Updated July 7, 2025

On July 4, President Trump signed into law a massive tax and spending bill that largely centers around extending the 2017 Trump tax cuts. This megabill will mostly benefit the wealthiest people in the country.

You can find our analysis here. See more resources on the tax provisions in the law below.

At a glance:

- The megabill will slash taxes for the wealthy and corporations while deeply cutting funding for health care, food assistance, and other public services.

- Even with these spending cuts, the megabill will add trillions to the national deficit.

- The tax cuts for most working-class Americans will be erased by increased costs that stem from program cuts in the bill and President Trump’s tariffs.

- The megabill is very unpopular. While a majority of Americans have for decades thought that the wealthy and corporations pay too little in taxes, this bill slashes their taxes.

By the Numbers:

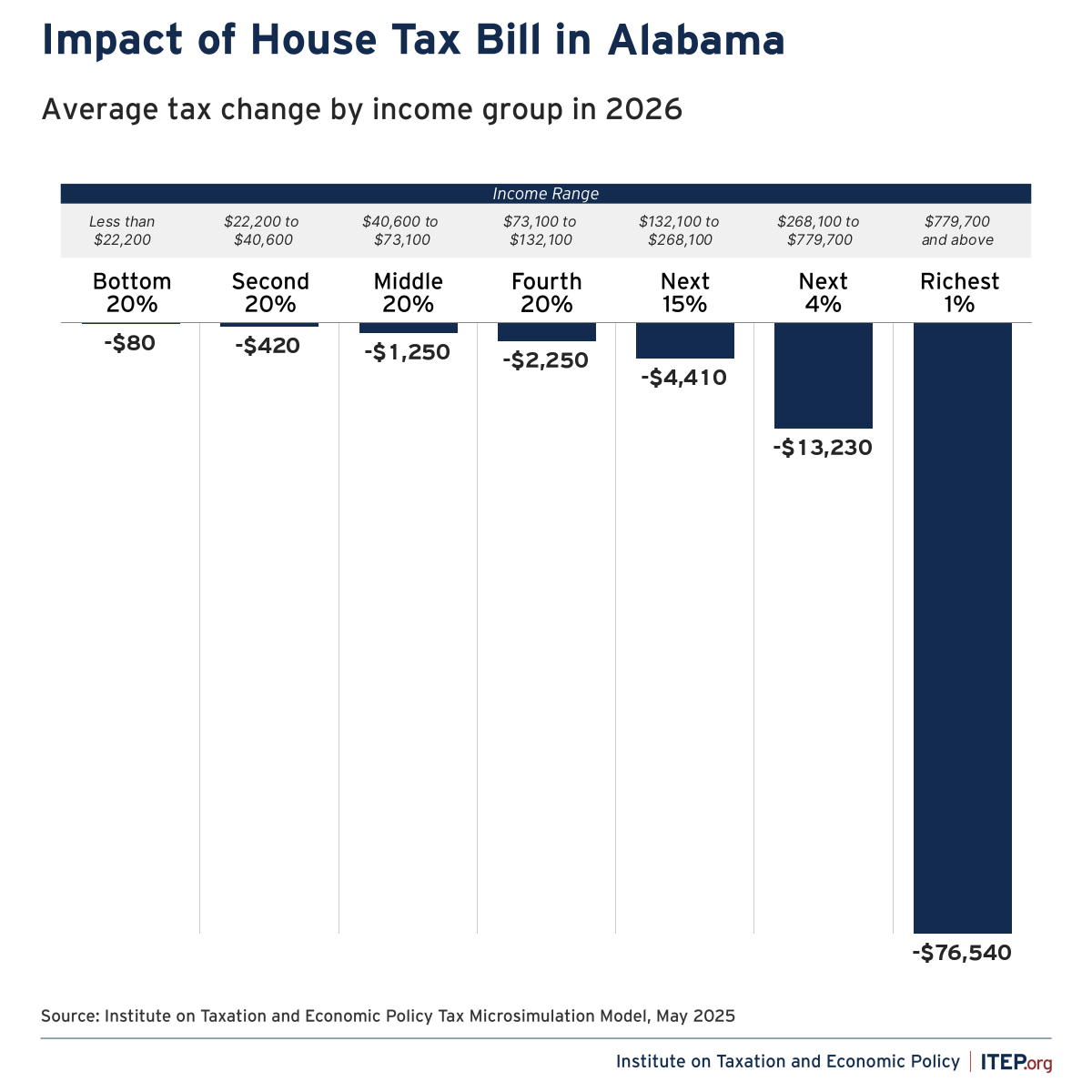

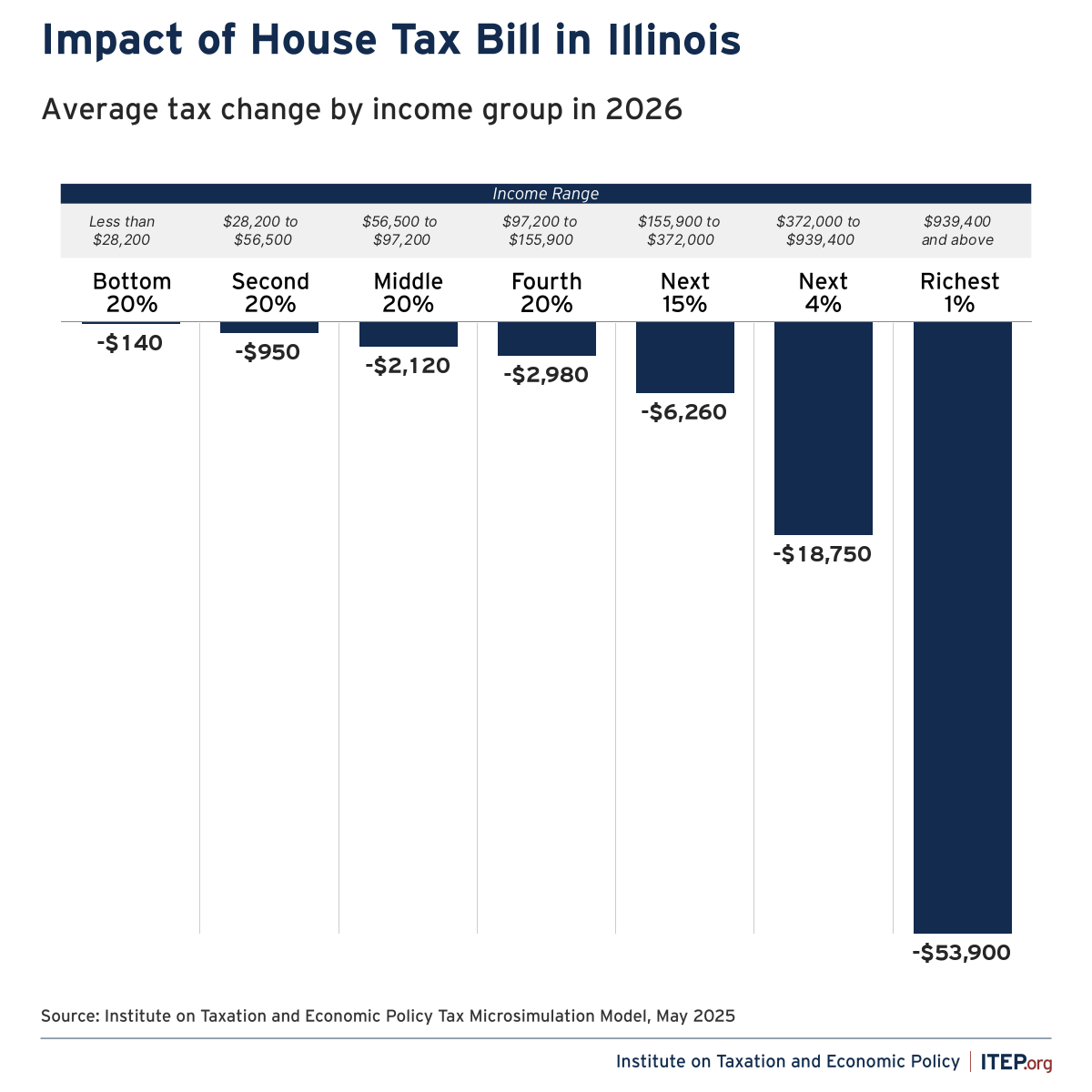

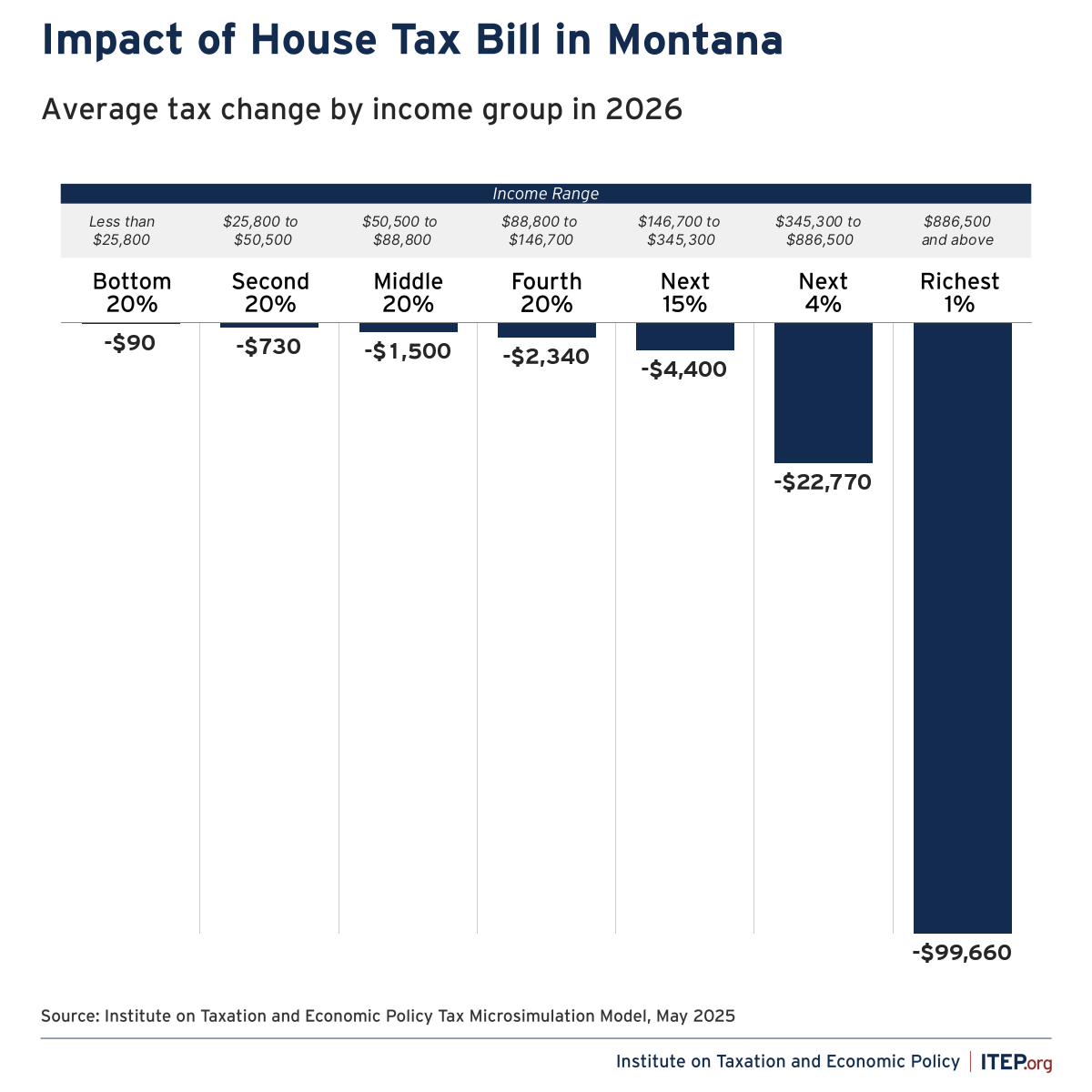

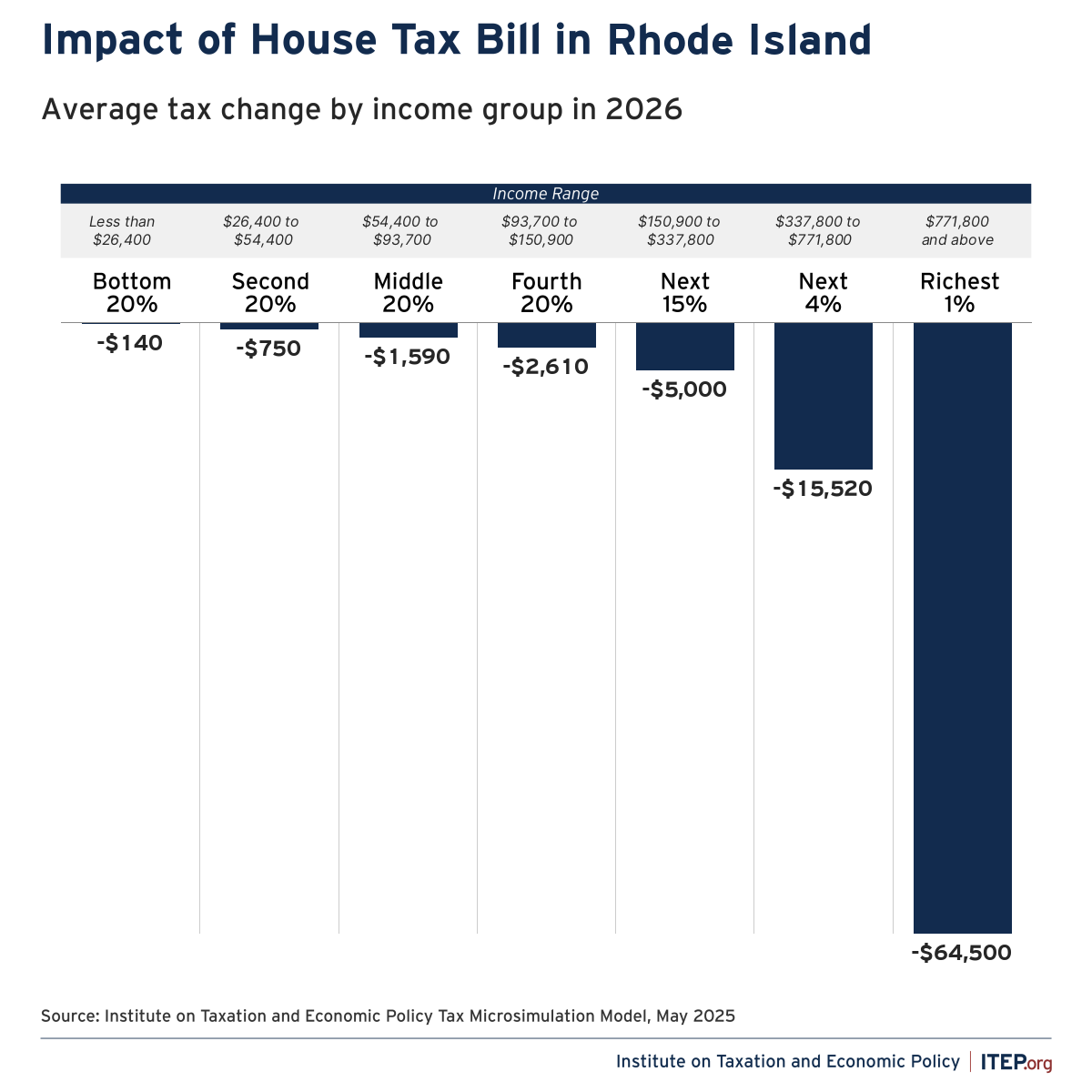

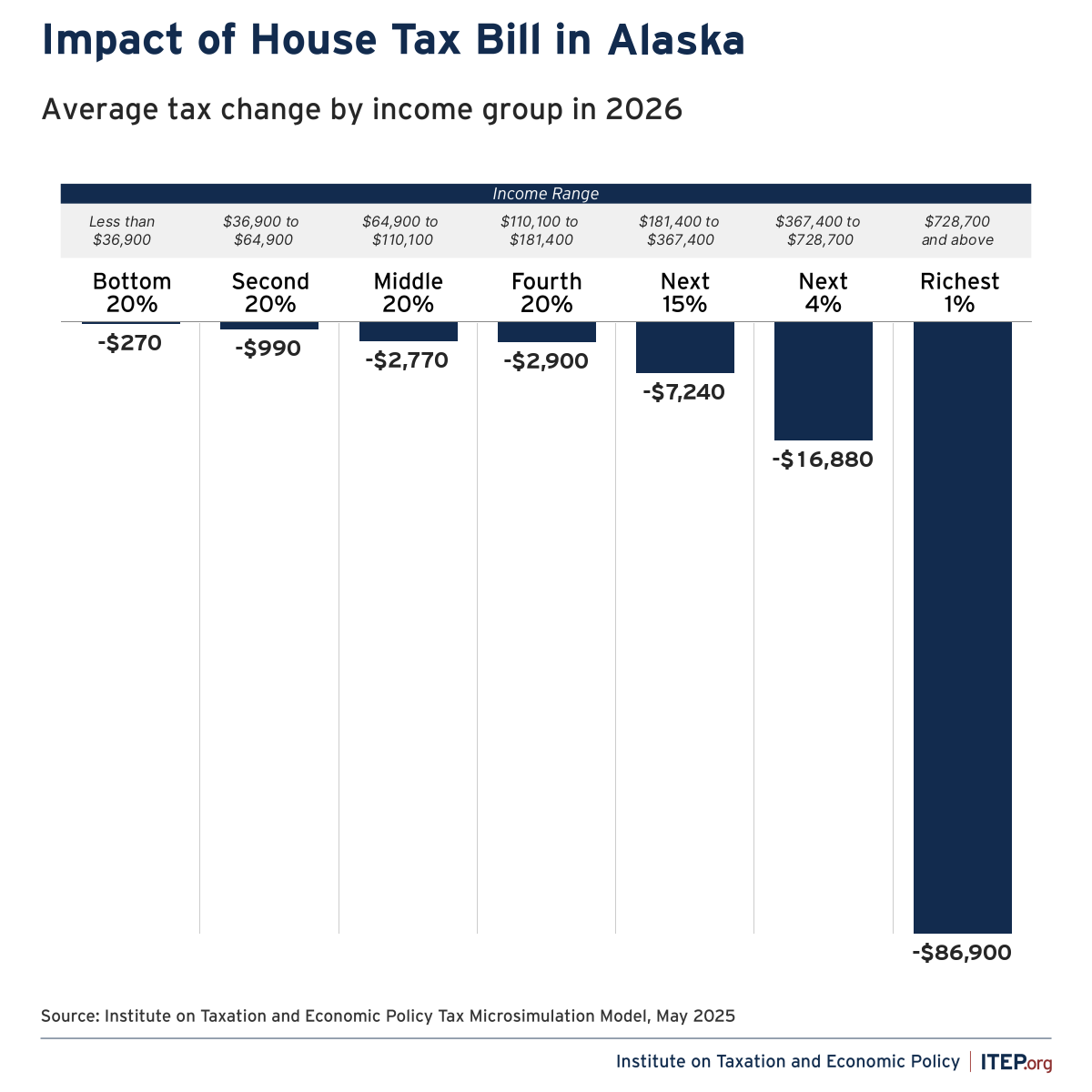

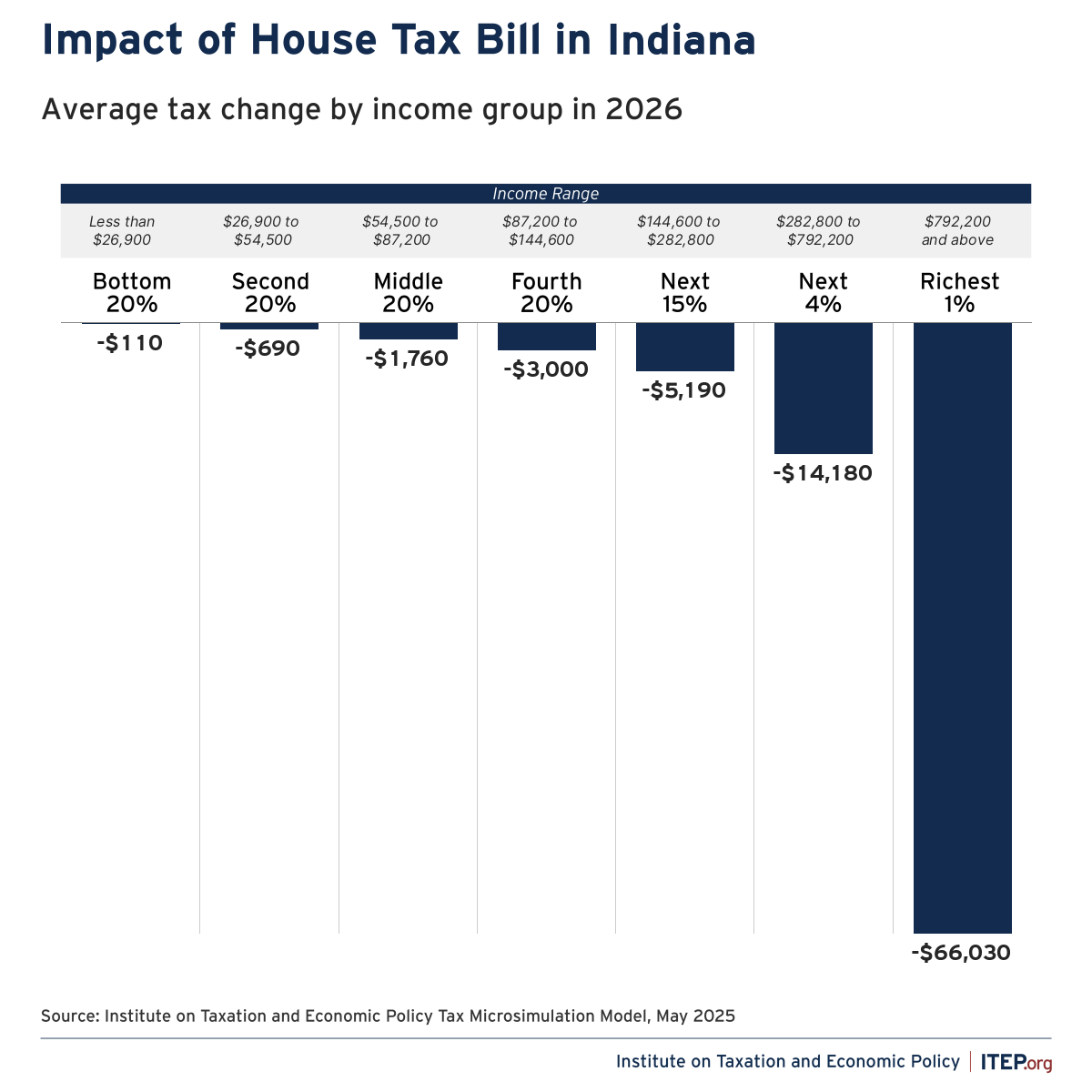

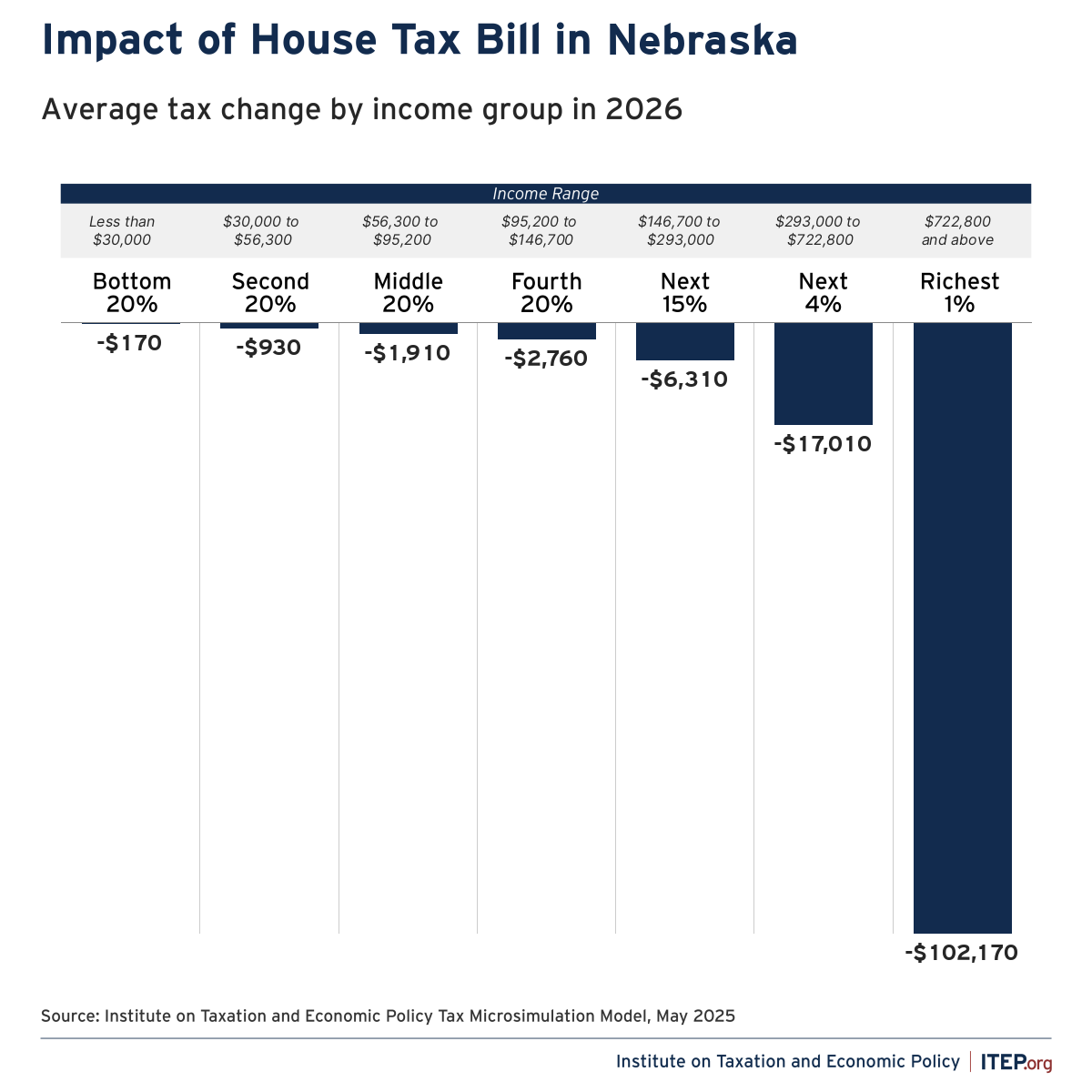

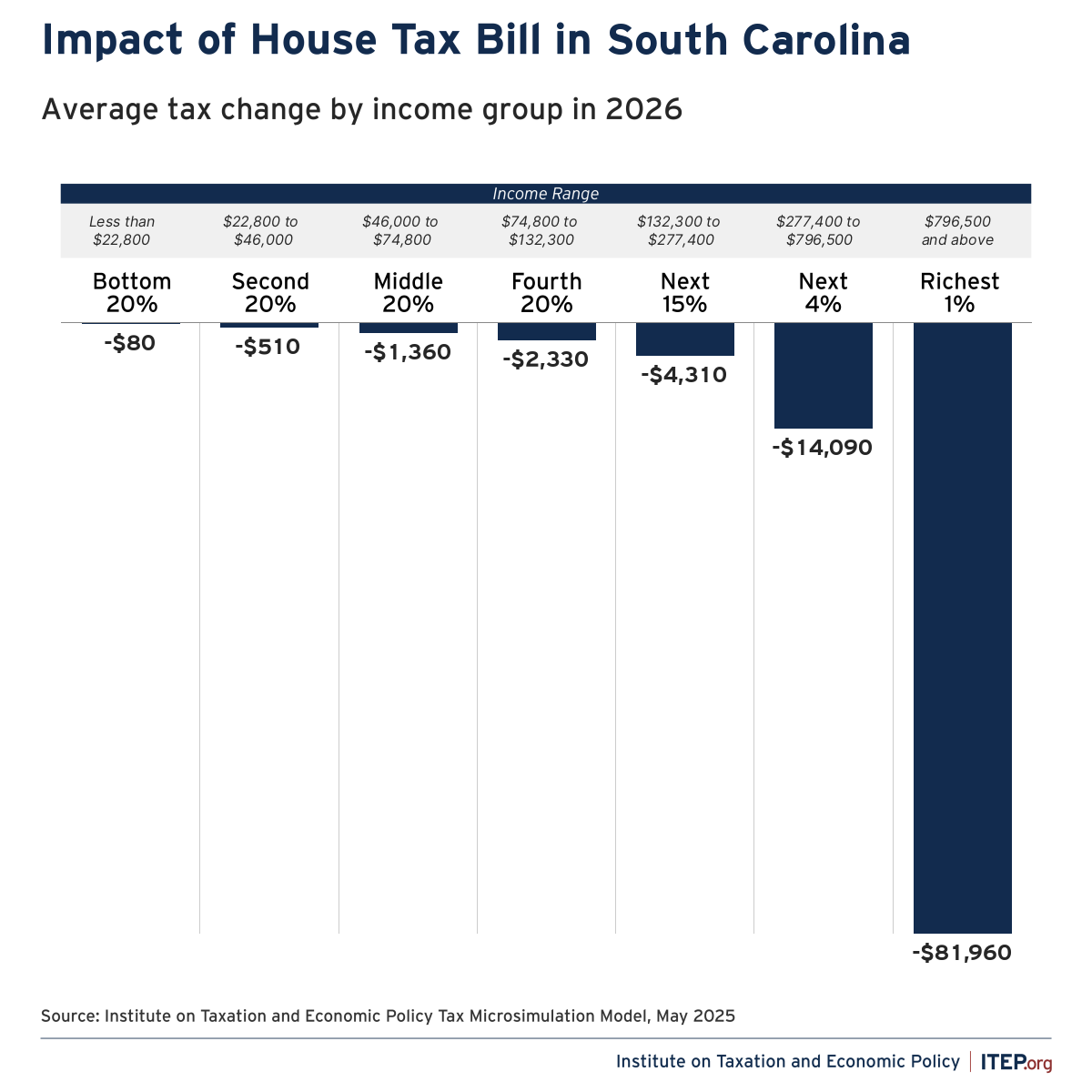

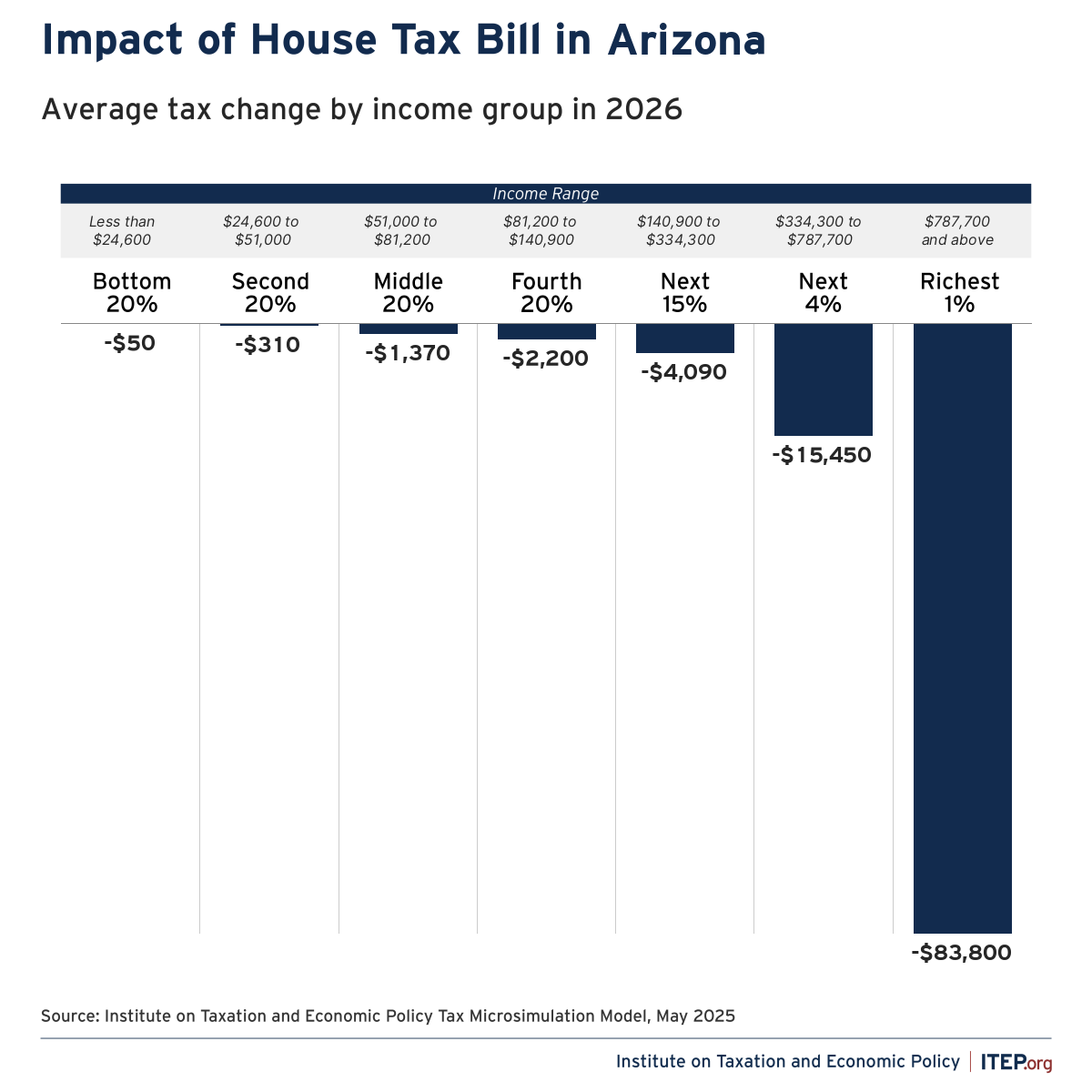

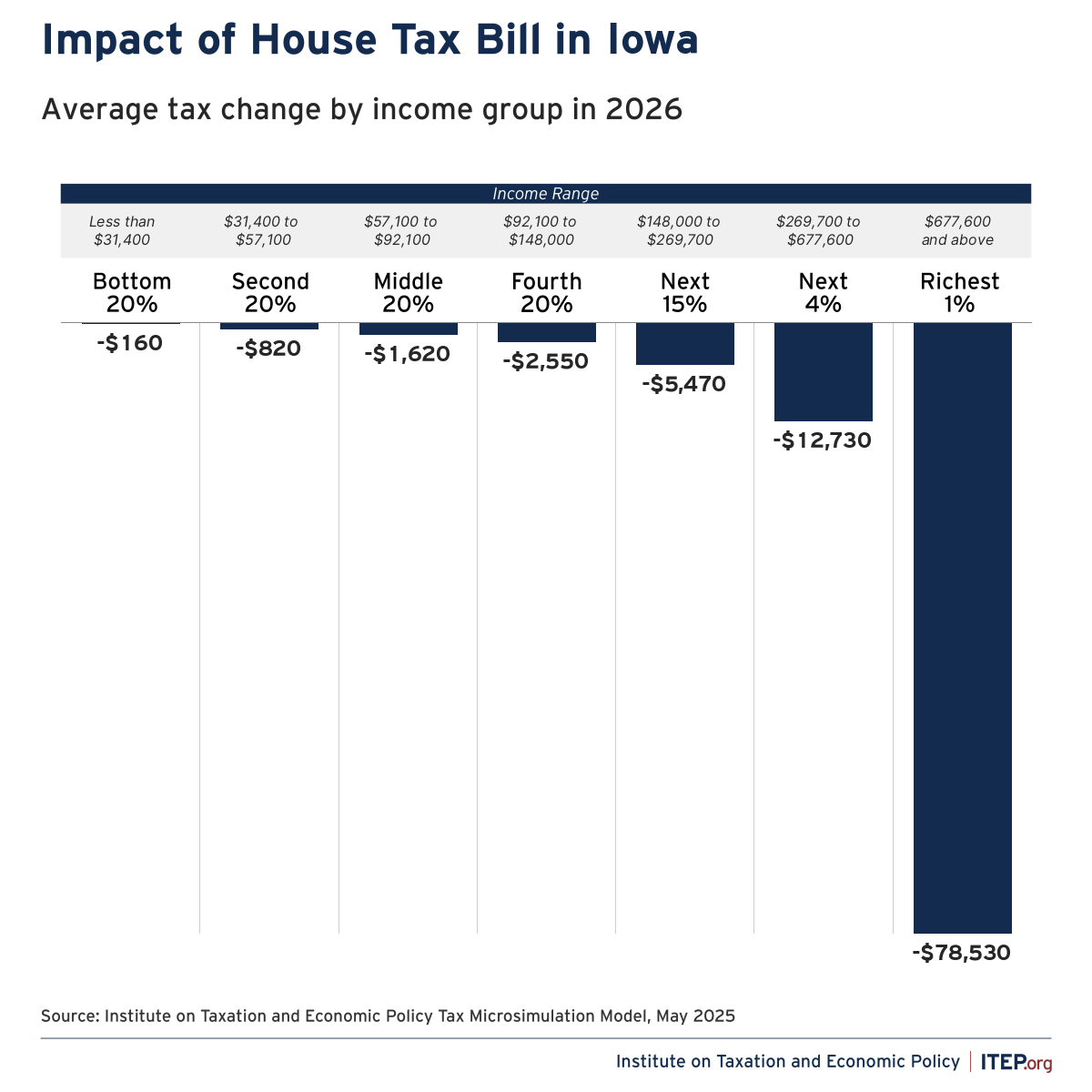

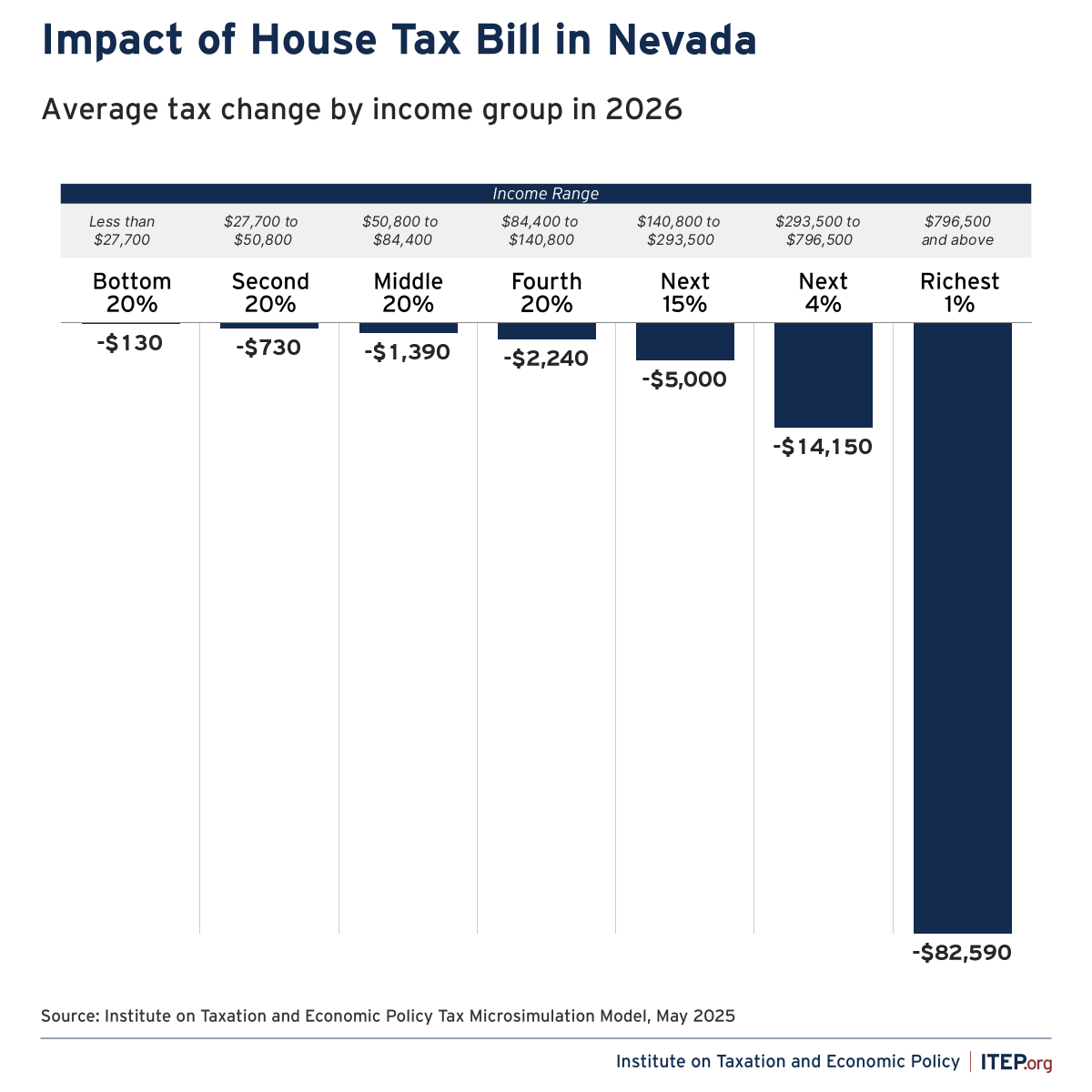

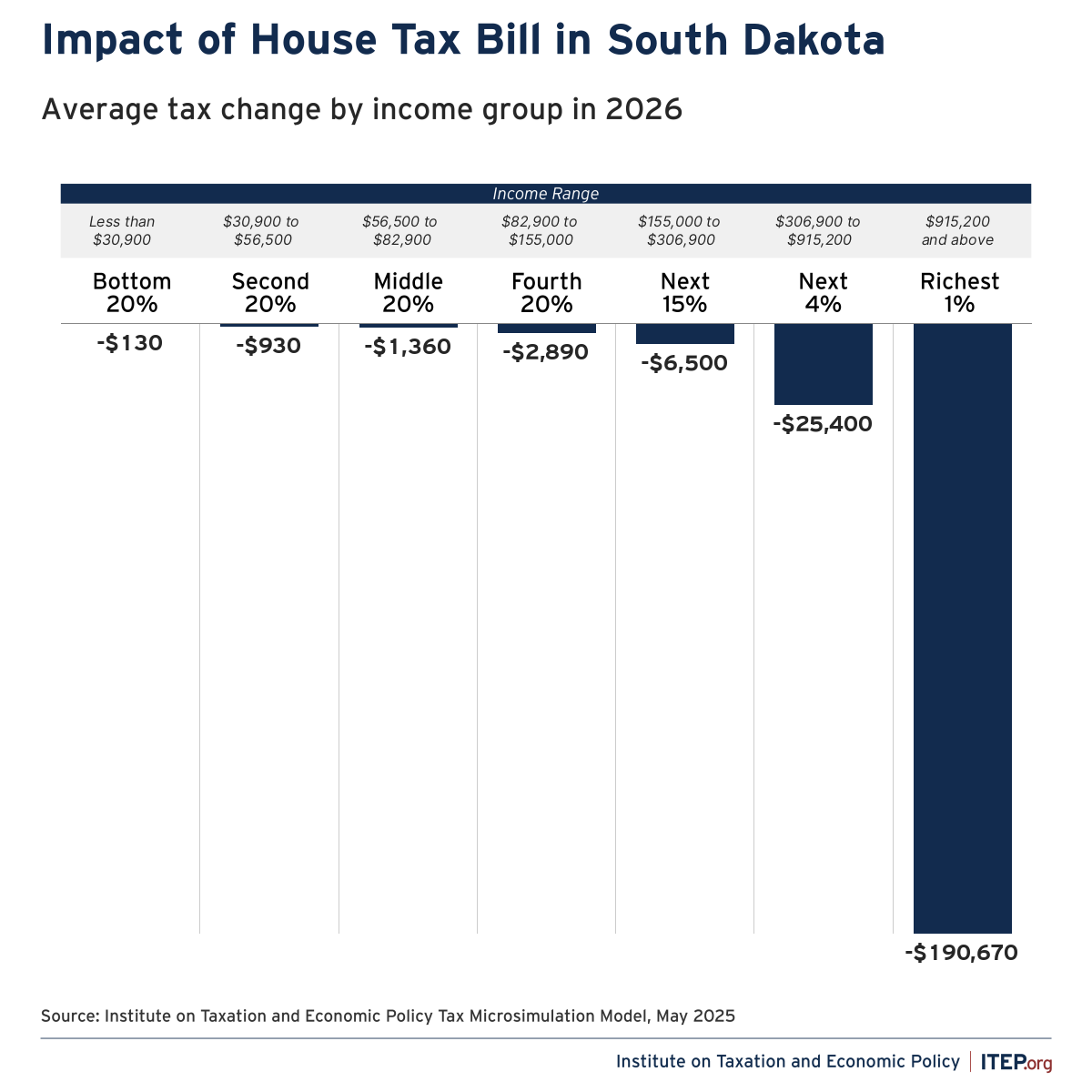

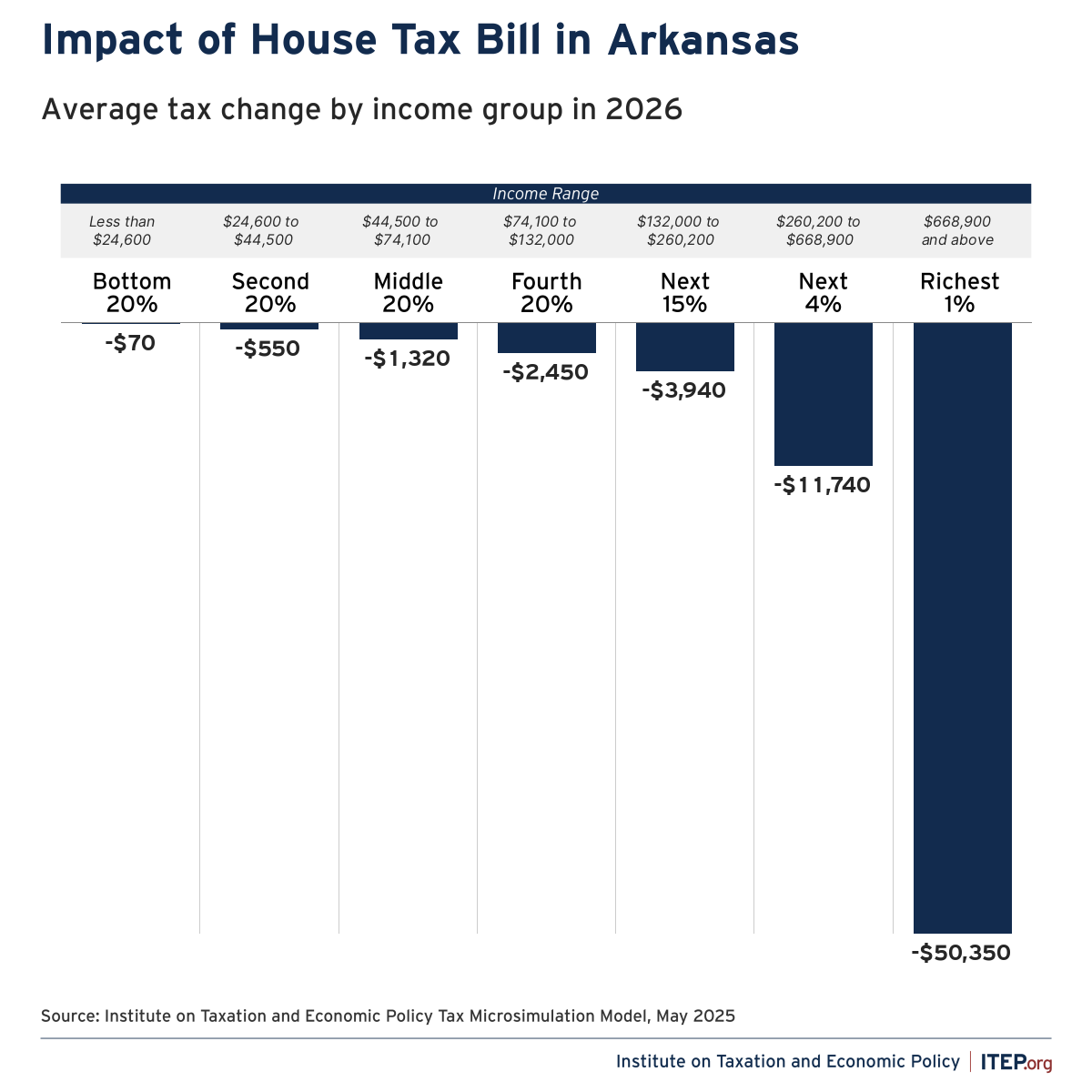

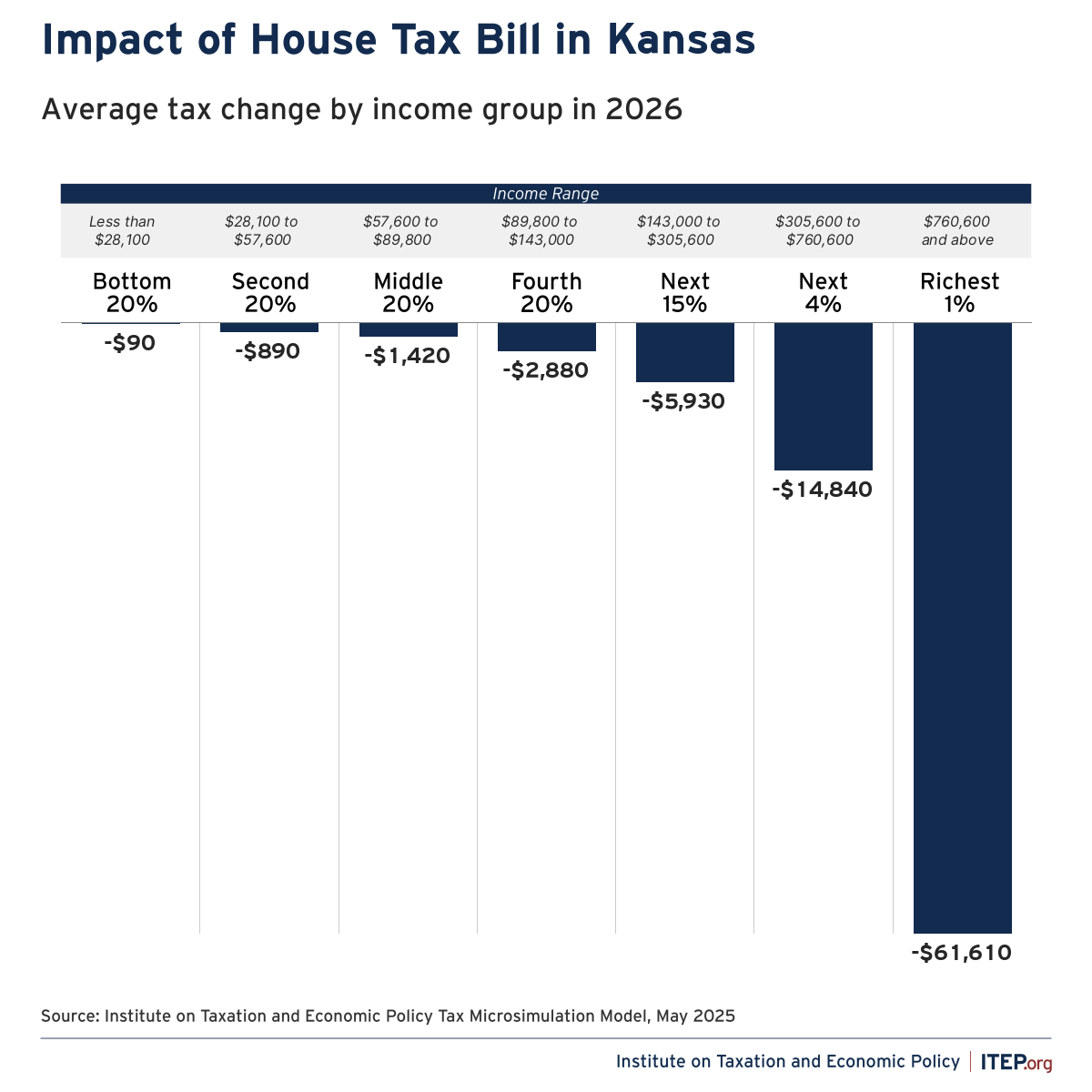

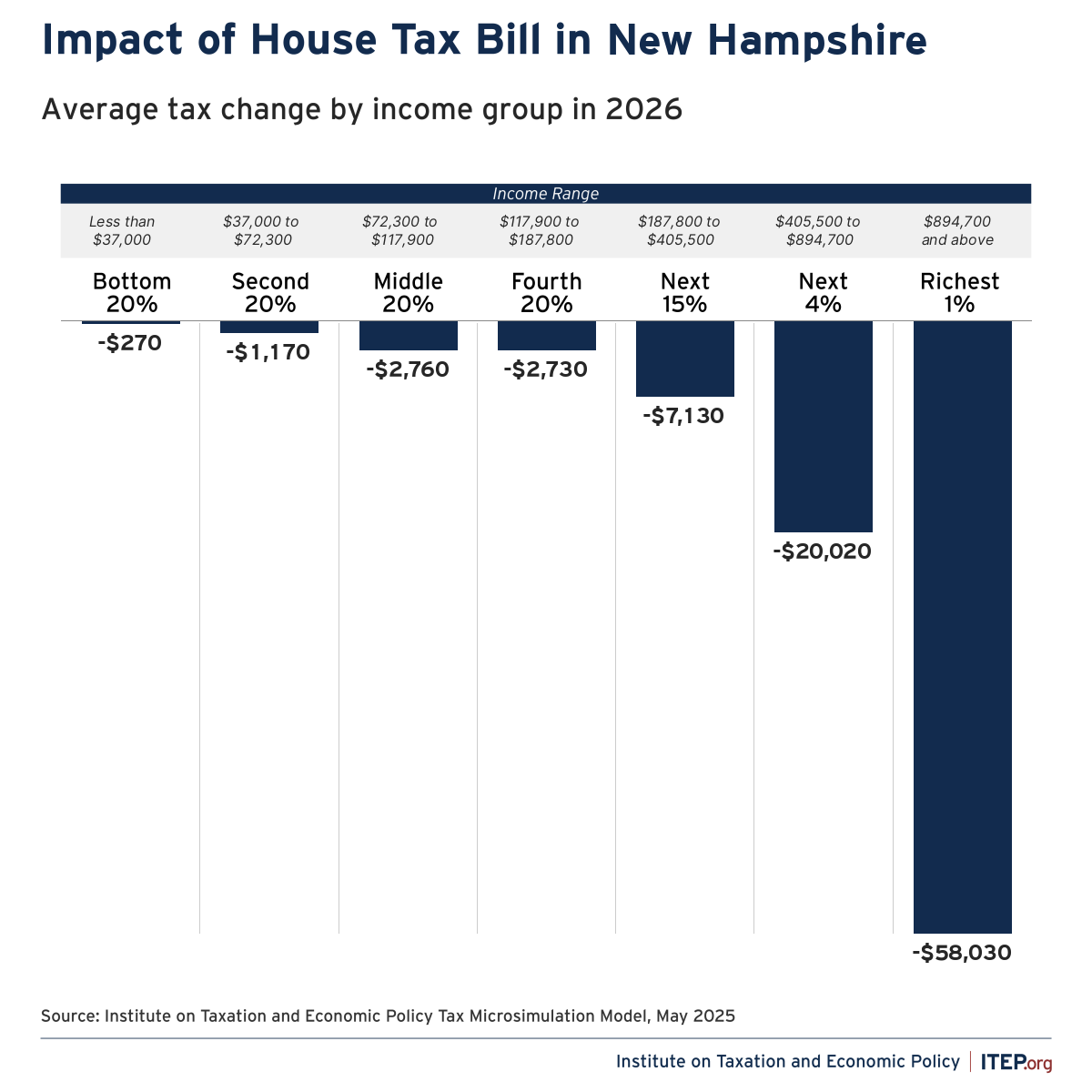

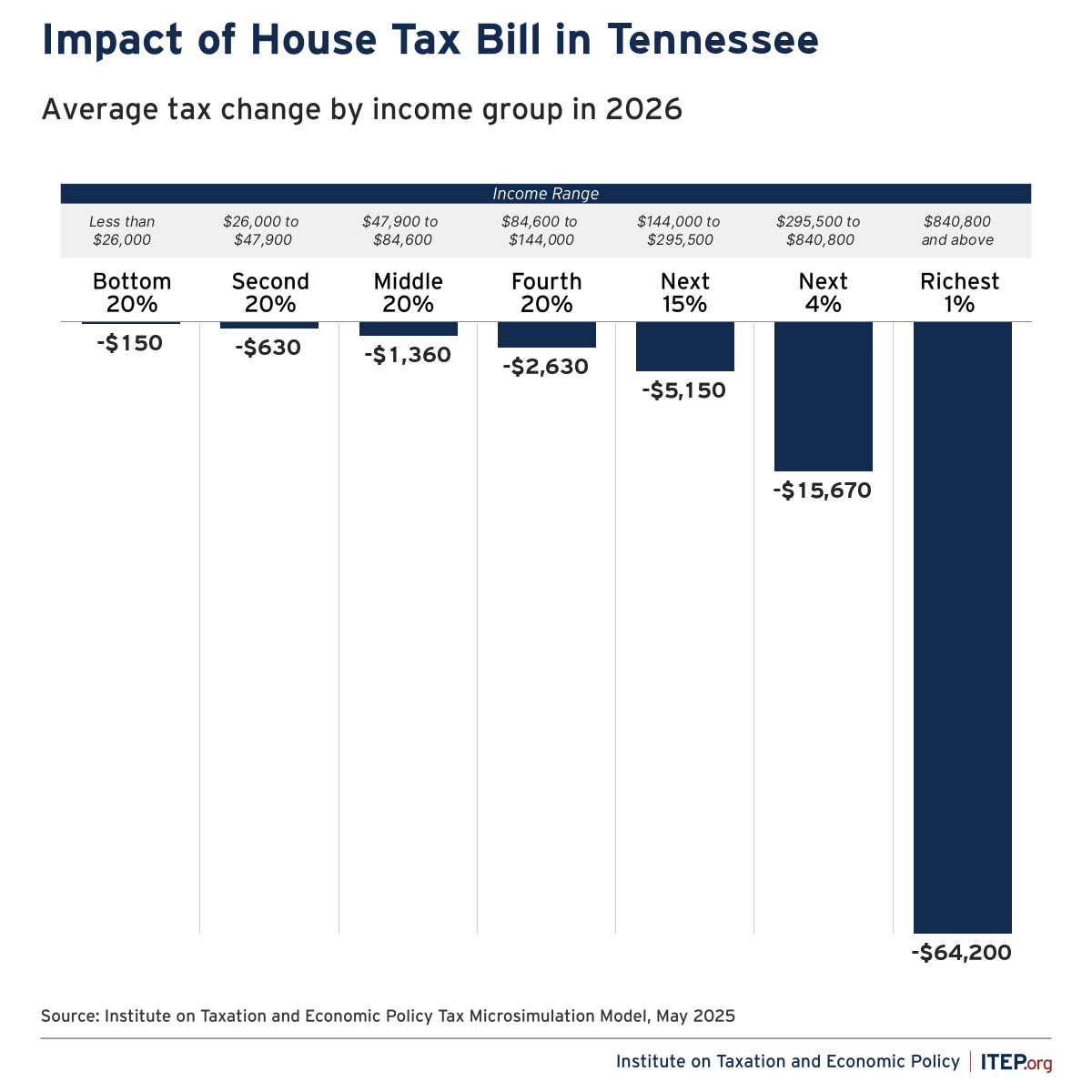

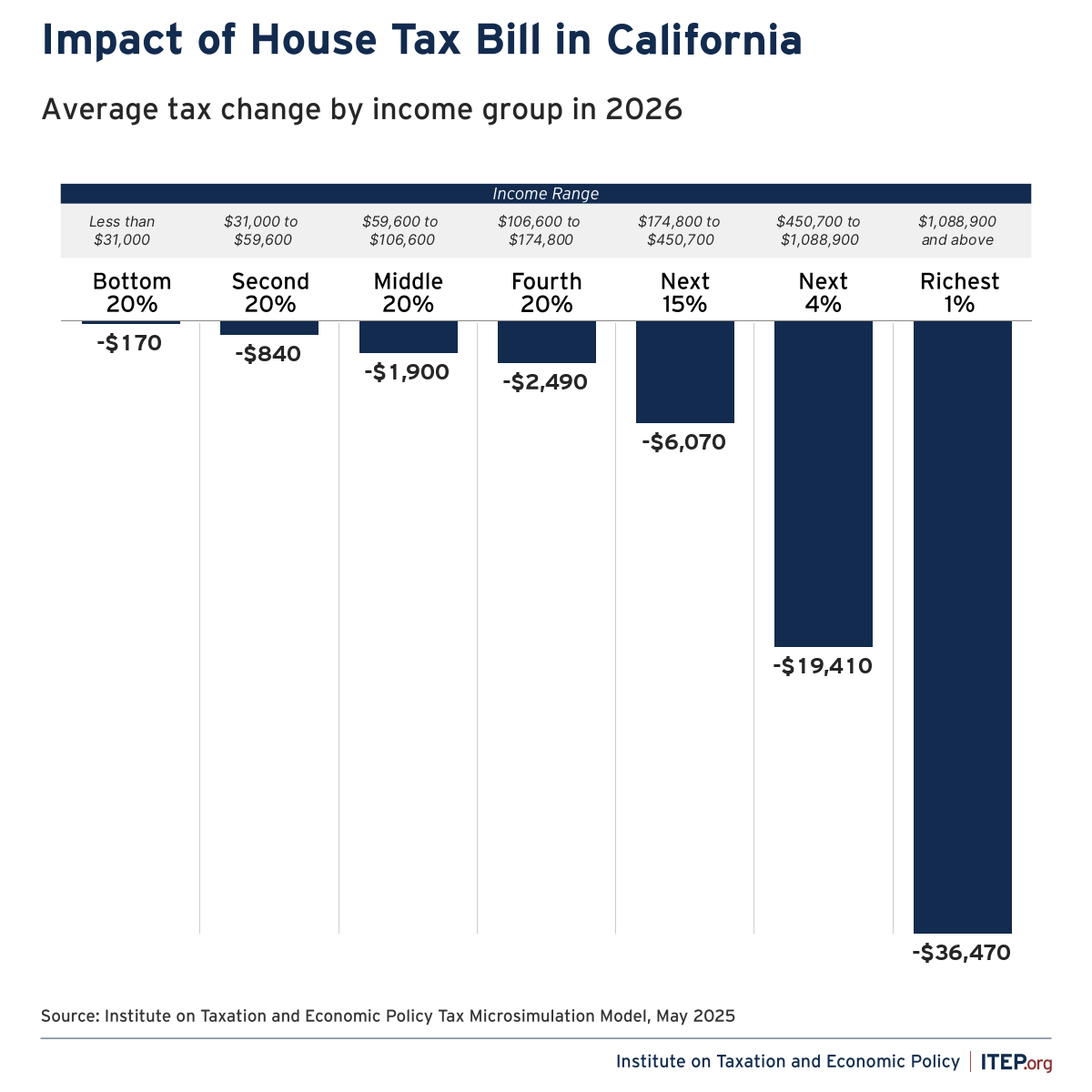

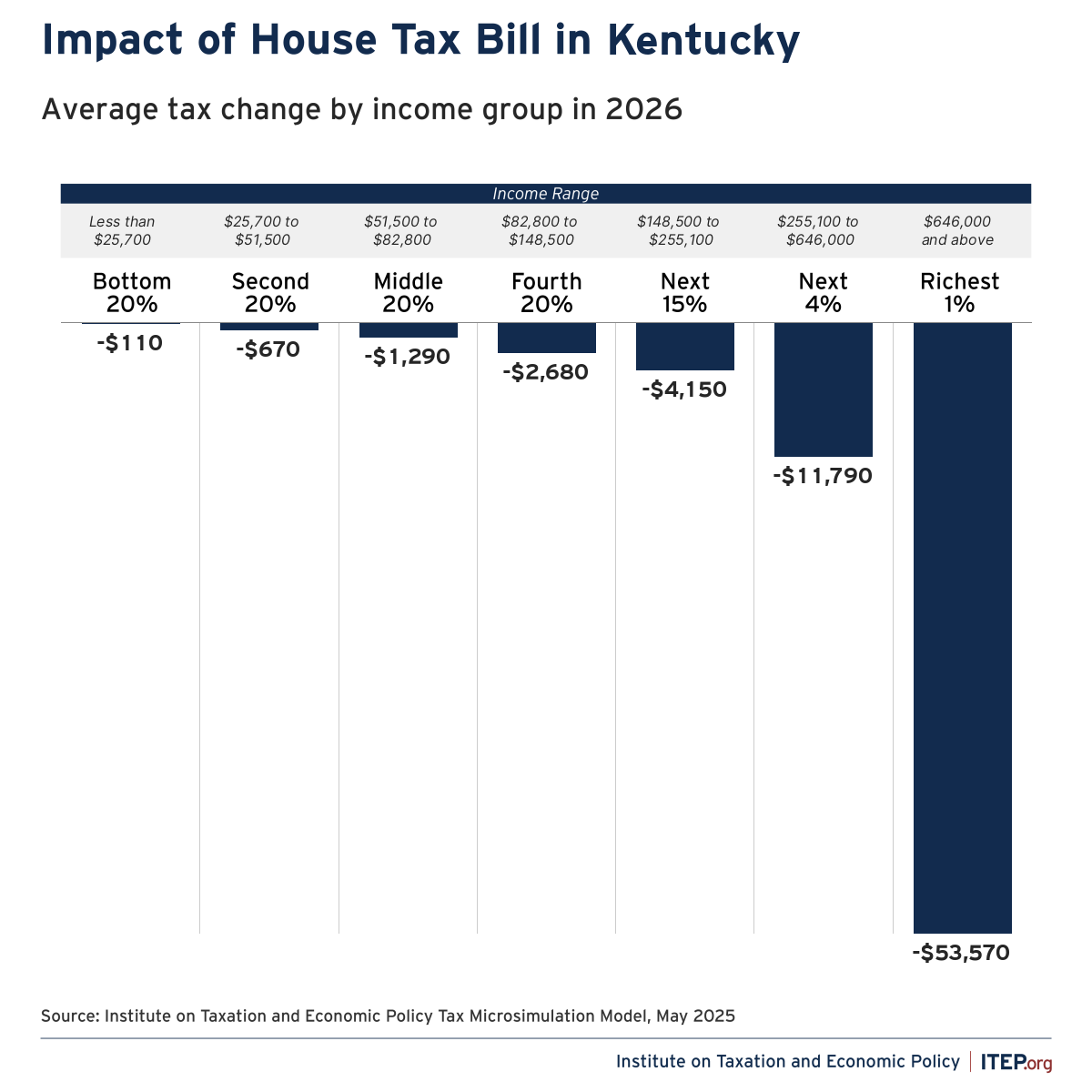

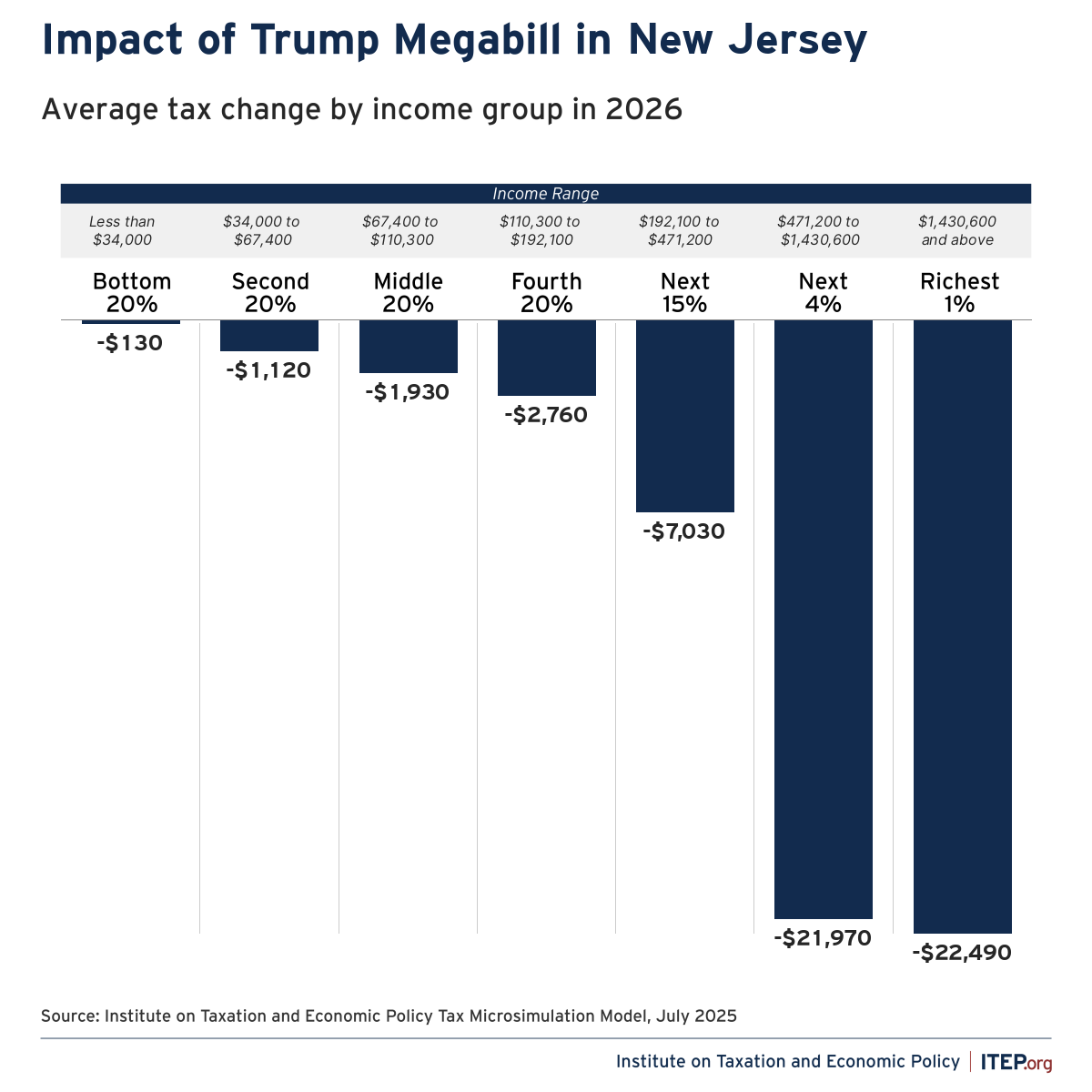

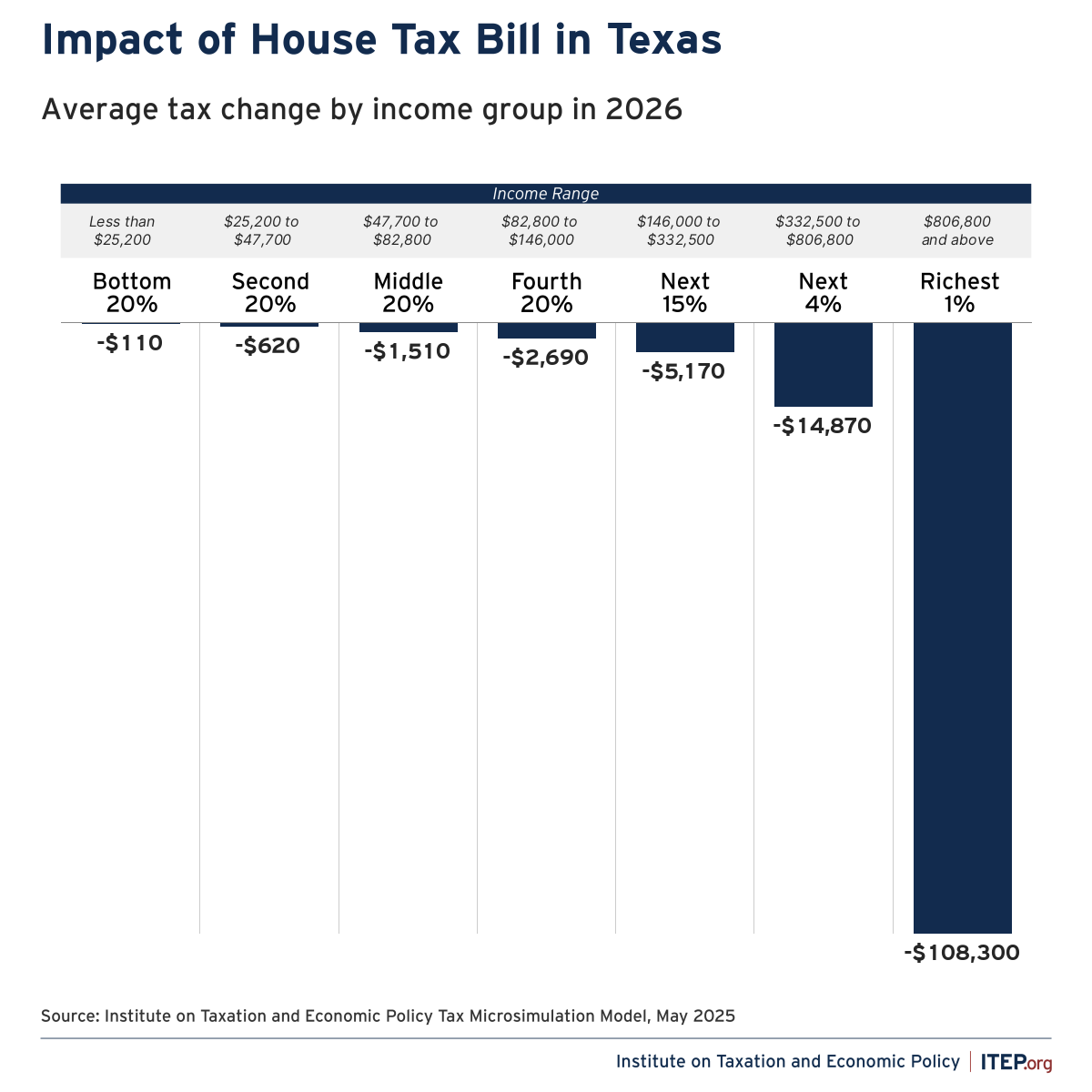

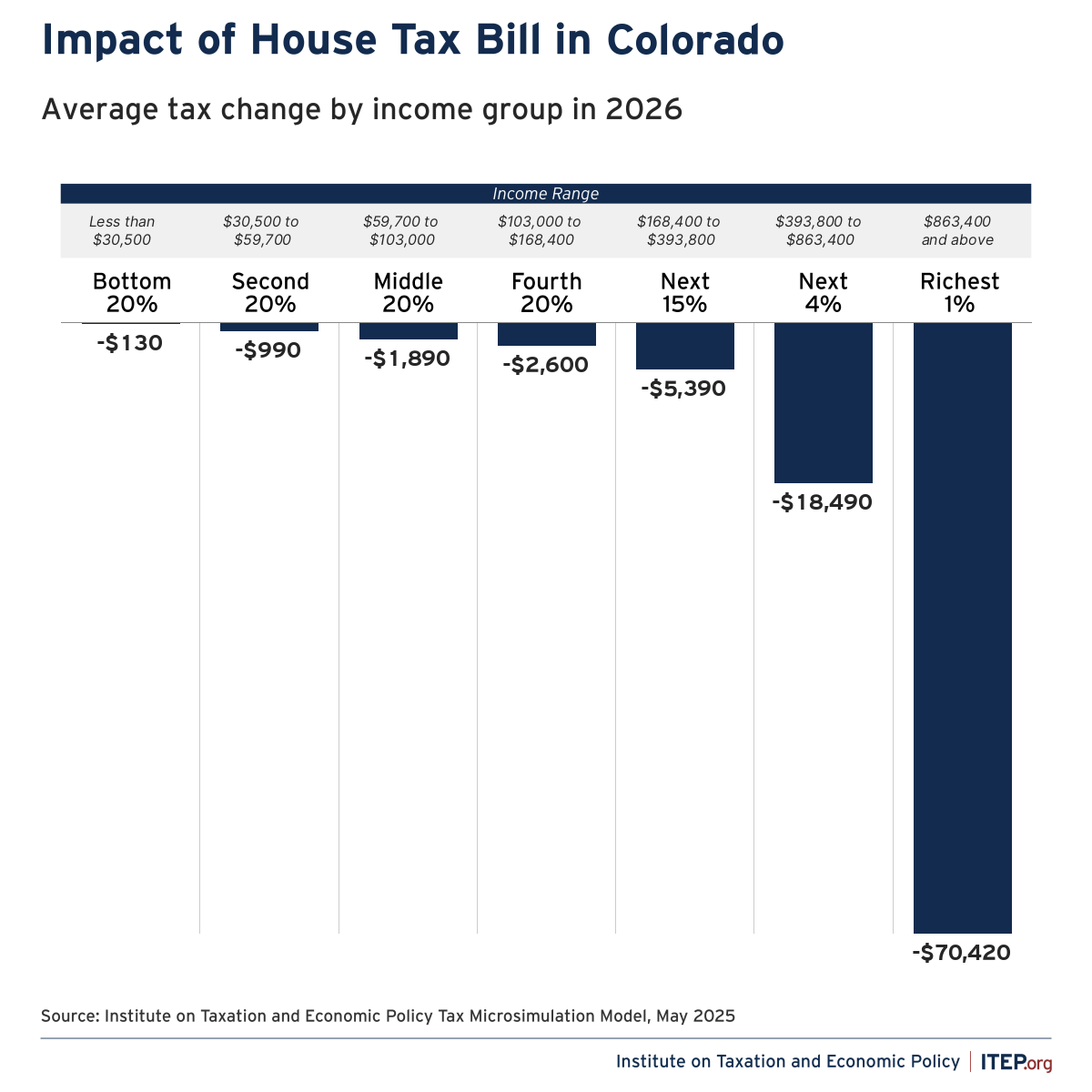

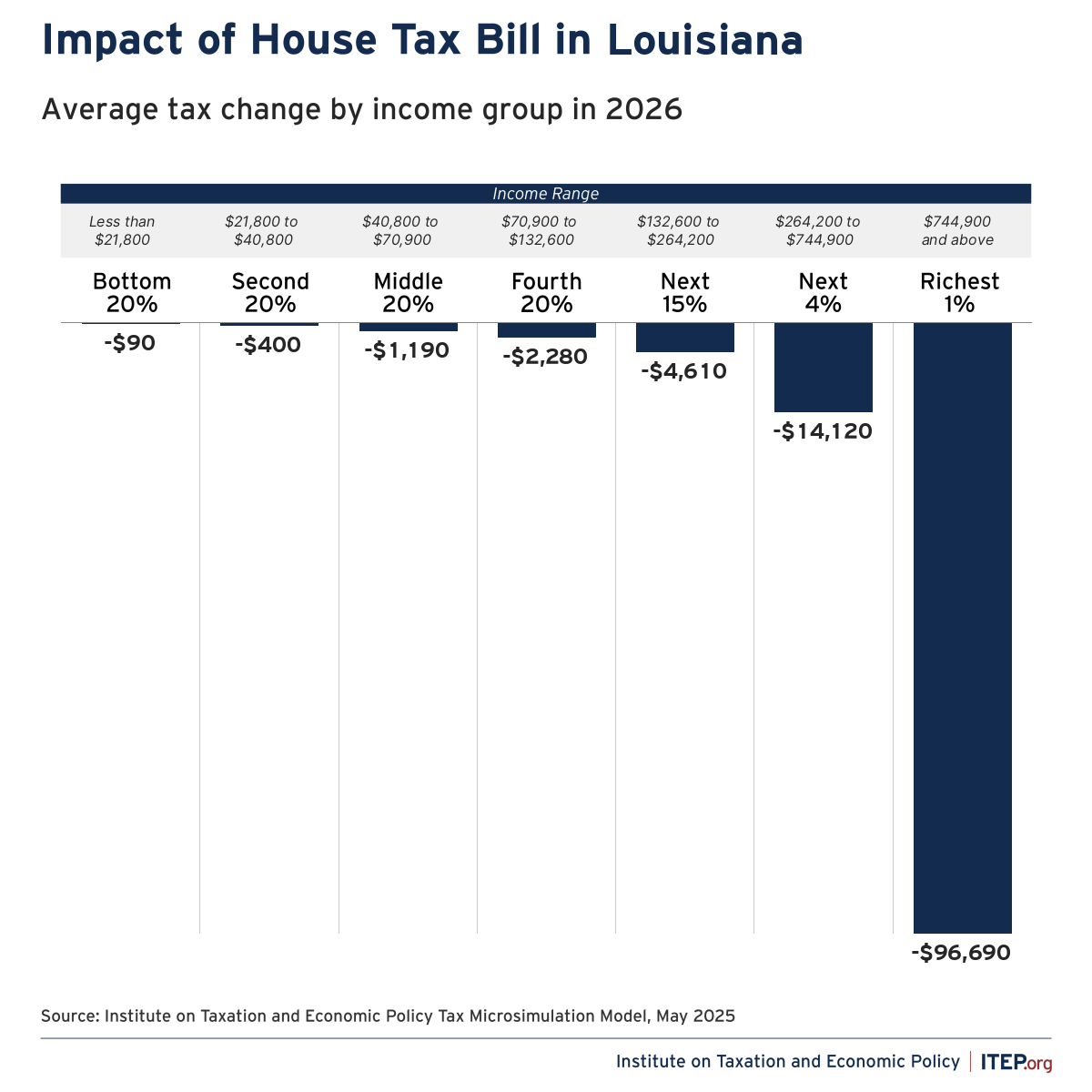

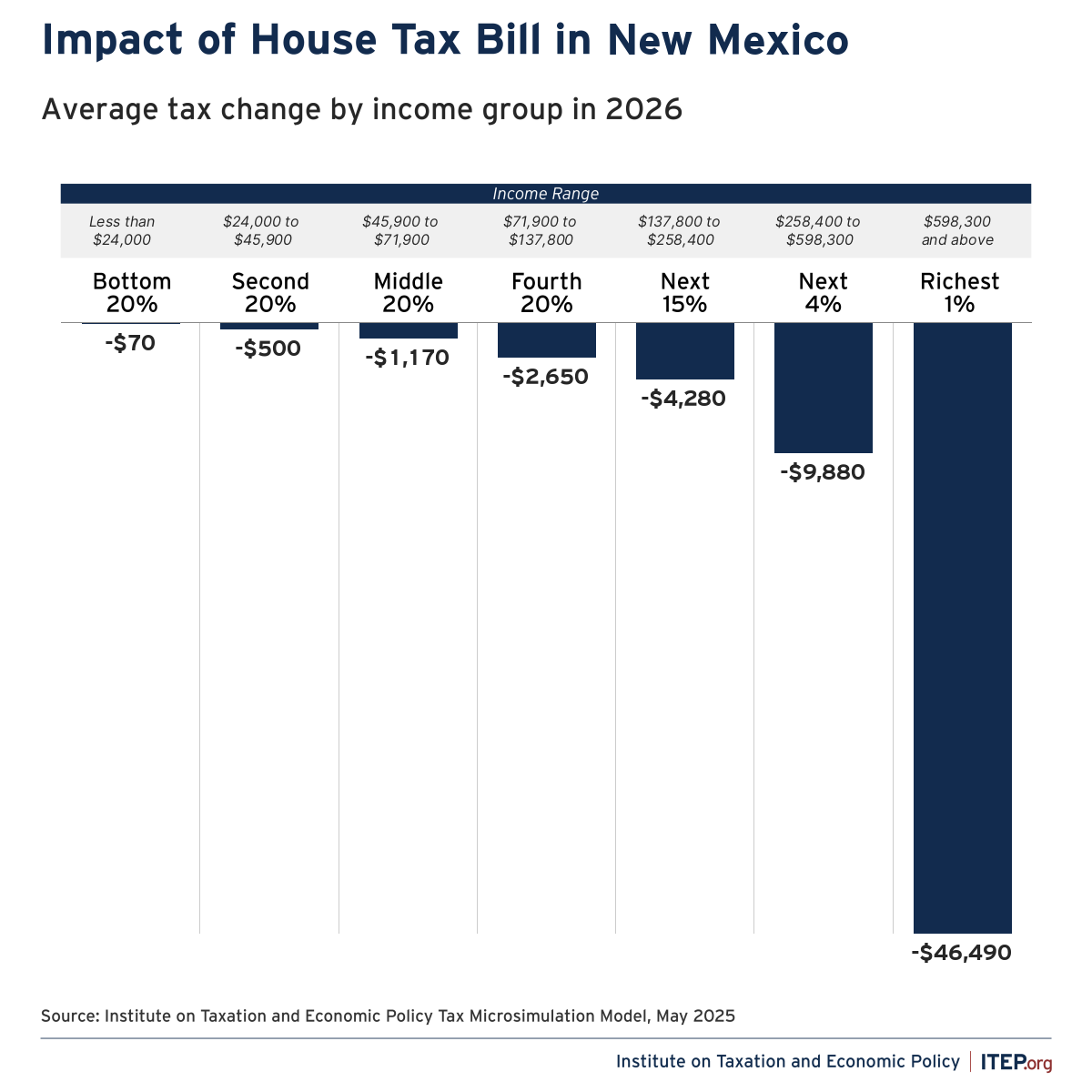

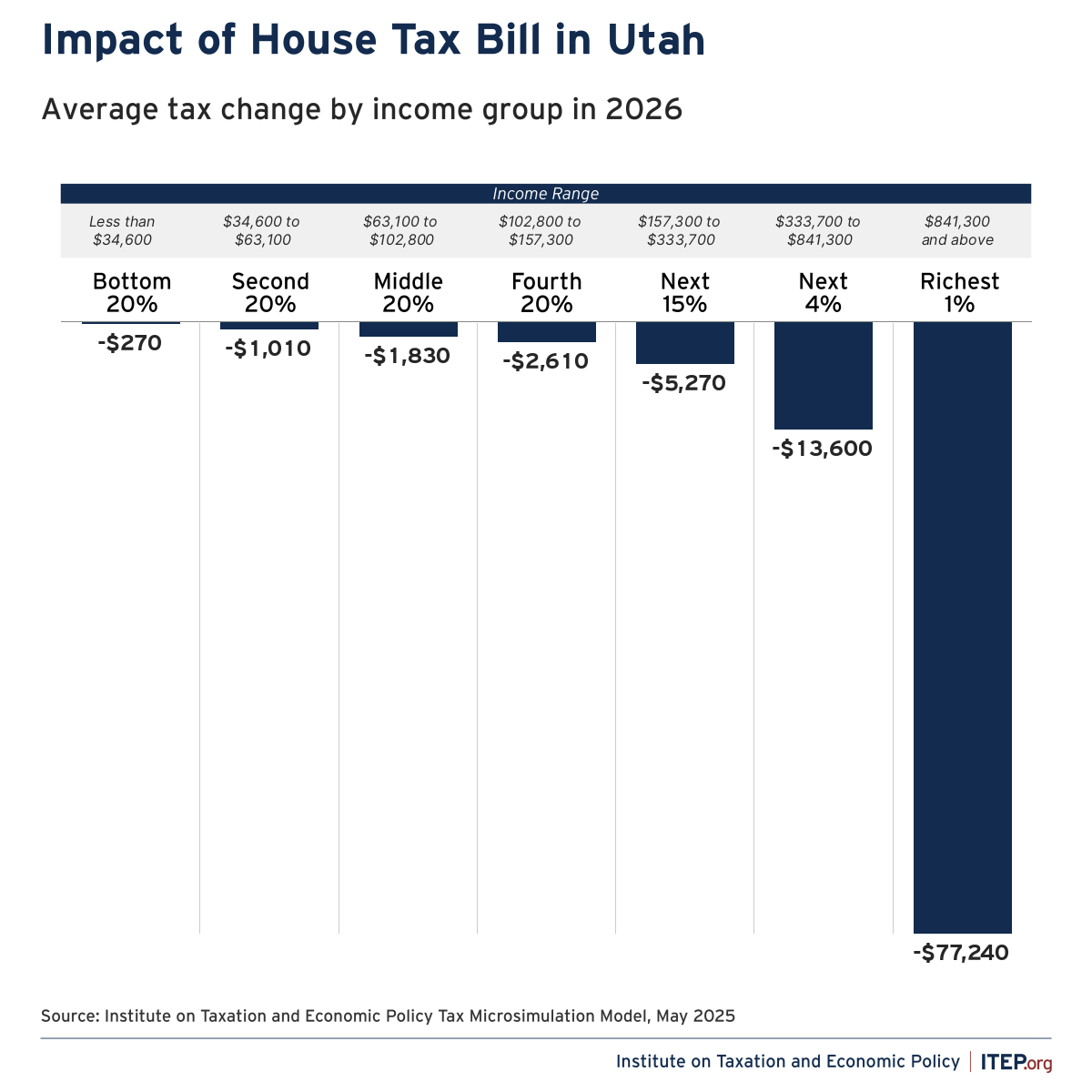

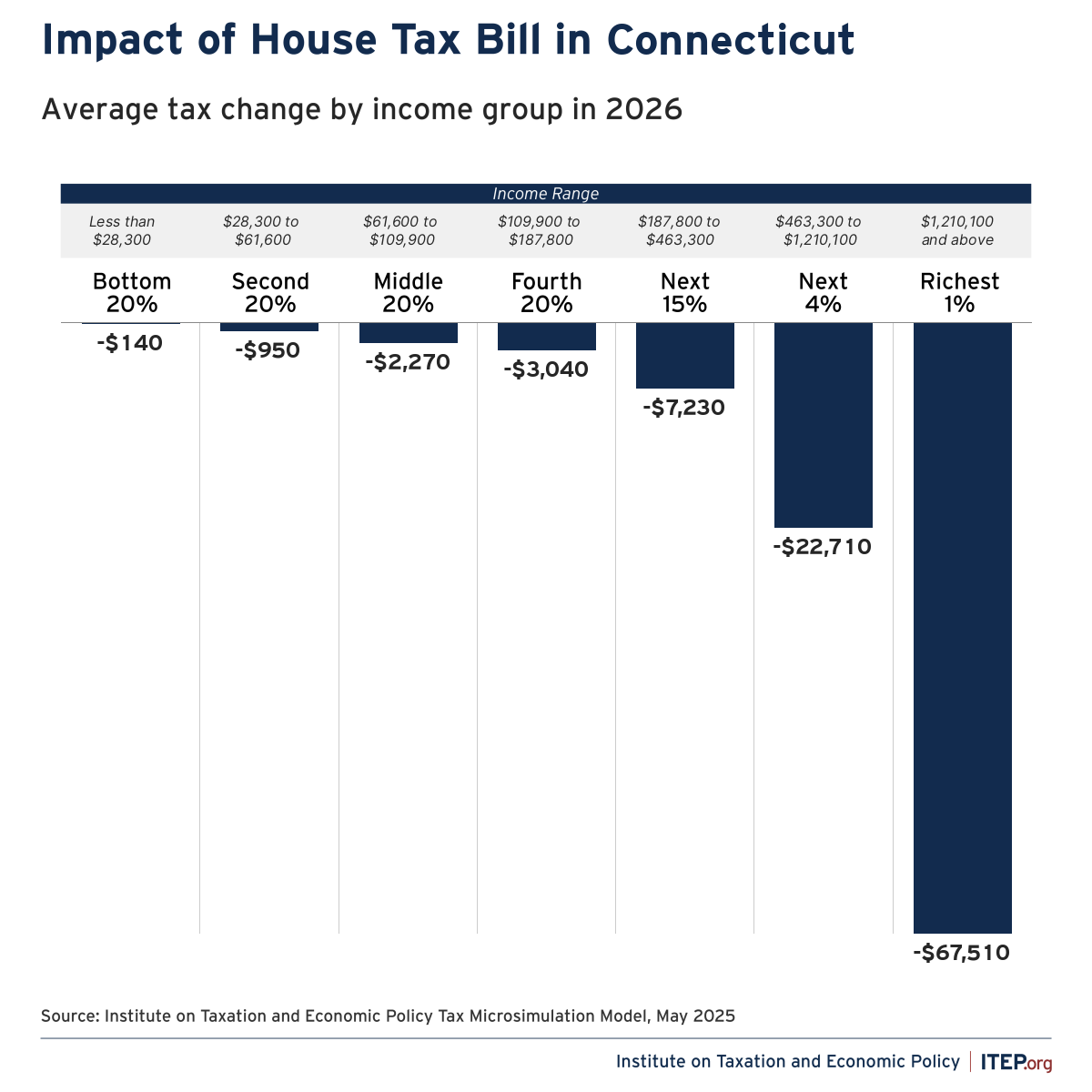

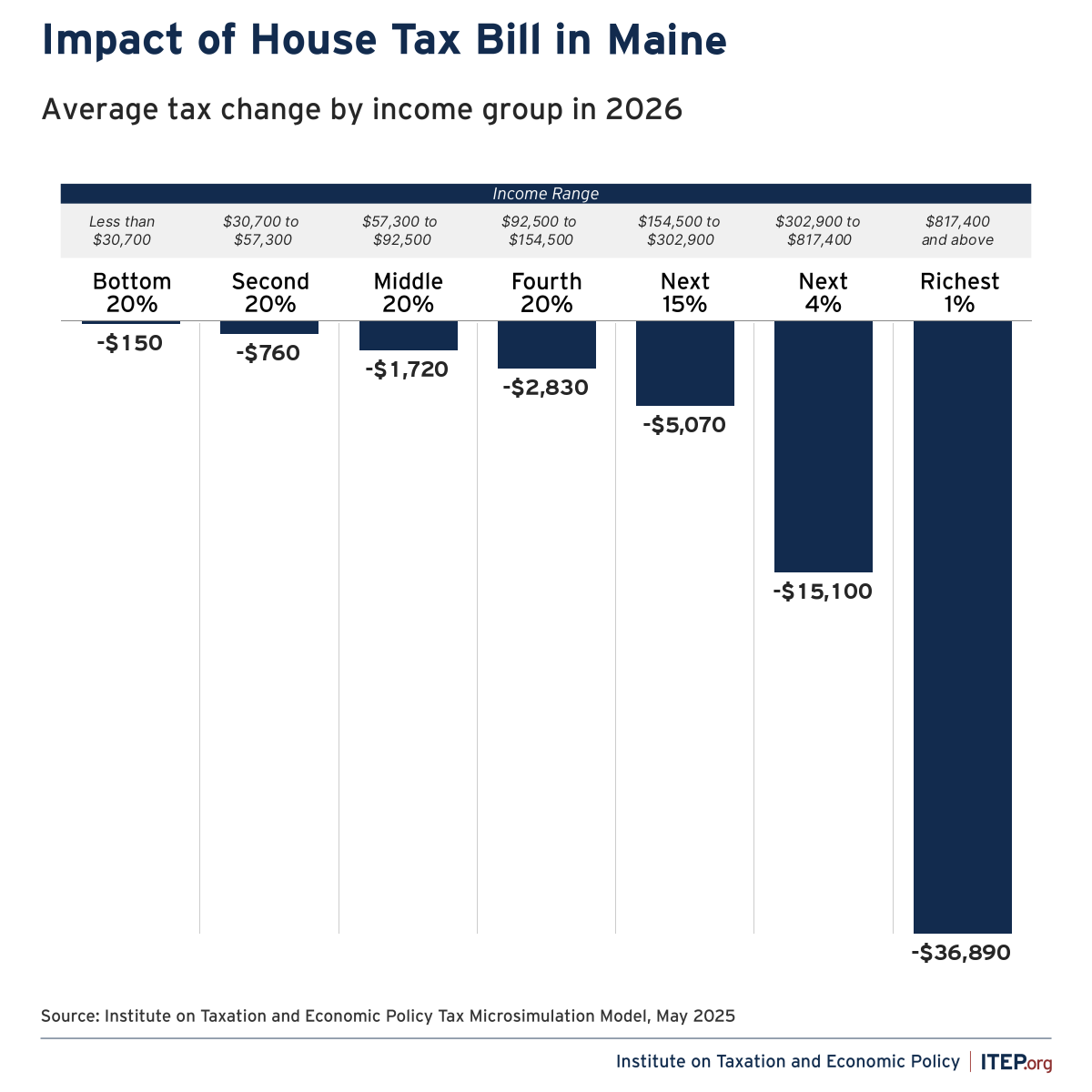

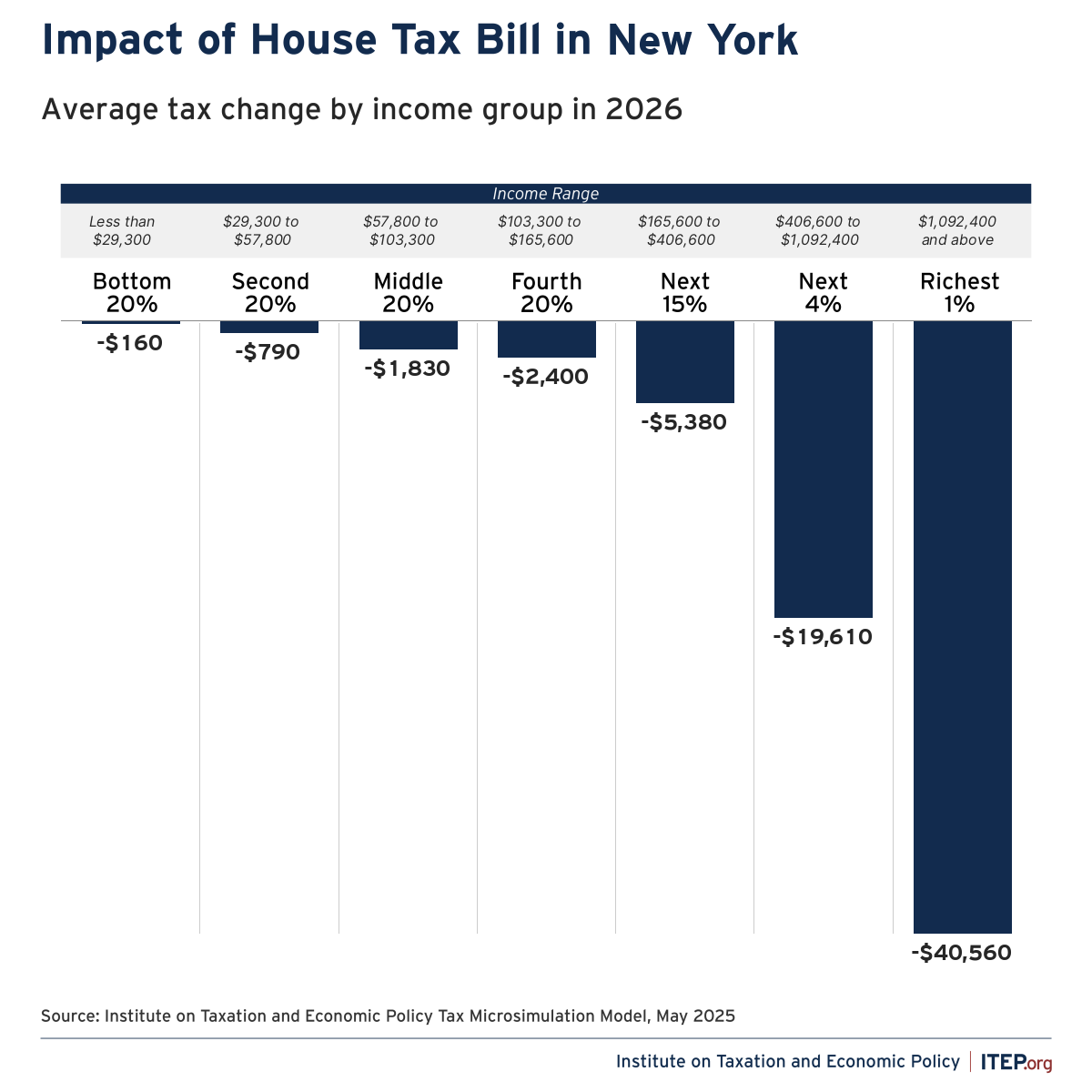

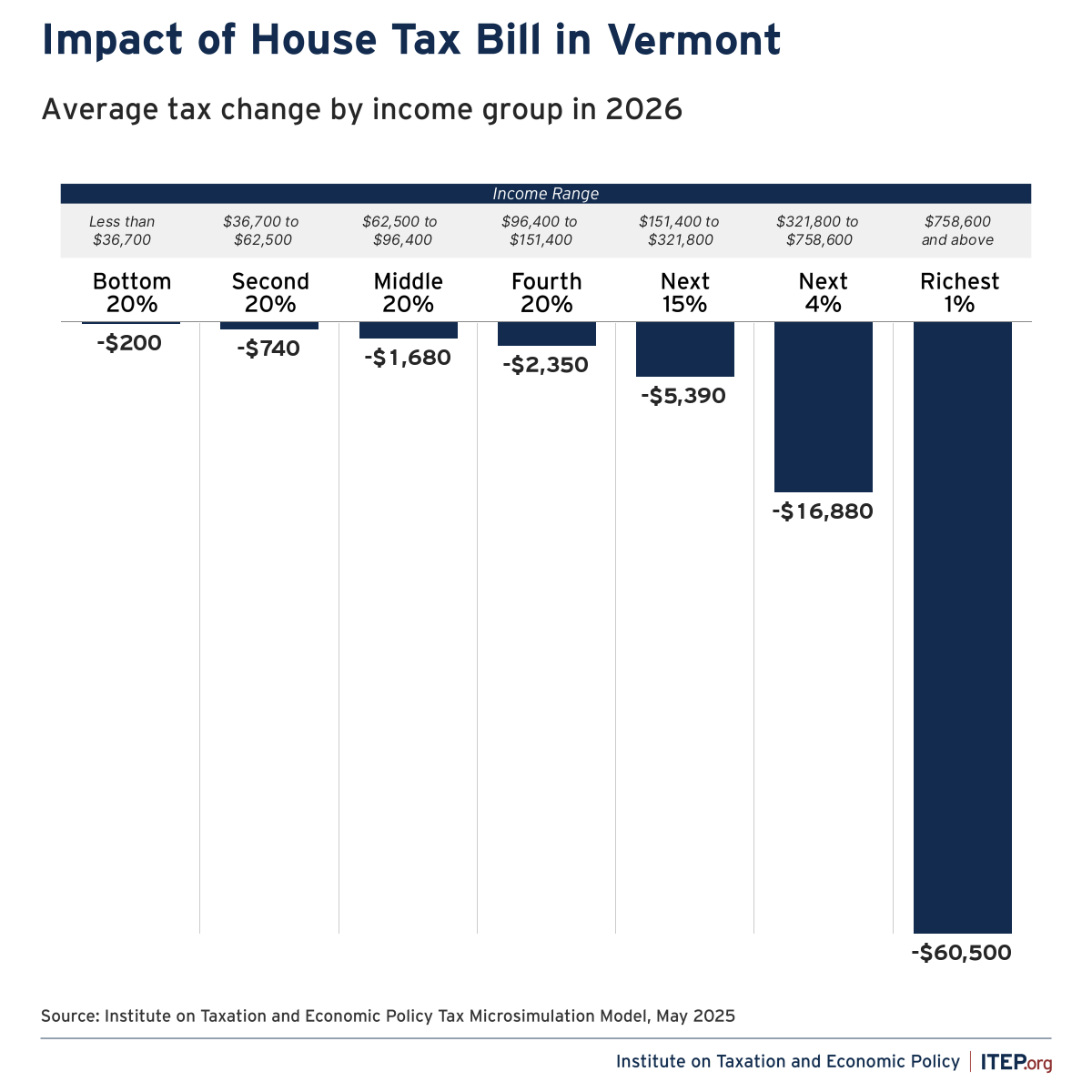

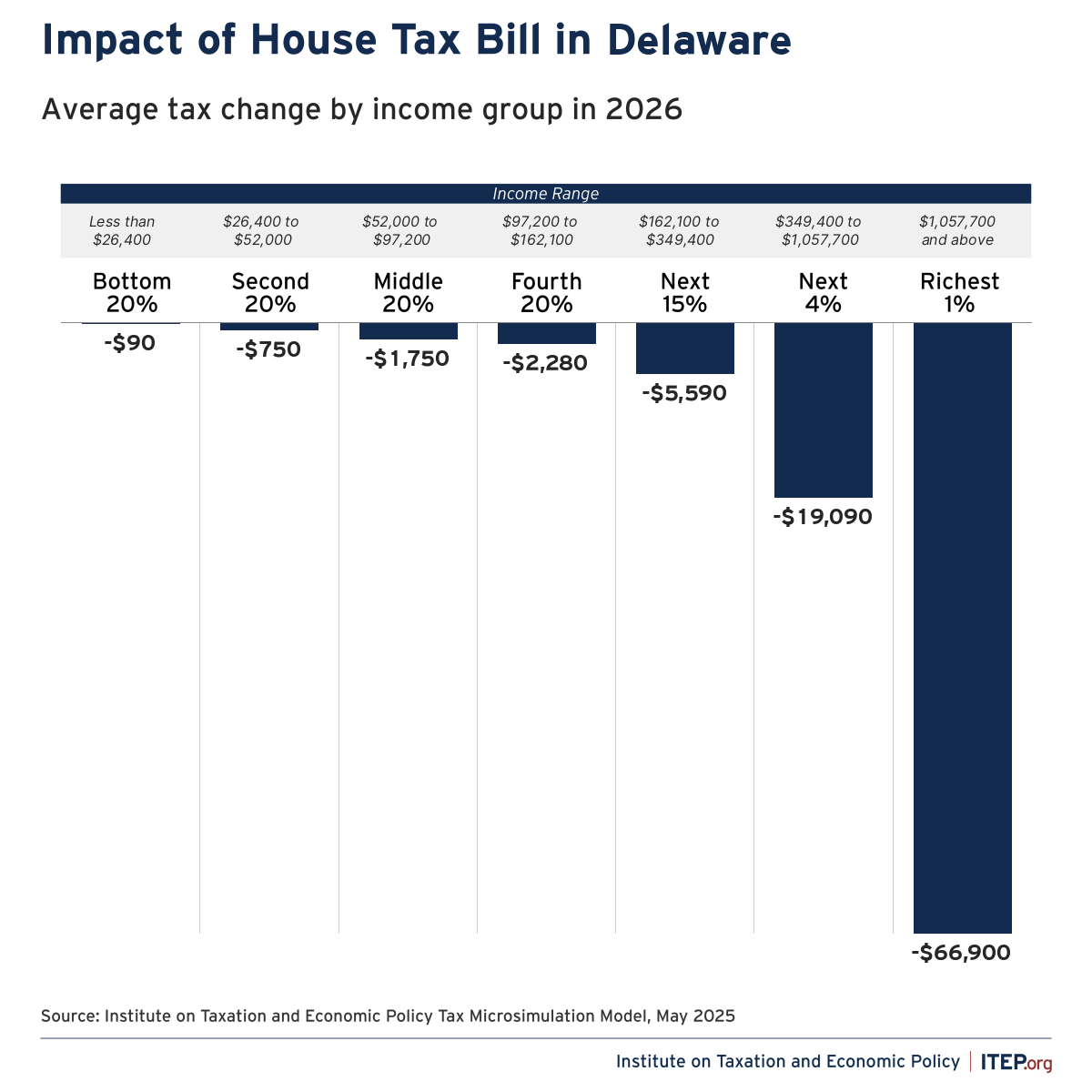

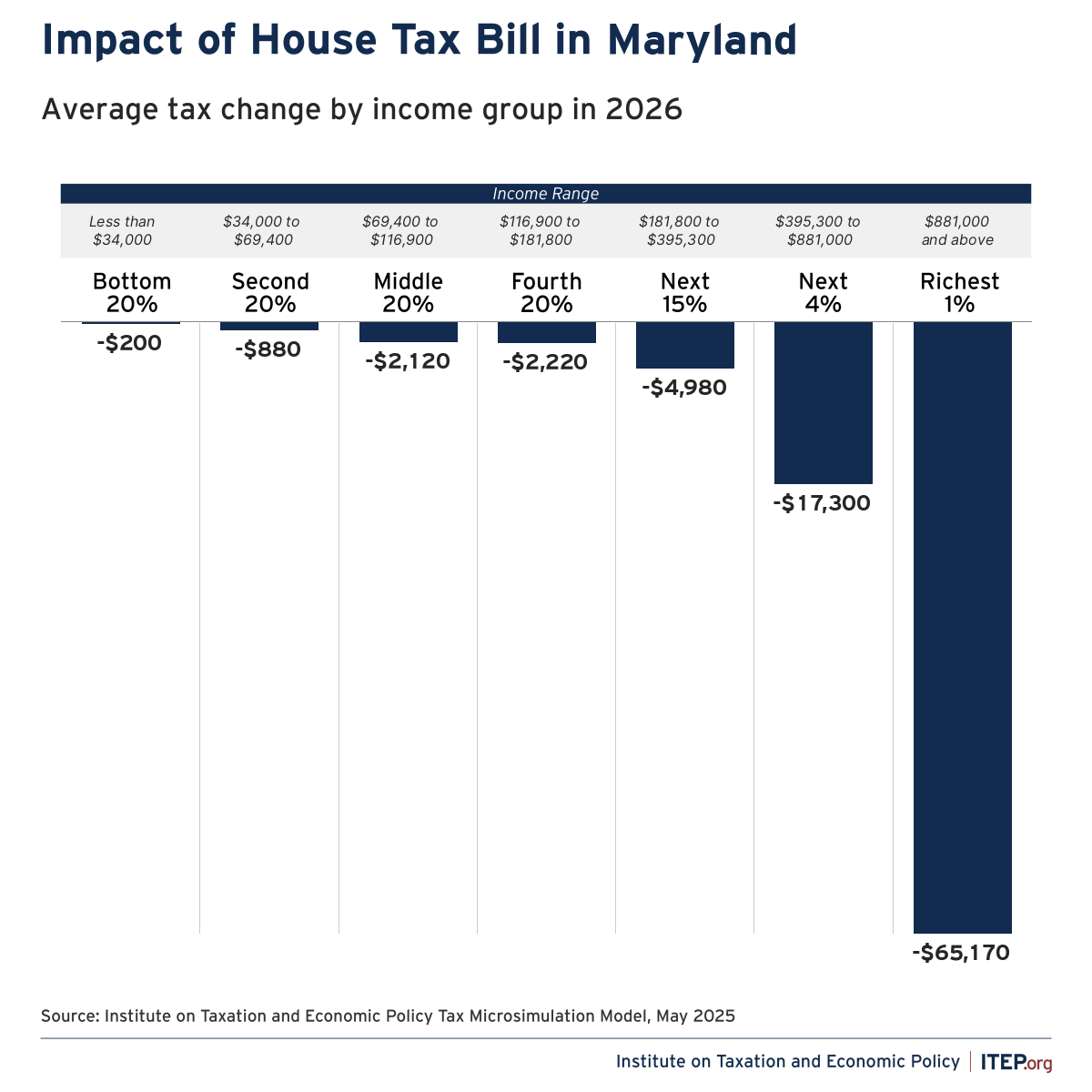

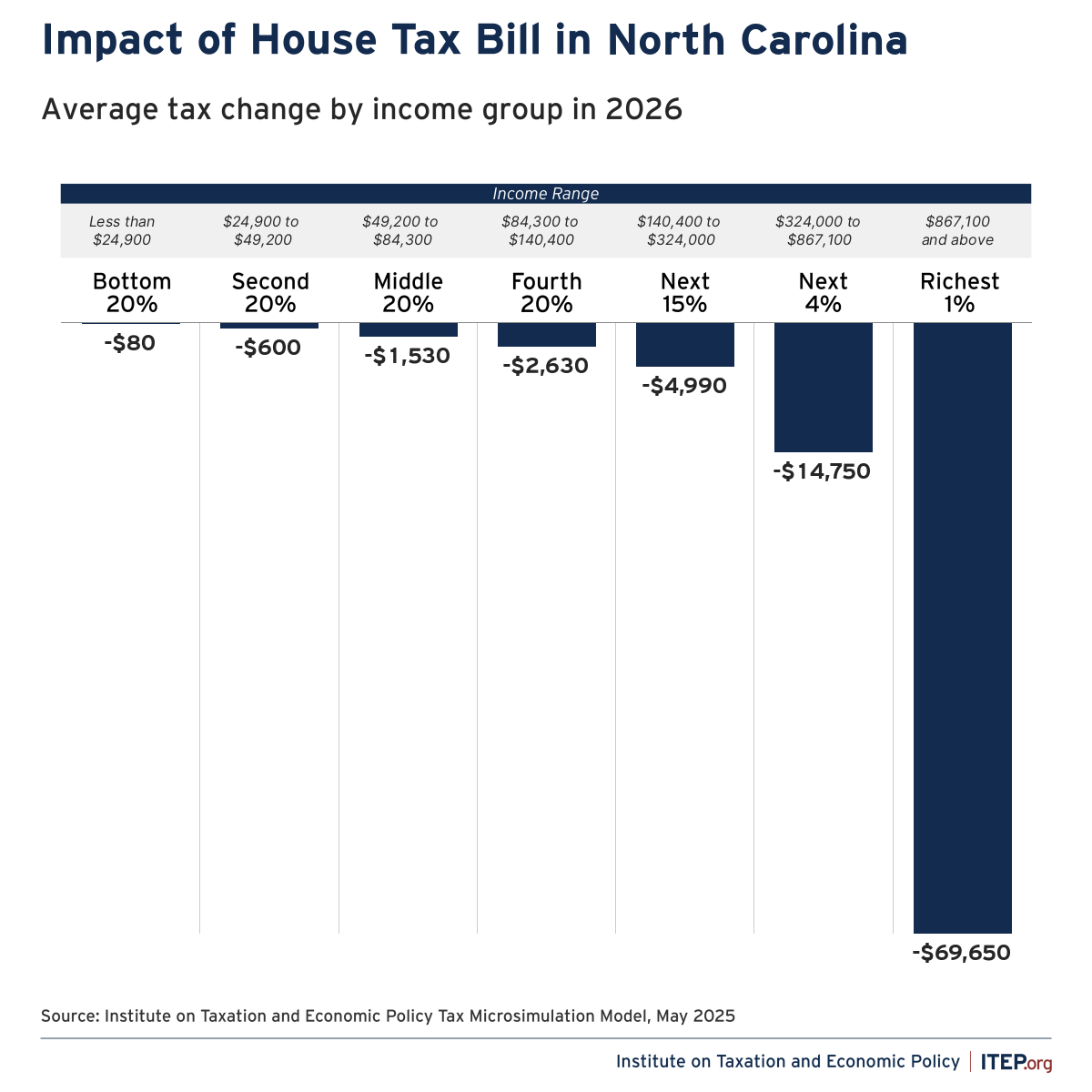

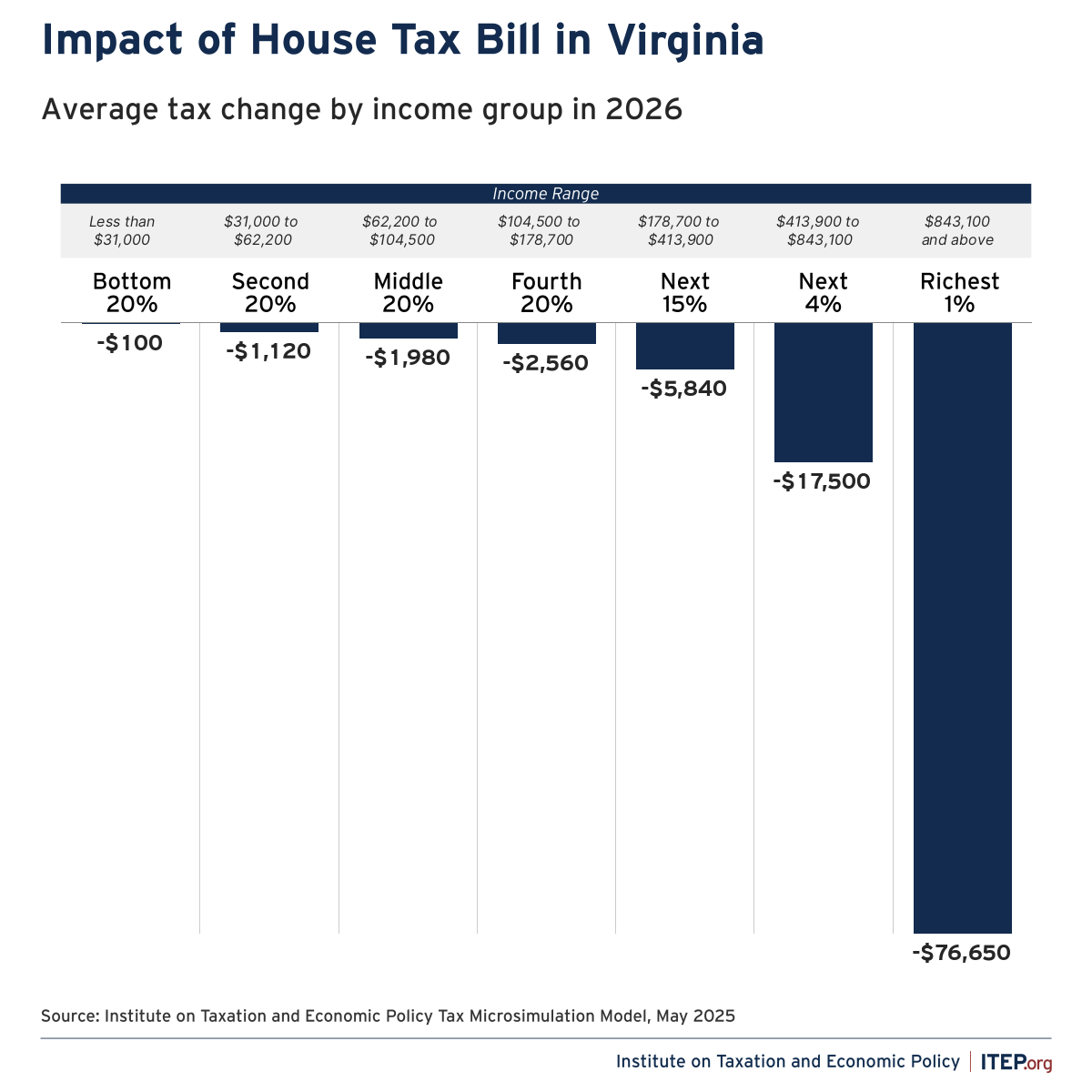

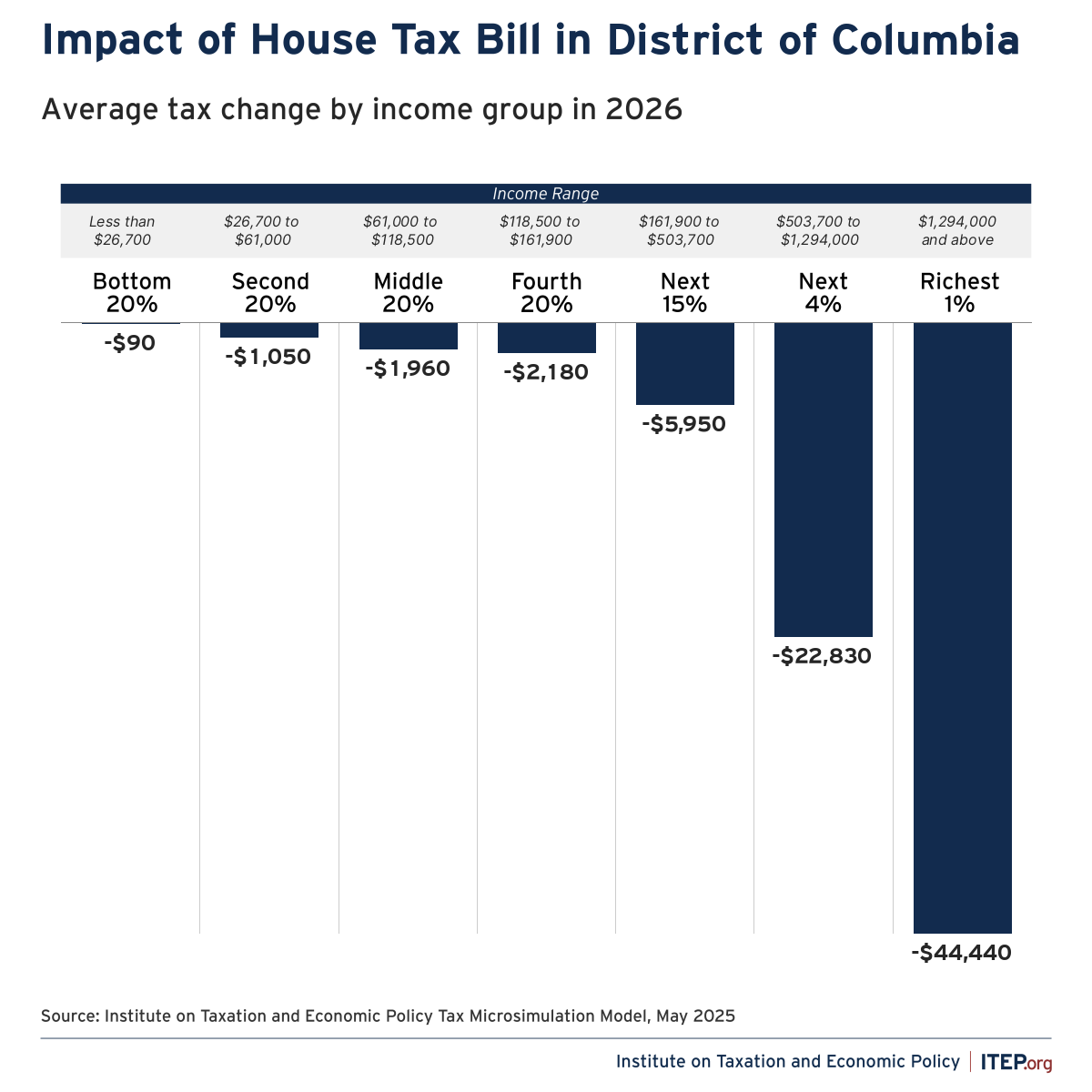

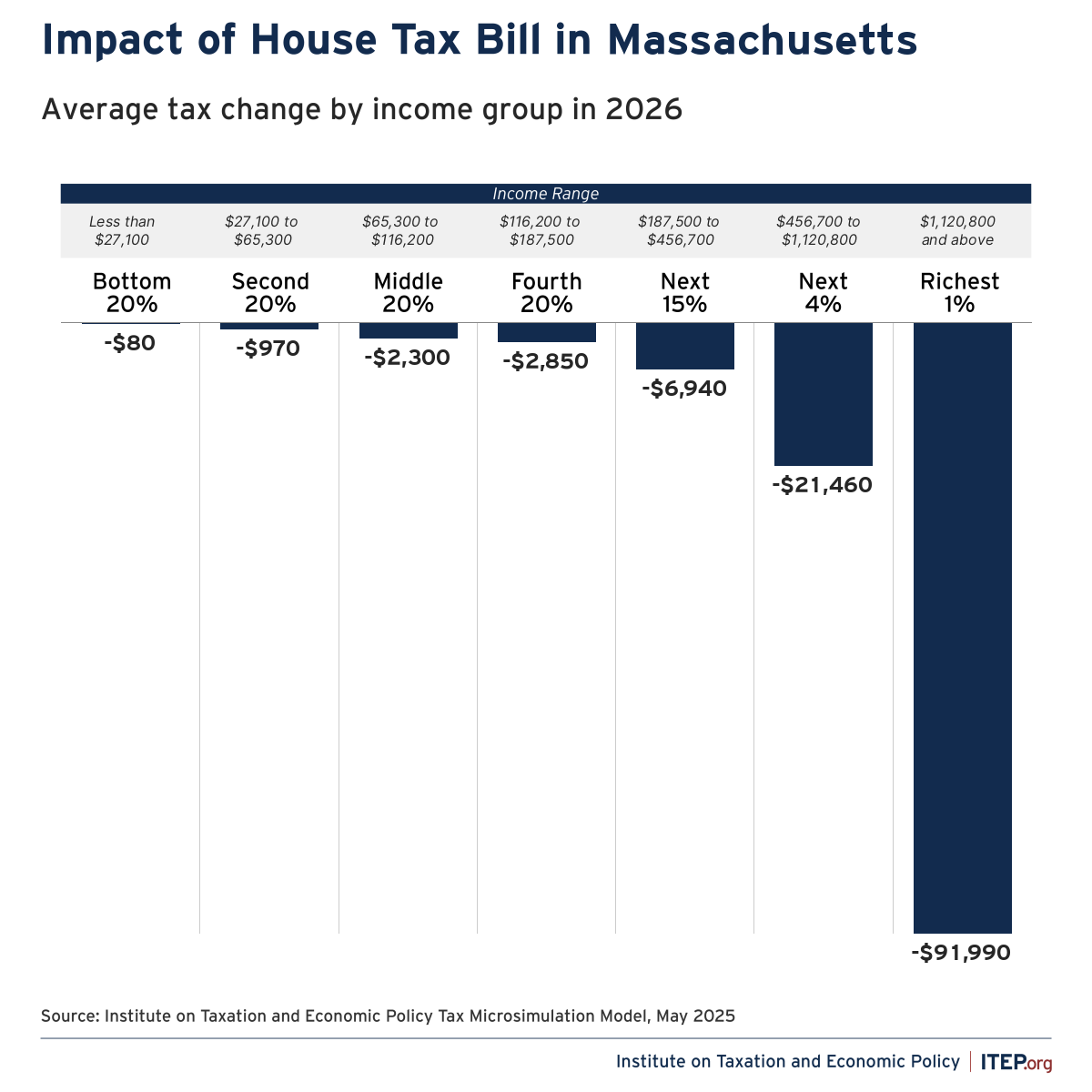

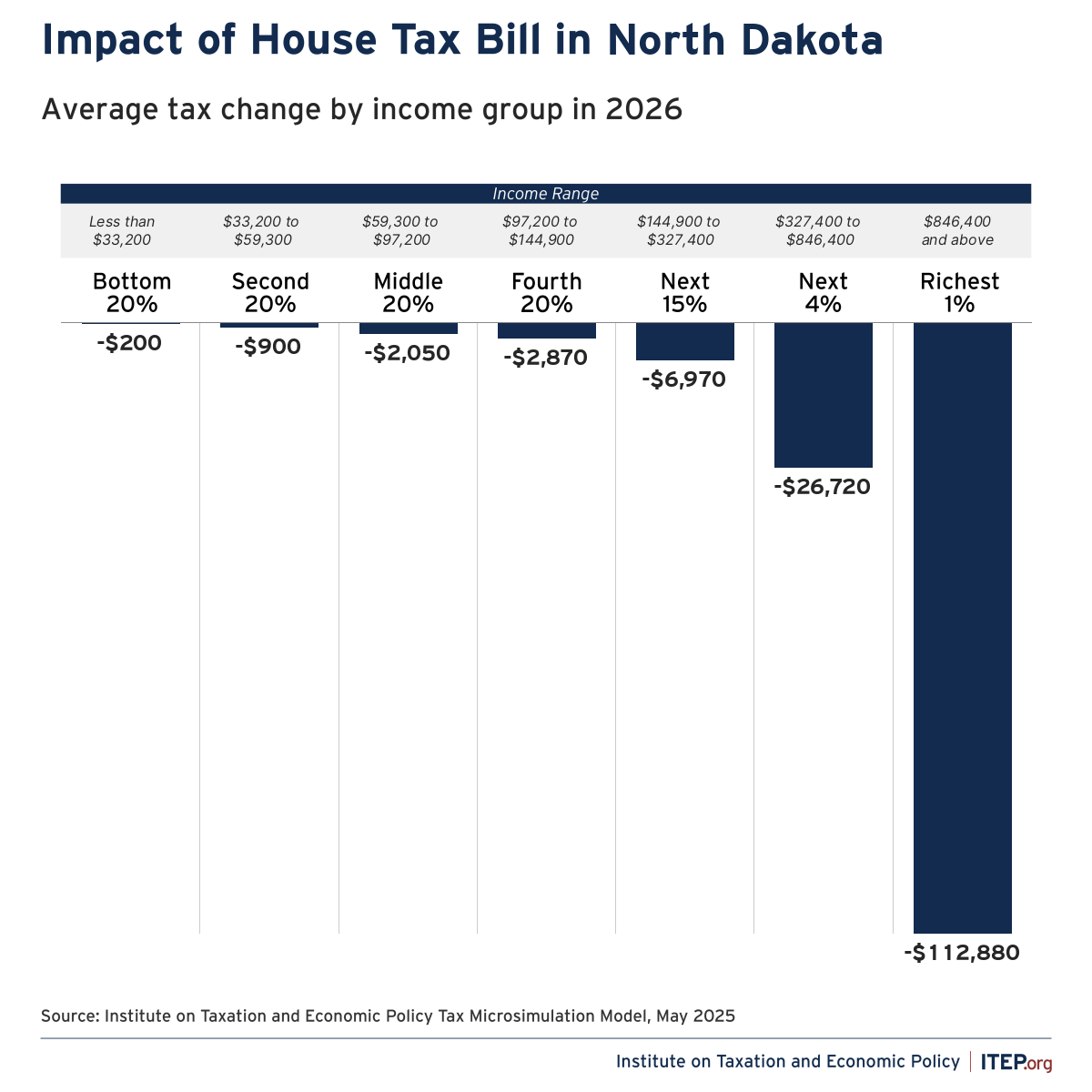

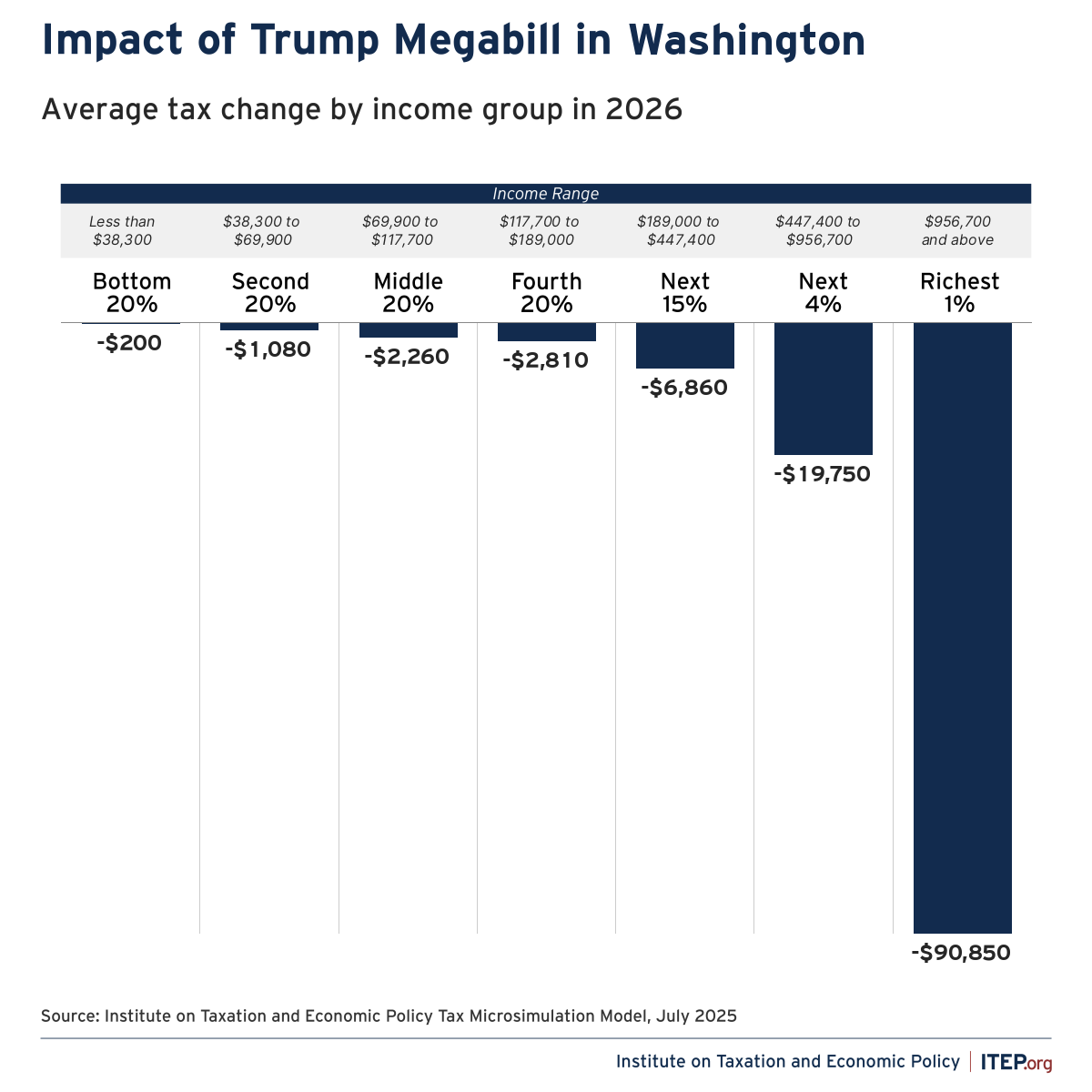

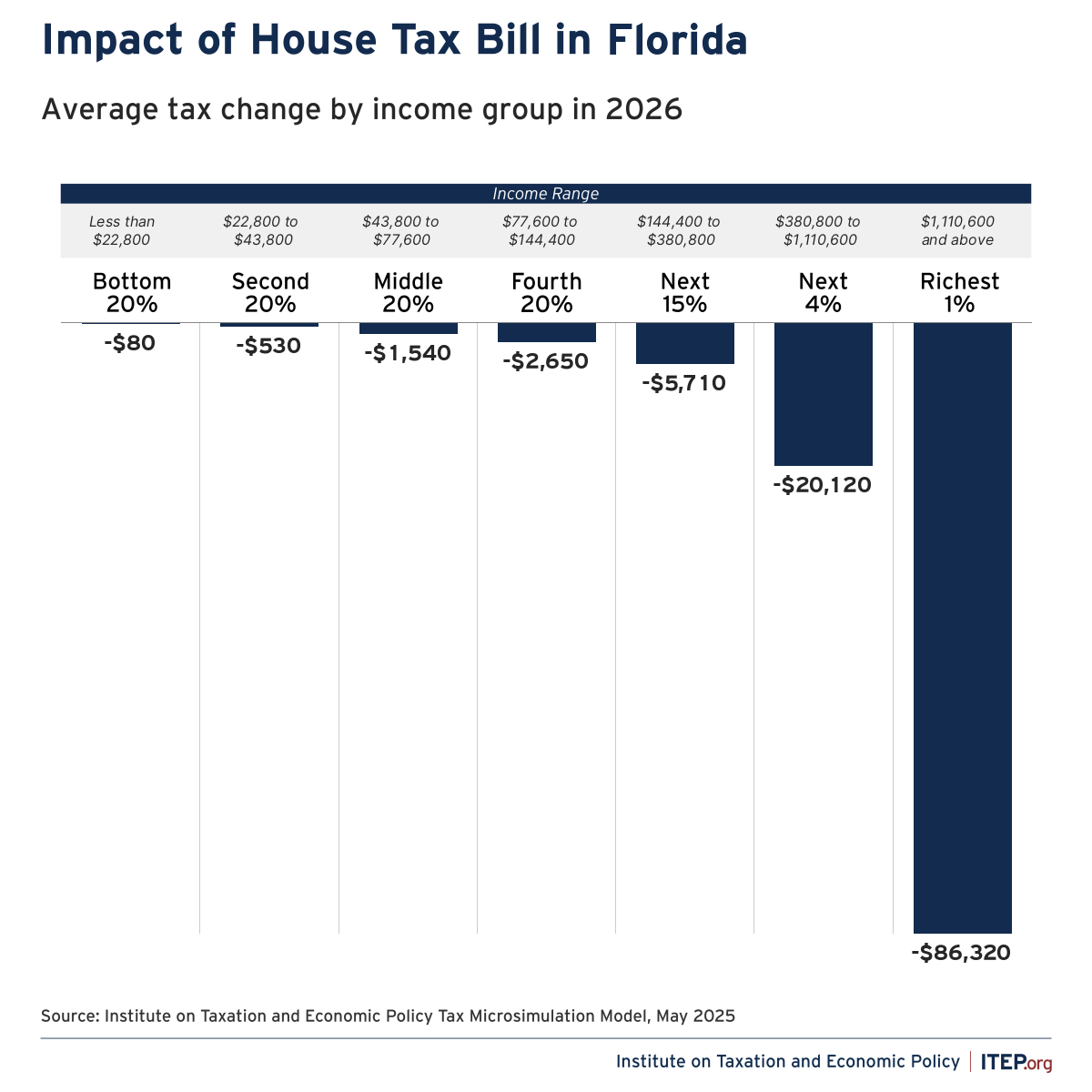

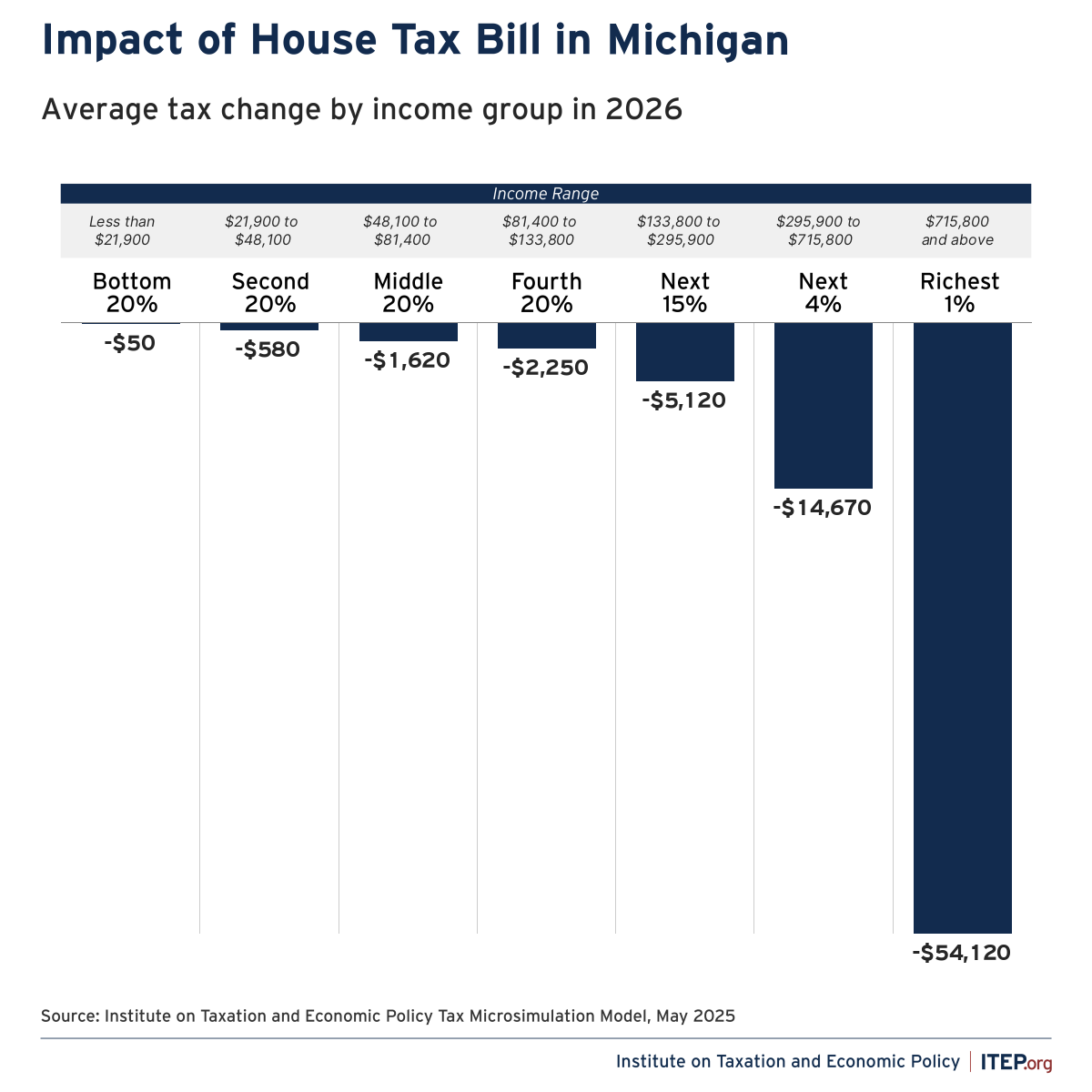

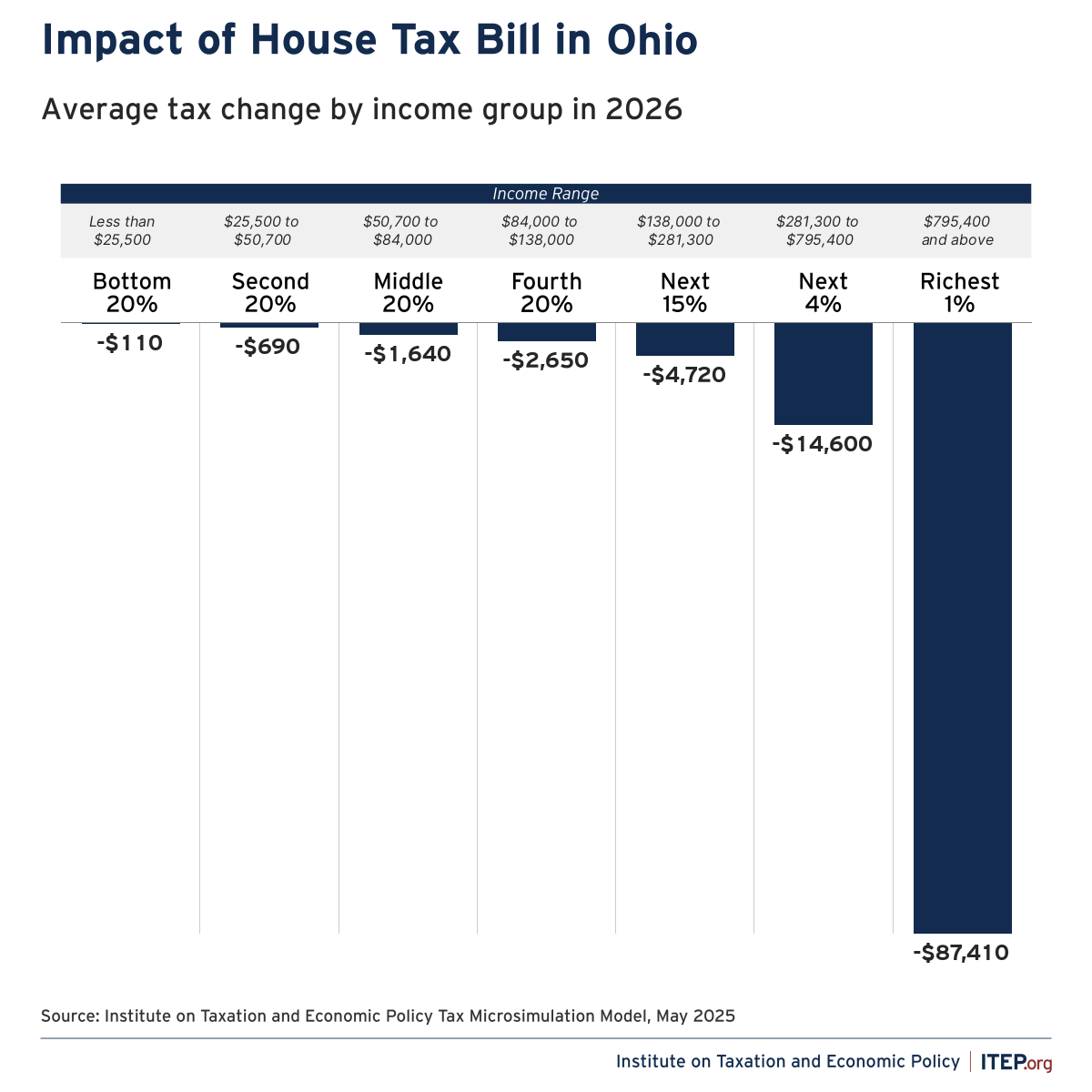

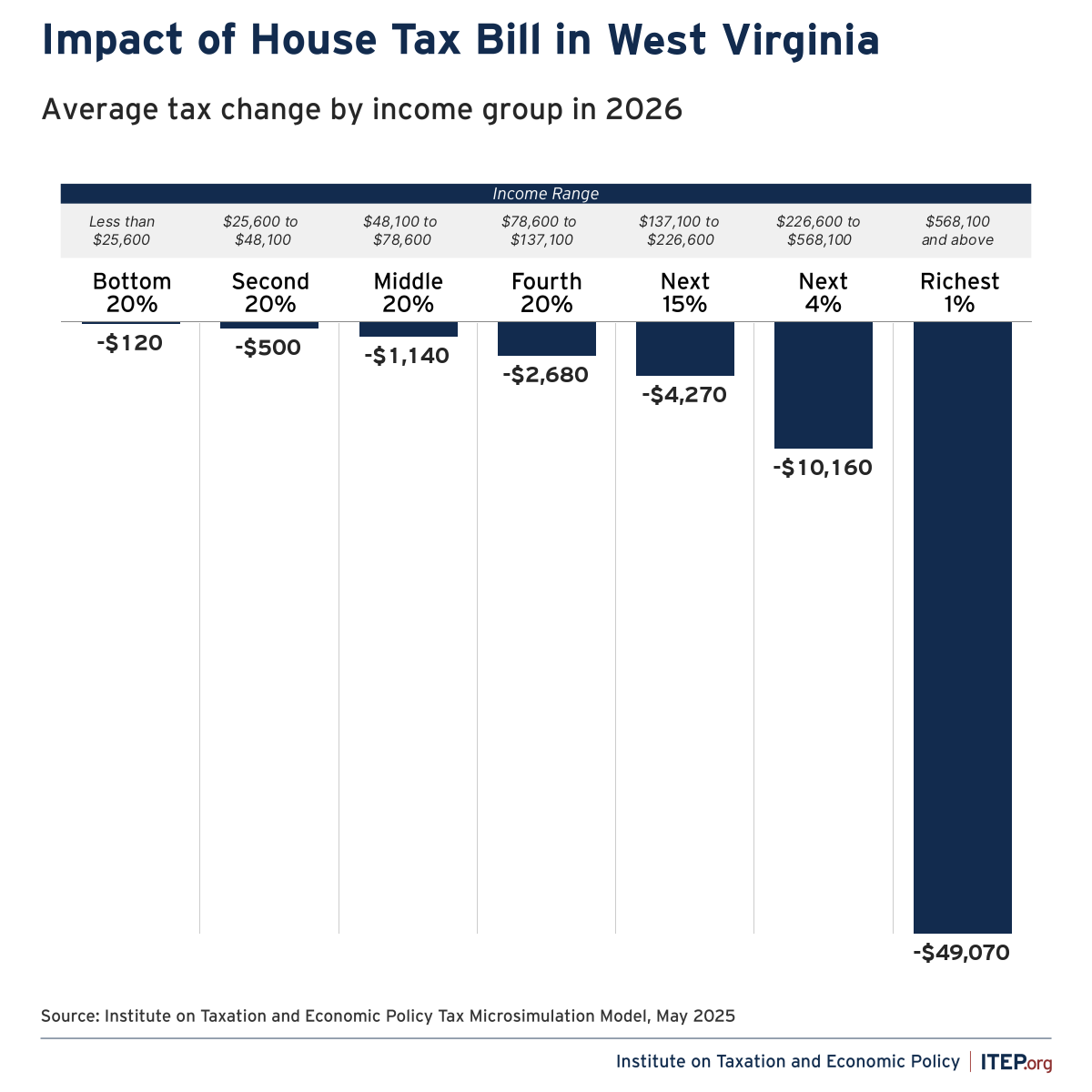

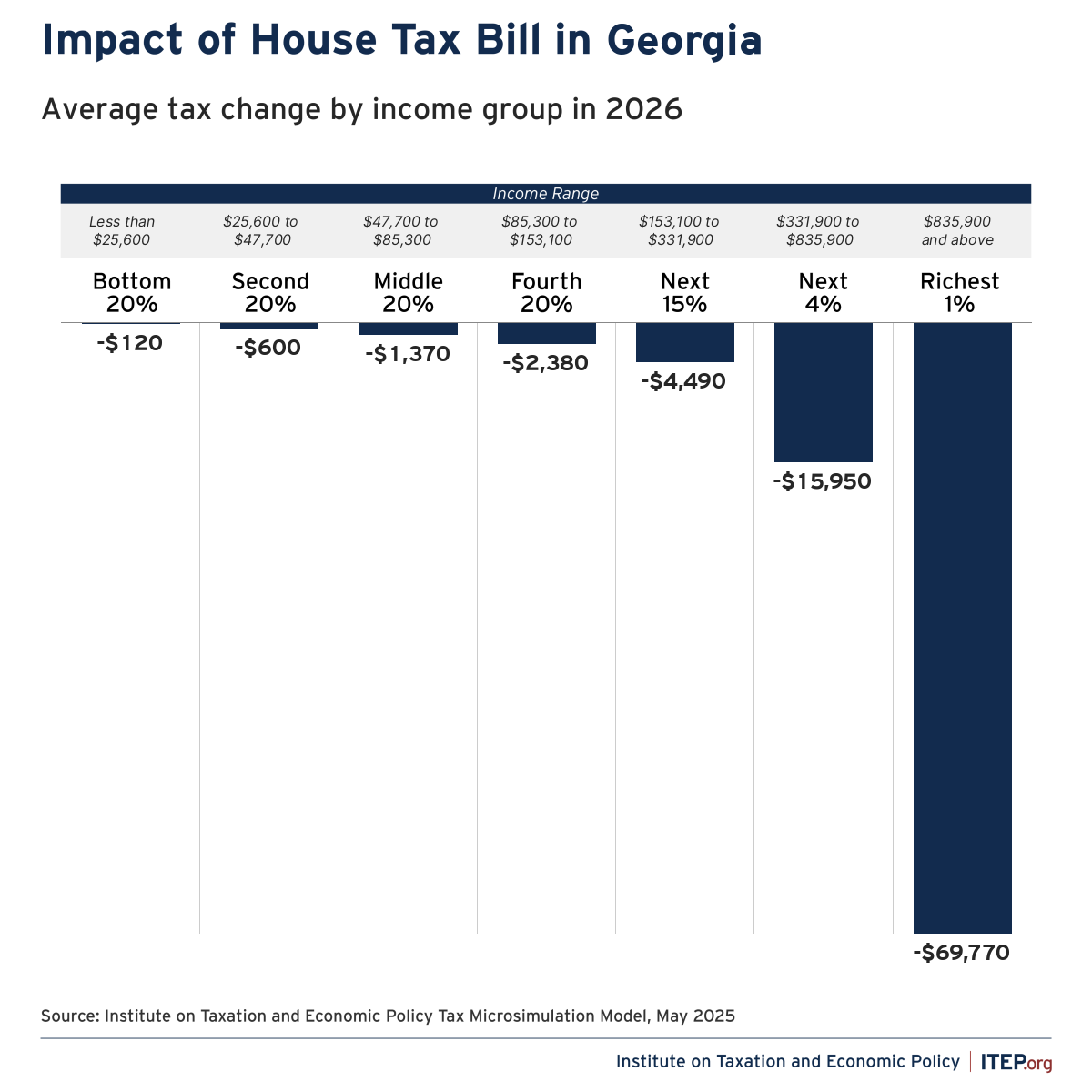

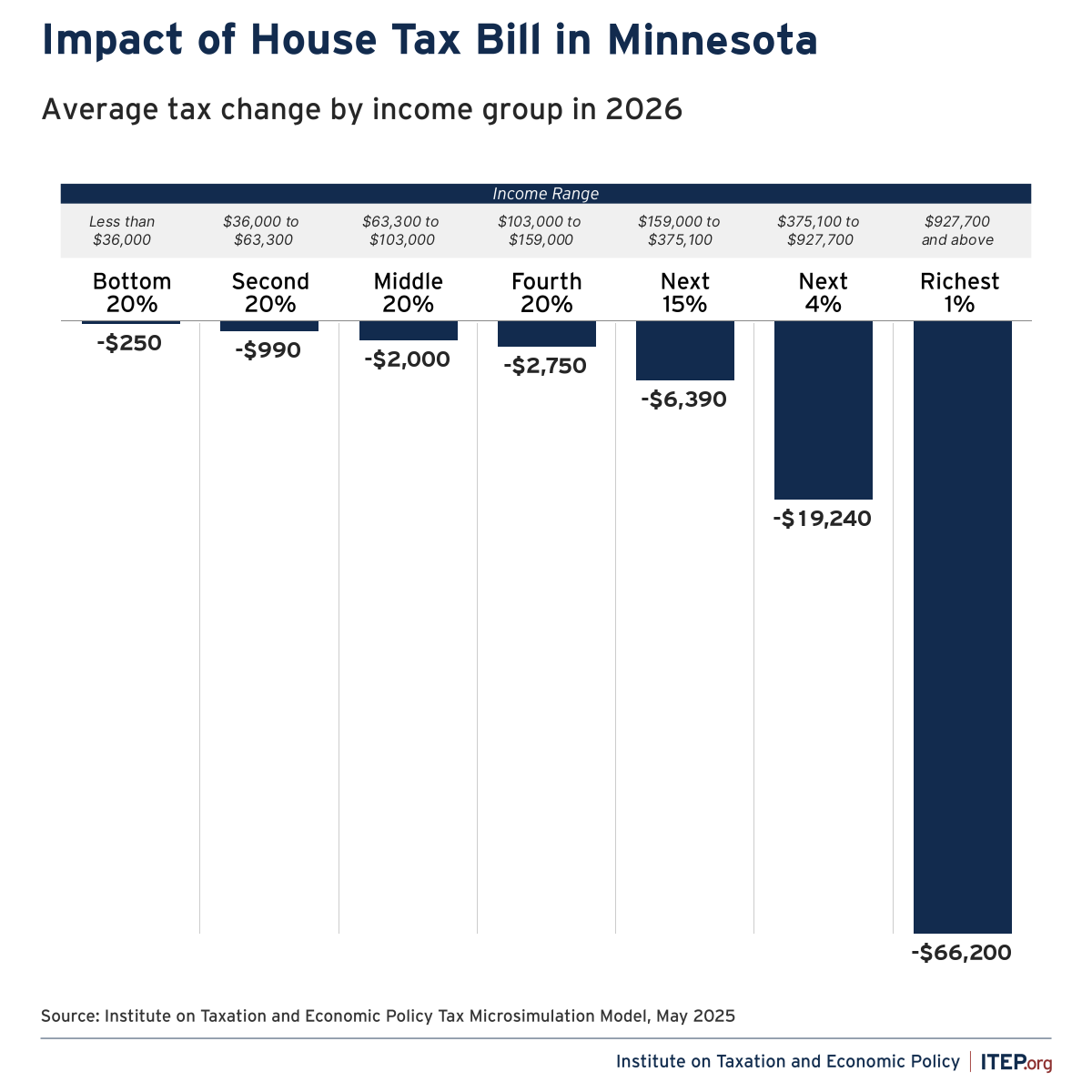

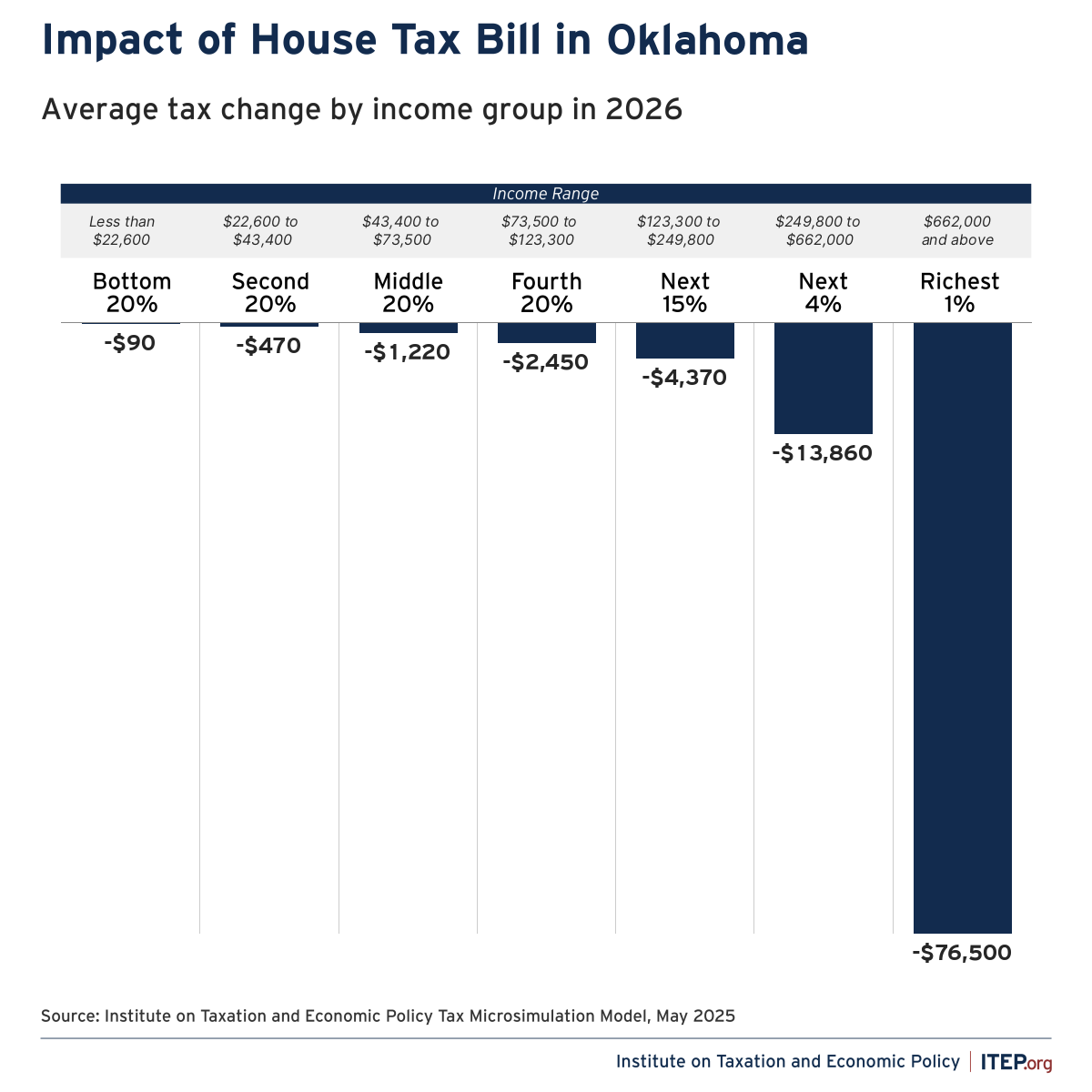

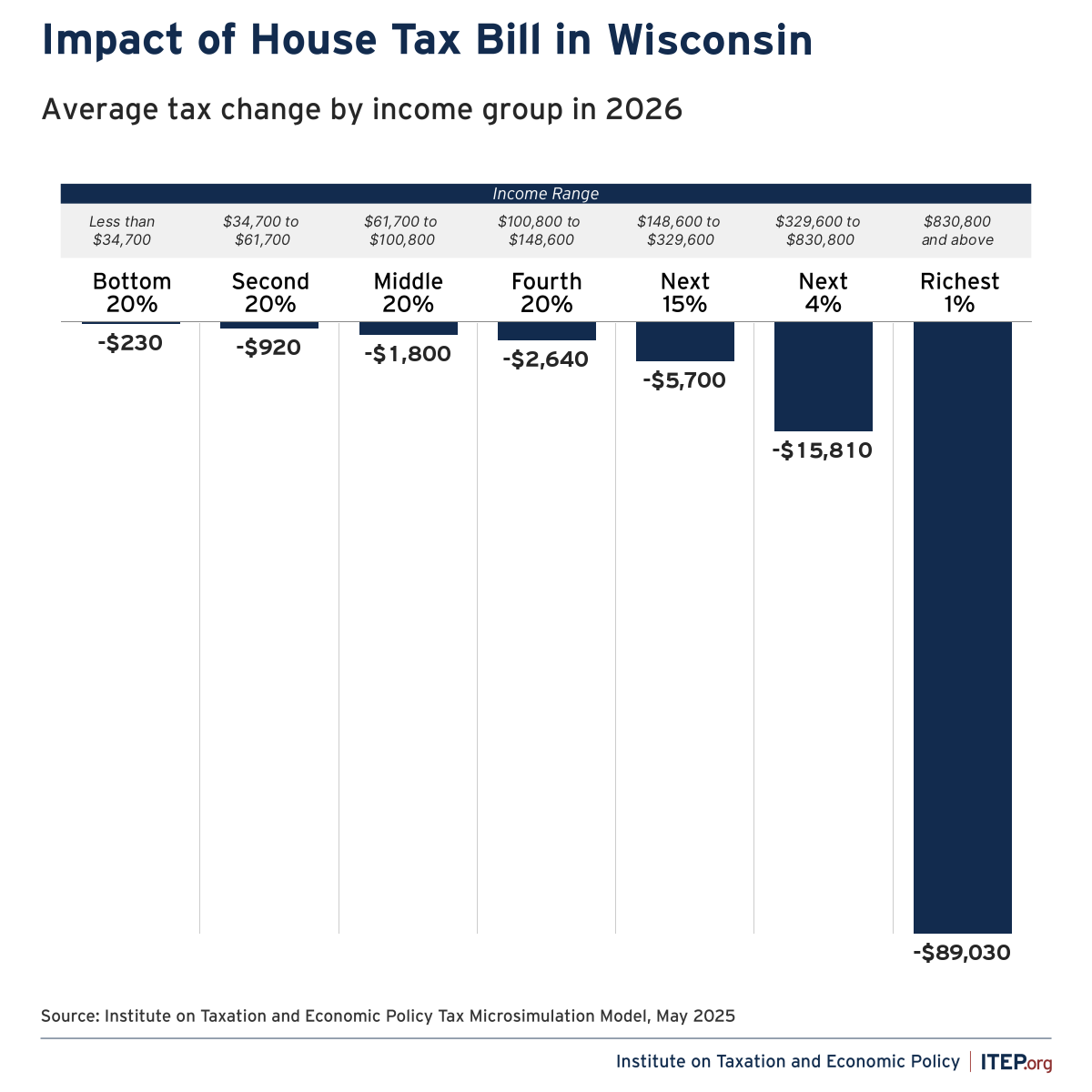

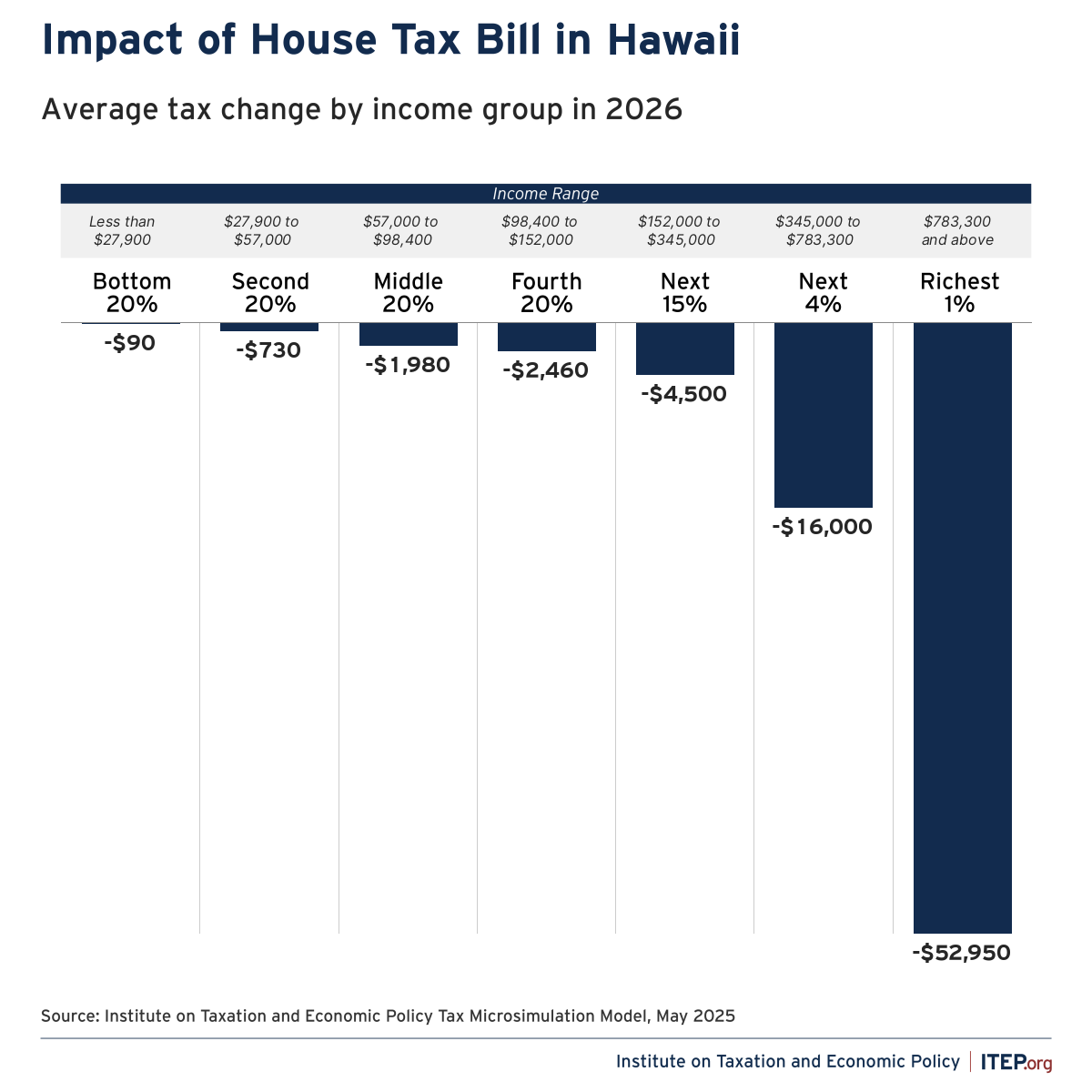

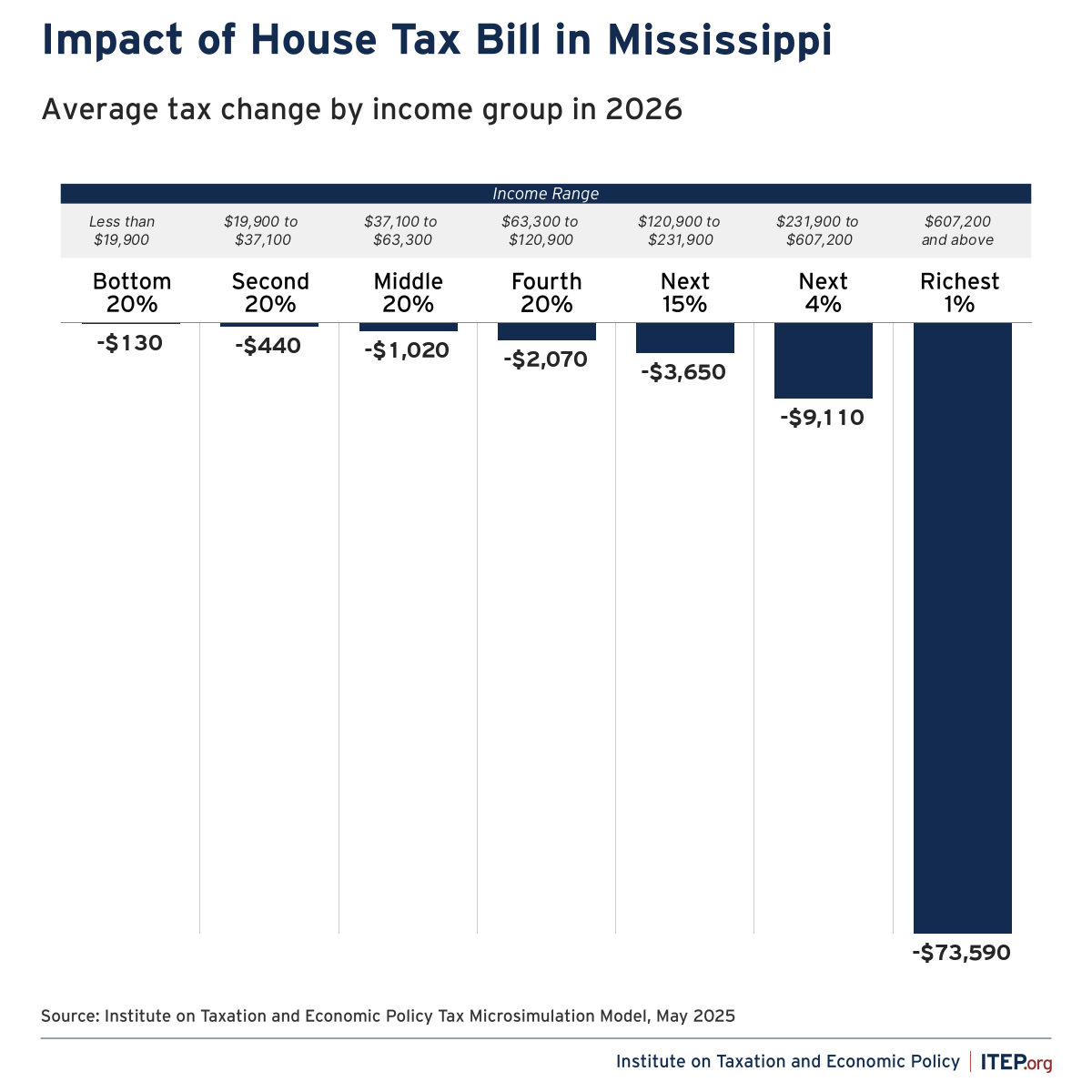

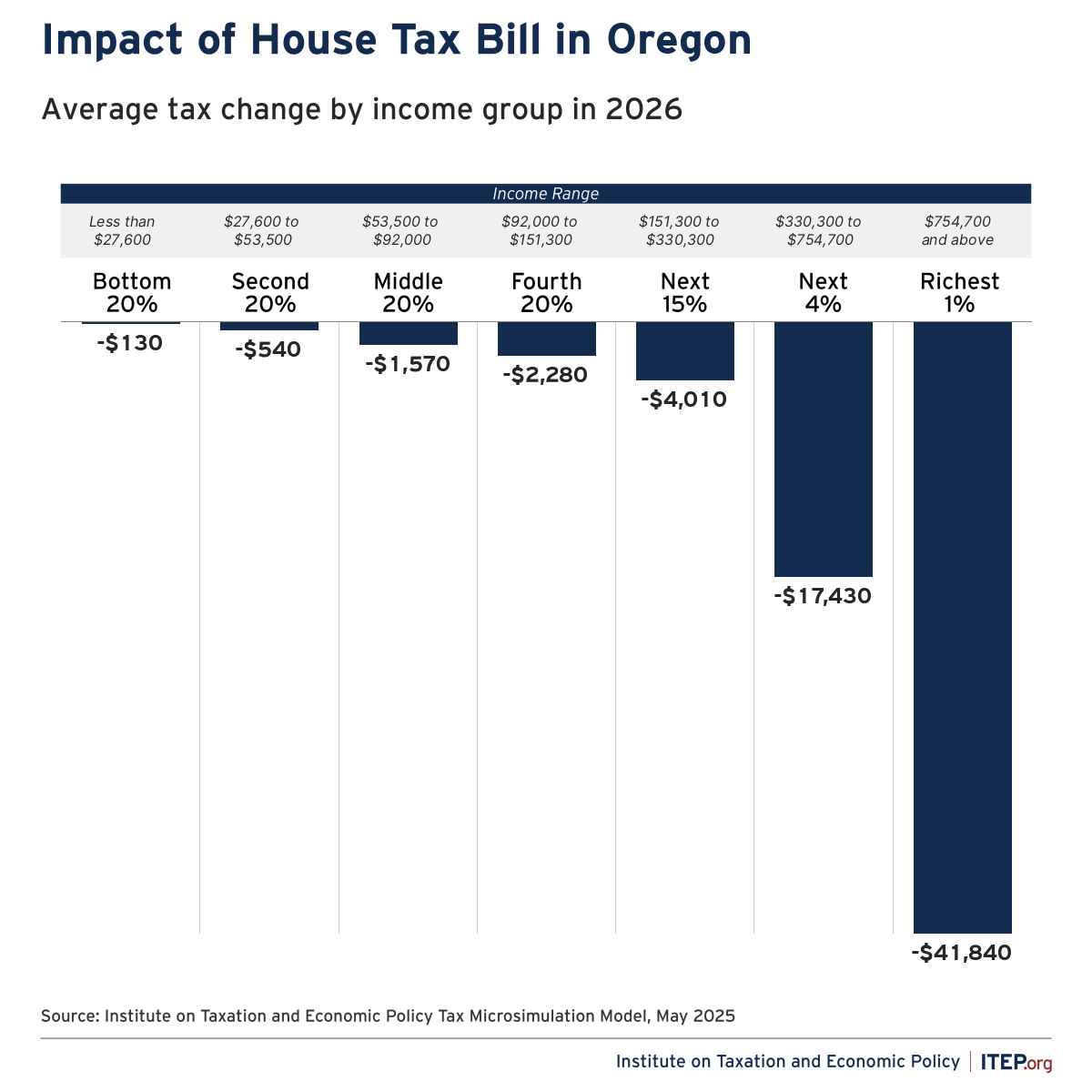

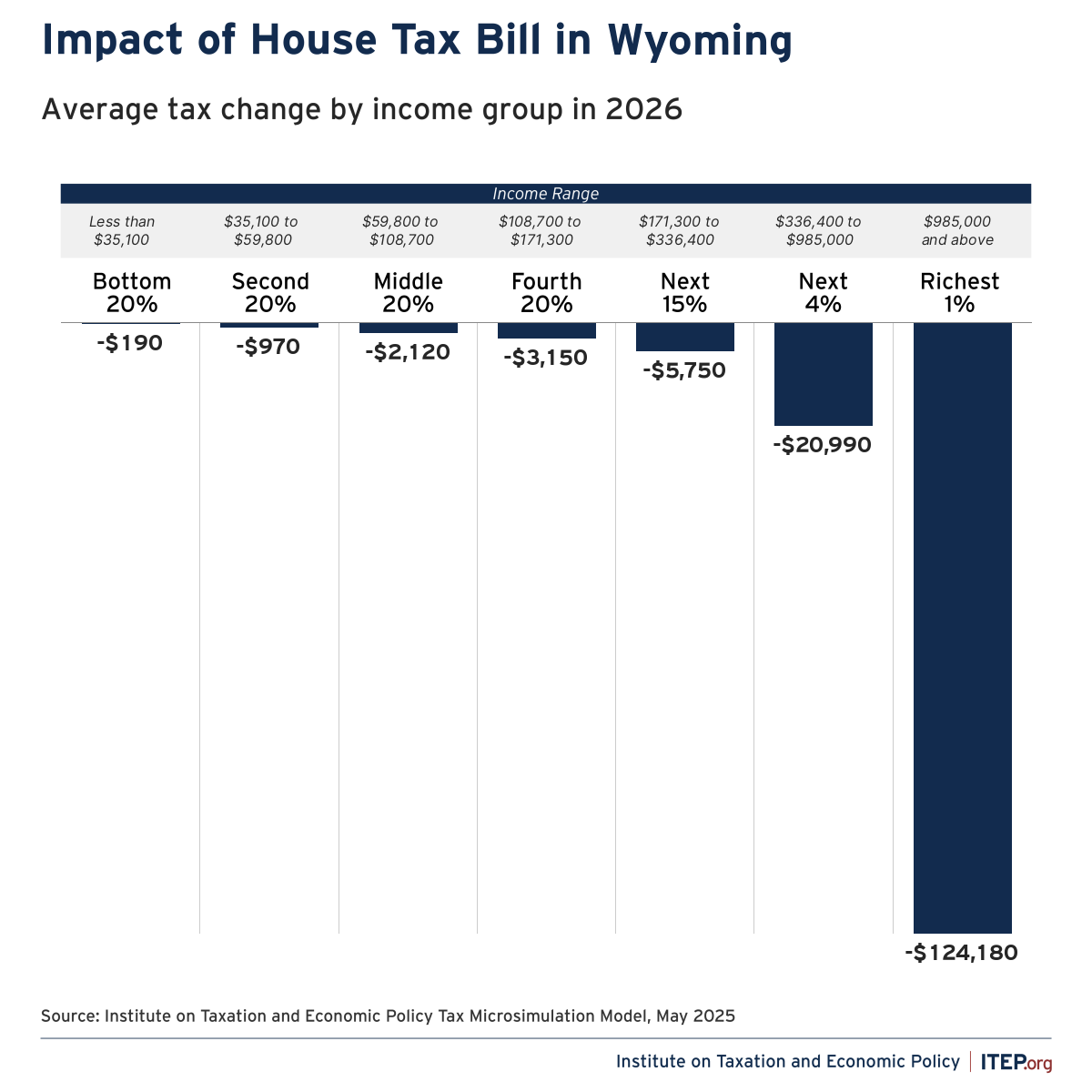

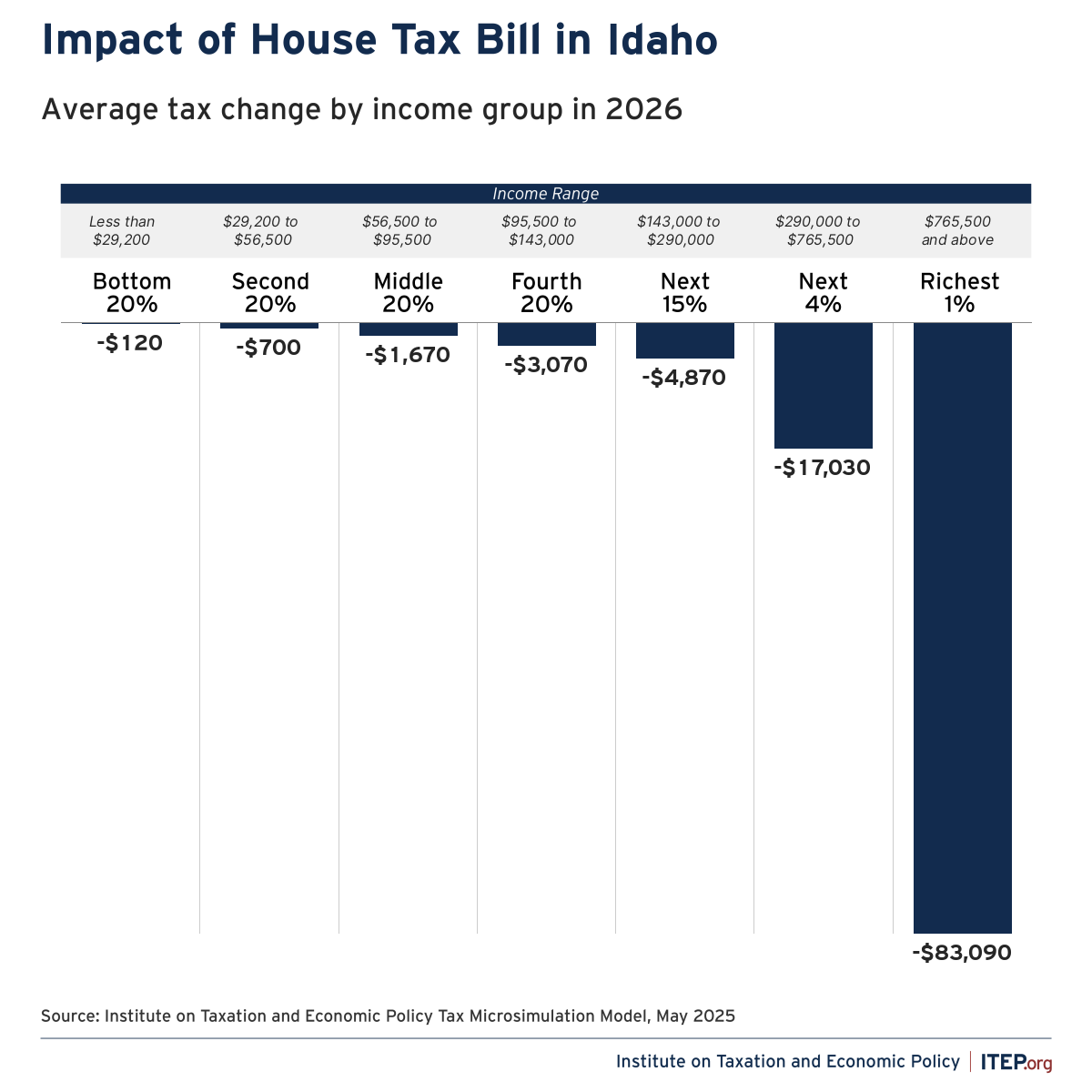

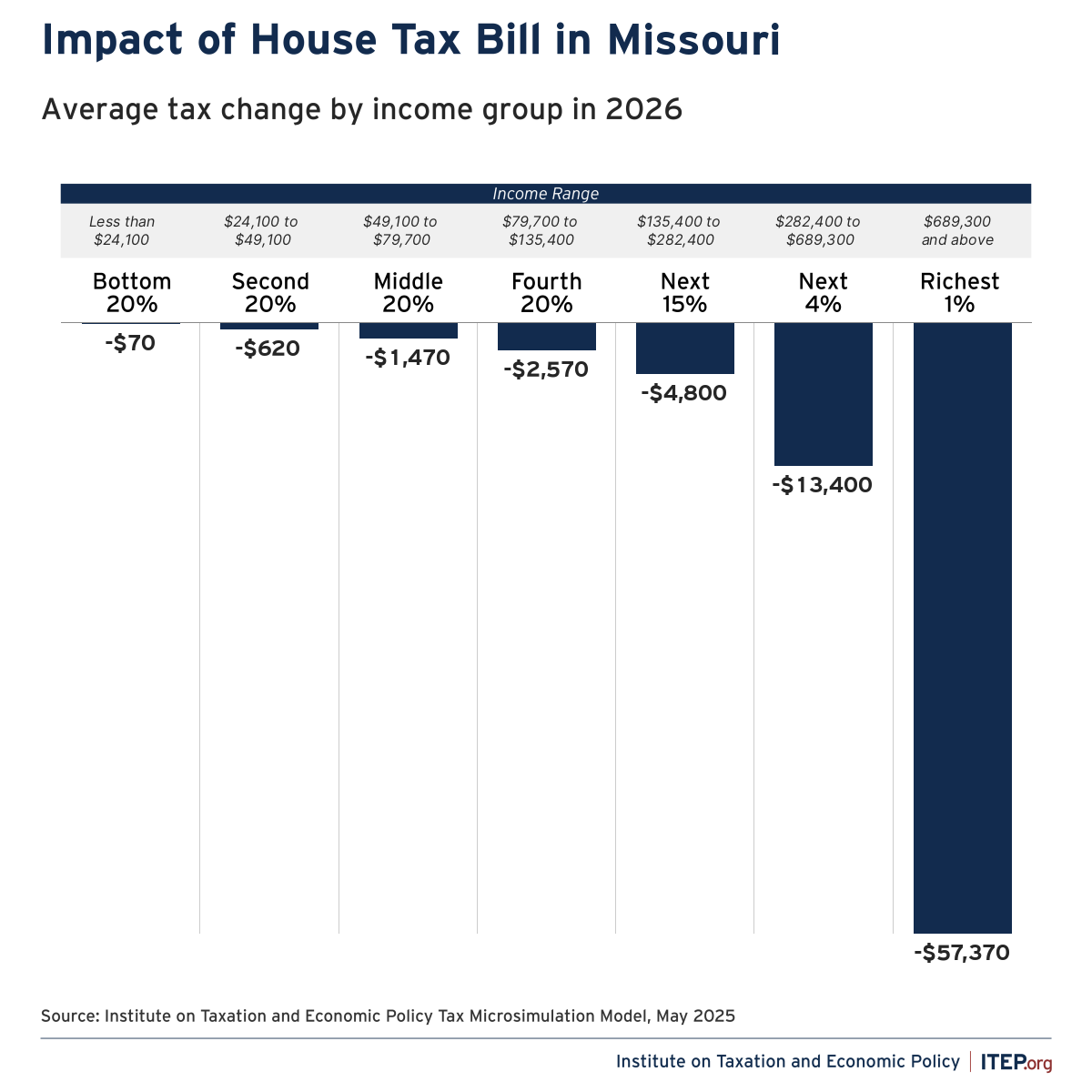

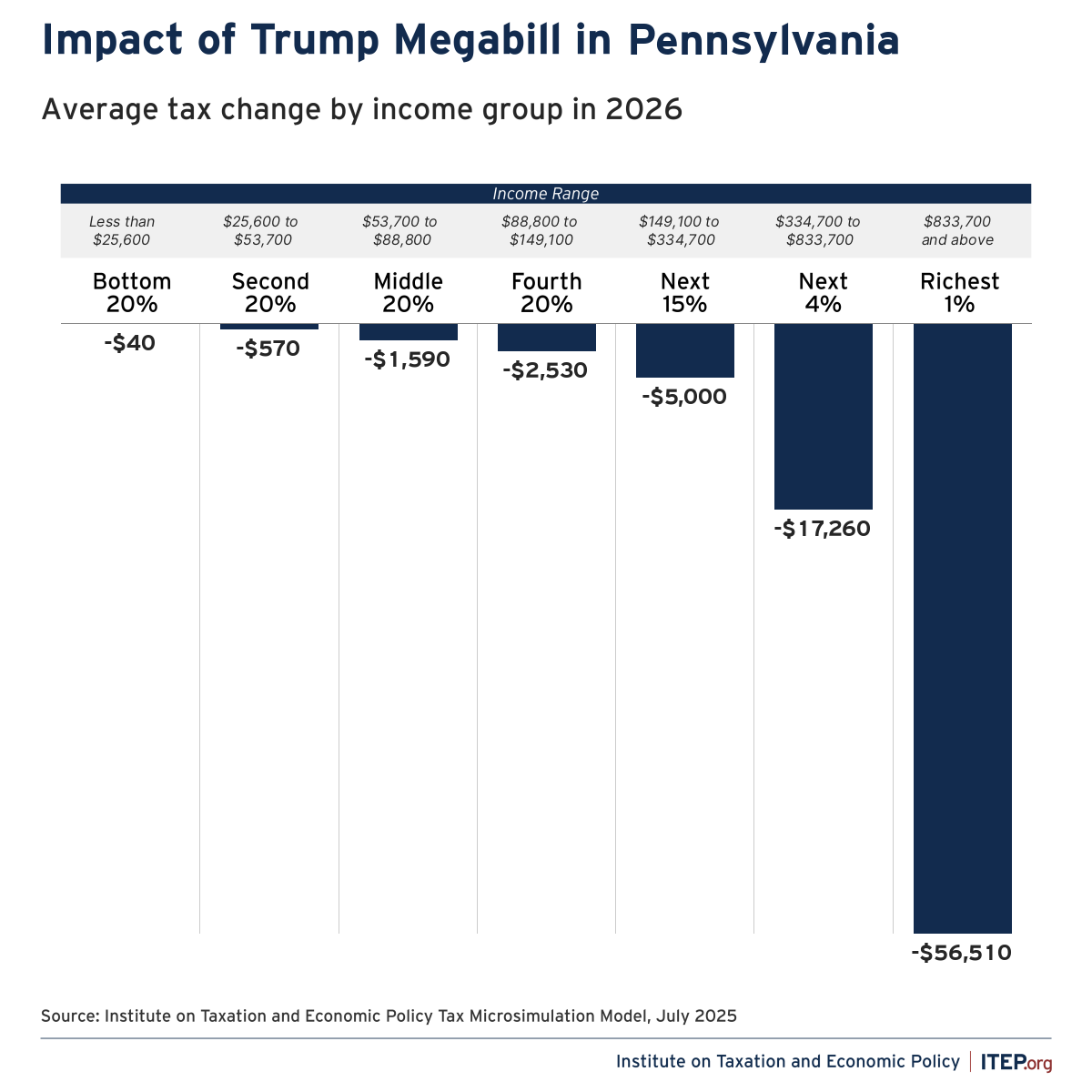

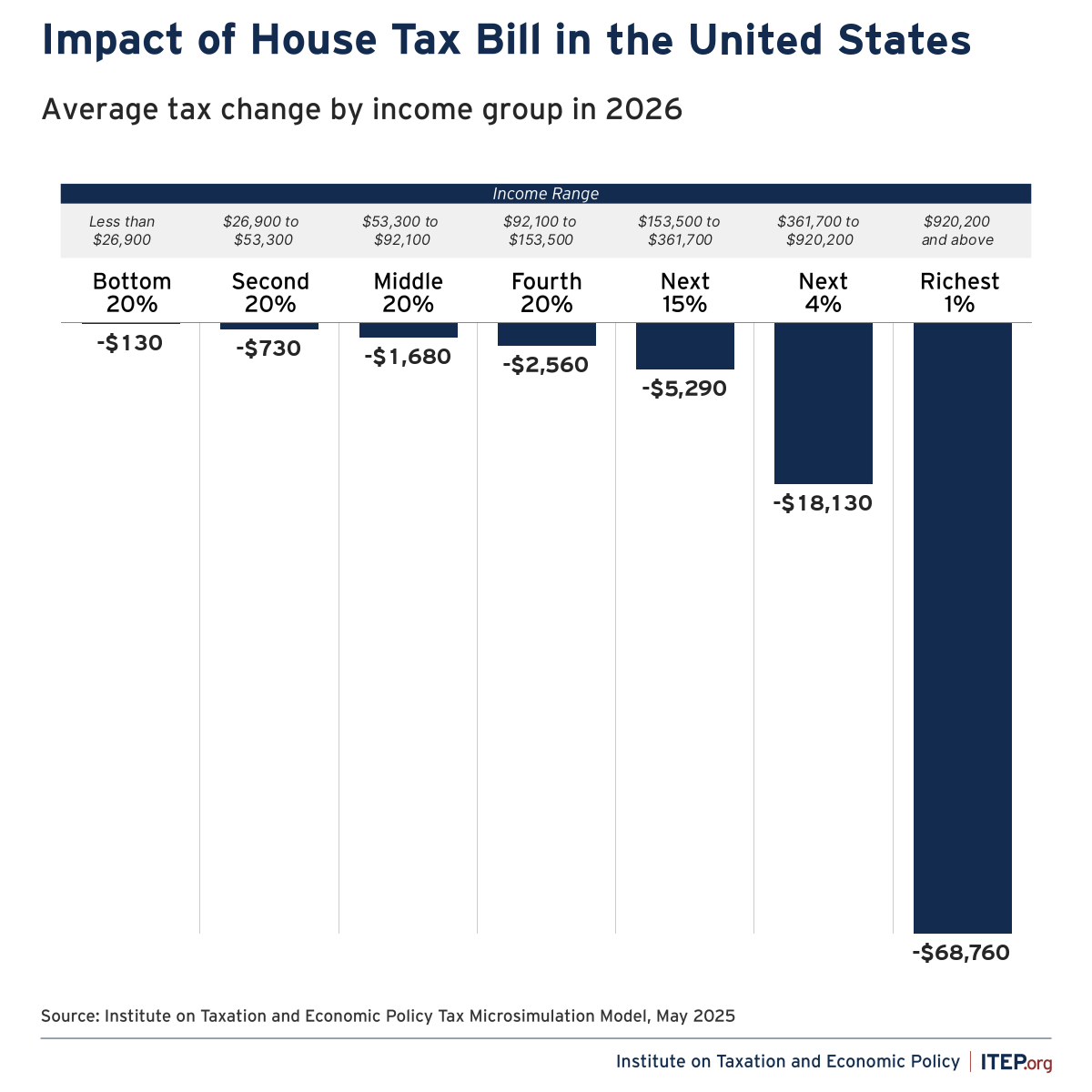

- The richest 1% of Americans will receive a total of $117 billion in net tax cuts in 2026, and more than a trillion in tax cuts over a decade.

- More than 70% of the net tax cuts will go to the richest fifth of Americans in 2026. Only 10% will go to the middle fifth of Americans, and less than 1% would go to the poorest fifth.

- The richest 5% alone will receive 45% of the net tax cuts next year.

- The effects of President Trump’s tariff policies alone offset most of the tax cuts for the bottom 80% of Americans. For the bottom 40% of Americans, the tariffs impose a cost that is greater than the tax cuts they will receive under this legislation.

Recent Work

- How Will the Trump Megabill Change Americans’ Taxes in 2026?

- There Were Far Cheaper and Fairer Options than the Trump Megabill

- Top 1% to Receive $1 Trillion Tax Cut from Trump Megabill Over the Next Decade

- Megabill Takes Cap Off Unprecedented Private School Voucher Tax Credit, Potentially Raising Cost by Tens of Billions Relative to Earlier Version

- Trump Megabill Will Give $117 Billion in Tax Cuts to the Top 1% in 2026. How Much In Your State?

Read More

Media Mentions

- New York Times: States Brace for Added Burdens of Trump’s Tax and Spending Law

- Washington Post: How Trump’s Big Bill Will Affect You, From Medicaid Cuts to Tax Credits

- Yahoo Finance: Child Tax Credit Gets Small Boost in Trump’s Tax Bill, but Millions of Families Are Left Out

- New York Times: Congress Passes a National School Voucher Program

- Video: ITEP’s Amy Hanauer Discusses Megabill on BreakThrough News

Read More

State-by-State Data

Download national and state-by-state estimates

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}