Introduction

In 2018, 38.1 million adults and children lived in poverty in the United States according to data released this month by the U.S. Census Bureau.[1] While the official poverty rate declined for the fourth year in a row, falling from 12.3 percent to 11.8 percent in 2018, still more than one in eight people live in households with poverty-level income. The poverty rates decreased a statistically significant amount in 14 states between 2017 and 2018 and increased in one state.[2]

The Supplemental Poverty Measure (SPM), a more comprehensive measure based on expenditures of food, clothing, housing and utilities, also demonstrates that the tax code can be used as an effective poverty-fighting tool. The federal EITC and refundable portion of the Child Tax Credit, for example, together lifted 8.3 million people out of poverty decreasing the supplemental poverty rate from 16.5 to 13.9 percent in 2017. [3] And, thanks in large part to those credits, the supplemental poverty rate for children in 2017 was actually lower than their official poverty rate (15.6 percent compared to 17.3 percent).

Astonishingly, tax policies in virtually every state make it harder for those living in poverty to make ends meet. When all the taxes imposed by state and local governments are taken into account, every state imposes higher effective tax rates on poor families than on the richest taxpayers.

Despite this unlevel playing field states create for their poorest residents through existing policies, many state policymakers have proposed (and in some cases enacted) tax increases on the poor under the guise of “tax reform,” often to finance tax cuts for their wealthiest residents and profitable corporations.

State and local tax systems typically make things harder for families living in poverty. A 2018 ITEP report, Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, found that the poorest 20 percent of Americans paid on average 11.4 percent of their incomes in state and local taxes. Middle-income taxpayers didn’t fare much better, paying an average of 9.9 percent of their incomes toward those taxes. But when it comes to the wealthiest 1 percent, ITEP found they paid an average of just 7.4 percent of their incomes in state and local taxes.

Nearly every state and local tax system takes a much greater share of income from middle- and low-income families than from the wealthy. This “soak the poor” strategy from a budgeting perspective does not yield much revenue compared to modest taxes on the rich. It also pushes low-income families further into poverty and increases the likelihood that they will need to rely on safety-net programs.

There is a better approach. Just as state and local tax policies can push individuals and families further into poverty, there are tax policy tools available that can help them move out of poverty. In most states, a true remedy to improve state tax fairness would require comprehensive tax reform. Short of this, lawmakers should use their states’ tax systems as a means of providing affordable, effective and targeted assistance to people living in or close to poverty in their states. Through the use of tax policy tools, state lawmakers can take steps to improve the standard of living for low-income residents. Similar to the way in which the Supplemental Nutrition Assistance Program (SNAP) helps families put food on the table, thoughtful changes to state tax codes can help struggling families pay for necessities.

This report presents a comprehensive overview of anti-poverty tax policies, surveys tax policy decisions made in the states in 2019 and offers recommendations that every state should consider to help families rise out of poverty. States can jump start their anti-poverty efforts by enacting one or more of four proven and effective tax strategies to reduce the share of taxes paid by low- and moderate-income families: state Earned Income Tax Credits, property tax circuit breakers, targeted low-income credits, and child-related tax credits.

2019 State Developments in Poverty Reducing Tax Policy |

|

|---|---|

| CALIFORNIA lawmakers more than doubled the state’s EITC with three key expansions: eligible families with at least one child under age six will receive an additional $1,000 credit, the amount of the base credit was increased for some beneficiaries, and the income eligibility was increased to allow full-time minimum wage workers to benefit. | |

| ILLINOIS lawmakers increased the state’s property tax credit and created a nonrefundable $100 per child credit in legislation contingent on voter approval in 2020 of an initiative to enact a graduated income tax. | |

| MAINE took similarly substantive steps to strengthen its EITC for young workers and those without children in the home. Lawmakers lowered the age eligibility threshold for childless workers from 24 to 18 and increased the percentage of the credit for these workers from 5 to 25 percent (recognizing this group receives a fraction of the federal EITC compared to those with children in the home). All other eligible workers will see their credit increased from 5 to 12 percent of the federal EITC. Maine lawmakers also expanded the states Property Tax Fairness Credit to benefit more Maine families and to provide larger refunds to many of those who are eligible. | |

| MARYLAND expanded the state’s Child and Dependent Care Expenses Credit to more families, increasing the income cap from $50,000 to $143,000. The expansion will send $11 to 12 million per year to these families and will vary from about $350 to $800 per family. | |

| MINNESOTA enacted a $30 million expansion of their refundable Working Family Credit. Much of the benefit will go to families with three or more children, as well as workers without children in the home (in the form of both a larger credit and a higher income ceiling), although families with one or two children will also see increases. | |

| NEW MEXICO lawmakers increased the state’s refundable Working Families Tax Credit from 10 to 17 percent of the federal credit. | |

| OHIO increased its nonrefundable Earned Income Tax Credit from 10 to 30 percent of the federal credit and removed the cap for taxpayers with incomes above $20,000. | |

| OREGON increased its refundable EITC from 11 to 12 percent for families with a child under age 3 in the home and from 8 to 9 percent for all other eligible workers. | |

State Tax Strategies for Reducing Poverty

Refundable Earned Income Tax Credits

The federal Earned Income Tax Credit (EITC) is widely recognized as an effective anti-poverty strategy. It was introduced in 1975 to provide targeted tax reductions to low-income workers and also to reward work and increase incomes.

The federal EITC is administered through the personal income tax. With the goal of encouraging greater participation in the workforce, the EITC is based on earned income, such as salaries and wages. For example, for each dollar earned up to $14,570 in 2019, families with three or more children will receive a tax credit equal to 45 percent of those earnings, up to a maximum credit of $6,557. Because the credit is designed to boost incomes for low- and moderate-income workers, there are income limits that restrict eligibility for the credit. Families continue to be eligible for the maximum credit until income reaches $19,030 for single heads of household. Above this income level, the value of the credit is gradually reduced to zero and is unavailable when family income exceeds the maximum eligibility level. The credit is entirely unavailable to families with three or more children earning more than $50,162 for single parents and $55,952 if married. For taxpayers without children, the credit is much less generous: the maximum credit is $529 and single filers earning more than $15,570 (or $21,370 for married couples without children) are ineligible.

To date, nearly two-thirds of the states (29 states and the District of Columbia—see Appendix A) offer state Earned Income Tax Credits based on the federal EITC. All of the states except Minnesota allow taxpayers to calculate their EITC as a percentage of the federal credit (Minnesota’s credit is structured as a percentage of income rather than a percent of federal credit). This approach makes the credit easy for state taxpayers to claim (since they have already calculated the amount of their federal credit) and straightforward for state tax administrators. However, states vary dramatically in the generosity of their credits. The EITC provided by the District of Columbia, for example, amounts to 40 percent of the federal credit (100 percent for workers without dependents in the home), while five states have credits that are worth less than 10 percent of the federal credit. Six states (Delaware, Hawaii, Ohio, Oklahoma, South Carolina and Virginia) allow only a non-refundable credit, limiting the ability of the credit to offset regressive state and local taxes.

In 2013, North Carolina became the first state to allow their EITC to expire. 2015, on the other hand, marked the beginning of a continued 4-year trend of states and the federal government embracing new EITCs and improvements to existing credits. The federal government made EITC expansion provisions under the American Recovery and Reinvestment Act (ARRA) permanent for families with three or more qualifying children. California enacted a new refundable EITC targeted to families living in deep poverty. Massachusetts, New Jersey, and Rhode Island lawmakers boosted the value of their state credits and Maine lawmakers converted the state’s non-refundable EITC to a fully refundable credit. 2017 saw the addition of EITCs in Hawaii, Montana and South Carolina. Louisiana, Massachusetts, New Jersey and Vermont all increased the size of their EITCs in 2018. And in 2019, California, Maine, Minnesota, New Mexico, Ohio, and Oregon all enacted expansions to their credits.

Refundability is Key

Refundability is especially important in ensuring that deserving families get the full benefit of the state EITC. Refundable credits do not depend on the amount of income taxes paid: if the credit amount exceeds your income tax liability, the excess amount is given as a refund. Thus, refundable credits are useful in offsetting the regressive nature of sales and property taxes and can provide a much-needed income boost to help families pay for basic necessities. In 2017, all but four states (Delaware, Ohio, Oklahoma, and Virginia) with EITCs offer a fully refundable credit, meaning that low-income families earning too little to owe state income taxes are ineligible for the credit. Delaware legislators passed a bill that would change the state’s nonrefundable 20 percent credit to a refundable 5.9 percent credit. The shift will benefit the state’s lowest-income workers and their families, those who earn too little owe state income taxes, but to date it has not been signed by the governor.

Expanding Benefits for Workers Without Children

State EITCs generate bipartisan support because they are easily administered and relatively inexpensive. However, EITCs are most generous to families with children. Policymakers should be aware that because the EITC was designed to specifically help families with children it does little to benefit seniors and low-income individuals without children. There are other tax provisions offered by states, like enhanced personal exemptions or standard deductions, that are available to elderly taxpayers. But for millions of low-income workers without dependents in the home, federal and state taxes force them into or deeper into poverty.[4] This subset of the population includes: working parents who do not live under the same roof as their kids, but want to provide for them; veterans and members of the military; and young workers just starting out whose low wages barely cover the cost of food and rent. The EITC itself can be modified to reach these otherwise excluded groups.

Policymakers in Washington, DC, for example, enhanced the District’s EITC for workers without children in 2014, increasing eligibility thresholds and expanding the credit to 100 percent of federal. In 2018, California eliminated the age requirement for its EITC for workers without dependents in the home. This action expanded the EITC to young workers between 18 and 24, and workers over 65. California also adjusted its state-level EITC income limits to reflect the state’s minimum wage increase to ensure that those working full-time for minimum wage are eligible to receive the credit. Maryland and Minnesota legislators also removed the state EITC’s minimum age requirement by using some of the revenue gained from the federal tax cut. In 2019, Maine lawmakers lowered the minimum age to 18 and increased the share of the federal credit workers without dependents in the home receive to 25 percent of the federal.

Recommendation: To help alleviate poverty, lawmakers and advocates in states with EITCs should consider increasing the percentage of the existing credit, making the credits fully refundable, and improving the benefits for workers without children. Those in states without a credit should consider introducing a generous and refundable EITC tied to the federal credit.

For more information, see ITEP brief Boosting Incomes and Improving Tax Equity with State Earned Income Tax Credits in 2019.

The Importance of Refundability |

|

|---|---|

| The hallmark of a truly effective low-income credit is that it is refundable. This means that if the amount of the credit exceeds the amount of personal income tax you would otherwise owe, you actually get money back. Refundability is a vital feature in low-income credits because for most fixed-income families, sales and property taxes take a much bigger bite out of their wallets than the personal income tax does. Refundable credits on income tax forms are the most cost-effective mechanism for partially offsetting the effects of regressive consumption taxes on low-income families. The recent trend to make credits nonrefundable as a measure of budgetary savings is misguided and ill-advised. | |

Property Tax Circuit Breaker for Homeowners & Renters

States employ a wide variety of mechanisms to reduce the amount of property taxes that low- and moderate-income families pay, though they vary significantly in effectiveness. A property tax circuit breaker is the only property tax reduction program explicitly designed to reduce the property tax burden on those low-income taxpayers hit hardest by the tax. Its name reflects its design: circuit breakers protect low-income residents from a property tax “overload”, just like electric circuit breakers prevent electricity surges in our homes. When a property tax bill exceeds a certain percentage of a taxpayer’s income, the circuit breaker offsets property taxes in excess of this “overload” level.

Eighteen states and DC offer property tax circuit breaker programs in 2019 that target tax reductions to low-income families who also owe significant property taxes relative to their incomes. Another 13 states provide property tax credits to some low-income families through credits based on income. By cutting off eligibility based on income, these credits do not include a provision requiring property taxes to exceed a set percentage of income to qualify for the credit (see Appendix B).

The most effective and targeted property tax credits are circuit breaker programs made available to all low-income taxpayers, regardless of age, that are also extended to renters. Because it is generally understood that renters pay property taxes indirectly in the form of higher rents, many states now extend their circuit breaker credit to renters as well. The calculation is typically the same as the one used for homeowners, with the exception that renters must assume that their property tax bill is equal to some percentage of their rent. Renters in Maryland for instance, use 15 percent of their rent as their assumed property tax in calculating their circuit breaker credit. For a circuit breaker program to be successful, an effective outreach campaign is necessary.

Recommendation: State lawmakers and advocates interested in reducing the property taxes paid by low-income homeowners and renters should consider introducing a robust circuit breaker program. States with circuit breaker programs only available to older adults or homeowners should consider expanding the program to low-income homeowners and renters of all ages.

States with the Greatest Need for Improvement |

|

|---|---|

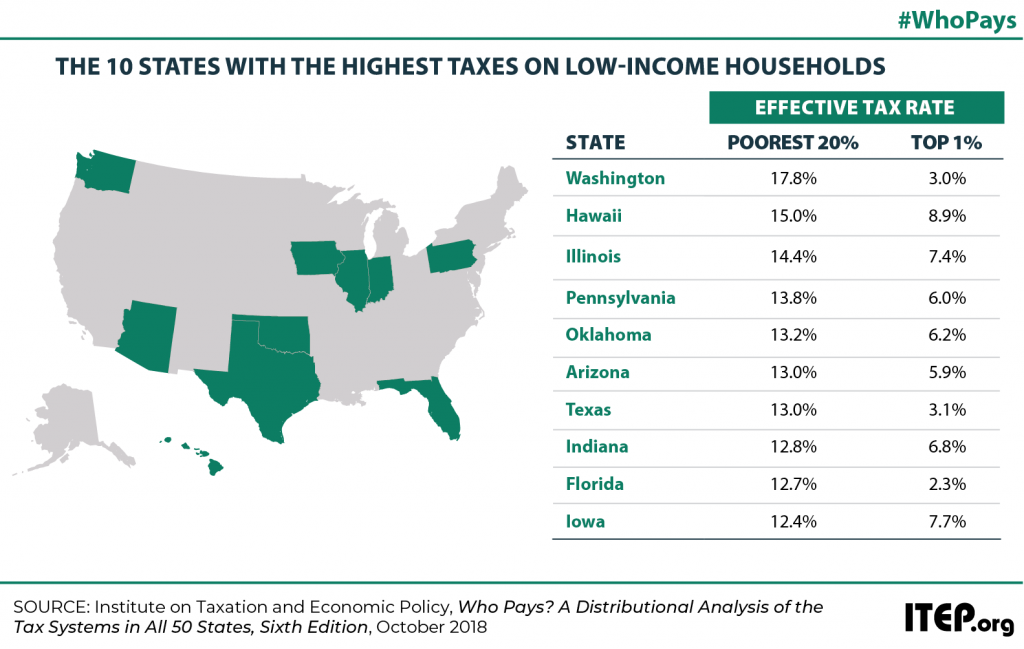

| Every state could stand to improve its tax policies toward low- and moderate-income families. However, some states have a need to consider the reforms outlined in this report. The map to the right shows the 10 states with the highest state and local taxes on the poor as a share of income according to ITEP’s 2018 Who Pays? report. Washington State, which does not have an income tax, is the highest-tax state in the country for poor people. In fact, when all state and local sales, excise, and property taxes are tallied up, Washington’s poor families pay 17.8 percent of their total income in state and local taxes. Compare that to neighboring Idaho and Oregon, where the poor pay 10.1 percent and 9.2 percent, respectively, of their incomes in state and local taxes—far less than in Washington. Hawaii, which relies heavily on consumption taxes, ranks second in its taxes on the poor, at 15 percent. Illinois—a state with a flat income tax rate—taxes its poor families at a rate of 14.4 percent, ranking third in this dubious distinction.

|

|

Targeted Low-Income Tax Credits

Because the Earned Income Tax Credit is targeted to low-income working families with children, it typically offers little or no benefits to older adults and workers without children. Thus, refundable low-income credits are a good complementary policy to state EITCs (see Appendix C).

Eleven states offer targeted income tax credits to reduce (or zero out) low-income families’ personal income tax contributions. For example, Ohio offers a nonrefundable credit that ensures that families with incomes less than $10,000 aren’t subject to the income tax. Kentucky offers a nonrefundable credit based on family size to ensure that families at or below the poverty level aren’t subject to state income taxes. Making these targeted low-income credits refundable would increase their effectiveness for low-income families.

Seven states offer an income tax credit to help offset the sales and excise taxes that low-income families pay. Some of the credits are specifically intended to offset the impact of sales taxes on groceries. These credits are normally a flat dollar amount for each family member, and are available only to taxpayers with income below a certain threshold. They are usually administered on state income tax forms, and are refundable—meaning that the full credit is given even if it exceeds the amount of income tax a claimant owes.

Refundability is crucial because it allows low-income credits to be used by taxpayers who have little or no income tax liability but pay a substantial amount of their income in sales taxes. For example, Idaho offers a refundable credit for each Idahoan and their dependents to offset grocery taxes even if taxpayers are not subject to the income tax. Kansas lawmakers eliminated their state’s refundable grocery tax credit in 2012 but enacted a new, less-effective nonrefundable credit in 2013.

Recommendation: State lawmakers and advocates committed to making sure taxes don’t push families further into poverty should create refundable, targeted low-income credits especially to help offset regressive sales and excise taxes. In states where these credits already exist, lawmakers should act to enhance them, such as by making them refundable.

For more information, see ITEP brief Options for a Less Regressive Sales Tax in 2019.

Child-Related Tax Credits

Child Tax Credits

The current federal Child Tax Credit, which provides up to $2,000 per child, is designed to provide an income boost to parents or guardians of children and other dependents. However, many low-income families do not receive the full benefit of the federal credit due to an earnings requirement and lack of full refundability for families with low incomes. Children with parents or guardians who have less than $2,500 in earnings are ineligible for the federal CTC. Families above this earnings requirement receive a federal CTC worth 15 percent of each dollar of earnings over $2,500 until reaching a maximum credit of $2,000 per child. The CTC is also only partially refundable, so families can only receive $1,400 per child as a refundable credit.

Existing state-level CTCs are limited in breadth and scope. Only two states, Oklahoma and New York, have credits directly tied to the federal Child Tax Credit. Oklahoma offers a choice between a nonrefundable credit worth 5 percent of the federal credit or a nonrefundable credit worth 20 percent of the federal Child and Dependent Care Tax Credit. The state limits the credit to taxpayers with incomes under $100,000. But like the federal CTC, the credit remains limited in its reach to families in or on the verge of poverty. New York has a refundable credit worth $100 per qualifying child or 33 percent of the taxpayer’s allowable federal credit, whichever is greater. Lawmakers in New York opted to decouple their state credit (the Empire State child credit from changes to the federal CTC, so they continue to maintain a maximum credit of $330 (the pre-TCJA maximum) and other pre-TCJA tax parameters. Colorado approved a refundable, income-limited credit for children under 6 tied to the federal CTC, but the credit remains in limbo having not received funding from the state legislature

A handful of other states have Child Tax Credits that are best thought of as state CTCs in name only. Idaho and Maine recently added nonrefundable dependent credits to replace previously existing personal exemptions. Similarly, California offers personal credits in the place of exemptions. These states have a refundable, income-limited dependent credit that is higher than the state’s personal credit for filers. The majority of states offer a dependent exemption usually at the same amount as the filer exemption. In 2018, Utah began to provide a limited CTC to account for some of the changes under TCJA while Wisconsin provided a one-time $100 child tax rebate. Illinois lawmakers approved a new $100 per child nonrefundable tax credit contingent in the approval of a 2020 ballot initiative to allow for a graduated income tax.

A state-level CTC is a tool that states can employ to remedy inequalities created by the current structure of the federal CTC while significantly reducing child poverty and deep poverty in all states.

Child and Dependent Care Credits

The average cost of full-time child care can range from $3,000 to $17,000 per year depending on the age of the child and location of the family. Low- and middle-income working parents spend an increasingly significant portion of their income on child care. Families in poverty contribute over 30 percent of their income to child care compared to about 6 percent for families at or above 200 percent of poverty.1 Most families with children need one or more incomes to make ends meet which means child care expenses are an increasingly unavoidable and unaffordable expense.

The federal government allows a nonrefundable income tax credit to help offset child care expenses. In 2017, single working parents (and two-earner married couples) with children 12 years of age or younger can claim a credit to partially offset up to $6,000 of child care expenses; low-income taxpayers can receive a credit of up to 35 percent of these expenses. The credit percentage gradually falls for higher-income taxpayers. This “sliding scale” approach helps to target tax relief somewhat more effectively to low-income taxpayers, but making the credit refundable would help those parents and children most in need.

Nearly half of the states offer some form of state income tax break for families with dependent care expenses. Of those, the majority (23 states including the District of Columbia—see Appendix D) model their state credit after the federal credit. For example, Georgia allows taxpayers to take 30 percent of their federal child and dependent care credit as a nonrefundable child care credit. Nebraska takes a slightly different approach, offering both a refundable and a nonrefundable credit depending on a family’s income. The refundable child care credit is calculated as 100 percent of the federal credit for low-income filers with incomes under $22,000. Higher earners can claim a nonrefundable credit, equal to 25 percent of the federal credit once income levels reach $29,000. This approach targets the benefits of the Nebraska credit much more efficiently to low- and middle-income parents than does the federal credit.

Recommendation: State lawmakers and advocates who want to help low-income families with children should consider increasing the value of existing child credits, making them refundable, or introducing a new refundable per child credit. Lawmakers and advocates interested in targeting child and dependent care credits to help families most in need would do well to make their credits refundable and make the credit available only to families with limited incomes.

For more information, see ITEP brief Reducing the Cost of Child Care Through State Tax Codes in 2019 and report The Case for Extending State-Level Child Tax Credits to Those Left Out: A 50-State Analysis.

Implementation: A Vital Step

The tax policies described in this report are key to helping lift families out of poverty, but simply offering these credits is not sufficient. In order to ensure that as many eligible families benefit from these anti-poverty policies as possible, lawmakers should consider how to make the credits more accessible.

A simple design, such as linking a credit to an already established credit (as is the case with state EITCs) is a good place to start. Allowing taxpayers to claim credits on their personal income tax forms (as opposed to filling out a separate form or application at a different time of the year) also increases the likelihood that eligible taxpayers will take advantage of the credits.

Furthermore, policymakers, advocacy groups, and the media must work together to ensure that an effective outreach effort is established and adequately funded so that taxpayers are informed about these credits. Outreach programs should be frequently evaluated to improve the effective reach of the tax credits offered.

Summary of Recommendations

- State lawmakers and advocates in states with EITCs should consider increasing the percentage of the existing credit, making the credits fully refundable, and improving the benefit for workers without children in the home. Those in states without a credit should consider introducing a generous and refundable EITC tied to the federal

- State lawmakers and advocates interested in reducing the property taxes paid by low-income homeowners and renters should consider introducing a robust circuit breaker States with circuit breaker programs only available to older adults or homeowners should consider expanding the program to low-income homeowners and renters of all ages.

- State lawmakers and advocates committed to making sure taxes don’t push families further into poverty should create refundable, targeted low-income credits to help offset regressive sales and excise taxes. In states where these credits already exist, lawmakers should act to enhance them, such as by making them

- State lawmakers and advocates who want to help low-income families with children should consider increasing the value of existing child credits, making them refundable, or introducing a new refundable per-child Lawmakers and advocates interested in targeting child and dependent care credits to help families most in need would do well to make their credits refundable and available only to families with limited incomes.

Conclusion

Many U.S. families continue to live in poverty, struggling to afford the high cost of housing, health care, child care and other basic necessities, and many state tax systems across the country do too little to offer the assistance low-income families need. In fact, regressive state tax structures can push working families and individuals even deeper into poverty. State lawmakers have a responsibility to ensure that their state’s tax code does not exacerbate this crisis and should consider using the low-income tax credits outlined in this paper as means of mitigating poverty in their states. Refundable tax credits are effective, time-tested anti-poverty solutions that provide additional income to help families pay for food, housing, transportation, and other necessities. The reforms discussed in this paper are among the most cost-effective anti-poverty strategies available to state lawmakers.

[1] Semega, Jessica, Melissa Kollar, John Creamer, and Abinash Mohanty, U.S. Census Bureau, Current Population Reports, P60-266,“ Income and Poverty in the United States in 2018,” U.S. Government Printing Office, Washington, DC, 2019.

[2] U.S. Census Bureau. “2018 American Community Survey 1-Year Estimates: Comparative Economic Characteristics,” Accessed: September 26, 2019. https://data.census.gov/cedsci/

[3] Liana Fox. “The Supplemental Poverty Measure: 2017,” U.S. Census Bureau, September 2018. https://www.census.gov/content/dam/Census/library/publications/2018/demo/p60-265.pdf Note: The 2018 Supplemental Poverty Measure is being revised thus this report uses 2017 data.

[4] “Childless Adults Are Lone Group Taxed Into Poverty: Expanding Earned Income Tax Credit Would Address Problem.” Center on Budget and Policy Priorities (CBPP). April 19, 2016. http://www.cbpp.org/research/federal-tax/childless-adults-are-lone-group-taxed-into-poverty