A refundable tax credit proposed by Rep. Rashida Tlaib (D-MI) would be more expansive than other recent tax credit proposals, new estimates from ITEP show.

Rep. Tlaib’s proposal, unlike others, does not require households to work to receive the benefit. Called the BOOST Act, it would provide a tax credit of $3,000 for single adults and $6,000 for married couples, adjusted annually for inflation. Income limits would target benefits to low- and middle-income households, phasing out the credit as household income increases.

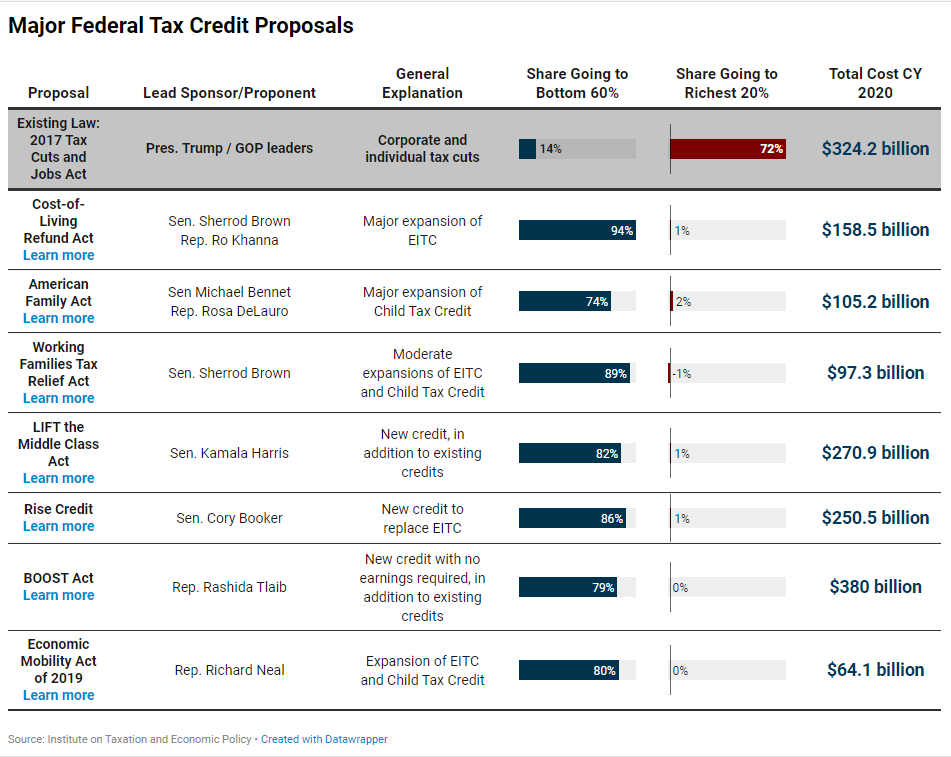

ITEP’s estimates are projections for 2020, when the credit amounts and income thresholds would be slightly higher due to inflation adjustments.

The BOOST Act is different from other proposed tax credit expansions analyzed by ITEP because it would provide a refundable tax credit to low- and moderate-income people generally regardless of whether they have earnings or have children or are students. By comparison, five proposals that ITEP examined in a May report would target lower-income and moderate-income people who either have earnings or have children, or in some cases, are students. As with other proposals to create or expand tax credits, those who are claimed as dependents of other tax filers would not be eligible.

The BOOST Act could help millions of people who would receive no benefit from the other major tax credit proposals, including working-age people who are not employed and retirees who have no earnings and no dependent children and, therefore, would not benefit from the other tax credit proposals. It is, in other words, the first proposal that would be made fully available to all low-income people and families.

Like the other tax credit proposals recently analyzed by ITEP, the BOOST Act is the inverse of the 2017 Tax Cuts and Jobs Act, which provided most of its benefits to the richest fifth of Americans and foreign investors. Like the other major refundable tax credit proposals, the BOOST Act would provide most of its benefits to the bottom 60 percent.

The BOOST Act’s credit would phase out for single childless adults with incomes between $30,000 and $50,000, and for married couples with incomes between $60,000 and $100,000. For single parents, the credit would phase out for those with incomes between $60,000 and $80,000.

Because eligibility under the BOOST Act hinges on income alone, it benefits more people and costs more. ITEP estimates that it would cost $380 billion in 2020—more than any of the other tax credit proposals ITEP has analyzed. It would benefit 153 million adults (65 percent of US adults) and 65 million children (68 percent of all children).

By not including work requirements to receive the tax credit, the BOOST Act differs from the Earned Income Tax Credit and the Child Tax Credit. For years, many politicians have argued that providing benefits without requiring work would lead to reduced work incentives. But some advocates and researchers question whether any such effects on work incentives are even significant enough to worry about and whether they justify withholding benefits from those who may need them the most – those with very little or no earnings.

ITEP is skeptical that a $3,000 benefit would cause many adults to stop working or that many adults would work fewer hours. (Evidence suggests that low-paid workers have little control over exactly how many hours they work anyway.) We do not include any such behavioral responses in our estimates because they are likely to be minimal.

While the BOOST Act is the most expansive tax credit proposal so far, it is not the first and likely will not be the last. Lawmakers’ interest in this approach is building, and we can expect to hear more about it.