Flat or graduated personal income taxes have varying effects on the annual individual tax liabilities of taxpayers at different income levels. Less examined is how tax structures affect income inequality and racial wealth gaps. This brief illustrates how Illinois’s historic flat income tax structure compares to the proposed Fair Tax through a multi-year retrospective analysis. It shows that Illinois’s flat income tax in lieu of a graduated rate tax used by most states amounts to a tax subsidy for the wealthiest Illinoisans that compounds income inequality and racial wealth gaps.

Fair vs. Flat: Choice Between Income Tax Structure Implicates More than Individual Tax Liability, Affects Income Inequality, Racial Wealth Gaps

This November, Illinoisans will decide whether to amend the state constitution to allow a graduated income tax. A “yes” vote on the Illinois Fair Tax constitutional amendment will make effective legislation that will replace the current flat tax rate of 4.95 percent with graduated rates that cut taxes for those with taxable income less than $250,000 and institute higher marginal rates on taxable incomes greater than $250,000 (Figure 1).

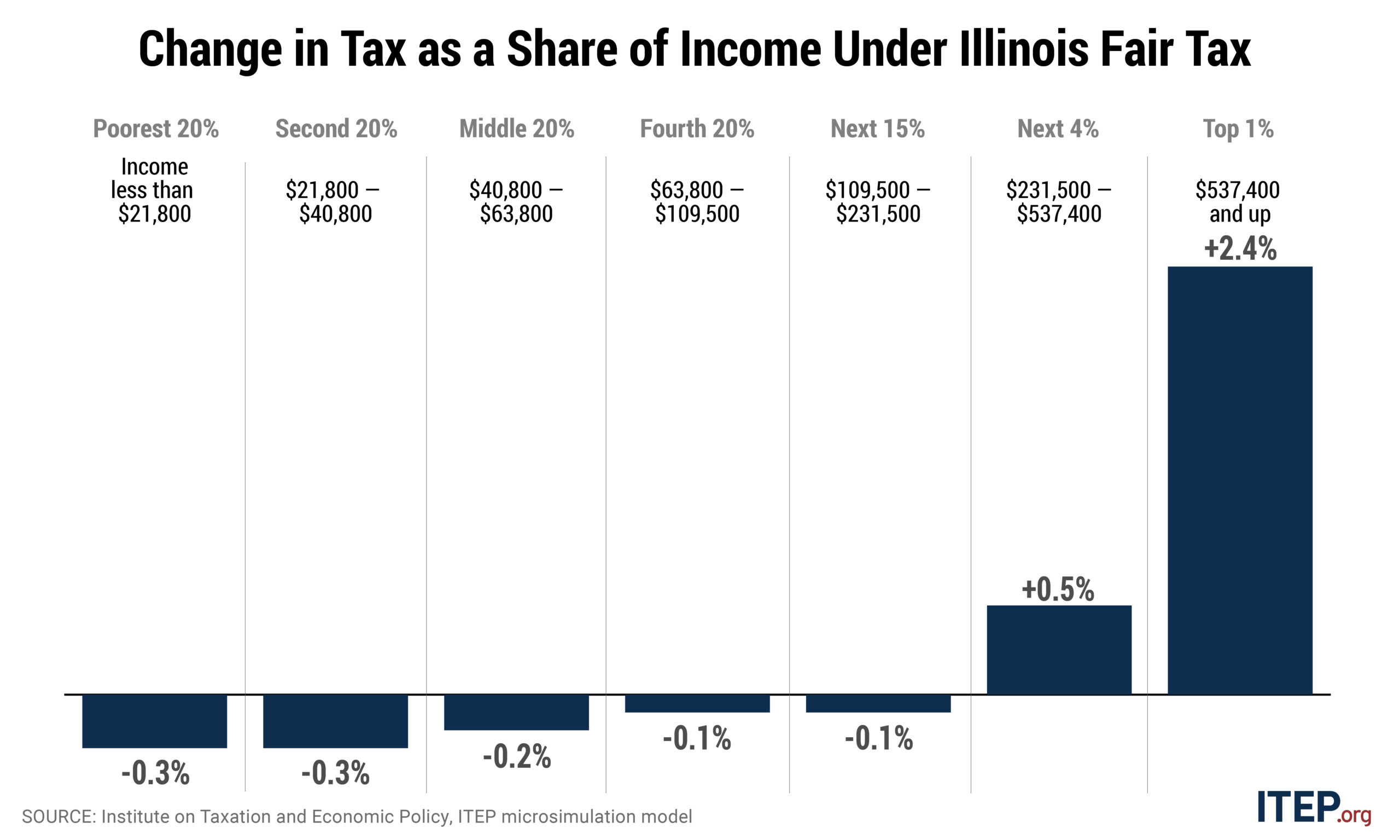

Under the Fair Tax, 97 percent of taxpayers with income tax liability would receive a tax cut and only the wealthiest 3 percent would pay more. The Fair Tax would improve the fairness of Illinois’s combined state and local taxes. Currently Illinoisans in the bottom 20 percent of income—less than $21,800 in income—pay 14.4 percent of their incomes in combined state and local taxes, while the top 1 percent—$537,400 and higher in income—pay only 7.4 percent (Figure 2).[1] In contrast, the Fair Tax would increase effective tax rates by 2.4 percent for the top 1 percent while cutting taxes for taxpayers whose incomes fall in the bottom 95 percent (Figure 3), improving Illinois’s tax system from the 8th most regressive in the nation to the 20th.

The choice between maintaining the flat tax status quo or adopting the Fair Tax extends beyond questions of individual income tax liability and improved tax equity. It also affects income inequality and racial wealth gaps.

Tax laws that collect higher shares of taxpayer income from those with lower incomes exacerbate income inequality. In Illinois today, after state and local taxes, a family making less than $21,800 has 85.3 percent of their income remaining post-taxes while a family with more than $537,400 has 92.6 percent of theirs. Tax laws that perpetuate these inequities year after year make it even harder for families already struggling to get by with low, stagnating wages.

Another consequence of Illinois’s flat income tax is that the wealthiest don’t contribute as much as they would under a graduated income tax like the Fair Tax—both in terms of absolute tax dollars paid and the share of total taxes paid. In 2019, Illinoisans with more than $250,000 in taxable income paid 38 percent of all personal income taxes under the flat 4.95 percent rate, but under the Fair Tax they would pay 47 percent of total income taxes—an increase of 9 percentage points. In contrast, those with less than $250,000 in taxable income currently pay 62 percent of all personal income taxes but would pay 53 percent under the Fair Tax—a decrease of 9 percentage points. By taxing higher incomes at higher rates and lower incomes at lower rates, more total tax dollars are paid by those with greater ability to pay, shifting more of the responsibility for the tax from those with low- and moderate-wages to the wealthiest.

What do wealth and wealth gaps have to do with it? Because the wealthiest Illinoisans have lower tax responsibilities under the current flat tax than they would if Illinois joined most other states in levying a graduated rate tax, the wealthy can invest these “saved” tax dollars to build even more wealth. Meanwhile, the same laws make it harder for low- and moderate-income families to get by. The result is widening wealth gaps that compound over time and are starkest along racial and ethnic lines.

To illustrate these collective and compounding effects on income inequality and wealth, ITEP conducted a multi-year analysis comparing tax liabilities under Illinois’ flat tax compared to the Fair Tax for taxpayers with less than and greater than $250,000 in taxable income. Due to difficulties forecasting income and economic conditions 20 years in the future, this is a retrospective analysis, using data on historic flat tax rates and actual personal income tax collections from 1999-2019. For each year, ITEP determined tax liabilities for taxpayers under the actual flat tax in effect that year compared to what tax liabilities would have been had each group paid the same share of taxes as they would under the Fair Tax (tax collections held constant). As a scenario analysis contextualized in the past, our intention is to illustrate the long-term consequences of the choice on income inequality and wealth gaps and should not be confused as an exercise in “predicting the past.”[2]

Our key findings follow.

Key Findings

- Compared to the Fair Tax, Illinois’s flat tax structure shifts responsibility for paying $27 billion more in personal income taxes from the top 3 percent of earners to families with less than $250,000 of taxable income over the 20-year period studied, lowering these families’ standard of living while enabling the wealthiest Illinoisans to build an additional $50.2 billion in wealth. (See Table 1)

-

- Under the same distribution of the Fair Tax, the wealthiest 3 percent of Illinoisans would have paid on average an additional 8 percent of total income taxes or $27 billion from 1999-2019.

- Owing $27 billion less in taxes under the flat tax structure is equivalent to a wealth gain of almost $50.2 billion for the richest Illinoisans over this 20-year period, assuming the money was invested in the stock market.[3]

- Illinois has had a flat income tax since its adoption in 1969, so cumulative tax subsidies to and resulting wealth accumulation of the highest-income Illinoisans compared to the Fair Tax are far greater over the entire duration of the tax’s history.

- Black and Hispanic Illinois taxpayers with taxable incomes less than $250,000 pay $4 billion more in taxes over the 20-year period studied under a flat tax than they would under the Fair Tax. These tax differences reduced the standard of living for these families and exacerbated income and wealth gaps while enabling the wealthiest Illinoisans to accumulate an additional $7.5 billion in wealth due to these tax subsidies. (See Table 2)

-

- Income disparities by race and ethnicity in the United States are striking and pervasive—as old as the history of our country founded with an economic system dependent on enslavement and the subsequent years of inequality, discrimination, and differential access to power and opportunity. In 2016, median household incomes for Black and Hispanic households were, respectively, 42 and 37 percent lower than white non-Hispanic households. The wealth divides are even starker, with median household wealth for Black and Hispanic households equaling $17,000 and $21,000 respectively compared to $171,000 for white non-Hispanic households.[4]

- Over the 20-year period studied, Illinois’s unusual choice to levy a flat income tax system exacerbated racial and ethnic income gaps by requiring Black and Hispanic taxpayers with taxable income less than $250,000 to pay $4 billion more in personal income taxes than they would have under the Fair Tax.

- The $4 billion in additional taxes that Black and Hispanic taxpayers with income less than $250,000 effectively paid under the state’s flat tax would otherwise have been paid by the wealthiest Illinoisans, 84 percent of whom are white, non-Hispanic. Assuming an ordinary rate of return, that $4 billion transfer from the state’s Black and Hispanic taxpayers with low and moderate incomes to its top 3 percent of earners allowed the state’s most affluent residents to build their wealth by as much as an additional $7.5 billion.

Methodological Notes

Retrospective and Hypothetical Analysis

This analysis compares actual personal income tax collections under historic Illinois flat tax rates from 1999-2019 to what they would have been under the same distributional divisions of tax liability under the Fair Tax. It is a retrospective (rather than prospective) analysis given the inherent difficulties in credibly forecasting economic conditions and incomes 20 years in the future. This choice in data set should not be confused with an attempt to “predict the past,” i.e., we do not seek to answer or imply answers to questions like, “Would lawmakers have adopted a graduated rate structure in the late 1990s?”, “What thresholds and rates would have been required to yield the same amount of revenue the flat tax in a specific year generated?”, etc.

This analysis is hypothetical in the sense that it seeks to answer questions about the cumulative and comparative effects of the flat v. Fair Tax projected backward onto a time frame when the Fair Tax was not a constitutional amendment or contingent legislation. We considered two approaches for normalizing the calculations across income tax systems:

- Assume the same level of historical tax collections but impose a division of tax liability that mirrors the share of tax paid under the Fair Tax compared to the share of taxes paid under the flat tax in effect in each of the years 1999-2019. This approach requires flexibility to the exact rates and brackets that would have been in place to achieve the same level of tax collections from year to year.

- Hold the Fair Tax rate structure constant (see Figure 1) for each of the years from 1999-2019 and compare relative tax liabilities to an imputed flat tax rate that would have brought in the same amount of tax collections.

The comparative distributional point this analysis aims to illustrate is more clearly seen in holding tax collections to actuals, so we rely on the first approach in this analysis.

Static v. Dynamic Modeling

ITEP’s modeling of the Fair Tax proposal follows a “static” approach: it estimates revenues for the proposal under the assumption that the economic behavior of households and businesses are not affected by the tax. This static approach to modeling the revenue effects of changes in tax policy contrasts with “dynamic” approaches which, in addition to the more immediate static impacts, include subsequent effects of behavioral changes among households and businesses responding to the change in tax policy.

Although, in principle, dynamic approaches could be more realistic, in practice, they are significantly limited, particularly for purposes of modeling state tax policy changes. Those limitations include the following:

- Dynamic modeling necessarily relies on particular assumptions about the economy that, at best, reflect only particular aspects of real economic behavior. For example, widely used macroeconomic growth models and carefully calibrated computable general equilibrium (CGE) models might be informative as to the variety of final equilibrium outcomes for the economy as a result of tax changes, but they are generally mute on the precise path the economy follows in adjusting from pre-policy to post-policy equilibrium, and, importantly, how long the adjustment period would last (often it is decades). At worst, simplistic models that are little more than rules of thumb give the appearance of “modeling” but, in fact, they decisively bias the revenue estimates to conform with the prior beliefs and intentions of the analyst, not the myriad complexities of economic reality.

- Dynamic models are not designed to simulate the effects of changes in tax policy on the distribution of incomes among the households and businesses that are directly affected by the policy. The dynamic models used to adjust static revenue impacts for behavioral feedback are macroeconomic in nature, whether they have a national or regional focus. That is, they are designed to predict changes in aggregate economic indicators (e.g., output, employment, total revenue) and are silent on how, for example, a particular tax change might affect lower-income households differently from more affluent households.

- Dynamic models necessarily rely on incomplete data, especially models for states and localities. Dynamic models must quantify linkages between dozens of economic sectors. Even at the national level, these linkages are often opaque and require arbitrary approximations. Data on these linkages are often nonexistent at the state level.

- Estimates of the macroeconomic effects of policy changes are highly uncertain. Economists differ substantially on the size of macroeconomic feedbacks from reducing marginal income tax rates or other changes in taxes or spending. There is no consensus on the impact of tax changes on labor supply, savings, investment, or consumption.[5]

These are among the reasons that ITEP believes that the static revenue estimates are more informative to policymakers than conventional dynamic estimates, certainly as a first approximation.

Nominal v. Real Dollars

All tax and wealth dollar figures throughout this brief and in the tables are in 2020 dollars. Actual tax collections under the state’s flat personal income taxes reported and estimated revenues under the Fair Tax in current dollars were converted to real dollars using a Personal Consumption Expenditures (PCE) deflator.

Revenue Collections Data

“Personal Income Tax Receipts Under Historic Flat Tax Rates” are sourced from the State of Illinois Department of Revenue Tax Stats. This analysis excludes receipts from non-residents.

Calculation of Share of Taxes Paid by Taxable Income Less/Greater Than $250,000

ITEP relied on its Microsimulation Tax Model to calculate the share of taxes paid by Illinois taxpayers by fixed income brackets of less than and greater than $250,000 in taxable income for each year of the historic flat tax (e.g., 3 percent from 1999-2010, 5 percent 2011-2014, 3.75 percent 2015-2017, and 4.95 percent 2018-2019) and in contrast what it would have been under the Fair Tax. Taxpayers who fall into these respective income categories are not constant from year to year.

Calculation of Share of Taxes Paid by Black and Hispanic Taxpayers with Taxable Income Less Than $250,000

ITEP calculated the share of taxes paid by race and ethnicity for taxpayers with taxable income less than and greater than $250,000 for both the Fair Tax and flat tax in tax year 2019 using its Microsimulation Tax Model and ACS 2013-2017 data.

Race outcomes were produced by matching ACS individual and household data, followed by producing frequencies of demographic sub-tax units within all tax units. We use a method developed by the Tax Policy Center to crosswalk between ACS individual and household data and tax data. Under this methodology, where relevant, we link individual spousal records and assign dependents to adults based on several criteria related to age, income, and education status. ITEP’s resulting estimates of tax units’ racial and ethnic composition are validated by checking against published Census data on households and persons, as well as demographic data published by states.

The analysis imputes the shares of taxes paid by each race and ethnicity group from 1999-2018 by adjusting the 2019 shares of tax paid by changes in the share of aggregate income help by each race and ethnic group over the same period using Census Table H-2. Share of Aggregate Income Received by Each Fifth and Top 5 Percent from 1967 to 2018. Note that growth in the share of taxes paid by Black and Hispanic taxpayers with less than $250,000 in taxable income while the share of taxes paid by all taxpayers with less than $250,000 decreased from 2012-2018 is primarily driven by increases in the Hispanic population and share of aggregate income held by these households during that time.

Calculation of the Wealth Equivalent

This section of the analysis assesses the value of the higher tax payments made by families with less than $250,000 in annual taxable income under the flat tax compared to the Fair Tax and what the value of that money was if invested in the stock market (S&P 500 Index) and allowed to accrue in value. For each year, this gives us the total wealth (in 2020 dollars) that wealthier households in effect accrued as a result of the higher taxes taxpayers with less than $250,000 in taxable income paid under the flat tax compared to the Fair Tax.

Market return data was developed leveraging data from Aswath Damodaran at the NYU Stern School of Business, “Historical Returns on Stocks, Bonds and Bills – United States,” available online.

About the ITEP Tax Model

The ITEP Microsimulation Tax Model is a tool for calculating revenue yield and incidence, by income group, of federal, state and local taxes. The ITEP model is capable of calculating the impact of current tax law and tax change proposals on taxpayers and can also project potential revenue yields of tax law changes. The model is unique in its ability to produce analysis at the federal and state levels and to analyze income, consumption and property-based taxes.

In computing its estimates, the ITEP model relies on one of the largest databases of tax returns and supplementary data in existence, encompassing close to three-quarters of a million records. To forecast revenues and incidence, the model relies on government or other widely respected economic projections.

The ITEP model’s federal tax calculations are very similar to those produced by the congressional Joint Committee on Taxation, the U.S. Treasury Department and the Congressional Budget Office (although each of these four models differs in varying degrees as to how the results are presented). The ITEP model, however, adds state-by-state estimating capabilities not found in those government models.

Data Sources

A “microsimulation model,” the ITEP model works on a very large stratified sample of tax returns and other data, aged to the year being analyzed. The ITEP model uses the following micro-data sets and aggregate data:

Micro-Data Sets

IRS 1988 Individual Public Use Tax File, Level III Sample; IRS Individual Public Use Tax Files; Current Population Survey; Consumer Expenditure Survey; U.S. Census; American Community Survey.

Partial List of Aggregated Data Sources

Miscellaneous IRS data; Congressional Budget Office and Joint Committee on Taxation forecasts; other economic data (Commerce Department, WEFA, etc.); state tax department data; data on overall levels of consumption for specific goods (Commerce Department, Census of Services, etc.); state-specific consumption and consumption tax data (Census data, Government Finances, etc.); state-specific property tax data (Govt. Finances, etc.); American Housing Survey; Census of Population Housing; Energy Information Administration; Federal Highway Administration; BDS Analytics.

Acknowledgments

Thanks to data collaborator Ken Gaebler for the inspiration for this research project, collecting the IL Department of Revenue tax receipts data, and wealth computations; Jessica Schieder and Lorena Roque for the race/ethnicity analysis; Meg Wiehe, Carl Davis, and Matthew Gee for methodological review; and Erika Frankel, Matthew Gardner, and Matthew Salomon for modeling support.

Endnotes

[1] Meg Wiehe, Aidan Davis, Carl Davis, Matt Gardner, Lisa Christensen Gee and Dylan Grundman. “Who Pays? A Distributional Analysis of the Tax System in all 50 States (Sixth ed.),” Institute on Taxation and Economic Policy, October 2018. Online at https://itep.org/whopays/.

[2] As a hypothetical retrospective analysis, we have no interest in speculating whether a Fair Tax would have been enacted at the turn of the century, what combination of rates and brackets would be required to yield historic tax collections, whether there would have been changes to the tax system over time, etc.

[3] See Methodological Note on Calculation of Wealth Equivalent Analysis

[4] Nieves, Emanuel. “Infographic: The Racial Wealth Gap,” Prosperity Now, June 2019. Based on Board of Governors of the Federal Reserve System, 2016 Survey of Consumer Finances (SCF) (Washington, DC: Federal Reserve Board, 2017), see “Excel Based on Public Data,” “Estimates inflation-adjusted to 2016 dollars.” Online at https://prosperitynow.org/blog/infographic-racial-wealth-gap.

[5] Mazerov, Michael. “Academic Research Lacks Consensus on the Impact of State Tax Cuts on Economic Growth,” Center on Budget and Policy Priorities, June 2013. Online at http://www.cbpp.org/research/academic-research-lacks-consensus-on-the-impact-of-state-tax-cuts-on-economic-growth.

{kind=link}

{kind=link}