Several Democratic candidates have proposed raising the statutory corporate tax rate from its current level of 21 percent to fund their spending proposals. Sen. Bernie Sanders and South Bend Mayor Pete Buttigieg have both proposed increasing the corporate tax rate back to pre-Tax Cuts and Jobs Act (TCJA) levels at 35 percent. Former Vice President Joe Biden and former Congressman Beto O’Rourke have mentioned raising the corporate tax rate to 28 percent while Sen. Amy Klobuchar proposes a rate of 25 percent. Political reporters and observers may read a great deal into the different corporate rates proposed by candidates, but the truth is that rates mean very little on their own.

What matters more is how candidates propose to shut down the loopholes and special breaks that allow corporations to pay much less than the statutory tax rate. Until last year, the statutory corporate tax rate was 35 percent, but the effective corporate tax rate—what companies actually paid as a share of their profits—was much lower. ITEP found that the effective tax rate for the Fortune 500 corporations that were consistently profitable from 2008 through 2015 was just 21.2 percent.

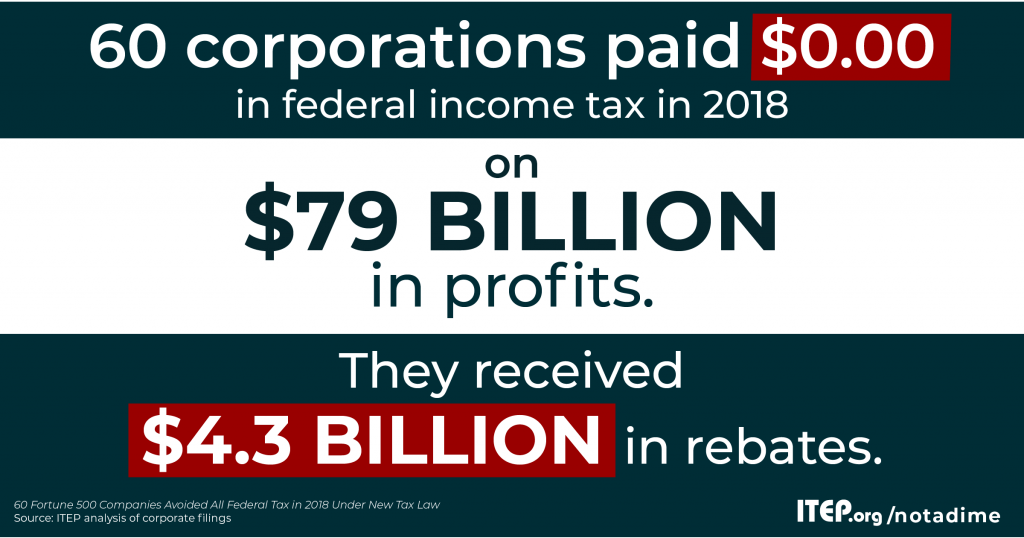

Now the statutory corporate tax rate is 21 percent, but once again most companies pay much lower rates. ITEP found that at least 60 profitable Fortune 500 corporations paid nothing in 2018, the first year under the new tax law. Many companies, such as Amazon, responded to ITEP’s findings stating that they paid what was required of them. While that may be true, it only confirms the point that members of Congress who voted for the 2017 tax law completely failed to fix our corporate tax system.

It is the job of lawmakers to enact an equitable tax system requiring corporations to pay their fair share. This requires ending several special breaks and loopholes from the tax code. Some presidential candidates have been more specific than others about how they would do this.

One category of corporate tax breaks is the provision taxing the offshore profits of American corporations less than their domestic profits. This encourages companies to use accounting gimmicks that make U.S. profits appear to be earned elsewhere or to move operations and jobs offshore Several candidates have plans to address this, and the strongest of them would simplify the tax code by taxing offshore profits at the same rate as domestic profits.

Another category of corporate tax breaks is the provision for accelerated depreciation. One of the most overlooked tax breaks, accelerated depreciation gives companies the ability to write off purchases of equipment more quickly than it wears out. TCJA took this further by allowing “full expensing” which allows businesses to write off the entire cost in the same year it is purchased. Proponents argue that this encourages investment, but the reality is it mainly rewards investment that would have happened anyway. Sen. Sanders is the only candidate who has addressed accelerated depreciation at the time of this writing.

A straightforward approach to real tax reform would wipe out most or all of these tax breaks. Another approach that has promise is a proposal by Sen. Elizabeth Warren to base part of the corporate tax rate on profits that companies disclose to shareholders and the public. This means that a corporation using various breaks and loopholes to report little or nothing in income to the IRS would nonetheless pay taxes if it reports profits to shareholders and potential investors.

If the next president and Congress want to raise adequate revenue, they will need a comprehensive tax plan that shuts down special breaks and loopholes for corporations and the wealthy. While some presidential candidates have provided detailed proposals along these lines, we look forward to seeing the rest fill in the blanks on how they plan to achieve real corporate tax reform.