After the 2017 tax law capped state and local tax (SALT) deductions from federal taxes at $10,000, several states responded by attempting to create workarounds that would allow their residents to avoid the cap. These workarounds included maneuvers such as classifying SALT payments as charitable contributions.

Last summer, the Trump Administration responded to these machinations with proposed regulations that would prevent these workarounds. It also proposed addressing a very similar, longstanding tax shelter that allows taxpayers who “donate” to private school voucher programs to turn a profit by reaping tax cuts larger than their donations. Both types of programs operate in the same basic way, and, in fact, the private school credits are one of the main inspirations behind the recent wave of SALT cap workaround proposals. ITEP and others commended the IRS for proposing even-handed regulations that affect both categories of state policy.

Now, we’re likely only days away from the unveiling of the final version of these regulations.

Under the draft regulations, taxpayers would no longer be allowed to write off the portion of any so-called charitable “donation” that states ultimately reimburse with tax credits. The draft regulations also would sensibly address the new tax credits that some “blue states” are offering for donations to fund public services and longer-running credits such as those offered by mostly red states for donations to private K-12 schools. The latter have been used to dodge SALT deduction limits for many years: even before Congress enacted the $10,000 cap, SALT deductions were limited under the Alternative Minimum Tax (AMT). By helping high-income taxpayers dodge the AMT, these private school credits acted as a profitable tax shelter and accelerated the movement of public funds into private schools.

While the details can be complex, the core principle is not. Tax deductions for charitable giving are supposed to reward genuine gifts, and if your state or local government is reimbursing you for your gift then the payment you made is not truly charitable.

With that broad principle in mind, here are some of the finer points we’ll be watching for when the final regulations are made public:

- Did private school groups win a carveout for themselves? There is no doubt that the final regulations will crack down on taxpayers receiving state tax credits in return for donating to public institutions. But some members of the private school community have requested that the IRS turn a blind eye to donations made to non-public institutions, such as nonprofits that distribute private K-12 school vouchers. As ITEP explained in its official comments, such a carveout would be inequitable and would undermine the IRS’s ability to prevent SALT cap avoidance.

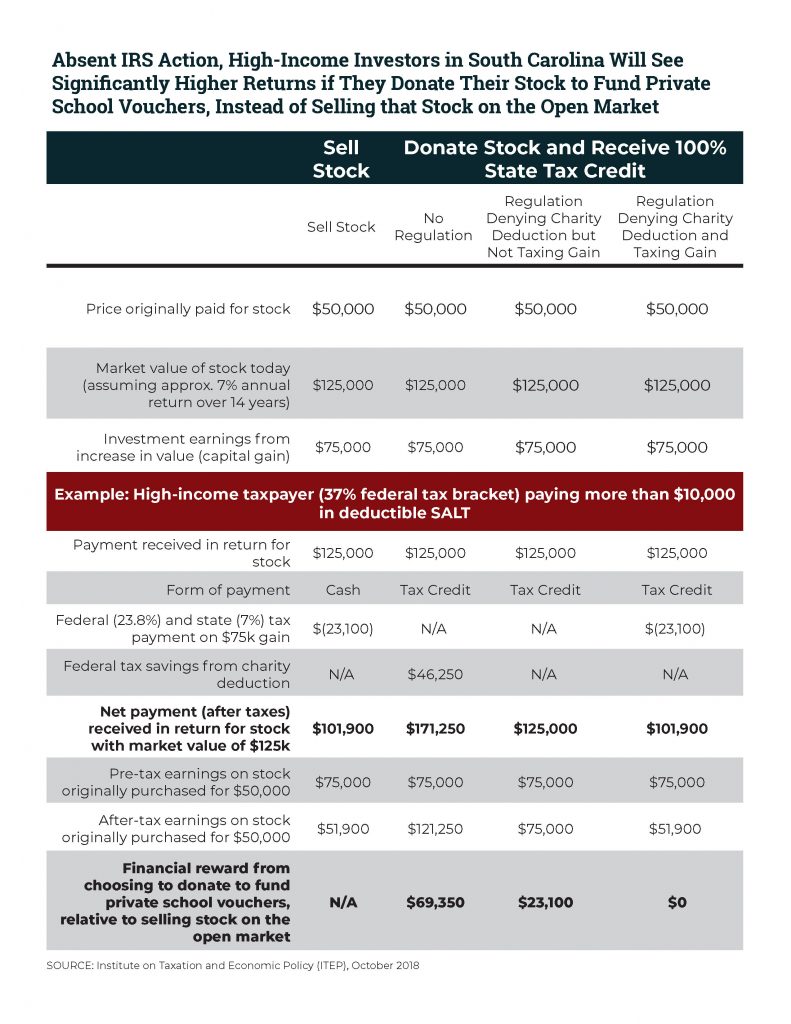

- Do the regulations prevent investors from using state tax credits to dodge taxes on their earnings? The draft regulations were silent regarding how donations of appreciated property should be treated when those donations trigger a sizeable state tax credit. Investors in states such as South Carolina and Virginia have been able to dodge capital gains taxes for many years by “donating” stock or other property to private school groups in exchange for tax credits. ITEP recommended that the IRS treat these taxpayers as if they are selling their stock because failing to do so creates a perverse incentive in which investors looking to cash in will find that “giving” their stock away to private schools (in exchange for tax credits) is a smarter financial move than selling that same stock on the open market (in exchange for cash).

- Will profiteering continue, albeit on a smaller scale, under a weakened de minimis rule? To simplify matters, the draft IRS proposal would exempt smaller state and local tax credits–those worth less than 15 percent of the amount donated–from the scope of these regulations. Some private school groups proposed weakening that rule so that the first 15 percent of any credit would be exempted. In practice, this change would allow a taxpayer receiving a full reimbursement of their donation (via a 100 percent state tax credit) to write-off 15 percent of the amount donated as a federal charitable deduction. This extra federal tax break, on top of the state tax credit, would reopen the door to profiteering as some taxpayers would find that donating would, once again, trigger tax cuts larger than the amount donated.

- When do the regulations take effect? As drafted, the regulations are scheduled to apply to donations made after August 27, 2018. This means that existing credits were likely effective as SALT cap workarounds for the first eight months of 2018–including in states such as Arizona and Alabama where private school credits were claimed in record time by opportunistic taxpayers. Some private school groups urged delaying the effective date and it remains to be seen how the IRS will respond.

This is by no means a comprehensive list of the regulations’ important features. And with a court challenge of the regulations likely to come from New Jersey, even the smallest of details could be important in ensuring the regulations’ longevity. We’ll be taking a close look at those details as soon as the final regulations are unveiled and will have more to say in this space once that happens.