Conformity

Most states use the federal tax code as a starting point for their calculations of state personal income taxes, corporate income taxes, and estate taxes.

State Rundown 3/18: New Mexico Enacts Most Significant Corporate Tax Reform of the Year

March 18, 2026 • By ITEP Staff

As states lawmakers continue to weigh their linkages to the federal tax code in light of the recent federal tax law, New Mexico provides a blueprint for limiting multinational corporate tax avoidance.

States Should Be Doing More About Corporate Tax Avoidance. New Mexico’s Tax Conformity Law Shows How.

March 17, 2026 • By Carl Davis

On top of declining to fold large federal business tax cuts into state law, New Mexico also took the monumental step of hardening the state’s corporate tax base against offshore profit shifting.

State Rundown 3/12: Washington Lawmakers Pass Millionaires’ Tax, Expand Working Families Tax Credit

March 12, 2026 • By ITEP Staff

Washington is on its way to making history after the legislature approved the “millionaires’ tax,” a 9.9 percent tax on income over $1 million. The bill, which is expected to raise more than $3 billion a year, making significant investments in public education and childcare, will also expand the Working Families Tax Credit – the […]

Testimony: ITEP’s Marco Guzman Outlines Positive Tax Reform Proposals for Colorado Lawmakers

March 10, 2026

This testimony was delivered to the Colorado House Finance Committee on March 9, 2026. You can watch video of the testimony here (Marco starts around the 6:12:40 PM mark). My name is Marco Guzman, and I am a Senior Analyst at the Institute on Taxation and Economic Policy (ITEP). ITEP is a non-profit, non-partisan tax […]

Governor Should Put New Mexico’s Tax Interests First

March 6, 2026 • By Amy Hanauer, Amber Wallin

By decoupling from three misguided federal corporate income tax cuts under the One Big Beautiful Bill, plus taking steps to curb unfair corporate tax avoidance, SB 151 would raise and safeguard more than $120 million annually.

As many state legislative sessions near or cross the halfway point, lawmakers are facing tough choices.

Testimony: ITEP’s Miles Trinidad Urges Maryland Lawmakers to Decouple from Tax Breaks for Opportunity Zones and FDEII

March 3, 2026

Chair, Vice Chair, and Members of the Committee, Thank you for the opportunity to submit testimony in support of House Bill 1080, which would decouple the state from federal tax breaks for Opportunity Zones (OZs) and Foreign-Derived Deduction Eligible Income (FDEII). My name is Miles Trinidad, and I am a state analyst with the Institute on Taxation and Economic Policy (ITEP), […]

Testimony: ITEP’s Miles Trinidad Urges Maryland Lawmakers to Decouple from Expanded 529 Education Savings Plans and Not Opt-In to New Private School Voucher Program

March 3, 2026

This testimony was delivered to the Maryland House Ways and Means Committee on February 26, 2026 Chair, Vice Chair, and Members of the Committee, Thank you for the opportunity to submit testimony in support of House Bill 930, which would decouple Maryland’s tax code from recent federal expansions of 529 education savings plans as they related to private K-12 tuition, and would ensure […]

Testimony: ITEP’s Miles Trinidad Urges Maryland Lawmakers to Decouple from Increased SALT Cap

March 3, 2026

This testimony was delivered to the Maryland House Ways and Means Committee on February 26, 2026 Chair, Vice Chair, and Members of the Committee, Thank you for the opportunity to submit testimony in support of House Bill 926, which would decouple Maryland from recent federal increases to the cap on state and local tax (SALT) deductions. My name is Miles Trinidad, […]

Testimony: ITEP’s Miles Trinidad Urges Maryland Lawmakers to Decouple from Bonus Depreciation and Business Interest Deductions

March 3, 2026

This testimony was delivered to the Maryland House Ways and Means Committee on February 26, 2026 Chair, Vice Chair, and Members of the Committee, Thank you for the opportunity to submit testimony in support of House Bill 880, which would decouple Maryland from federal corporate tax changes on the expanded bonus depreciation and business interest deductions. My name is […]

Testimony: ITEP’s Miles Trinidad on Decoupling from the QSBS Exclusion Before the Maryland House Ways and Means Committee

February 27, 2026

This testimony was delivered to the Maryland House Ways and Means Committee on February 26, 2026. Chair, Vice-Chair, and Members of the Committee, Thank you for the opportunity to provide testimony in support of House Bill 801. My name is Miles Trinidad, and I am an analyst at the Institute on Taxation and Economic Policy […]

Testimony: ITEP’s Marco Guzman Details a Package of Tax Bills for the Connecticut General Assembly Finance Committee

February 27, 2026

This testimony was delivered to the Connecticut General Assembly Finance Committee on February 26, 2026. My name is Marco Guzman, and I am a Senior Analyst at the Institute on Taxation and Economic Policy (ITEP). ITEP is a non-profit, non-partisan tax policy organization, conducting rigorous analyses of tax and economic proposals and providing data-driven recommendations […]

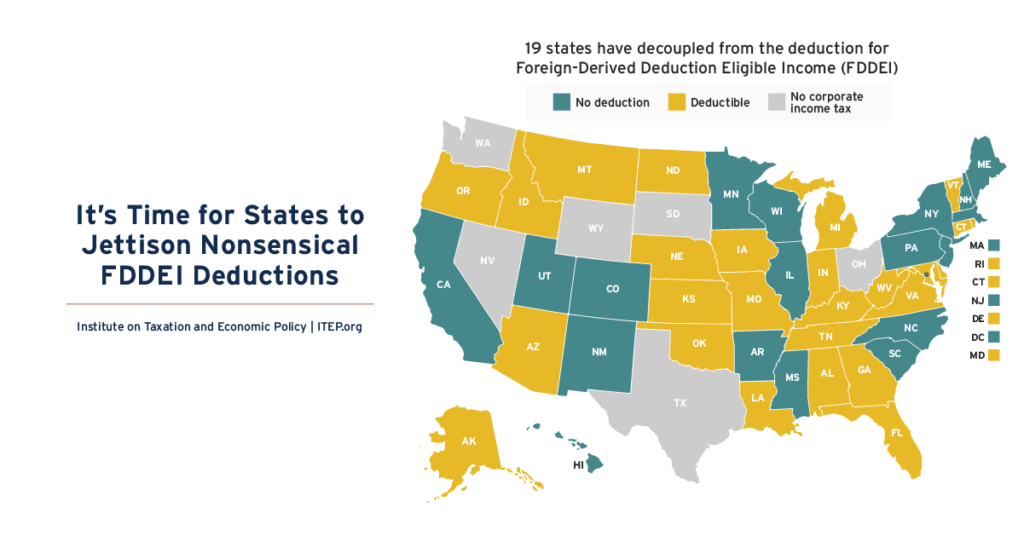

It’s Time for States to Jettison Nonsensical FDDEI Deductions

February 19, 2026 • By Carl Davis

FDDEI deductions should be repealed for policy reasons alone as they do not serve a legitimate purpose at the state level.

NCTI is an Important Part of the Federal Corporate Tax. States Should Adopt It Too.

February 12, 2026 • By Carl Davis

Including NCTI in state corporate tax law is an effective way to neutralize much of the tax avoidance that occurs when multinational companies artificially shift their profits into overseas tax havens.

What Did 2025 State Tax Changes Mean for Racial and Economic Equity?

February 9, 2026 • By Brakeyshia Samms

The results are a mixed bag, with some states enacting promising policies that will improve tax equity and others going in the opposite direction.

D.C.’s Fiscal Autonomy is at Stake, District’s Conformity Decisions Should Stand

February 6, 2026 • By Kamolika Das

Federal lawmakers passed a bill along party lines that would force the District of Columbia to override the decision of local elected officials and implement all of the costly and inequitable federal tax cuts passed under the “One Big Beautiful Bill Act” (OBBBA).

Testimony: ITEP’s Carl Davis on Federal/State Tax Conformity at Pair of Vermont Committee Hearings

February 3, 2026

ITEP Research Director Carl Davis testified on the impact of the 2025 tax law on Vermont on January 15, 2026 at the Vermont House Ways & Means Committee and the Vermont Senate Committee on Finance. See the slide deck here Watch the videos here (House) and here (Senate) See all of our resources on conformity […]

Testimony: ITEP’s Sarah Austin Urges Washington House Finance Committee to Decouple from Venture Capital Tax Break

January 28, 2026

The prepared testimony below was delivered by ITEP Senior Analyst Sarah Austin to the Washington House Finance Committee on January 27, 2026. For more on the tax break in question, check out our October 2025 brief. Chair Berg, Vice Chair Street, and members of the House Finance Committee, My name is Sarah Austin, I’m a […]

States Can Push Back Against Reckless Federal Tax Policy. Here’s How.

January 22, 2026 • By Aidan Davis, Wesley Tharpe

They should take steps to protect and boost their own revenues. And they should take a second look at their own tax cuts.

Curbing Tax Deductions for Executive Pay is a Federal Tax Change States Should Get Behind

January 9, 2026 • By Matthew Gardner

This provision in last summer’s tax law could actually make budget-balancing a little bit easier for states if they follow suit.

From Congressional discussions over the so-called "One Big Beautiful Bill Act" to debates on property taxes, ITEP kept busy this year analyzing tax proposals and showing Americans across the country how tax decisions affect them.

States Can Create or Expand Refundable Credits by Taxing Wealth, Addressing Federal Conformity

December 19, 2025 • By Zachary Sarver

Many states already recognize the potential of these credits to boost low- and moderate-income households. Other states should follow suit.

No, Scott Bessent: States Aren’t Taking Away Anyone’s Tax Cuts

December 11, 2025 • By Nick Johnson

It’s wildly inappropriate for a U.S. Treasury Secretary to lean on states to adopt or not adopt specific federal provisions in their own state tax codes.

Linking to Tipped and Overtime Income Deductions Would Worsen State Shortfalls, Do Little to Help Workers

December 8, 2025 • By Neva Butkus, Galen Hendricks

State deductions for tips and overtime are not only ineffective at supporting working-class people, it will come at a substantial cost to state budgets.

Conforming to the ‘No Tax on Tips’ Gimmick Just Got Riskier and Costlier for States

November 25, 2025 • By Nick Johnson

An unknown number of workers who previously were assumed to be ineligible for the tax break may nonetheless claim it.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.