This is the third installment of our six-part series on 2017 state tax trends. The introduction to this series is available here.

As we described last week, many states are gearing up for challenging budget debates this year. But the need to address revenue shortfalls has not stopped lawmakers in many states from pursuing harmful tax policies that will drain critical revenues from state coffers and make upside-down state and local tax systems more regressive, leaving low- and middle-income earners paying more to finance tax cuts for the wealthy. At the same time, however, lawmakers in a handful of states are exploring meaningful income tax reforms that could improve the fairness and sustainability of their tax systems.

Efforts to Eliminate State Personal Income Taxes

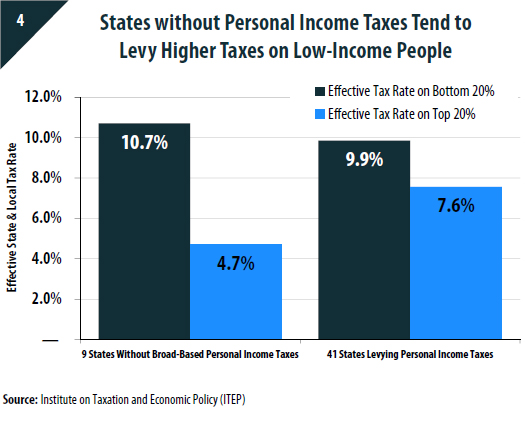

Debates over personal income tax elimination are gearing up in both Michigan and West Virginia this year. Repealing this vital revenue source would impede these states’ ability to balance their budgets in the long run, and would make their tax systems more regressive. This is particularly problematic because both states already have upside-down tax systems under which the highest effective tax rates are levied on the lowest-income taxpayers.

State personal income taxes are a powerful counterbalance to the regressive nature of most other state and local taxes. As revealed in our Fairness Matters chart book, states without personal income taxes tend to be “high tax” for poor people despite their reputations as being “low tax” states.

Two bills to eliminate Michigan‘s personal income tax may be at play this legislative session. In the House, a bill has been filed that would reduce the current income tax rate from 4.25 percent to 3.9 percent in 2018 and then phase down the rate by 0.1 percentage point each year over the next 40 years, well after all of the state’s current elected officials have left office (Michigan prevents any individual from serving more than 14 years in the legislature). A state senator has also indicated that he will introduce a bill that eliminates the personal income tax within a five-year period. Neither proposal is coupled with tax increases to replace the $9 billion (more than one third of the state’s total tax revenue) currently generated through the personal income tax.

West Virginia‘s Senate created a select committee to examine state taxes and explore comprehensive tax reform. According to the committee’s chairman, the legislature is exploring steps to eliminate West Virginians state personal income tax. The committee announced this despite a projected deficit of nearly $500 million that is expected to grow to $700 million by 2019.

A Push Toward Flat Rate Personal Income Taxes

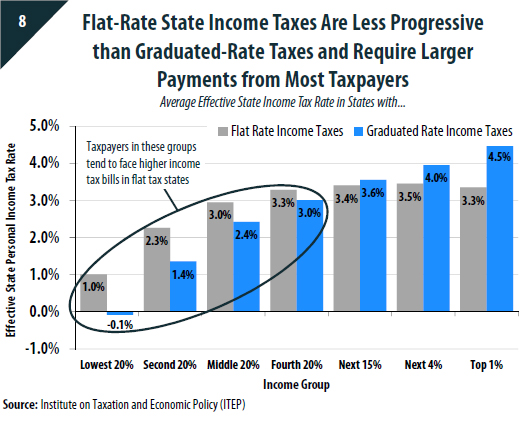

Graduated-rate income taxes allow states to collect more revenues from high-income taxpayers that often face the lowest overall state and local tax rates. The revenue these taxes generate from the wealthy also typically allow states to levy lower rates on low- and moderate-income families less able to afford a higher tax bill, as ITEP’s chart book shows. Yet despite these benefits, lawmakers in Alabama, Arizona, Iowa, Kentucky, Maine, Maryland, Ohio, and South Carolina are considering converting their graduated income taxes to a single flat rate under the guise of tax fairness. In reality, there’s nothing fair about a flat tax.

The Task Force on Budget Reform in Alabama has not released its findings and may not do so for another year, but it has reportedly discussed flattening or even eliminating the state’s income tax. Arizona lawmakers, heeding recommendations from the state’s Joint Task Force on Income Tax Reform, continue to strive toward condensing their moderately progressive, five bracket income tax to a flat rate tax. In Georgia, it remains to be seen whether an attempt to flatten or eliminate the state’s income tax will resurface this year after advocates defeated two such proposals last year. Tax reform is also a topic likely to be broached by lawmakers in Kentucky this year, with efforts to flatten or otherwise reduce the personal income tax playing a central role in that discussion. And in South Carolina, a House Tax Policy Review Committee has been looking into a potential 5 percent flat tax.

The main proposals under consideration range from outright tax cuts to revenue neutral swaps or shifts that would change what most income groups pay in taxes. In most cases, “tax shifts” are designed to transfer revenues away from progressive forms of taxation and toward more regressive options, leaving low- and middle-income earners paying more to finance tax cuts for the wealthy.

Maine’s Gov. Paul LePage has proposed shifting the state to a flat rate personal income tax of 5.75 percent by 2020. Moving to a flat rate is an egregious move on its own, but the governor’s plan also effectively eliminates the 3 percent surcharge on taxable income above $200,000 voters approved at the ballot box just months ago. How? His plan first calls for a flat rate of 2.75 percent and then redesigns that 3 percent surcharge to apply to all taxable income, for a combined overall rate of 5.75 percent. The biggest beneficiaries, by far, of his flat tax plan are the state’s wealthiest residents. In fact, the average lower-income taxpayer will pay more in taxes under this plan because it also increases the sales tax.

In Ohio, a joint committee of the Ohio General Assembly has been tasked with recommending how the state can transition to a flat personal income tax rate of 3.5 or 3.75 percent. Policy Matters Ohio recently released a report using ITEP data, Flat tax would mean more taxes for most, that finds that three-quarters of Ohioans would pay more under a flat tax while the affluent would receive the resulting windfall. Gov. John Kasich’s recently released budget proposal does not go quite this far, but it does condense the state’s personal income tax brackets and reduces rates across the board. Ultimately, the plan flattens the state’s income tax and results in a tax shift away from income taxes and toward the sales tax.

Cutting Taxes at All Costs

Many states are taking steps to cut their personal income taxes despite revenue deficiencies. Arkansas lawmakers, for example, recently passed Gov. Asa Hutchinson’s plan to cut $50 million in taxes for those with taxable incomes under $21,000 despite the fact that revenues are under forecast for the first 6 months of this fiscal year. To achieve balance, the governor’s budget proposal includes very optimistic revenue projections, relying on assumptions of robust 4.4 percent growth in general revenues absent any tax increases.

Iowa is another state where income tax cuts are at the top of the agenda for many in the state’s new Republican majority despite a budget shortfall caused largely by prior tax cuts and warnings from the nation’s longest-serving governor that the state cannot afford them.

But cutting taxes when revenues are already down is often unappealing since doing so would exacerbate painful budget cuts. Recently, however, some lawmakers have developed a slick workaround. Instead of proposing cuts that would result in an immediate revenue loss and require offsetting reduction in public services, they instead offer up proposals with triggers or phase-ins – delaying the need to identify what services will be eliminated to fund the tax cut until some later date (perhaps even a date when the lawmakers voting for that tax cut have already left office).

Oklahoma may be the poster child of tax triggers gone awry. Just last year an income tax rate reduction was triggered despite the presence of a budget shortfall and an official “revenue failure.” Reasonably, lawmakers have since questioned the merits of maintaining the trigger.

In Nebraska, despite projected shortfalls of $900 million and $1.2 billion in the state’s next two budget cycles, Gov. Pete Ricketts has proposed to slash taxes for the state’s wealthiest, but delay implementation and slowly phase them in each time the state hits arguably arbitrary revenue targets.

And as mentioned above, Michigan lawmakers – lacking for ideas on how to fund income tax repeal – are hoping that adopting a very slow phase-in schedule may allow them to repeal the tax anyway.

Some Progressive Revenue Ideas Shine Through

While there seems to be an endless stream of proposals to chip away at state personal income taxes, proposals to strengthen the tax, or even create one from scratch, have also surfaced, along with proposals to generate meaningful revenues through other means.

For instance, last year Alaska Gov. Bill Walker proposed reinstating a personal income tax for the first time in more than 35 years to deal with a downturn in oil tax and royalty revenues. While the governor has yet to officially rerelease an income tax plan this year, he recently voiced support for an income tax yet again and there are indications that this year’s fiscal debate will include meaningful discussion of the idea.

In Kansas, advocates have filed a bill to undo many of the harmful changes enacted since Gov. Sam Brownback took office in 2012. Additional tax reforms will also be under consideration by a new coalition in the legislature. The stage is set for tax reform in Louisiana as well, if the political stars can align. The Task Force on Structural Changes in Budget and Tax Policy released its final report last week, including recommendations that the state eliminate regressive exemptions, broaden the sales tax base, and lower the rate.

Governors in Montana, New York, and Washington have introduced progressive revenue-raising ideas to address their lean budgets. In Montana, Gov. Steve Bullock has proposed adding a new top bracket for taxpayers with more than $500,000 in taxable income and limiting a capital gains credit to those with incomes under $1 million. In New York, Gov. Andrew Cuomo’s budget proposal includes a 3-year extension of the state’s millionaires’ tax. New York’s Assembly Speaker Carl Heastie has taken the revenue raising potential of the tax even further, proposing to increase the rates on those earning over $5 million and $10 million annually. Gov. Jay Inslee in Washington has put forward a proposal that would generate an additional $4 billion for public education by raising business and occupation taxes on services, expanding the sales tax base, and levying new taxes on carbon and capital gains, though this ambitious proposal faces an uphill battle in the legislature.

Gearing up for 2018, advocates in Massachusetts are backing a constitutional amendment to create a 4 percent tax surcharge on incomes over $1 million. Receiving strong support in public polling, the millionaires’ tax, also known as the fair share amendment, could go before voters on the state’s 2018 ballot.