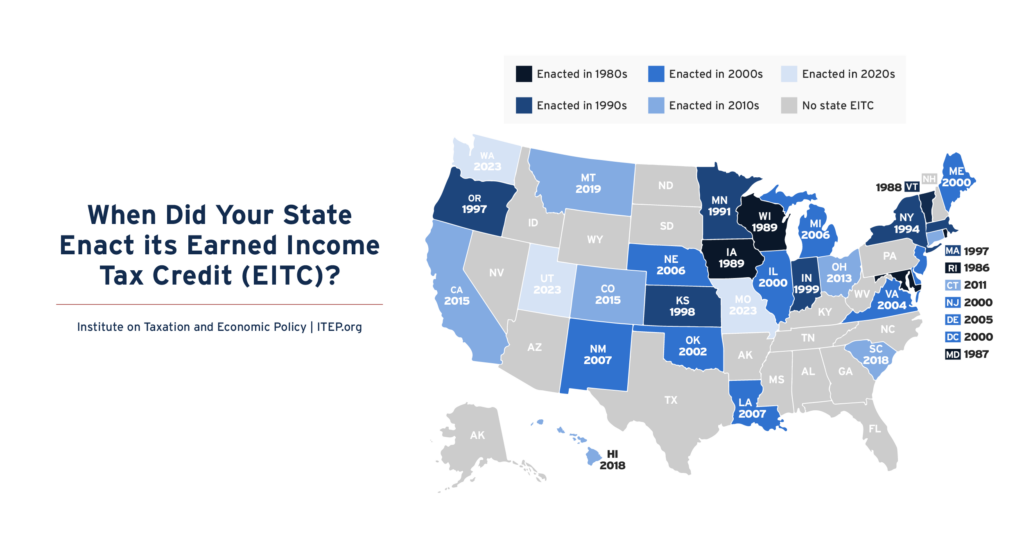

EITC

Twenty states have sales tax holidays in 2026. These sales tax holidays will cost states and localities nearly $600 million in lost revenue this year, and they're poorly targeted and too temporary to meaningfully change the regressive nature of a state’s tax system.

2026 Sessions in Review: States Fund Tax Credits by Preserving, Raising Revenue

July 2, 2026 • By Aidan Davis

In a year of cautious uncertainty around current and ongoing revenues, many state lawmakers strengthened their tax credits for families and children.

The Impact of Proposed New Tax Credit Restrictions for Immigrant Filers: An Analysis of the DACA Recipient Population

June 16, 2026 • By Carl Davis, Erika Frankel, Emma Sifre

We find that 337,000 people in households with at least one DACA recipient will suffer financial harm, and that nearly two-thirds (66 percent) of the impacted individuals are U.S. citizens.

The Impact of Proposed New Tax Credit Restrictions for Immigrant Filers: An Analysis of State EITCs

June 16, 2026 • By Neva Butkus

Immigrants and their families in as many as 30 states are at risk of seeing their state tax credits such as the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) reduced unless state lawmakers act.

New EITC Proposal Would Help Families Dealing with Rising Costs

April 30, 2026 • By Joe Hughes

A new proposal in Congress to expand the Earned Income Tax Credit (EITC) would help families with the costs of raising children. The Working Parents Tax Relief Act is one of the latest approaches to help working-class families deal with an ongoing affordability crisis.

State Rundown 4/23: While Some States Stop Digging, Others Move Full Steam Ahead with Anti-Affordability Agendas

April 23, 2026 • By ITEP Staff

Missouri lawmakers passed legislation that will have residents vote on a proposal at the ballot box. The ask: for them to pay more in sales taxes to offset cuts – and the possible elimination – of the state's individual income tax, which makes up nearly two-thirds of Missouri’s general fund.

While States Debate New Trump Tax Changes, Equity Must Be at the Core

April 20, 2026 • By Brakeyshia Samms

States continue to debate whether and how to link their state tax codes to the 2025 federal tax law. This is not just a technical debate.

South Carolina’s Expensive, Regressive Tax Law Will Eliminate State’s Income Tax

March 31, 2026 • By Neva Butkus, Dylan Grundman O'Neill

South Carolina signed into law a regressive tax cut that will disproportionately benefit the state’s highest-income residents while simultaneously jeopardizing the state’s ability to pay for basic public services in the years to come.

State Rundown 3/12: Washington Lawmakers Pass Millionaires’ Tax, Expand Working Families Tax Credit

March 12, 2026 • By ITEP Staff

Washington is on its way to making history after the legislature approved the “millionaires’ tax,” a 9.9 percent tax on income over $1 million. The bill, which is expected to raise more than $3 billion a year, making significant investments in public education and childcare, will also expand the Working Families Tax Credit – the […]

Sen. Chris Van Hollen has recently introduced the Working Americans’ Tax Cut Act, which offers a generous middle-class tax cut paid for with a new tax on millionaires.

State Rundown 2/11: This Valentine’s Day, Conscious Decoupling Is Our Love Language

February 11, 2026 • By ITEP Staff

While some may be excited for a romantic Valentine’s Day this weekend, many state lawmakers are breaking up and decoupling from recent federal tax changes that are poised to leave states with revenue shortfalls – much like a bad date who forgets their wallet and asks you to pick up the tab.

What Did 2025 State Tax Changes Mean for Racial and Economic Equity?

February 9, 2026 • By Brakeyshia Samms

The results are a mixed bag, with some states enacting promising policies that will improve tax equity and others going in the opposite direction.

Pennsylvania Just Gave Low-Income Workers a Tax Credit Boost. Now It’s Philadelphia’s Turn.

December 30, 2025 • By Kamolika Das

In the same way states are building upon federal tax credits, localities should consider building on state tax credits.

States Can Create or Expand Refundable Credits by Taxing Wealth, Addressing Federal Conformity

December 19, 2025 • By Zachary Sarver

Many states already recognize the potential of these credits to boost low- and moderate-income households. Other states should follow suit.

State Earned Income Tax Credits Support Families and Workers in 2025

September 11, 2025 • By Neva Butkus

Nearly two-thirds of states now have an Earned Income Tax Credit (EITC). Momentum continues to build on these credits that boost low-paid workers’ incomes and offset some of the taxes they pay, helping lower-income families achieve greater economic security.

Refundable tax credits were a big part of state tax policy conversations this year. In 2025, nine states improved or created Child Tax Credits or Earned Income Tax Credits.

The Earned Income Tax Credit (EITC) supports millions of workers and families and continues to grow in states and localities across the country. Today, 31 states plus the District of Columbia and Puerto Rico offer EITCs. Local EITCs can also now be found in Montgomery County, Maryland, New York City, and San Francisco, where they benefited 700,000 households in 2023.

This week, we celebrate 50 years of the federal Earned Income Tax Credit (EITC) and the impact it's had on millions of workers and families. In 2023 alone, the latest year of available data, the federal EITC alongside the refundable portion of the Child Tax Credit lifted 6.4 million people and 3.4 million children out of poverty.

Advantaging Affluence: A Distributional Analysis of Missouri HB 798’s Uneven Tax Cuts for Wealth and Work

March 28, 2025 • By Aidan Davis, Carl Davis, Dylan Grundman O'Neill, Eli Byerly-Duke, Matthew Gardner

Missouri House Bill 798 would reduce personal and corporate income tax rates, fully eliminate taxes on capital gains income from sale of assets, and eliminates the state’s modest Earned Income Tax Credit that assists many working people in lower-paid jobs. HB 798 would radically transform Missouri’s income tax code into a system that privileges income from wealth over income from work, leaving many middle-income families to pay a higher income tax rate than wealthy people living off their investments.

The no tax on tips idea isn't a new one, but it's always been abandoned because it's practically impossible to do without creating new avenues for tax avoidance. Despite its embrace by the candidates from both major parties, this policy idea would do little to help the roughly 4 million people who work in tipped occupations while creating a host of problems.

Four states expanded or boosted refundable tax credits for children and families, and the District of Columbia is poised to create a new Child Tax Credit. These actions — in Colorado, Illinois, New York, Utah, and D.C. — continue the recent trend of improving the well-being of children and families with refundable tax credits.

Improving Refundable Tax Credits by Making Them Immigrant-Inclusive

July 17, 2024 • By Emma Sifre, Marco Guzman

Undocumented immigrants who work and pay taxes but don't have a valid Social Security number for either themselves or their children are excluded from federal EITC and CTC benefits. Fortunately, several states have stepped in to ensure undocumented immigrants are not left behind by the gaps in the federal EITC and CTC. State lawmakers should continue to ensure that immigrants who are otherwise eligible for these tax credits receive them.

These Three Local EITCs Are Boosting Family Incomes at Tax Time

April 10, 2024 • By Andrew Boardman

This tax season more than 800,000 households in New York City, Maryland's Montgomery County, and San Francisco are set to receive a boost through local refundable EITCs. These credits put dollars directly into the pockets of low-income households, equipping families with resources to better make ends meet and invest in their futures. In turn, they can help build stronger, fairer, and more resilient communities.

States differ dramatically in how much they allow families to make choices about whether and when to have children and how much support they provide when families do. But there is a clear pattern: the states that compel childbirth spend less to help children once they are born.

Three Localities are Boosting Communities with Refundable EITCs; Others Should Follow Suit

October 30, 2023 • By Kamolika Das

Most states already offer their own Earned Income Tax Credits, typically matching a certain percentage of residents’ federal EITC, but this is still a rarity among localities.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.