Key findings

• The trio of tax bills that House Republicans will consider in committee on Tuesday, June 13, include tax cuts that would mostly benefit the richest one percent of Americans and foreign investors.

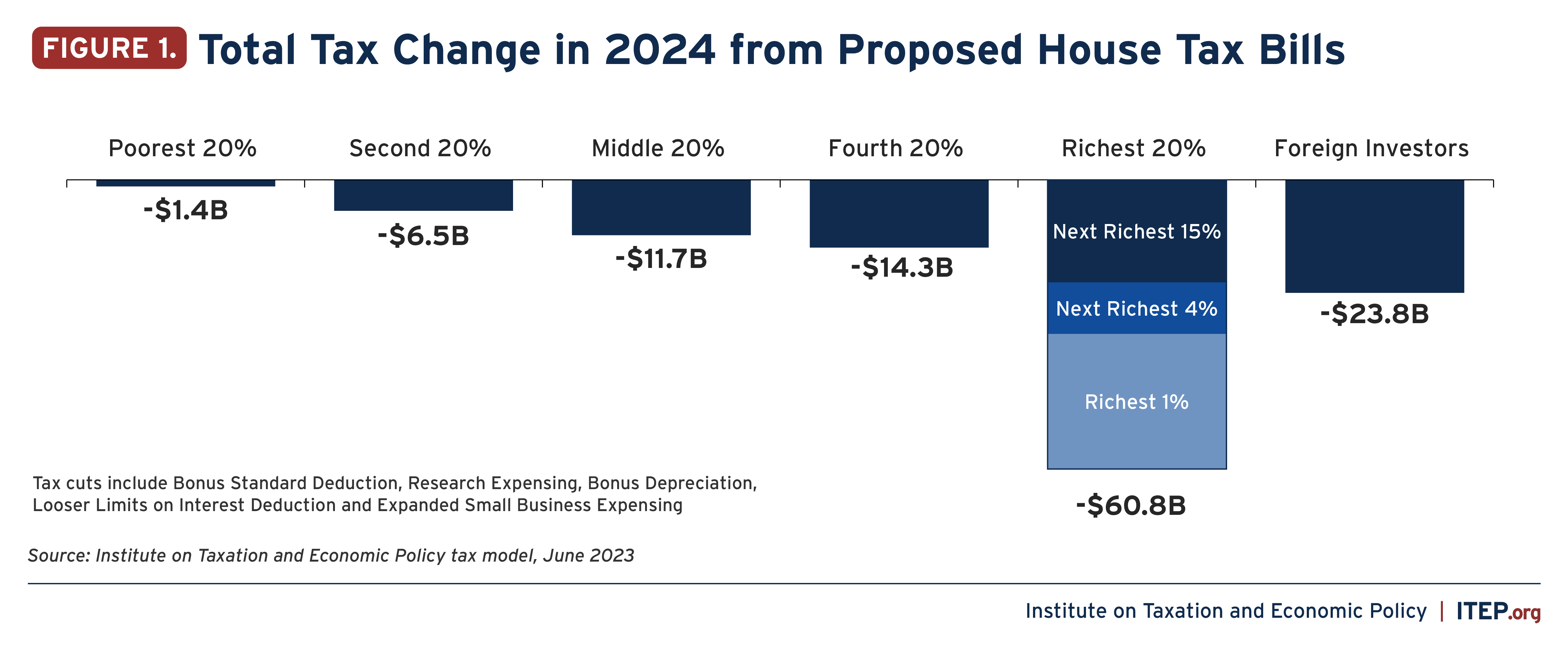

• Under the legislation, the richest fifth of Americans would receive $60.8 billion in tax cuts next year while the poorest fifth of Americans would receive $1.4 billion in tax cuts.

• Because foreign investors own much of the stock in U.S. corporations, they would ultimately receive $23.8 billion of the corporate tax cuts next year.

• The only group of Americans receiving more than foreign investors next year would be the richest 1 percent, who would receive $28.4 billion.

• The legislation includes an increase in the standard deduction that would help some middle-income taxpayers but would do little for those who most need help.

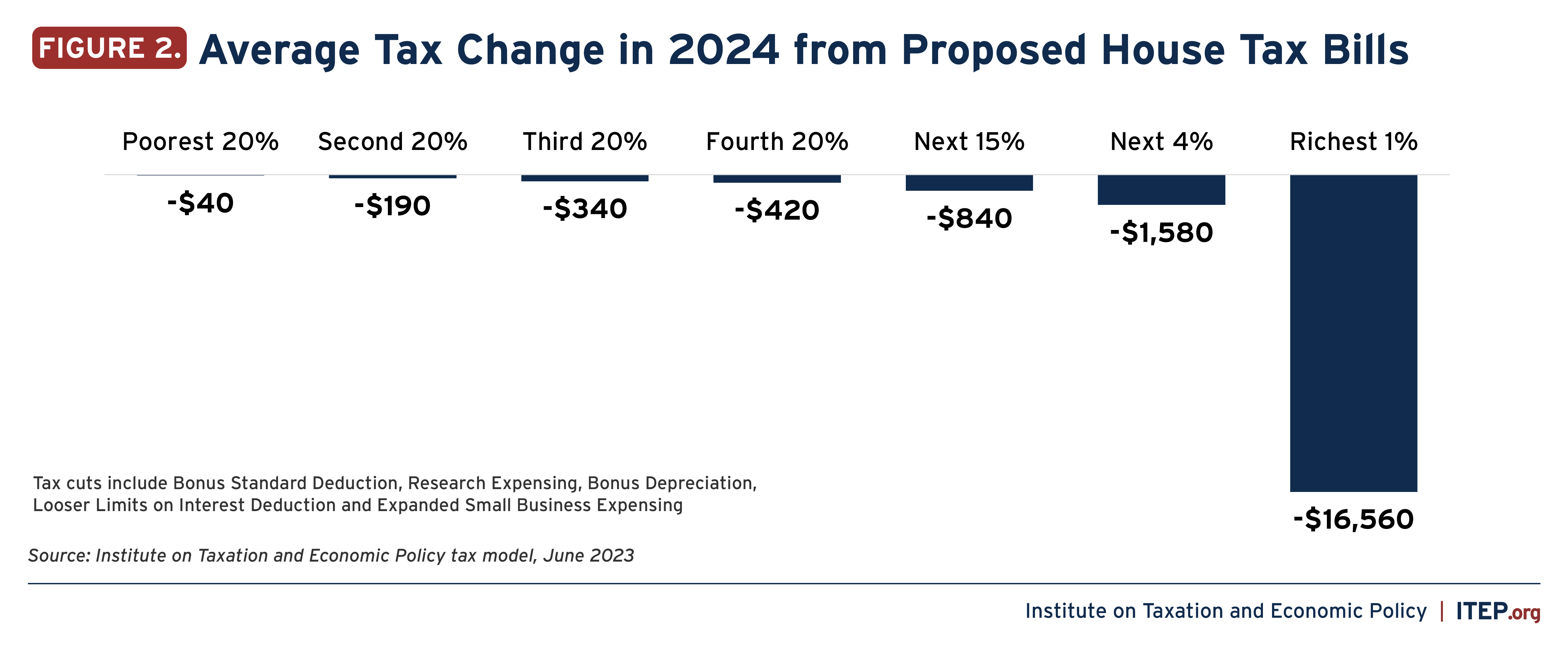

• As a result, the poorest fifth of Americans would receive an average tax cut of just $40 next year while the richest one percent would receive an average $16,550 tax cut next year.

• This analysis does not address who ultimately pays for the revenue-raising provisions (which would repeal clean energy tax credits) because their costs would ultimately fall on everyone in the form of greater climate damage.

Just weeks after threatening to cause a catastrophic default on the federal debt to address an alleged budget crisis, House Republicans plan to consider legislation that would increase the deficit by expanding the Trump tax cuts for corporations and other businesses.

Officially the cost of the new tax cuts would be offset, mostly by provisions that would roll back certain parts of President Biden’s Inflation Reduction Act addressing climate change, but the true costs are hidden by budget gimmicks.

The most important budget gimmick is that the legislation enacts the biggest tax cuts for only two years even though its proponents plan to extend them in the future making them, in effect, permanent. The Committee for a Responsible Federal Budget estimates that if all provisions are permanent, the trio of bills would result in more than $1 trillion in revenue losses over the next ten years.

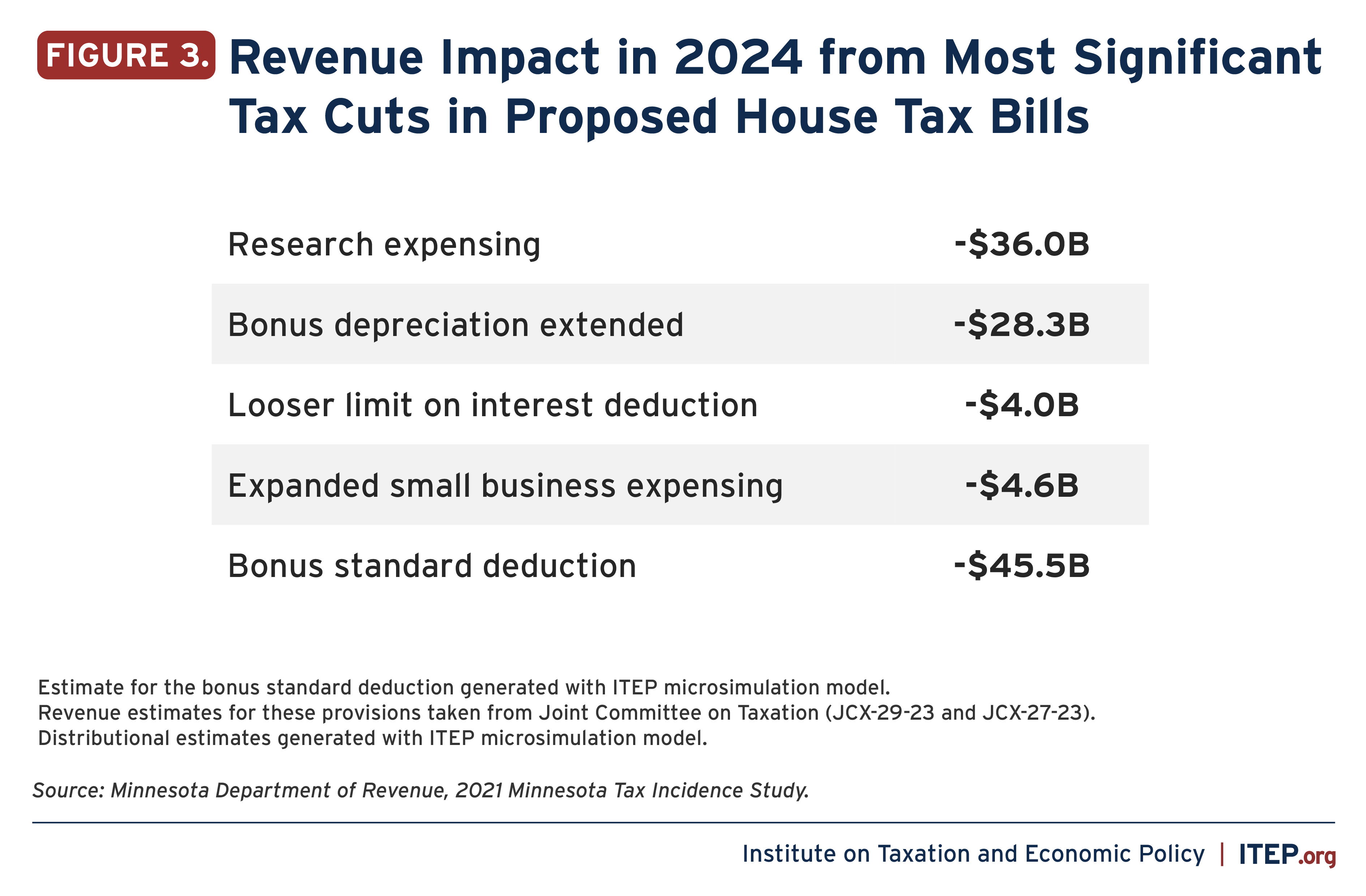

The analysis presented here examines the five most significant provisions that would cut taxes in the legislation, not the revenue-raising provisions that drafters of the bills present as offsetting the costs.

Four of these tax-cutting provisions would expand corporate and business tax breaks that were enacted in 2017 as part of the Trump tax law, the Tax Cuts and Jobs Act. The fifth provision is an increase in the standard deduction which would lower the tax liability for some middle-income people.

While the three bills include other business tax breaks not considered here, the four included in this analysis account for 95 percent of the cost of business tax breaks next year according to estimates from Congress’ official revenue-estimators at the Joint Committee on Taxation.[1]

The significant tax cuts are explained in more detail below.

Research expensing

2024 Revenue Impact: -$36.0B

This tax break is supposedly an incentive for corporations to conduct research that benefits society, but lawmakers have not asked what it has accomplished.

▪️ Some activities subsidized by this tax break do not meet any definition of “research” that most people would understand. Companies urging Congress to extend this tax break range from a brewery and a company that develops frozen and packaged foods to a sausage business and a company that develops electronic games for casinos. Lawmakers should ask what “research” this tax break supports before blindly extending it.

▪️ Many of the companies lobbying for this tax break have paid very little in taxes. Netflix, for example, has paid federal corporate income taxes equal to less than 1 percent of its reported profits over four years.

▪️ Read more about research expensing here.

Bonus depreciation

2024 Revenue Impact: -$28.3B

This tax break allows companies to deduct the cost of equipment the year they purchase it, rather than deducting the cost over several years until the equipment wears out. This extreme version of accelerated depreciation raises several problems.

▪️ Accelerated depreciation has let many large corporations (Verizon, Amazon, Walt Disney, Con Edison, General Motors, Dish Network, and others) largely avoid taxes, particularly during the last several years when this bonus depreciation provision has been in effect.

▪️ Bonus depreciation is supposed to encourage investment, but research shows that corporate leaders pay little attention to depreciation tax breaks when making investment decisions, even though their tax departments naturally exploit them to the greatest extent possible.

▪️ Read more about bonus depreciation here.

Looser limit on deductions for interest payments

2024 Revenue Impact: -$4.0B

This proposal would overturn a stricter limit on deductions that businesses take for interest payments they make on their debt and would extend the more lenient rule that was in effect until last year.

▪️ Without strict limits, the tax deduction for interest payments results in the tax code favoring corporations that borrow money over corporations that raise funds from investors by selling shares.

▪️ This provides an unwarranted subsidy to private equity firms that buy businesses and load them up with debt, which often results in the companies spiraling into bankruptcy.

▪️ In recent years this practice has led to the collapse of Toys “R” Us, Payless and other well-established companies.

▪️ Read more about the looser limit on interest deductions here.

Expanded Small Business Expensing

2024 Revenue Impact: -$4.6B

This provision, raising the limits on investment that can be deducted immediately under section 179 of the tax code, is more or less bonus depreciation but limited to relatively smaller companies.

▪️ The Tax Cuts and Jobs Act allowed full expensing of up to $1 million in investments in equipment (up from $500,000 previously) for companies that invest less than $2.5 million a year (up from $2 million previously).

▪️ These rules are already generous enough to benefit companies that most Americans think of as “small businesses.”

▪️ The legislation Republicans plan to consider would increase those limits further, so that up to $2.5 million could be invested by companies that invest up to $4 million in a single year.

Bonus Standard Deduction

2024 Revenue Impact: -$45.5B

The legislation would increase the standard deduction by $4,000 for married joint filers, $3,000 for heads of household, and $2,000 for other taxpayers.

▪️ The bonus standard deduction would be phased out for very high-income taxpayers, but the full benefit is available to married couples with incomes up to $400,000, heads of households with incomes up to $300,000, and other taxpayers with incomes up to $200,000.

▪️ This tax break does not help many low-income families who already have incomes less than the current standard deduction or who are eligible for tax credits targeting working families with very modest incomes.

▪️ As a result, the poorest fifth of Americans would receive just 2 percent of the benefits of this provision, and an average tax break of just $30 next year, as shown in the table in the appendix.

Appendix: More Details and Methods

The table below illustrates the distribution of the bonus standard deduction and the business tax cuts for Americans at different income levels and foreign investors, in 2024.

For this analysis, each of the business tax breaks is first broken into two components: first, the portion of the tax break that reduces corporate tax revenue, and second, the portion that reduces personal income taxes because it is claimed by owners of pass-through businesses (so called because the profits are passed through to the owners and reported on their personal income tax returns rather than subject to the corporate income tax).

For each provision, the split between the corporate portion and the pass-through portion is taken from the breakdown shown in the tax expenditure reports published periodically by the Joint Committee on Taxation.

For example, JCT shows that typically 95 percent of the benefits of research expensing flows to C corporations (corporations that pay the corporate income tax) while only 5 percent flows to pass-through businesses. For limits on interest deductions, 92 percent of the impact is on C corporations and the rest is on pass-through businesses. About three-fourths of the benefits of bonus depreciation flows to C corporations while a quarter flows to pass-through businesses.

Small business expensing (under section 179) is the exception in that most of the benefits, about 88 percent in most years, flow to pass-through businesses while the rest flow to C corporations.

The portion of the business tax cuts that reduce personal income taxes paid on pass-through business profits is distributed in a way that matches the distribution of income taxes paid on pass-through profits. This results in heavy concentration on the richest 1 percent, who own most businesses.

The second portion of the business tax breaks is the portion reducing corporate income taxes. Economists generally agree that the benefits of corporate tax cuts initially go to those who own stocks in American corporations.

Recent research has concluded that foreign investors own 40 percent of stocks in American corporations and would therefore receive a significant share of the benefits from corporate tax cuts.[2] This is why Appendix Table 1 shows $23.8 billion of corporate tax cuts flowing to foreign investors in 2024 alone.

In fact, the only group of Americans who receive a larger share of tax cuts are the richest 1 percent, who would receive $28.4 billion in 2024 alone.

Endnotes

[1] See Joint Committee on Taxation. JCX-25-23, https://www.jct.gov/publications/2023/jcx-25-23/; JCX-27-23, https://www.jct.gov/publications/2023/jcx-27-23/; JCX-29-23, https://www.jct.gov/publications/2023/jcx-29-23/.

[2] Steve Rosenthal and Theo Burke, “Who’s Left to Tax? US Taxation of Corporations and Their Shareholders,” Tax Policy Center, October 27, 2020. https://www.law.nyu.edu/sites/default/files/Who%E2%80%99s%20Left%20to%20Tax%3F%20US%20Taxation%20of%20Corporations%20and%20Their%20Shareholders-%20Rosenthal%20and%20Burke.pdf