Policy Briefs

The Impact of Proposed New Tax Credit Restrictions for Immigrant Filers: An Analysis of the DACA Recipient Population

June 16, 2026 • By Carl Davis, Erika Frankel, Emma Sifre

We find that 337,000 people in households with at least one DACA recipient will suffer financial harm, and that nearly two-thirds (66 percent) of the impacted individuals are U.S. citizens.

The Impact of Proposed New Tax Credit Restrictions for Immigrant Filers: An Analysis of State EITCs

June 16, 2026 • By Neva Butkus

Immigrants and their families in as many as 30 states are at risk of seeing their state tax credits such as the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) reduced unless state lawmakers act.

The ‘Black Women Best’ Framework: An Innovative Method for Showing How Inheritance Taxes Affect the Racial Wealth Gap

May 20, 2026 • By Brakeyshia Samms, Francine Lipman

The approach posits that if policies improve the economic wellbeing of Black women, they will benefit the broader economic health of the rest of the population.

The Next Illegal, Costly Tax Cut for the Rich: Indexing Capital Gains

April 21, 2026 • By Steve Wamhoff

Proposals to index taxes on capital gains for inflation would overwhelmingly benefit the richest 1 percent and increase the deficit by nearly $1 trillion over a decade.

While States Debate New Trump Tax Changes, Equity Must Be at the Core

April 20, 2026 • By Brakeyshia Samms

States continue to debate whether and how to link their state tax codes to the 2025 federal tax law. This is not just a technical debate.

South Carolina’s Expensive, Regressive Tax Law Will Eliminate State’s Income Tax

March 31, 2026 • By Neva Butkus, Dylan Grundman O'Neill

South Carolina signed into law a regressive tax cut that will disproportionately benefit the state’s highest-income residents while simultaneously jeopardizing the state’s ability to pay for basic public services in the years to come.

Travelers’ Checks: How to Tax Tourists in States and Localities

March 30, 2026 • By Rita Jefferson

Taxing tourists is a relatively efficient way to ensure that visitors are paying a share of essential government services. Places with a modest number of tourists should limit general sales tax rates to minimize the effect on the full-time population. Places with higher proportions of tourists may have higher sales tax rates to better capture the economic behavior of tourists.

The recent spike in gasoline prices is on pace to cost American drivers an extra $9.4 billion per month. Gas prices are up dramatically across the country, but the South has been hit hardest and is on pace to pay $4.2 billion more per month.

How Four Big Pro-Trump Tech Companies Avoided Taxes

March 17, 2026 • By Steve Wamhoff, Matthew Gardner

The leaders of Alphabet, Amazon, Meta, and Tesla publicly supported Trump to ensure the most favorable corporate tax policies possible. And Trump delivered for them, both in his 2017 tax bill and again in 2025 with the so-called One Big Beautiful Bill Act.

Sen. Chris Van Hollen has recently introduced the Working Americans’ Tax Cut Act, which offers a generous middle-class tax cut paid for with a new tax on millionaires.

State-by-State Estimates of the First Year of Trump’s Tax Policies: All But the Richest Americans Face Higher Taxes

February 23, 2026 • By Steve Wamhoff, Michael Ettlinger

As a result of the tax policies approved by President Trump and the Republican majority in Congress, all but the richest Americans are paying higher taxes on average in 2026 than they did last year.

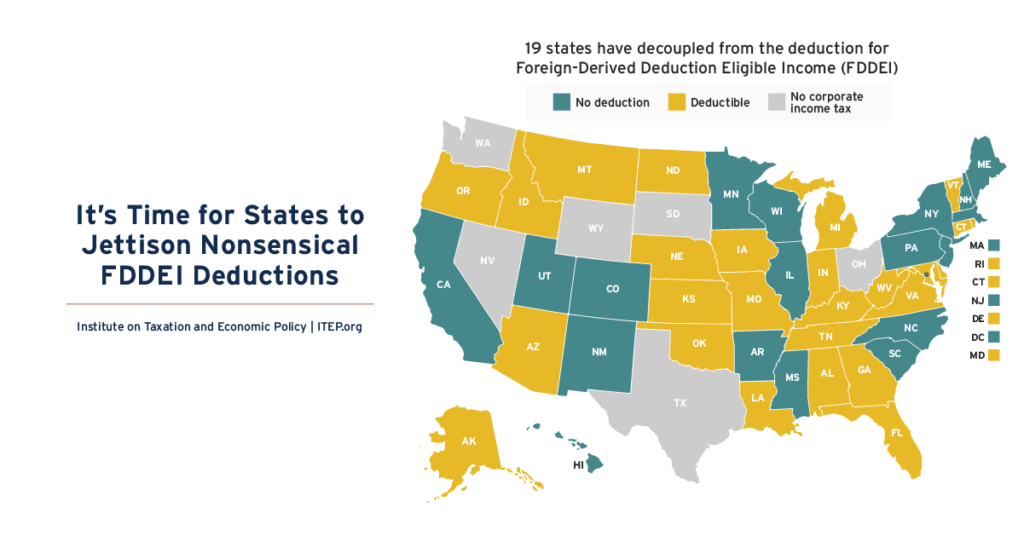

It’s Time for States to Jettison Nonsensical FDDEI Deductions

February 19, 2026 • By Carl Davis

FDDEI deductions should be repealed for policy reasons alone as they do not serve a legitimate purpose at the state level.

Michigan Ballot Proposal Would Boost Public Education While Creating a Fairer Tax System

February 17, 2026 • By Miles Trinidad, Matthew Gardner

A new proposal in Michigan would create a 5-percentage point surcharge on top earners with taxable incomes over $1 million for joint filers and $500,000 for single filers. This would raise about $1.7 billion a year, which would be used for public education priorities.

An Analysis of a Potential Reduction in Massachusetts’ Long-Term Capital Gains Tax Rate

January 26, 2026 • By Eli Byerly-Duke, Matthew Gardner

A ballot initiative in Massachusetts has proposed cutting the base rate for nearly all income sources from 5 to 4 percent. In 2026, this would cost the state about $5 billion per year of which $347 million would come from the reduced rate on long-term capital gains.

10 Reasons Why the U.S. Should Reform Its Corporate Income Tax

December 17, 2025 • By Steve Wamhoff

The U.S. needs a tax code that is more progressive and that raises more revenue than the one we have now. An important way to achieve this is to reform the taxation of business profits.

Tax Haven Data Demonstrate Need for Global Minimum Tax Despite Opposition from Trump Administration

December 10, 2025 • By Steve Wamhoff

American corporations use accounting gimmicks to make profits appear to be earned in tax havens. This widespread problem could be fixed by Congress enacting legislation to implement a minimum tax on corporations that meets the standards of the global minimum tax that other countries have begun to implement.

Linking to Tipped and Overtime Income Deductions Would Worsen State Shortfalls, Do Little to Help Workers

December 8, 2025 • By Neva Butkus, Galen Hendricks

State deductions for tips and overtime are not only ineffective at supporting working-class people, it will come at a substantial cost to state budgets.

Re-Examining 529 Plans: Stopping State Subsidies to Private Schools After New Trump Tax Law

November 20, 2025 • By Miles Trinidad, Nick Johnson

The 2025 federal tax law risks making 529 plans more costly for states by increasing tax avoidance and allowing wealthy families to use these funds for private and religious K-12 schools.

State Tax Dollars Shouldn’t Subsidize Federal Opportunity Zones

November 12, 2025 • By Eli Byerly-Duke

The Opportunity Zones program benefits wealthy investors more than it benefits disadvantaged communities.

The 5 Biggest State Tax Cuts for Millionaires this Year

October 16, 2025 • By Dylan Grundman O'Neill, Aidan Davis

Some states continue to hand out huge tax cuts to millionaires. The five largest tax cuts this year will cost states a total of $2.2 billion per year once fully implemented.

Quite Some BS: Expanded ‘QSBS’ Giveaway in Trump Tax Law Threatens State Revenues and Enriches the Wealthy

October 2, 2025 • By Sarah Austin, Nick Johnson

States should decouple from the federal Qualified Small Business Stock (QSBS) exemption.

IRS Enforcement Boost Was Supposed to Last 10 Years. Congress Killed It in Under Three.

September 16, 2025 • By Sarah C. G. Christopherson

The IRS was set to overhaul how it audits the ultra-rich. Now most of that funding is gone.

State Earned Income Tax Credits Support Families and Workers in 2025

September 11, 2025 • By Neva Butkus

Nearly two-thirds of states now have an Earned Income Tax Credit (EITC). Momentum continues to build on these credits that boost low-paid workers’ incomes and offset some of the taxes they pay, helping lower-income families achieve greater economic security.

State Child Tax Credits Boosted Financial Security for Families and Children in 2025

September 11, 2025 • By Neva Butkus

Child Tax Credits (CTCs) are effective tools to bolster the economic security of low- and middle-income families and position the next generation for success.

Sales Tax Holidays Miss the Mark When it Comes to Effective Sales Tax Reform

July 17, 2025 • By Miles Trinidad

Sales tax holidays are often marketed as relief for everyday families, but they do little to address the deeper inequities of regressive sales taxes. In 2025, 18 states offer these holidays at a collective cost of $1.3 billion.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.