Since 2013, the Federal Reserve has released an annual survey on family economic wellbeing that, among other things, asks respondents whether they could cover a $400 emergency expense. The latest survey released in May revealed that nearly 40 percent of people say they either couldn’t or would struggle to pay.

In the weeks following, conservative thinkers attempted to undermine this truth, arguing that the survey results aren’t so bad because most of those four in 10 conceded that they could rack up credit card debt or borrow via a personal loan, family or friends to fund an emergency. The 12 percent of people who flat out couldn’t pay for an emergency are an inconsequential few, these “think” pieces dismissively argued. Amplifying these ideological beliefs via news outlets intends to set a low bar for how the vast majority of us perceive poverty or financial hardship by equating having a few material comforts or access to consumer debt with relative economic security.

In the same spirit, op-eds in prominent publications this week distorted newly released Census data on poverty, income and health insurance coverage to challenge the prevailing (and correct) narrative that economic inequality is a challenge in the United States. One particularly misleading op-ed arrogantly argued, “Poverty is best viewed as an absolute phenomenon, not a relative one. Your quality of life is not harmed at all by someone else’s great wealth, as their wealth was almost certainly not gathered at your expense.”

Maintaining the myth that this nation is an absolute meritocracy and that low-income people don’t have it so bad and simply need to work harder if they want to share in economic prosperity is necessary to keep the status quo. If a broad swath of the public ascribes to a belief system that sets an extremely low bar for economic success (e.g. you’re not homeless and you ate today, so you’re fine), then it will be easier for special interests and their political allies who seek to dismantle or weaken poverty-alleviating programs while continuing to cut taxes for corporations and the wealthy to be successful in their mission.

The political class is aware the aforementioned is a deeply unpopular agenda, which is precisely why proposals to cut spending on safety net programs are often shrouded in euphemistic language about economic prosperity. In its first year, the Trump Administration released an FY2018 budget proposal (A New Foundation for American Greatness) that called for deep cuts to spending on discretionary programs. Then, in July 2018, it declared the five-decade war on poverty is over and “largely a success,” to justify its desire to slash spending on programs it deems “welfare” by imposing strict, often unrealistic work requirements. And in its most sinister move of all, the White House three months ago issued a proposed regulation that would slow the rate at which the federal poverty threshold increases, eventually resulting in millions fewer being eligible for means-tested programs (eligibility determined based on a poverty-based formula). The proposed regulation would move the goalposts to assure an illusory poverty-reduction win but do nothing to help more families move out of poverty.

The White House already proved its cynical intentions by weakening the Affordable Care Act, which vastly improved health insurance coverage. The 2017 Trump-GOP tax law repealed the individual mandate for health insurance coverage, and in 2018, it had its intended result. While that change did not go into effect until this year, publicity around that change (as well as the administration’s decision to reduce funding for enrollment assistance) is widely believed to have contributed to the drop in coverage.

None of this is consistent with a sincere desire to improve family wellbeing. A closer look at the 2018 Census poverty and income data reveals why this is the wrong agenda for the nation’s families.

From 2017 to 2018, the percent of people living in poverty declined for the fourth consecutive year and is now lower than it was in 2007, just before the Great Recession. Data reveal 11.8 percent of the U.S. population, or 38.1 million people, fall below the official federal poverty threshold. Key federal programs lift millions out of poverty each year. The Supplemental Nutrition Assistance Program (SNAP) lifted 3.1 million people out of poverty in 2018. Rental assistance helped 3 million people move out of poverty. Refundable tax credits are highly effective government programs, lifting 7.9 million people out of poverty in 2018.

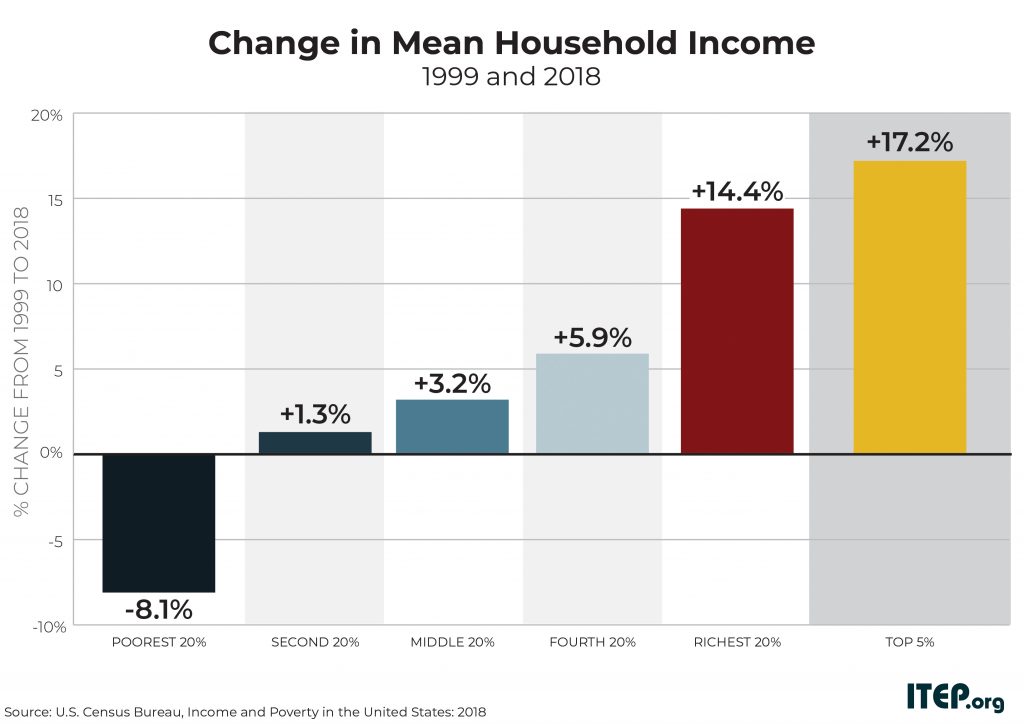

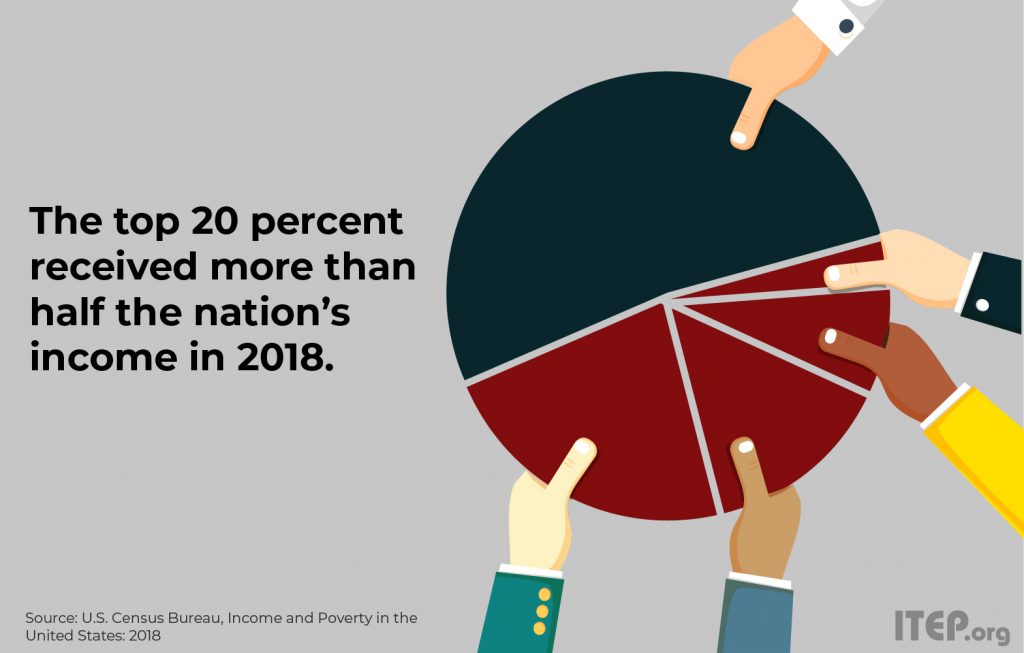

The overall decline in poverty certainly is positive news but doesn’t justify an assault on programs that boost family economic security. “Mission accomplished” or the war on poverty is “largely a success” only if the nation sets an extremely low bar for what widespread economic opportunity should look like. A broader examination of Census income data shows that nearly one in three (28.9 percent) are poor or low-income (200 percent or less of the federal poverty level).

Our elected officials should pause and check the pulse of the nation. The public is aware of the great income divide and likely isn’t keen on an agenda that would use sleight of hand to “reduce” poverty and spend less on domestic programs—particularly when that agenda is in tandem with using the tax code to further boost income for the wealthy.

A decrease in poverty is the very least we can expect from an economy that has entered its 11th year of recovery. To be clear, programs that help families put food on the table and keep a roof over their heads continue to play a substantial role in that achievement. Slashing spending on programs that help poor and moderate-income families—who, frankly, still haven’t benefited as much from economic growth as those families at the top—would mean even less economic security for families who already struggle to pay a $400 emergency expense.