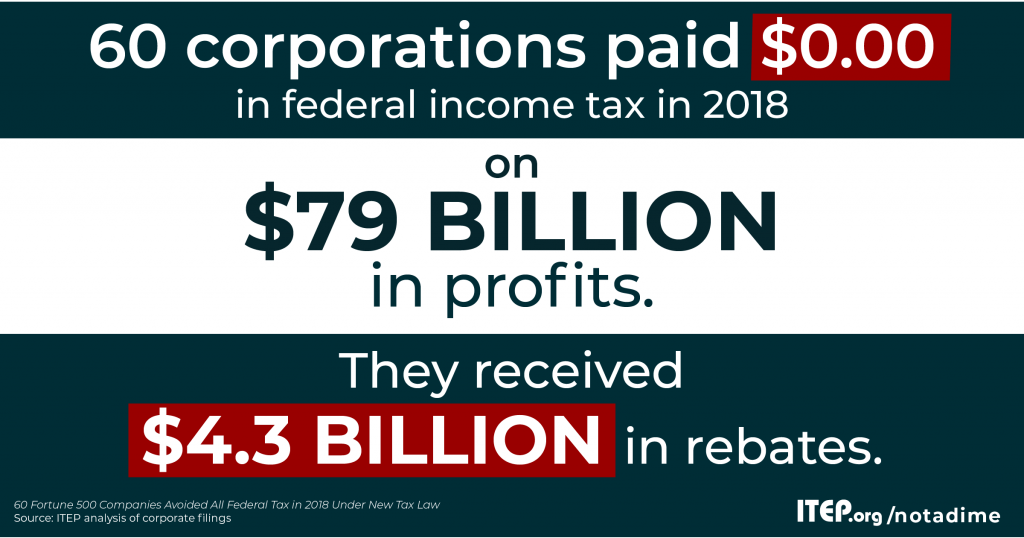

Earlier this year, Amazon and Netflix made headlines when ITEP reported findings that these and at least 58 other companies paid no federal income taxes in 2018. One of the tax breaks they use to manage this feat is related to stock options, the subject of a new ITEP report. As illustrated in the table to the right, some companies saved hundreds of millions, and in some cases more than a billion dollars, in taxes in 2018 alone with this break. It’s time for Congress to eliminate the stock options tax dodge.

Earlier this year, Amazon and Netflix made headlines when ITEP reported findings that these and at least 58 other companies paid no federal income taxes in 2018. One of the tax breaks they use to manage this feat is related to stock options, the subject of a new ITEP report. As illustrated in the table to the right, some companies saved hundreds of millions, and in some cases more than a billion dollars, in taxes in 2018 alone with this break. It’s time for Congress to eliminate the stock options tax dodge.

The rules governing stock options are a dream come true for corporations trying to attract investors while minimizing their tax liability. When companies pay employees with stock options, they can record a small expense on their books and in their public filings while reporting a much larger expense to the IRS. This means they report larger profits to the public to attract investors but report smaller profits to the IRS and thus pay less in corporate income taxes.

A recent change in the law may mitigate this to a degree, but as the ITEP report explains, lawmakers still have work to do to shut down this tax dodge.

How Stock Options Work

Many corporations compensate their top employees and executives with stock options, which are contracts allowing the purchase of the company stock at a set price (called a strike price) at some point during a specific time period, often 10 years.

Employees with stock options hope and wait for the market price of the stock to rise far above the strike price. When that happens, they can buy stock at the lower strike price and then sell it at the higher (sometimes far higher) market price.

Like other types of compensation and other types of business expenses, stock options are deducted from a company’s income for tax purposes. The problem is that the current rules used to calculate those tax deductions allow companies to claim expenses that are larger than what they actually incurred and what they reported to investors.

Companies Tell One Story to Investors, Another to the IRS

The value of the stock options is the difference between their strike price and the market value of the stock. Imagine you receive options to buy one million shares of stock at $1 per share, and somehow you know that the market price will rise to $3 per share. That means you can spend $1 million buying stock that will sell on the market for $3 million. The value of those options is, therefore, $2 million.

Of course, at the time a company grants options to an employee, there is no way to really know for sure how much the market price will rise over time, and therefore no way to be certain about the value of the stock options. Under the accounting rules that determine how the expense is recorded on the company’s books and how it is reported to investors, companies are required to estimate the value of options based on the potential future value of the stock, taking into account several different factors.

But the rules determining how the expense is calculated for tax purposes are totally different and often allow companies to deduct a far higher amount. For tax purposes, companies wait until the option is exercised and calculate the value of the options as the difference between the strike price and the market price when exercised. In many cases, the stock price has risen dramatically more than the company claimed it would at the time the options were granted. That often means that the value of the options for tax purposes is enormous, and far greater than the company recorded on its books and reported to investors previously.

For any other form of compensation, companies must tell the IRS and investors the same thing. Stock options are an anomaly. The rules encourage companies to low-ball the estimated cost of options at the time they are granted, enabling them to report higher profits to investors, while reporting a much larger expense for tax purposes, enabling them to report lower profits and thus pay less taxes.

One of the bizarre results for companies that grant stock options is that the more profitable they are over time, the less corporate taxes they pay. As the ITEP report explains, this is just one of the problems Congress can solve by eliminating this tax break.