The ITEP Guide to State & Local Taxes

Property & Wealth

How Do Real Property Taxes Work?

Property taxes on land and buildings are the oldest and still the largest major revenue source for state and local governments. They fund schools, health care, public safety, and other services. They are collected mostly by cities, counties, school districts, and other types of local government, but states typically make the rules for assessing the value of property and imposing the tax, with major implications for tax fairness and adequacy.

How Do Personal Property Taxes Work?

The great majority of property tax revenue is based on the value of land and buildings, but states also apply property taxes to certain business equipment, machinery, and supplies, and sometimes also to automobiles. Collectively these taxes are known as “personal property taxes.”

How Do State Estate and Inheritance Taxes Work?

Estate and inheritance taxes are taxes on wealth passed on after someone’s death. They are a common way for states to tax the inheritances of wealthy individuals. These taxes ensure that those very large estates help pay for public services like schools, hospitals, and parks.

How Can Communities Collect Property Taxes from Exempt Nonprofits?

Payment in Lieu of Taxes (PILT or PILOT) programs allow local governments to collect revenue from nonprofits that otherwise would not be contributing to the cost of providing local services.

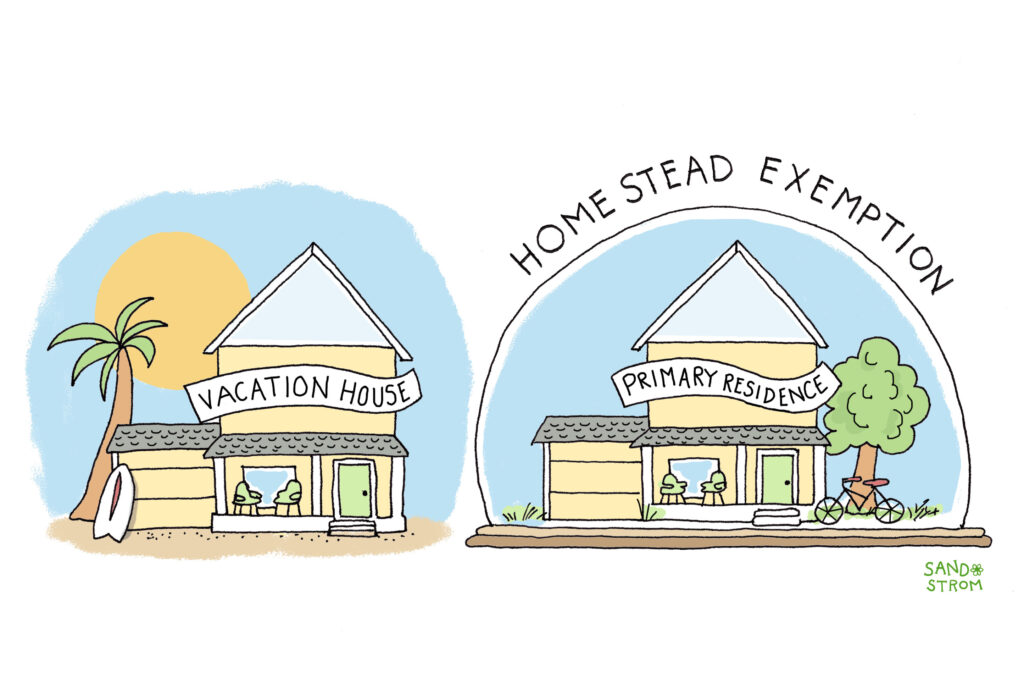

How Can Cities and States Reduce Property Taxes for Homeowners and Renters?

To reduce the cost of property taxes for homeowners and renters, many places offer homestead exemptions, circuit breakers, and deferrals. Such provisions are more cost-effective alternatives to broad tax cuts or tax limitations.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.