Earlier this year, ITEP released a report providing an overview of the impacts of state and local tax policies on race equity. Against a backdrop of vast racial disparities in income and wealth resulting from historical and current injustices both in public policy and in broader society, the report highlights that how states raise revenue to invest in disparity–reducing investments like education, health, and childcare has important implications for race equity.

The report looked at how different taxes have varying impacts on racial equity and unveiled data for two states—Minnesota and Tennessee—showcasing the consequences of their contrasting tax policy choices. In short, it found that income taxes can help narrow the racial income and wealth divides while sales taxes generally make those divides worse.

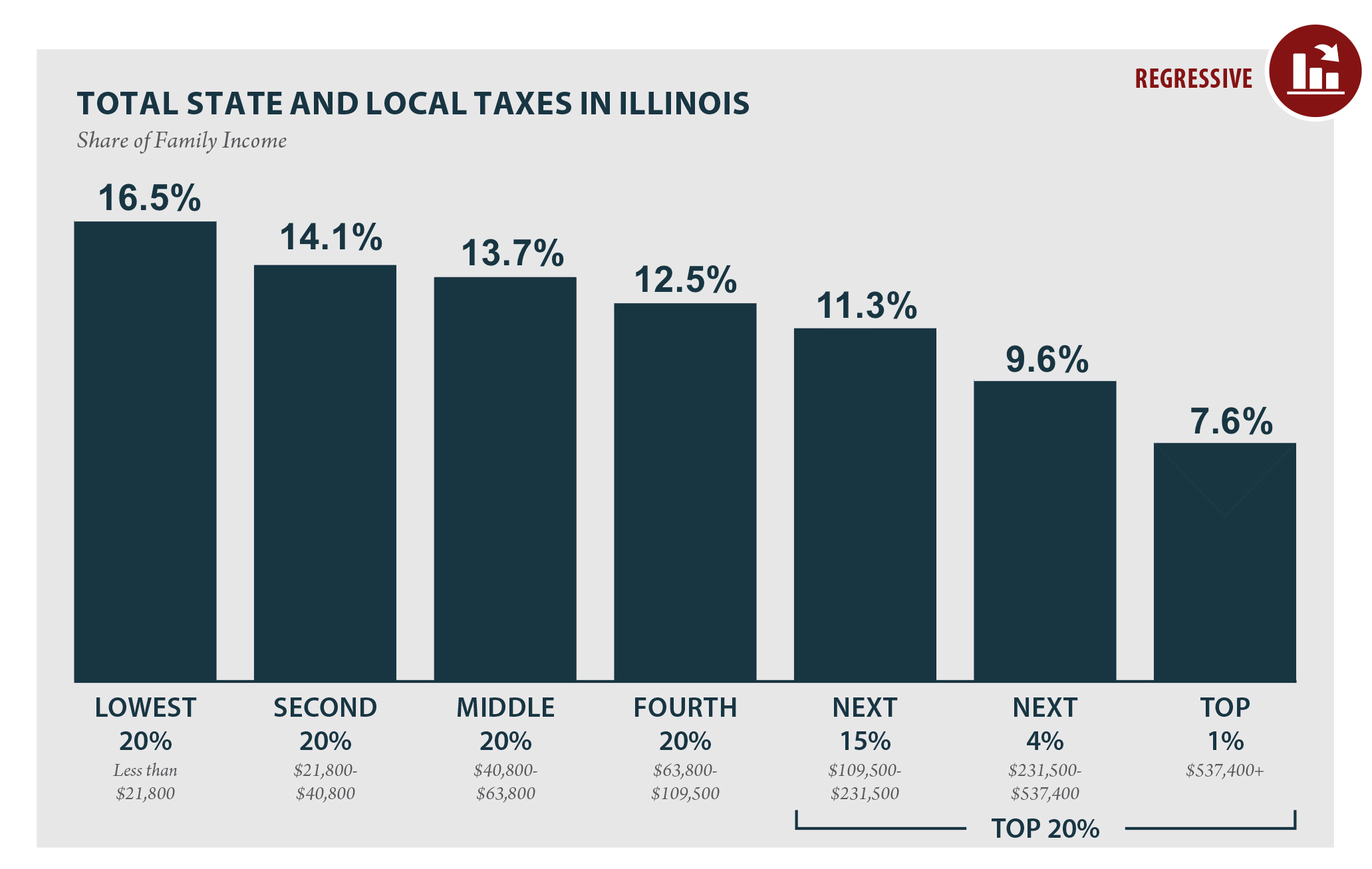

This same finding is true for all states and illustrated again in a new chartbook, Racial Inequities and the Illinois Tax Code.

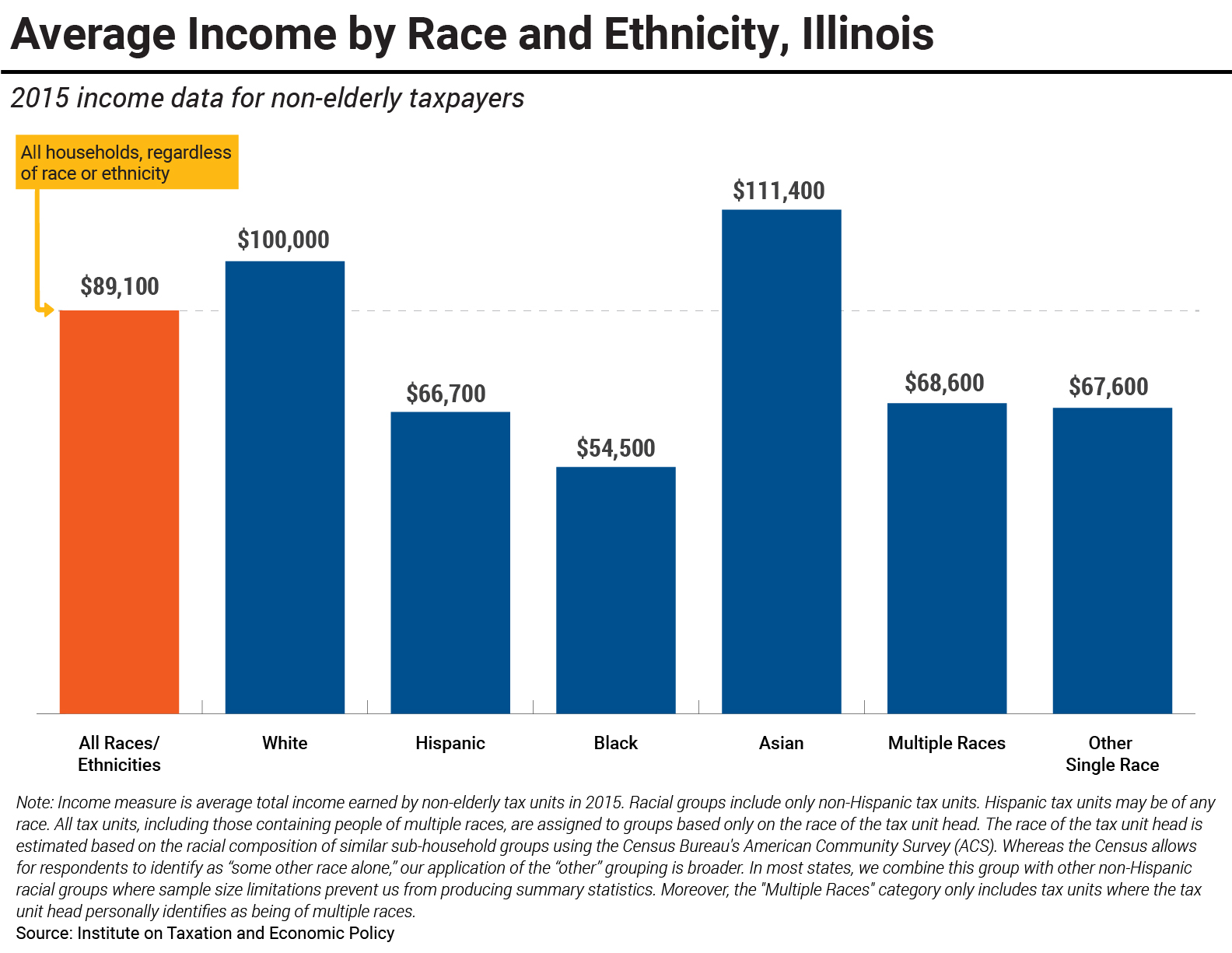

Disparities in income are a legacy of the long-lasting and compounding effects of historic & current racism, including employment discrimination, uneven education funding, redlining, and discrimination in lending practices.

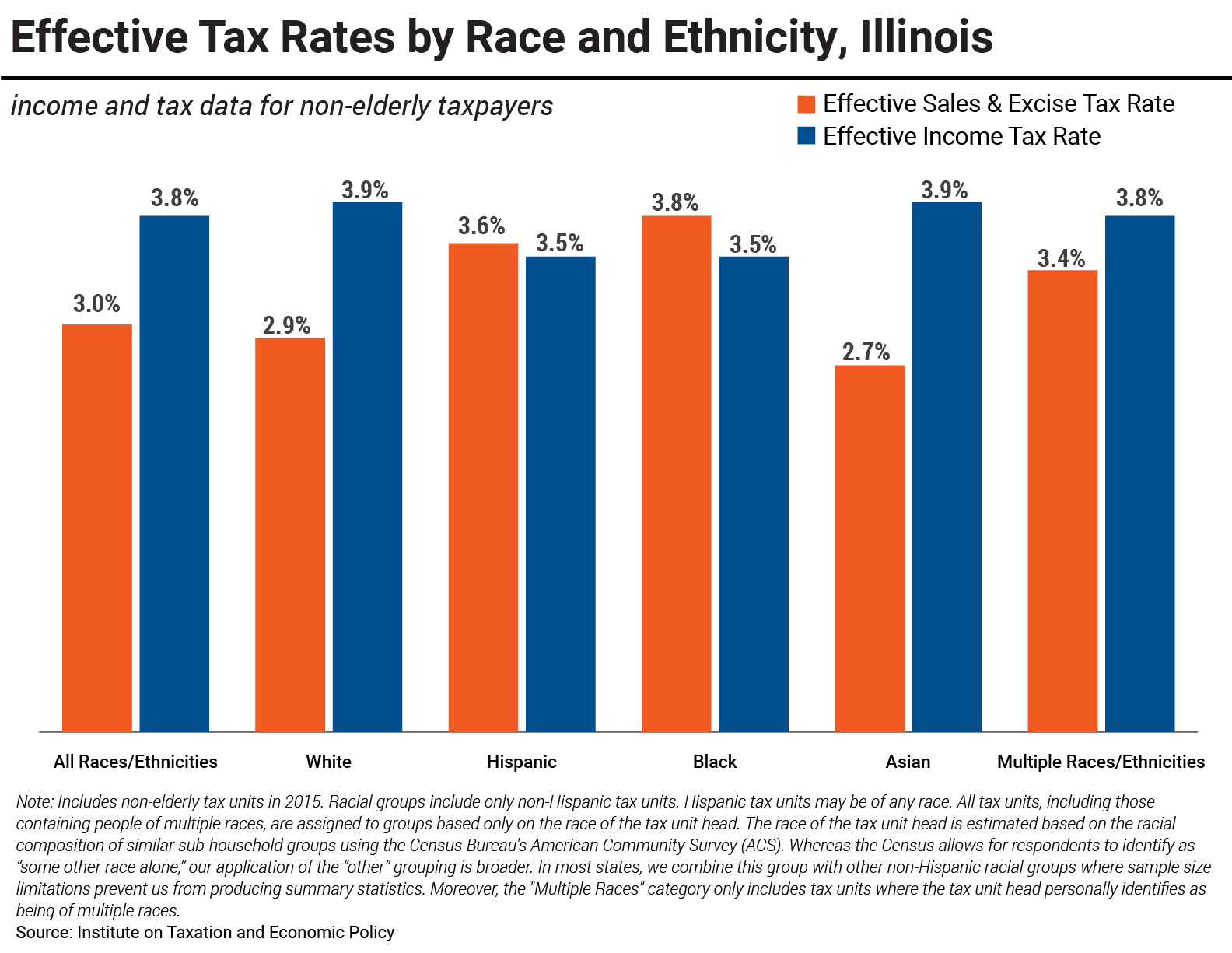

Illinois sales and excise taxes, for example, worsen disparities in income by race and because low-income households, in which households of color are disproportionately represented must spend a larger share of what they earn to make ends meet. Black households in Illinois pay an average effective sales and excise tax rate (3.8 percent) that is 27 percent above the average rate (3.0 percent) and 31 percent above the rate faced by the average white household (2.9 percent). Hispanic households pay an average rate (3.6 percent) that is 20 percent above average and 24 percent above the rate faced by the average white household.

The state’s personal and corporate income taxes, by contrast, slightly narrow the income gap by race and ethnicity in Illinois. Because white families have higher average incomes, their average combined income tax payment, at 3.9 percent of income, is higher than the rates Black or Hispanic (3.5 percent) families pay.

Different taxes have very different impacts by race and ethnicity. Regressive revenue sources like sales and excise taxes exacerbate inequities in tax liability and income by race, and progressive revenue sources like taxes on income and wealth are critical to narrowing these disparities.

This highlights that taxes on income and wealth are invaluable in narrowing disparities across race and ethnicity. While Illinois’s income tax is more equitable than its sales and excise taxes, the state’s flat income tax rate structure makes it impossible to sufficiently offset the inequitable impacts of its more regressive tax bases, and it poses a major barrier to using the tax code to address racial income disparities in a more substantive way.

While Illinois’s income tax doesn’t exacerbate underlying income inequalities, it doesn’t go far enough to offset the regressive impacts of the regressive components of Illinois’s state and local taxes, resulting in an overall tax system that worsens income inequality. Illinois’s reliance on a flat income tax is a barrier to its income tax being a more effective tool for addressing tax and income disparities by race.

To meaningfully address disparities in income by race and ethnicity, states including Illinois need to shift toward more overall progressive tax and local tax systems with higher effective tax rates on affluent residents and comparatively less reliance on tax dollars paid by lower- and middle-income families.

In Illinois, implementing a graduated personal income tax rate structure, eliminating regressive deductions, strengthening the corporate income tax, and strengthening the estate tax on high levels of wealth would all be moves in this direction. Policies designed to lift low-income families like tax credits for workers, renters, and families with children could also enhance the racial equity of Illinois’s tax code.

Just as policymakers and stakeholders came together to make choices that have resulted in current state and local tax systems, advocates and lawmakers today can also work together to create something better. By creating more progressive and sustainable tax codes, we can advance social and economic justice for taxpayers of all races and ethnicities in all states.

View the chartbook: Racial Inequities and the Illinois Tax Code.