucky’s tax-cut spree so far are disproportionately white while families in the most dire financial circumstances, including an outsized share of Black families, will receive next to zero benefit from the most recent round of income tax cuts. They will, however, undoubtedly suffer from the erosion of Kentucky’s largest revenue source. The most recent rate cut, to 4 percent, will cost the state an estimated $1.3 billion annually. That’s a huge loss in revenue and will hurt poor Kentuckians of all races while particularly hurting the state’s Black residents. The state is already facing a funding gap between wealthy and underfunded school districts. And the law is set to continue these unjust tax practices in one way or another.

States that enacted significant income tax cuts in 2023: Arkansas, Connecticut, Indiana, Kentucky, Maine, Michigan, Missouri, Montana, Nebraska, New Hampshire, North Dakota, Ohio, Utah, West Virginia, and Wisconsin.

Looking Ahead: Racial Justice and Tax Policy Options for 2024 State Legislative Sessions

Rather than top-heavy tax cutting that widens the racial wealth gap, states should consider strengthening refundable tax credits that are targeted to low-income families and boosting revenue through progressive tax increases on high-earners and corporations. Among the many policies that states should consider for next session, here are three that should be at the top of the list for lawmakers who prioritize racial justice:

- Enact Worldwide Combined Reporting. This would greatly strengthen state corporate taxation by making it all but impossible for companies to falsely claim that an outsized share of their profits were earned offshore and out of reach of state tax authorities. This year, Minnesota came close to enacting worldwide combined reporting, and other states should follow this promising path. Corporate tax dodging is a boon to wealthy shareholders, a disproportionate share of whom are white.

- Raise taxes on capital gains and dividends income. Minnesota set a valuable new precedent this year with the decision to begin taxing certain investment income at a higher rate than wages and salaries. This is a useful way to claw back some of the unwarranted preferential treatment that income from wealth receives in federal law. A groundbreaking analysis by officials at the U.S. Treasury Department concluded earlier this year that just 2 percent of the federal government’s preferential rates for capital gains income make their way to Black families, and just 3 percent flow to Hispanic families. Clearly, preferential treatment for investment income at the federal level is worsening racial disparities. States have a productive role to play in counteracting this negative effect, too.

- Enhance EITCs and CTCs. Robust, refundable tax credits strengthen economic security in ways that can be enormously beneficial for children and families of all races. Our research shows, however, that Black and Hispanic families are too often barred from receiving the full benefit of the federal CTC, so states should take steps to make up for this difference. Next year, state legislatures should continue to lean into strengthening CTCs and EITCs.

This year states took some steps forward and other steps back along our nation’s long and winding path to racial equity. Lawmakers dedicated to ending racial inequities have the tax code as an option to support that mission next year and into the future.