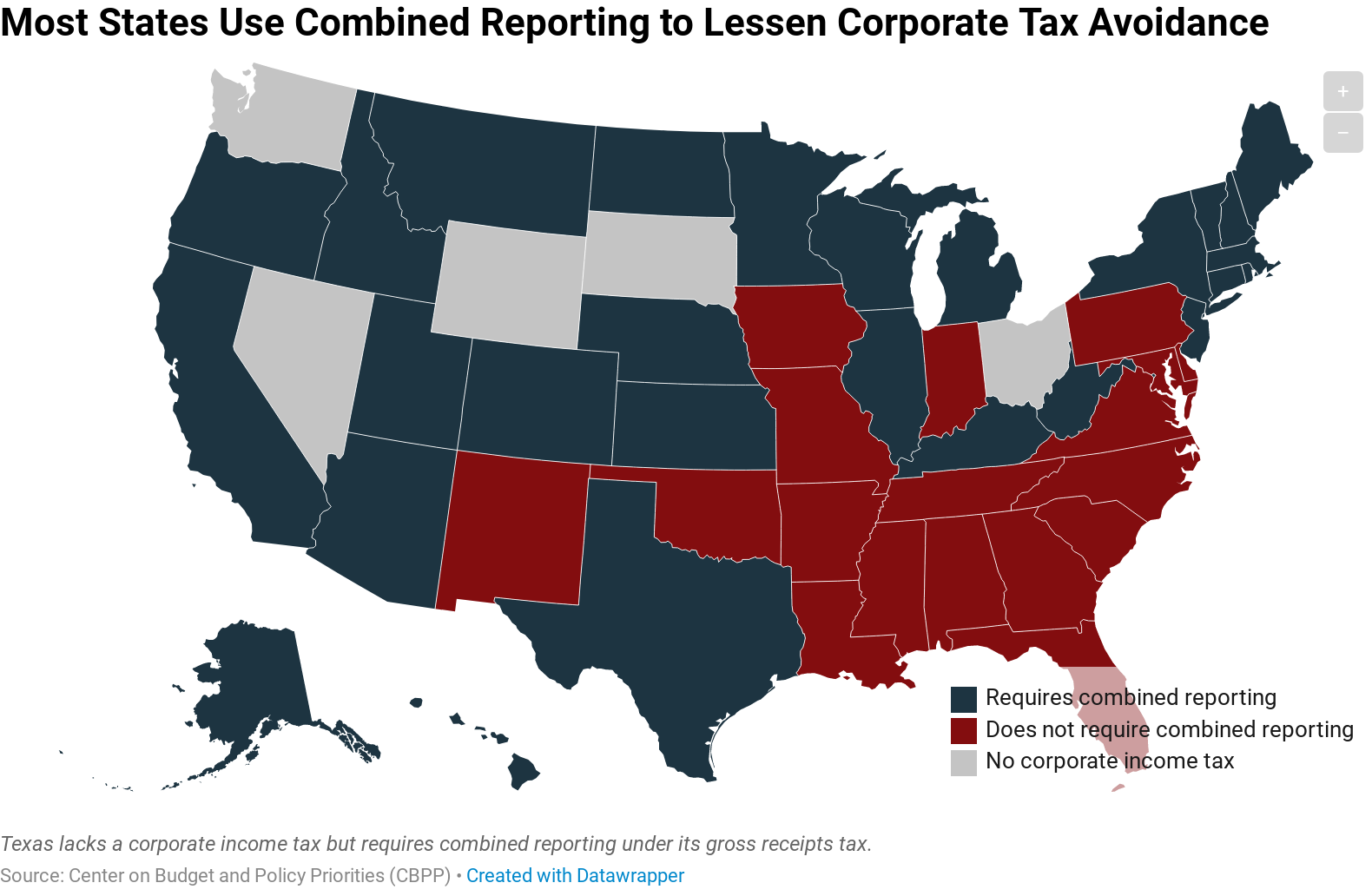

“Combined reporting” lessens the effectiveness of a tax avoidance scheme known as income shifting, in which large multi-state corporations dubiously claim that their income was earned in states with little or no corporate income tax. Twenty-seven states and the District of Columbia require combined reporting. Under combined reporting each company and its subsidiaries are treated as one combined entity for state income tax purposes, thereby removing the incentive for companies to tell state tax collectors that their profits were earned by out-of-state subsidiaries that those collectors cannot otherwise reach.

Read More: Combined Reporting of State Corporate Income Taxes: A Primer (February 2017)

{kind=link}