Chair, Vice Chair, and Members of the Committee,

Thank you for the opportunity to submit testimony in support of House Bill 1080, which would decouple the state from federal tax breaks for Opportunity Zones (OZs) and Foreign-Derived Deduction Eligible Income (FDEII). My name is Miles Trinidad, and I am a state analyst with the Institute on Taxation and Economic Policy (ITEP), a nonpartisan research organization based in Washington, D.C., specializing in state, local, and federal tax policy with a focus on equity and sustainability.

From their inception, OZs have suffered the enormous flaw that there is no requirement that the tax-subsidized investments benefit the people who currently live and work in high-poverty neighborhoods. Results have so far indicated that the program has largely failed to reach the populations that would most benefit from the stated support. ITEP finds that states that conform to the federal tax breaks for OZs will end up diverting resources from in-state priorities while assisting out-of-state investors and high earners.

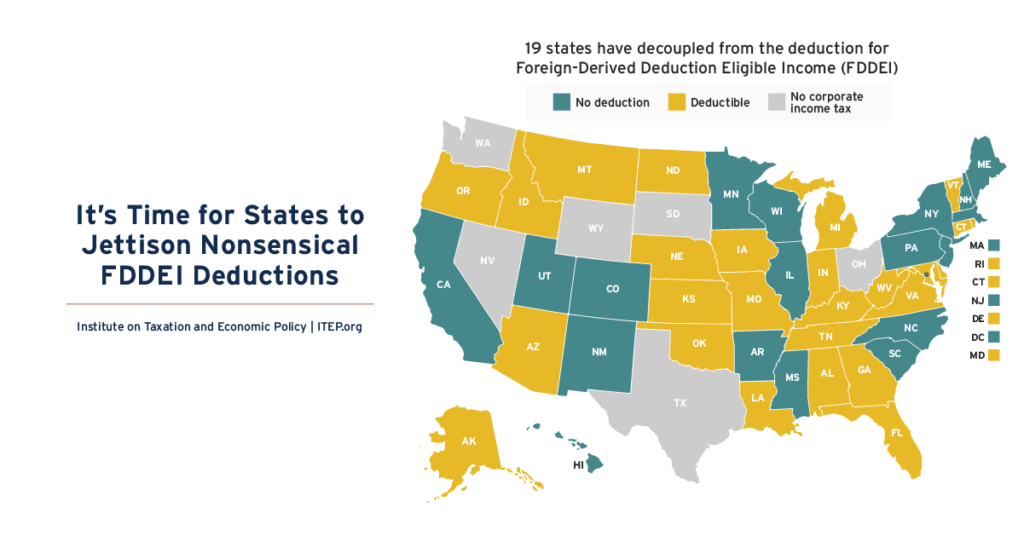

The FDDEI deduction (formerly known as FDII) is designed to lower the federal corporate tax rate on some profits generated from exports, meaning sales to customers in foreign countries. While the merits of the federal FDDEI deduction are disputed, one could argue that it at least was created with a certain logic in mind. The same cannot be said for state-level FDDEI deductions, which have received widespread criticism across the ideological spectrum, explaining why many states have opted not to offer FDDEI deductions. This provision taxes this designated income well below the standard corporate rate. And it has proven far more costly than originally estimated. But most egregiously, FDDEI has vanishingly little connection to in-state economic activity, and Maryland is providing FDDEI deductions on export sales originating out of other states. Put another way, there’s no guarantee that research and development, marketing, or management of intangibles incentivized by the FDDEI provision will occur in any particular state, yet coupled states lose revenue regardless.

The passage of the recent federal tax bill presents an opportunity for Maryland to be thoughtful about tax conformity. This committee can steer policy in a direction that better reflects the will of Marylanders and prevents tax giveaways that subsidize spending that may occur entirely outside of the state by wealthy out-of-state investors.

For these reasons, I urge a favorable report on HB 1080.

Thank you for your consideration.