Key Findings

- South Carolina lawmakers passed legislation, now signed by the governor, that would eliminate the state’s individual income tax over time.

- This would reduce revenue in South Carolina by $309 million this year, with full income tax elimination costing over $6.6 billion a year – nearly 45 percent of the current state general fund.

- This short-sighted move will jeopardize the many public services that South Carolinians rely on, and it comes as many states are doing the opposite and seeking to preserve revenue as they feel and continue to brace for the impact of recent federal tax and spending changes under the so-called “One Big Beautiful Bill Act” (OBBBA).

- The legislation would also disproportionately benefit the wealthiest South Carolinians, who just received a windfall from the federal tax cuts (to the tune of over $68,000 a year, on average, for the wealthiest 1 percent).

Bill Summary

H 4216 would make the following changes to South Carolina’s tax system (all changes are retroactive to 2026, except the triggers, which begin in 2027):

- Collapses the state’s three-bracket individual income tax structure into two brackets with rates of 1.99 percent on the first $30,000 of income and 5.2 percent on income over $30,000.

- Implements rate reduction triggers1 starting in 2027. If reached, the second bracket of 5.2 percent will be reduced until it collapses into the 1.99 percent bracket. At that point, the 1.99 percent flat rate will trigger down until it hits zero.

- Requires that filers add back their federal standard or itemized deductions to their Federal Taxable Income (FTI). South Carolina is one of seven states that start their state income tax calculations using FTI instead of Federal Adjusted Gross Income (FAGI).

- Creates the South Carolina Income-Adjusted Deduction (SCIAD) to replace federal standard and itemized deductions. This allows single filers to deduct $15,000, phasing out between $40,000 and $95,000 of income; Head of Household filers to deduct $22,500, phasing out between $60,000 and $142,500 of income; and joint filers to deduct $30,000, phasing out between $80,000 and $190,000 of income.

- Caps South Carolina’s already meager nonrefundable Earned Income Tax Credit at $200, therefore raising taxes on low- and middle-income South Carolinians and cutting the amount the state spends on their EITC in half.2

Bill Analysis

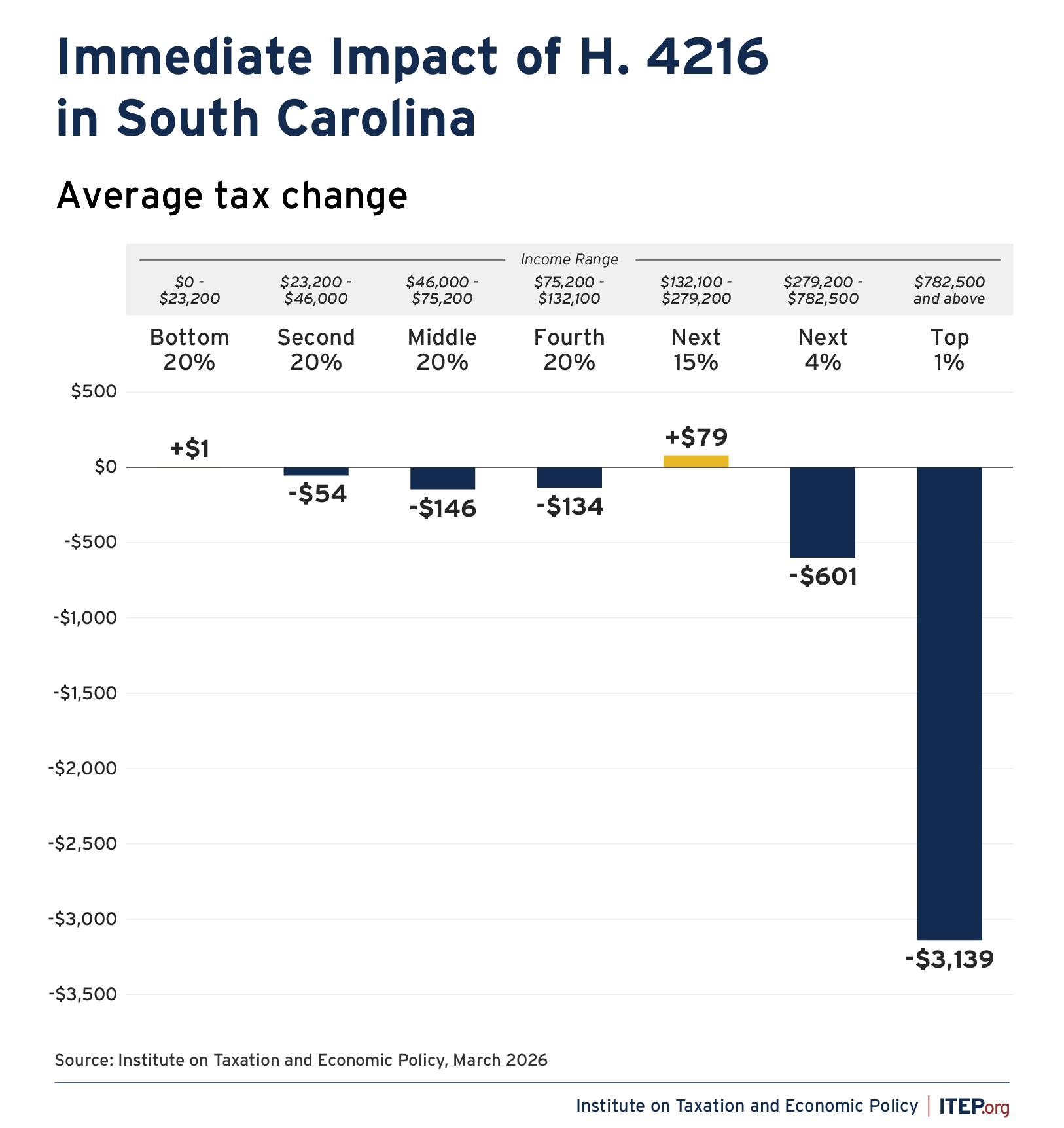

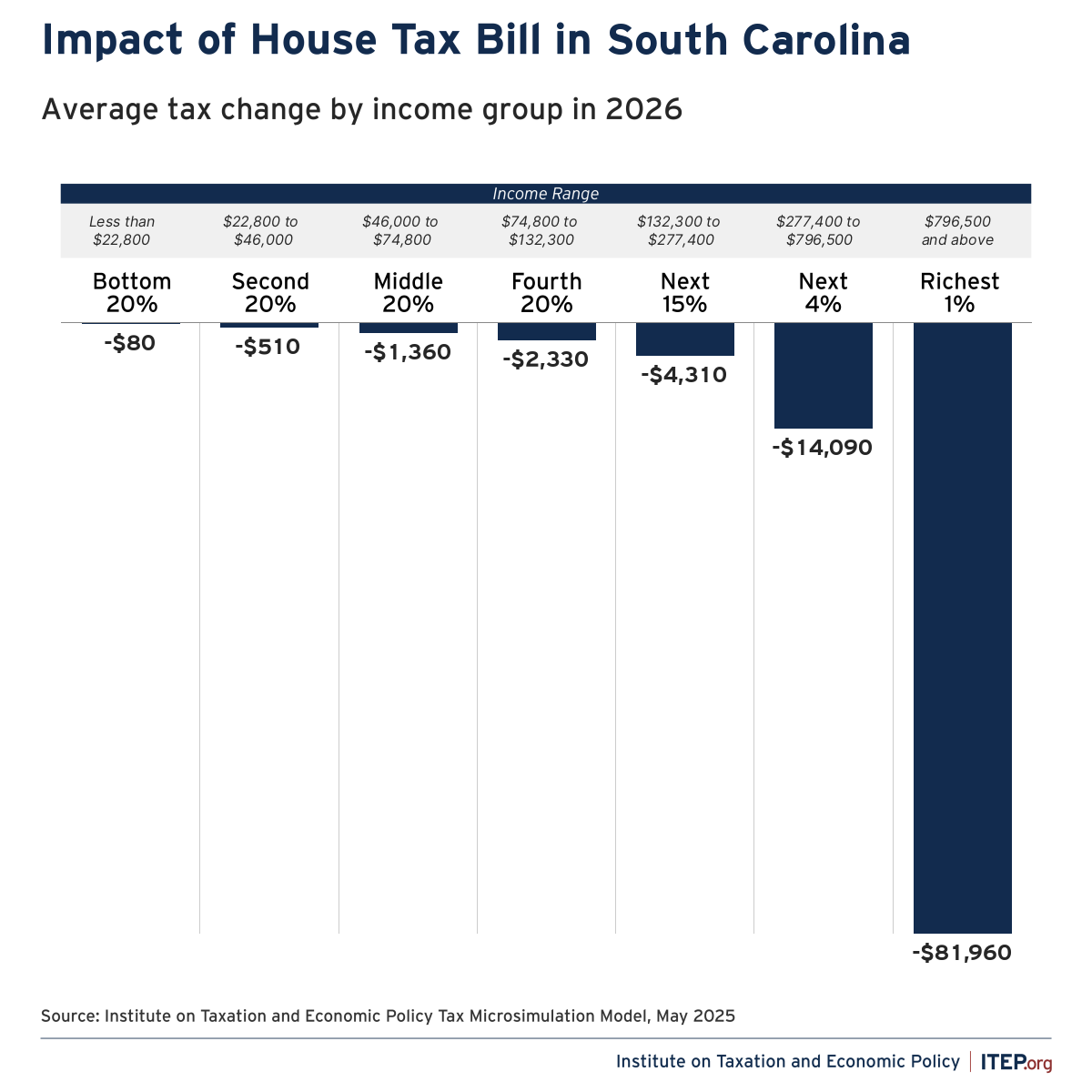

The initial impact of H 4216 would result in a $309 million revenue loss in 2026, according to South Carolina’s Revenue and Fiscal Affairs Office. The swap from federal deductions to the new SCIAD would initially raise taxes for 23 percent of filers. While most of these increases are on the highest-income 20 percent of filers who are now less likely to receive the new SCIAD, the overall distribution of the tax changes remains regressive. The bottom 20 percent of South Carolinians – households making under $23,200 annually – would receive no tax savings. Rather, the lowest-income South Carolinians are more likely to see a tax increase due to the new $200 cap on the state’s EITC.

Middle-income and working-class South Carolinians do not fare much better. The average household in the middle 20 percent of South Carolinians – with annual incomes of $59,900 – would see an average tax cut of $146 a year. The wealthiest South Carolinians get by far the largest tax cut. The top 1 percent of South Carolinians – with annual average incomes of $1.7 million – would see a tax cut of $3,139 in 2026.

Figure 1

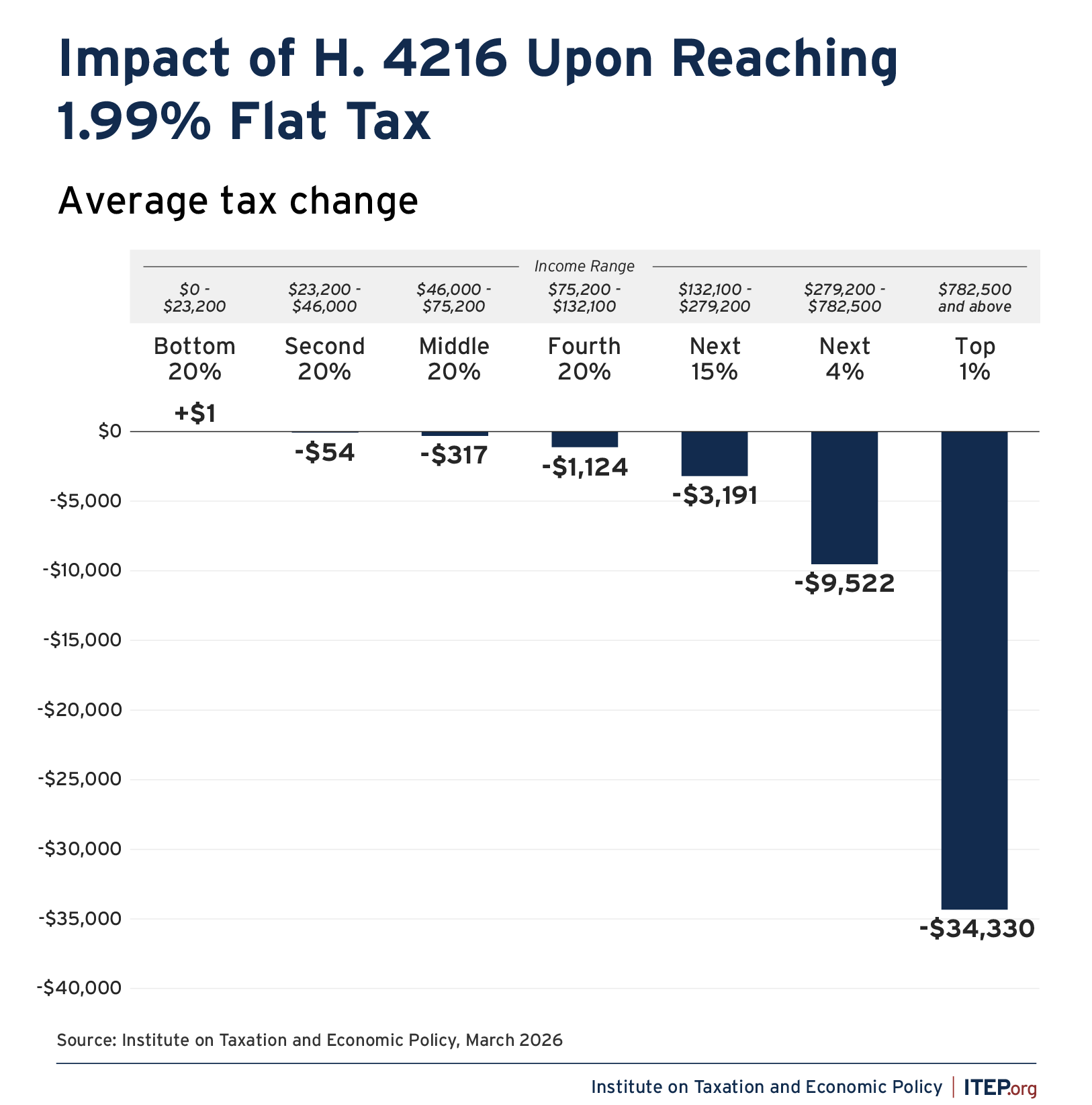

The legislation becomes increasingly more expensive and regressive, providing a larger benefit to the richest in the state, as the tax rates get closer to zero. Triggered reductions, under which certain conditions must be met before further rate cuts occur, create a façade of fiscal responsibility. On top of that, lawmakers across the country—impatient when triggers aren’t met—often weaken these requirements or accelerate rate cuts in subsequent legislative sessions.

When the brackets collapse into a 1.99 percent flat rate, the revenue loss jumps to $4.3 billion a year, according to ITEP modeling, with the bottom 20 percent continuing to receive no tax cut and the top 1 percent of South Carolinians seeing a $34,330 average annual tax cut. As a percentage of income, this amounts to a tax cut for the wealthiest South Carolinians that is four times larger than middle-class families receive.

Figure 2

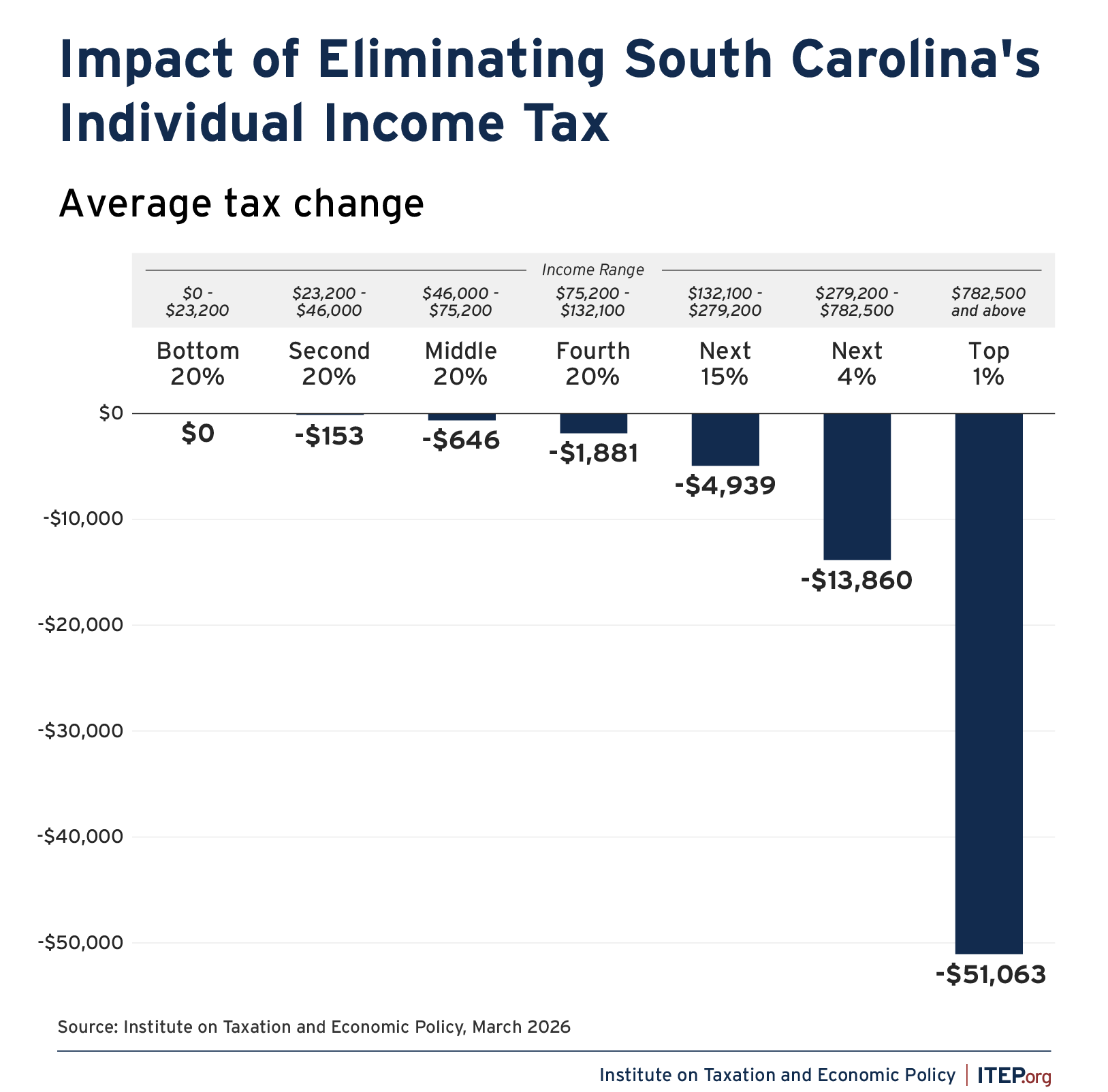

Full elimination of South Carolina’s individual income tax (as highlighted in Figure 3) is even more regressive and expensive.

The bottom 20 percent of households would still see no tax savings, everyone else would experience slightly larger tax cuts, and the top 1 percent would receive an astronomical tax cut of $51,063 annually, 3.46 percent of their total income. This would make South Carolina’s tax system even more tilted to the state’s wealthiest residents, who already enjoy the lowest effective tax rates of any income group in the state.

Figure 3

In addition to a more regressive tax code that asks more of low- and middle-income residents than the richest in the state, South Carolina would lose $6.6 billion in annual revenue (in 2026 dollars) upon eliminating its individual income tax. This equals nearly 45 percent of the state’s current general fund.

This top-heavy tax cut, nearly half of which flows to the richest 5 percent, would cost over $2 billion more than the state spends each year on public education through its general fund and over three times as much as the state spends annually on its Department of Health and Human Services. The bill includes no revenue raisers to offset this massive revenue loss, putting a wide range of public services in jeopardy.

This legislation comes on the heels of major federal tax changes under OBBBA, which provided a massive giveaway to the richest South Carolinians. The tax cuts given to South Carolina’s wealthiest from federal tax changes should be reason enough for South Carolina lawmakers to not only refute further individual income tax cuts but recapture a portion of the preposterous windfall to accommodate the many cost shifts pushed onto states by OBBBA.

Conclusion

South Carolina’s H 4216, recently signed into law, is a regressive tax cut that will disproportionately benefit the state’s highest-income residents while simultaneously jeopardizing the state’s ability to pay for basic public services in the years to come.

At a time when state budgets will be forced to take on more responsibility for programs such as SNAP and Medicaid, as the economy becomes increasingly fragile, and as everyday South Carolinians struggle to get ahead, paving a path for the wealthiest residents to receive tens of thousands of dollars in annual tax cuts on top of the giveaway provided by Congress last year is irresponsible and short-sighted.

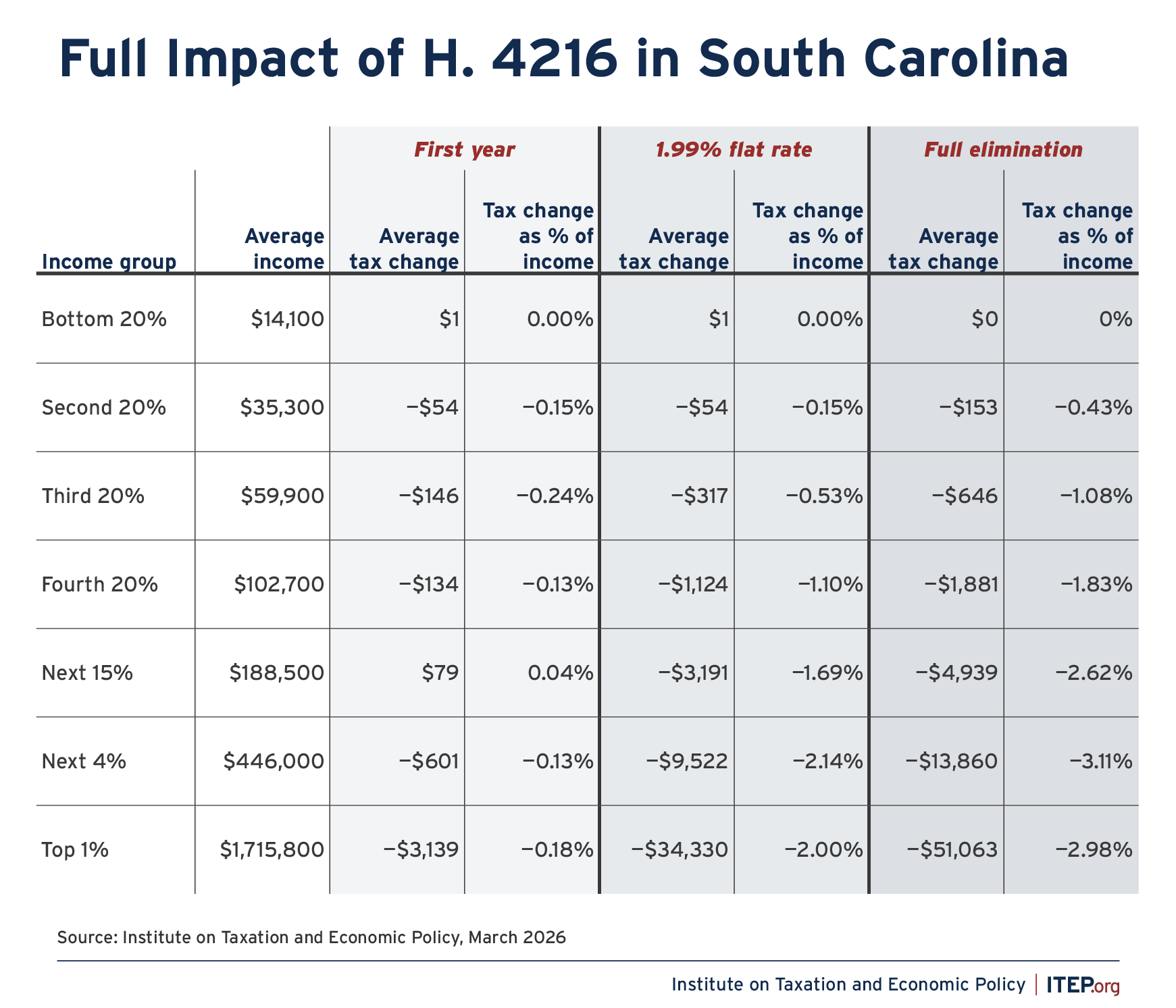

Figure 4

Endnotes

- 1. According to the South Carolina Revenue and Fiscal Affairs Office: The rate will be reduced annually such that the adjustment to the tax rate is projected to reduce individual income tax revenue by approximately $200,000,000 or 25 percent of the recurring income tax revenue surplus, whichever is greater. If the projected growth in individual income tax revenue is projected to be less than $200,000,000, then the tax rate adjustment must be limited to the projected increase in individual income tax revenue. The determination of the tax rate will be made annually based on the revenue forecast for the current and upcoming fiscal years as of February 15.

- 2. Although South Carolina’s EITC is set at 125 percent of the federal credit, it is non-refundable, meaning the average qualifying South Carolinian receives much less than states with smaller, refundable credits.

{kind=link}