On November 20, the House Judiciary Committee approved a bill that would legalize cannabis at the federal level and allow states to decide whether they will permit legal sales within their borders. From a tax perspective, the most attention-grabbing provision in the Marijuana Opportunity Reinvestment and Expungement (MORE) Act is a new 5 percent federal tax on sales of the drug. But this may not actually be the most consequential tax policy change in the bill.

A new ITEP report explains that an income tax cut for cannabis businesses embedded in the MORE Act is probably larger than the new 5 percent sales tax. This means that the average cannabis retailer—and its customers—could expect to pay LESS tax if the MORE Act is signed into law. Congress might have good reasons for structuring legalization this way, but it is an underappreciated aspect of the bill that should be made clearer as this debate progresses.

The MORE Act would reduce income taxes for cannabis sellers by allowing them to claim the same types of routine business expense deductions that other industries have long taken for granted, such as write-offs for rent, utilities, wages, and employee benefits paid at retail storefronts as well as marketing, legal, and accounting expenses. Currently, only the cost of goods sold is federally tax deductible by the cannabis industry.

If the federal government decides to legalize cannabis, then it is only fair that the cannabis industry should be allowed to write off most of the same types of expenses as other industries (though the report mentions advertising and marketing as possible exceptions). Frankly, an income tax cut along these lines is almost an inevitable part of legalization.

But Congress also has the power to levy a new sales or excise tax on cannabis that would offset some or all of that tax cut. Alcohol and tobacco are already subject to federal excise taxes and consistency would seem to require that cannabis be taxed as well.

Our report works through some arithmetic suggesting that the break-even federal sales tax rate, under which the average retailer would pay no more or less federal tax than it does today, is likely above 6 percent. If that math is correct, then the MORE Act and its 5 percent tax represent a net tax cut.

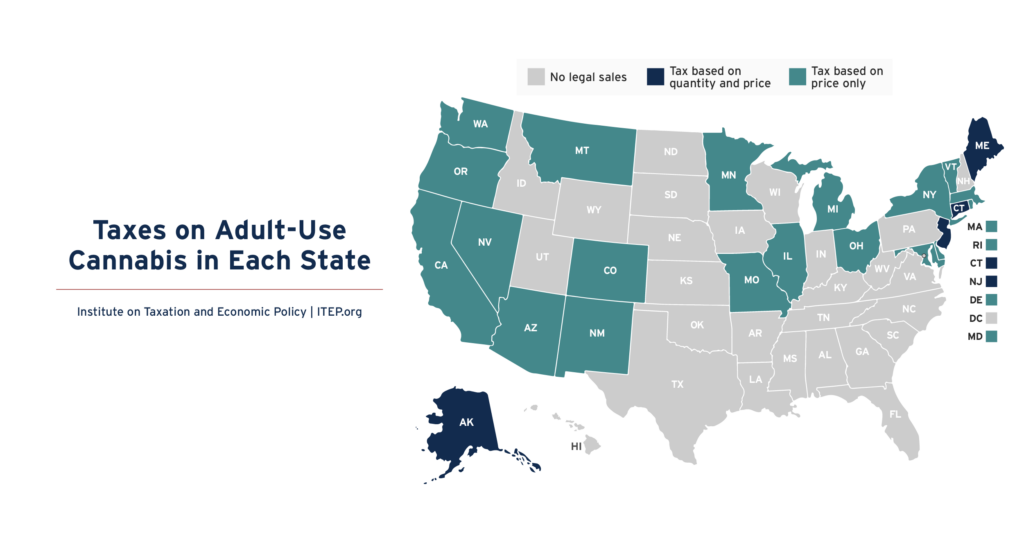

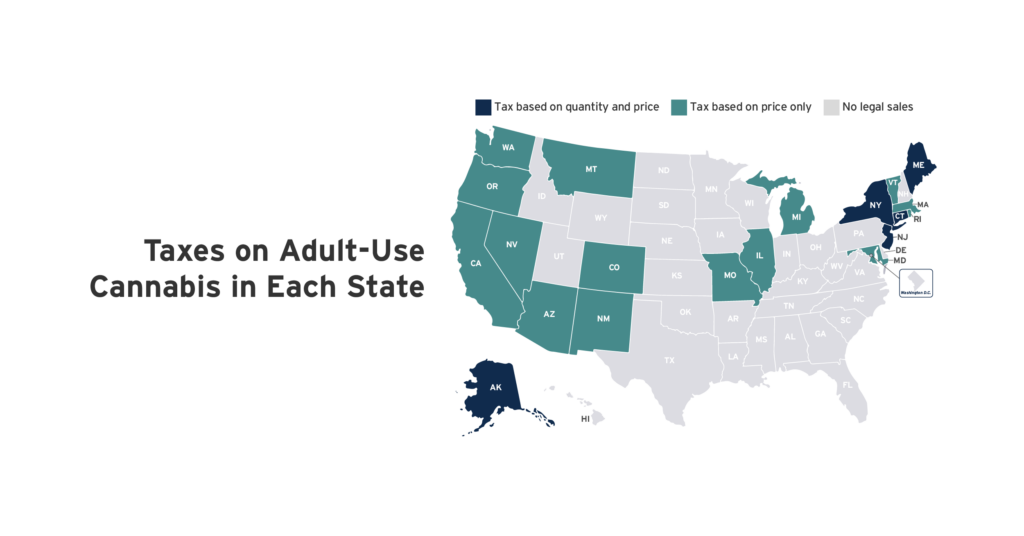

The sales tax contained in the MORE Act falls in the middle of the pack when compared to other prominent cannabis legalization bills pending in Congress. Under the Marijuana Revenue and Regulation Act (MRRA) the federal sales tax would start at 10 percent and ramp up to 25 percent by the fifth year. The Strengthening the Tenth Amendment Through Entrusting States (STATES) Act, by contrast, does not levy a federal sales tax on cannabis at all.

Congress will need to take several factors into consideration when selecting a tax rate to be applied to cannabis. Among those factors are promoting public health, raising revenue, achieving parity with other “sin taxes,” and hastening the decline of the illicit market.

But when weighing these various objectives, it will also be helpful to keep in mind what legalization will mean for the overall tax bills of the industry and its consumers, compared to the status quo. Through that lens, both the MORE Act and the STATES Act aren’t just legalization bills. They’re also cannabis industry tax cuts.