National and State-by-State Data Available for Download

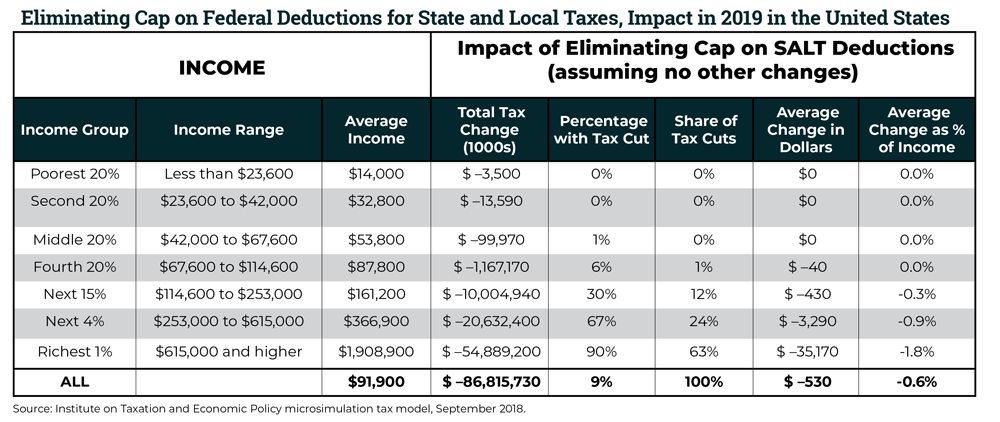

Nearly Two-Thirds of Benefits from Repealing the SALT Cap Would Go to the Richest 1 Percent

Lawmakers who opposed the Tax Cuts and Jobs Act (TCJA), the federal tax law enacted by President Trump and his allies in Congress last December, rightfully pointed out that the law benefits the wealthy at the expense of everyone else. Now, some lawmakers are proposing to give additional tax cuts to the rich by repealing one of the few provisions that controlled its costs.

The cost-controlling provision in question is the $10,000 cap on federal tax deductions for state and local taxes (SALT). Before TCJA, taxpayers could deduct an unlimited amount of SALT on their federal tax returns (although other provisions, like the Alternative Minimum Tax, could limit the benefits). Even with the cap on SALT deductions, TCJA will increase the federal deficit by $1.9 trillion over a decade.[1]

Outright repeal of the cap would primarily benefit the richest households. As illustrated in the table below, repealing the SALT cap would cost $87 billion in tax year 2019 alone and 63 percent of the benefits would go to the richest 1 percent.

The state-by-state data (which can be downloaded with the hyperlink at the top of this page) illustrate that in nearly every state, at least half of the benefits would flow to the top 1 percent of households in 2019.

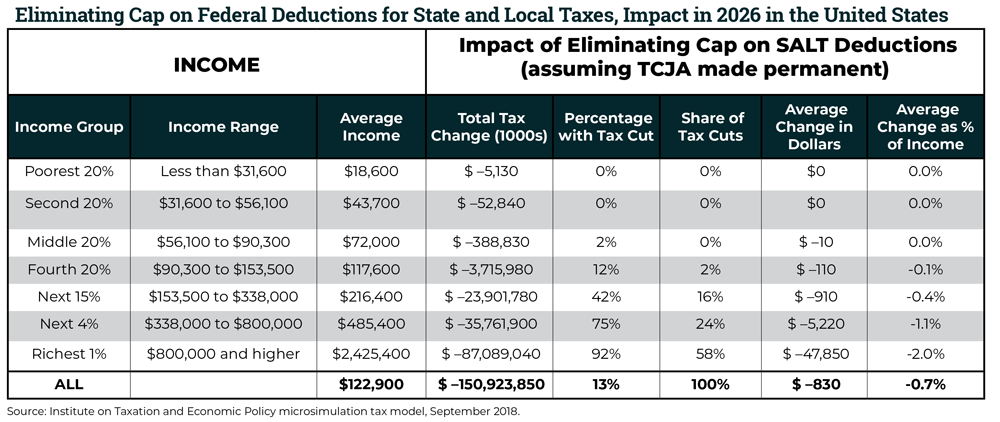

Congress will soon take up debate on so-called Tax Cuts 2.0 which would make permanent all of the temporary provisions of TCJA (which are now set to expire after 2025). Some lawmakers have expressed discomfort with extending the cap on SALT deductions and may call for eliminating the cap as part of a second round of tax cuts.

The table below illustrates the impact of eliminating the SALT cap in 2026, assuming all other TCJA provisions have been extended at least through that year. In later years, the SALT cap would affect more households (meaning repeal of the cap would benefit more households) because the $10,000 limit is not indexed for inflation. But repealing the cap would nonetheless primarily benefit high-income households far into the future. As illustrated in the table, repealing the cap would cost $151 billion in tax year 2026 (assuming the rest of TCJA is made permanent) and 58 percent of the benefits would go to the richest 1 percent that year.

It’s possible that lawmakers could try to replace the lost revenue from repealing the SALT cap by curbing some of the tax breaks that are included in TCJA, but that would not improve this proposal.

This would simply use badly-needed revenue to replace one tax cut for the richest households with another tax cut for the rich, leaving the cost of TCJA unchanged and making the distributional effects unchanged or even more tilted in favor of the wealthy. Repeal of the SALT cap would only make sense if it were replaced by a more progressive limit on itemized deductions for well-off households, but that has not been proposed by any lawmaker.

There are sound justifications for allowing families to deduct SALT on their federal returns, and there are valid criticisms of how the drafters of TCJA chose to strictly limit this type of deduction but not many others. But none of that changes the fact that the cap on SALT primarily affects the highest-income households. Rather than improving the tax law, repealing the SALT cap would only make it worse.

[1] Congressional Budget Office, “The Budget and Economic Outlook: 2018 to 2028,” April 9, 2018. https://www.cbo.gov/publication/53651