Most states use the federal tax code as a starting point for their calculations of state personal income taxes, corporate income taxes, and estate taxes.

Changes to the federal code and federal tax administration have the potential to affect state tax systems enormously, but to some extent states can pick and choose which of those federal changes to accept.

Why Do States Conform to the Federal Tax Code

States conform to the federal tax code because doing so can make tax calculations both simpler and easier to enforce. For example, in the personal income tax, state taxpayers often start their calculations from federal adjusted gross income (AGI) rather than calculating income from scratch. In a few states, taxpayers start their calculations from federal taxable income. The remaining states have their own state-defined starting points, but they typically reference the federal code in various statutes and regulations.

What Are the Types of State Tax Conformity?

Some states use rolling conformity, in which they automatically adopt federal tax changes as they occur. This approach keeps state and federal tax treatments aligned but can create unpredictability in people’s taxes and state revenues when federal tax laws change.

Other states use fixed-date conformity, in which they conform to the federal tax code as of a specific date. When federal laws change, these states must actively decide whether to adopt the new provisions. If the federal changes are relatively minor and technical in nature, then updating the state tax code to conform to them may be perfunctory. But larger changes will merit more scrutiny.

Some states conform to the federal code on a provision-by-provision basis, an approach known as selective conformity.

What Is Decoupling from Federal Tax Law?

One result of conformity is that if the federal government chooses to exempt certain income from AGI, a state that conforms to the federal definition of AGI will lose revenue unless it decouples. Decoupling would mean requiring taxpayers to add back the exempt income for purposes of state tax calculations. Similarly, if a state couples to a federal provision that benefits a particular group of people – e.g. a credit for working-class families with children or special treatment for wealthy households with passive income – the effects on those people of any federal changes to those provisions can be amplified by state conformity.

Whether conformity is rolling or static, states can decide which federal provisions to adopt. Most follow federal definitions for some items while maintaining independent rules for others, and states vary as to which ones they conform to. Choosing to ignore a federal provision is known as “decoupling,” and it is particularly common when the federal government enacts a tax break that narrows the tax base and therefore would cost states revenue.

Do States and Their Residents Benefit from Tax Conformity?

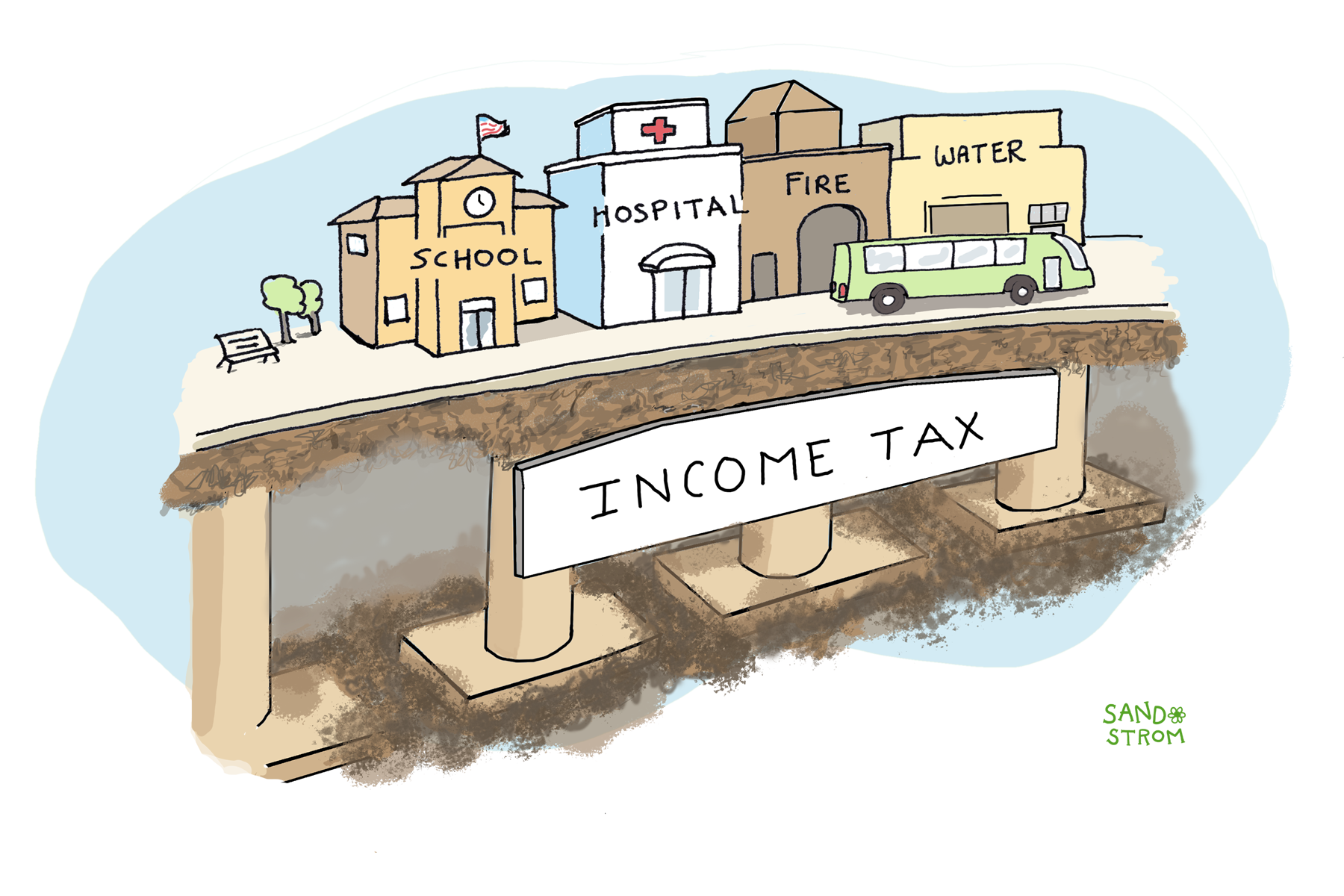

On core questions such as what is taxable income or how assets should be valued for the estate tax, there are practical reasons for conformity. If the rules are mostly the same, then taxpayers have fewer calculations to make. And if the federal Internal Revenue Service – which has greater enforcement resources than states – determines that a taxpayer (for example) has underreported their income to evade taxes, this information is automatically conveyed to the state tax authority, who can use that information to straightforwardly determine whether the taxpayer owes more state taxes as well.

The downside of conformity is that it sometimes forces a state into policy decisions it doesn’t agree with. That’s why, for example, states with estate taxes generally conform to federal rules on what’s included in an estate, but most have chosen not to go along with federal increases in exemption amounts. Decoupling has allowed states to avoid providing new, state-funded tax cuts for very wealthy estates even as the federal government has done so.

Rolling conformity can place state policymakers in a politically awkward position when the federal government cuts taxes in a way that reduces revenue: Either they accept the federal change and lose revenue automatically, or they decouple – creating the appearance that they are raising taxes even if the effect is simply to remain static.

One state, Maryland, has a unique solution to the threat of losing revenue due to federal action. Maryland automatically conforms to most federal changes if the revenue implications are minor but places a one-year hold on federal changes that would cost the state more than $5 million. This approach gives the legislature time to decide whether to conform.

How Does Your State Conform to the Federal Tax Code?

| State | How Does the State Conform to the Federal Code? | Starting Point for Calculating Personal Income Tax |

|---|---|---|

| Alabama | Rolling | State Definition |

| Arizona | Fixed | Federal Adjusted Gross Income |

| Arkansas | Selective | State Definition |

| California | Fixed | Federal Adjusted Gross Income |

| Colorado | Rolling | Federal Taxable Income |

| Connecticut | Rolling | Federal Adjusted Gross Income |

| District of Columbia | Rolling | Federal Adjusted Gross Income |

| Delaware | Rolling | Federal Adjusted Gross Income |

| Georgia | Fixed | Federal Adjusted Gross Income |

| Hawaii | Fixed | Federal Adjusted Gross Income |

| Idaho | Fixed | Federal Taxable Income |

| Illinois | Rolling | Federal Adjusted Gross Income |

| Indiana | Fixed | Federal Adjusted Gross Income |

| Iowa | Rolling | Federal Taxable Income |

| Kansas | Rolling | Federal Adjusted Gross Income |

| Kentucky | Fixed | Federal Adjusted Gross Income |

| Louisiana | Rolling | Federal Adjusted Gross Income |

| Maine | Fixed | Federal Adjusted Gross Income |

| Maryland | Rolling | Federal Adjusted Gross Income |

| Massachusetts | Fixed | Federal Adjusted Gross Income |

| Michigan | Rolling | Federal Adjusted Gross Income |

| Minnesota | Fixed | Federal Adjusted Gross Income |

| Mississippi | Selective | State Definition |

| Missouri | Rolling | Federal Adjusted Gross Income |

| Montana | Rolling | Federal Taxable Income |

| Nebraska | Rolling | Federal Adjusted Gross Income |

| New Jersey | Selective | State Definition |

| New Mexico | Rolling | Federal Adjusted Gross Income |

| New York | Rolling | Federal Adjusted Gross Income |

| North Carolina | Fixed | Federal Adjusted Gross Income |

| North Dakota | Rolling | Federal Taxable Income |

| Ohio | Fixed | Federal Adjusted Gross Income |

| Oklahoma | Rolling | Federal Adjusted Gross Income |

| Oregon | Rolling | Federal Taxable Income |

| Pennsylvania | Selective | State Definition |

| Rhode Island | Rolling | Federal Adjusted Gross Income |

| South Carolina | Fixed | Federal Taxable Income |

| Utah | Rolling | Federal Adjusted Gross Income |

| Vermont | Fixed | Federal Adjusted Gross Income |

| Virginia | Fixed | Federal Adjusted Gross Income |

| West Virginia | Fixed | Federal Adjusted Gross Income |

| Wisconsin | Fixed | Federal Adjusted Gross Income |

|

ITEP.org

| ||

Notes: “Rolling” conformity means that a state automatically adopts federal tax changes as they occur. “Fixed” (or static) conformity means that a state’s tax code is linked to the federal tax code as it existed on a specific date. “Selective” conformity means that there is no overall conformity but individual provisions of the state tax code refer to specific sections of federal code. Alabama uses its own definition of income as a starting point but references the federal code on a rolling basis. Iowa and Montana changed their codes’ references to the federal code in the last several years. Oregon has rolling conformity for purposes of the definition of taxable income.

Sources: Federation of Tax Administrators, “State Personal Income Taxes: Federal Starting Points,” 2023; ITEP analysis of state tax codes, March 2026.

Related Entries

How Do State and Local Personal Income Taxes Work?

The personal income tax funds public education, health care, public safety, and other public services provided by state and local governments. If well-designed, it is the fairest major revenue source available to states.

How Do State Corporate Income Taxes Work?

A robust corporate income tax ensures that profitable corporations help fund the public services they benefit from, just as working people do. It’s one of the few progressive taxes available to state policymakers.

How Do State Estate and Inheritance Taxes Work?

Estate and inheritance taxes are taxes on wealth passed on after someone’s death. They are a common way for states to tax the inheritances of wealthy individuals. These taxes ensure that those very large estates help pay for public services like schools, hospitals, and parks.

Learn More

- Comptroller of Maryland. “Maryland Tax Alert 07-24.” July 2020.