Steve Wamhoff and Richard Phillips[1]

“I never made an investment decision based on the tax code… You know, maybe I should say more directly to you, if you’re giving money away, I’ll take it. You know, if you want to give me inducements for something I’m going to do anyway, I’ll take it. But good business people don’t do things because of inducements.”

Former Treasury Secretary Paul O’Neill during his confirmation hearings in 2001[2]

Summary

One of the most significant, but least understood, business breaks in our tax code is accelerated depreciation, the ability to write off the cost of investments in equipment more quickly than the equipment wears out.

Proponents of accelerated depreciation argue that it encourages companies to invest and expand their operations, thereby growing our economy. It is more likely that managers take the approach described in the above statement by Paul O’Neill, who had run large corporations like International Paper and Alcoa. As this report explains, this is corroborated by recent academic research.

Despite accelerated depreciation’s ineffectiveness, and despite the conflict between it and other aspects of our tax system, accelerated depreciation has been a permanent feature of the federal tax law for some time. Moreover, temporary expansions of accelerated depreciation called “bonus depreciation” were enacted during the recession and extended several times since then. The new federal tax law, the Tax Cuts and Jobs Act (TCJA) goes even further. It allows “full expensing,” which is the ability to write off the entire cost of an investment in the year it is made. Congress permitted full expensing only for five years, which will encourage businesses to speed up investments they would have made later. Republicans in Congress have discussed making the expensing provision permanent.

This report argues that Congress should move in the other direction and repeal not just the full expensing provision but even some of the permanent accelerated depreciation breaks in the tax code, for several reasons.

Accelerated depreciation encourages wasteful tax shelters, drains enormous amounts of revenue from the Treasury, is (mostly) irrelevant to small businesses and does not help our economy. It is not clear that accelerated depreciation really increases investment in the long-run. Some companies may expedite planned investments in order to take advantage of tax breaks before they expire, but just as O’Neill explained, they are not likely to be doing anything they would not have done in the absence of tax breaks.

Why are depreciation breaks so ineffective at stimulating investment and boosting economic growth? The answer is connected to one of the more baffling aspects of the tax reform debate over the past decade. Corporate CEOs and their lobbyists for years begged Congress to cut the statutory tax rate (which was 35 percent) even though most companies paid an effective tax rate that was far lower than 35 percent, and many paid nothing at all. Why would CEOs whose corporations effectively dodged federal taxes even want federal tax reform? What could be in it for them? The surprising answer: what corporations report to investors is determined by accounting rules that recognize most tax breaks but ignore those related to depreciation. CEOs and CFOs could use depreciation breaks to wipe out their federal tax liability and yet they received no thanks from investors, who rely on information that ignores this type of tax break.

What Is Accelerated Depreciation? A Tax Break that Conflicts with the Idea of Taxing Income.

Our tax system is built on the simple principle of taxing income. In the case of a business, we can think of income as any increase in a company’s net worth. To take a simple example, if a store sells widgets, it will purchase widgets in bulk from a manufacturer and sell them to consumers at a slightly marked-up price. If the store generates $1 million this year in gross income from selling widgets, it will subtract the cost of purchasing that inventory, as well as the cost of compensating employees and other expenses, from its gross income to calculate its taxable income.

Calculating income becomes a bit trickier when one considers longer-term investments. If a company buys a machine for $10,000 that turns raw materials into widgets, its net worth remains constant. It has $10,000 less in cash but it owns a machine worth $10,000. However, if the value of the machine declines over time (because it wears out) then the net worth of the company declines as well. For example, if the $10,000 machine lasts 20 years and loses value at a constant rate during those 20 years, then the best way to account for its cost would be to reduce the company’s income by $500 each year for 20 years. This is another way of saying that the machine depreciates over time.

The income tax rules generally match the timing of the expenses and income so, ideally, the tax code would calculate income based on the actual economic depreciation or loss in value of assets each year. However, several special breaks in our tax code allow such depreciation for tax purposes to be accelerated. This means that businesses can write off the costs of such investments more quickly than would be justified by the real-world decline in the assets’ value (faster than economic depreciation, in other words).

This may initially seem like a trivial matter because, at first glance, it would seem to determine the timing rather than the amount of taxes paid. Corporations could deduct the costs of capital investments sooner rather than later. But the acceleration of these deductions is enormously important because of the time value of money, the fact that a dollar is worth more today than it is in the future. Taking these deductions earlier allows businesses to defer paying some portion of their taxes for several years, which is the equivalent of receiving an interest-free loan from the federal government.

For example, assume a company purchases a machine for $10,000, that the pre-tax rate of return on this investment is 6.1 percent annually (meaning it will generate revenue of $610 each year) and that the machine will wear out and stop producing revenue after two decades. Assume the company is a corporation subject to a tax rate of 21 percent.

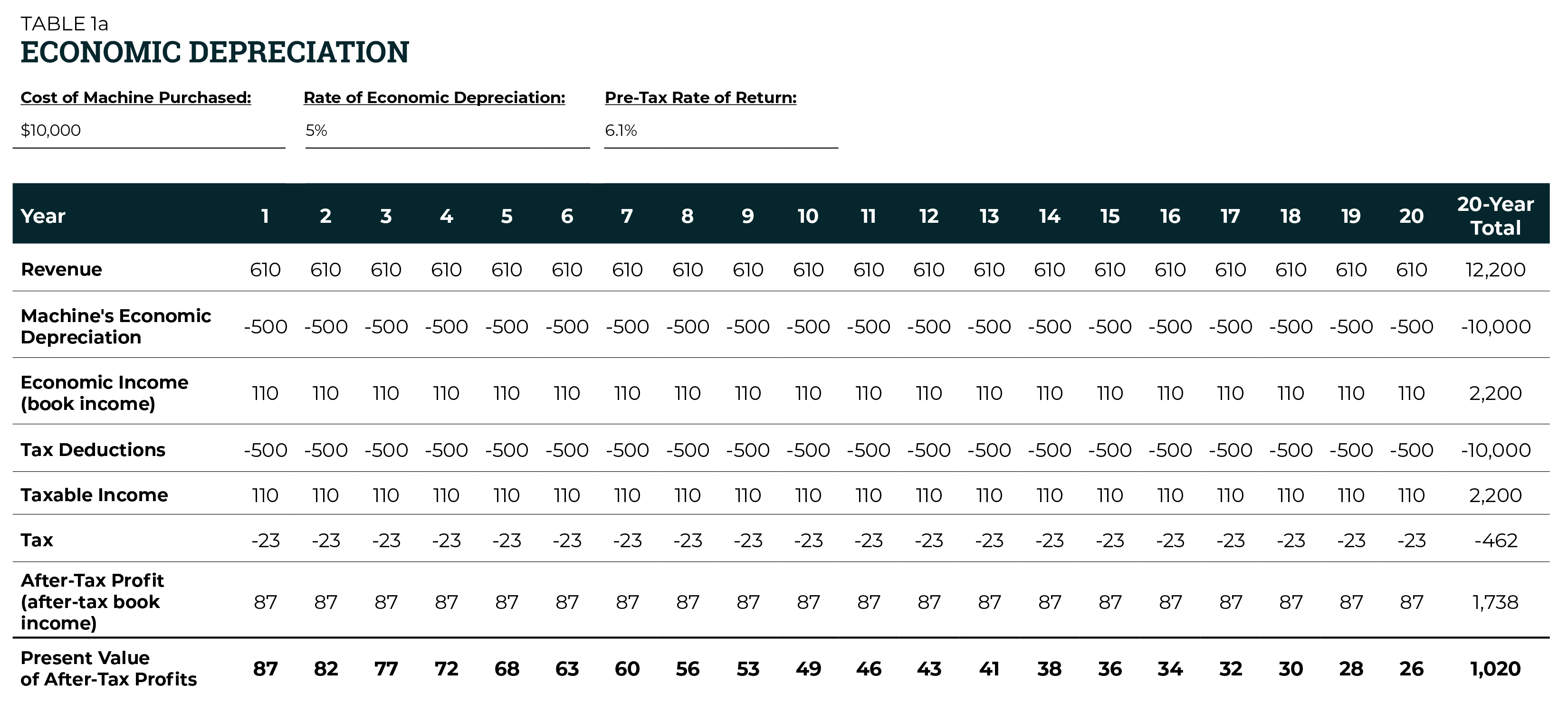

Table 1a illustrates what would happen in this very simple example if depreciation for tax purposes matched economic depreciation.

Five percent of the cost of the machine ($500) is deducted in each of the 20 years. The “economic income” (the increase in the company’s net worth each year) from this investment is equal to the revenue generated annually ($610) minus the amount by which the value of the machine declines each year ($500), for a total of $110 annually. Since the tax rules in this hypothetical example match economic depreciation, the company’s taxable income each year is the same as its economic income, $110 per year. Assuming the tax rate is 21 percent, the company pays $23 in taxes each year on the income from this investment, for an after-tax profit of $87 each year.

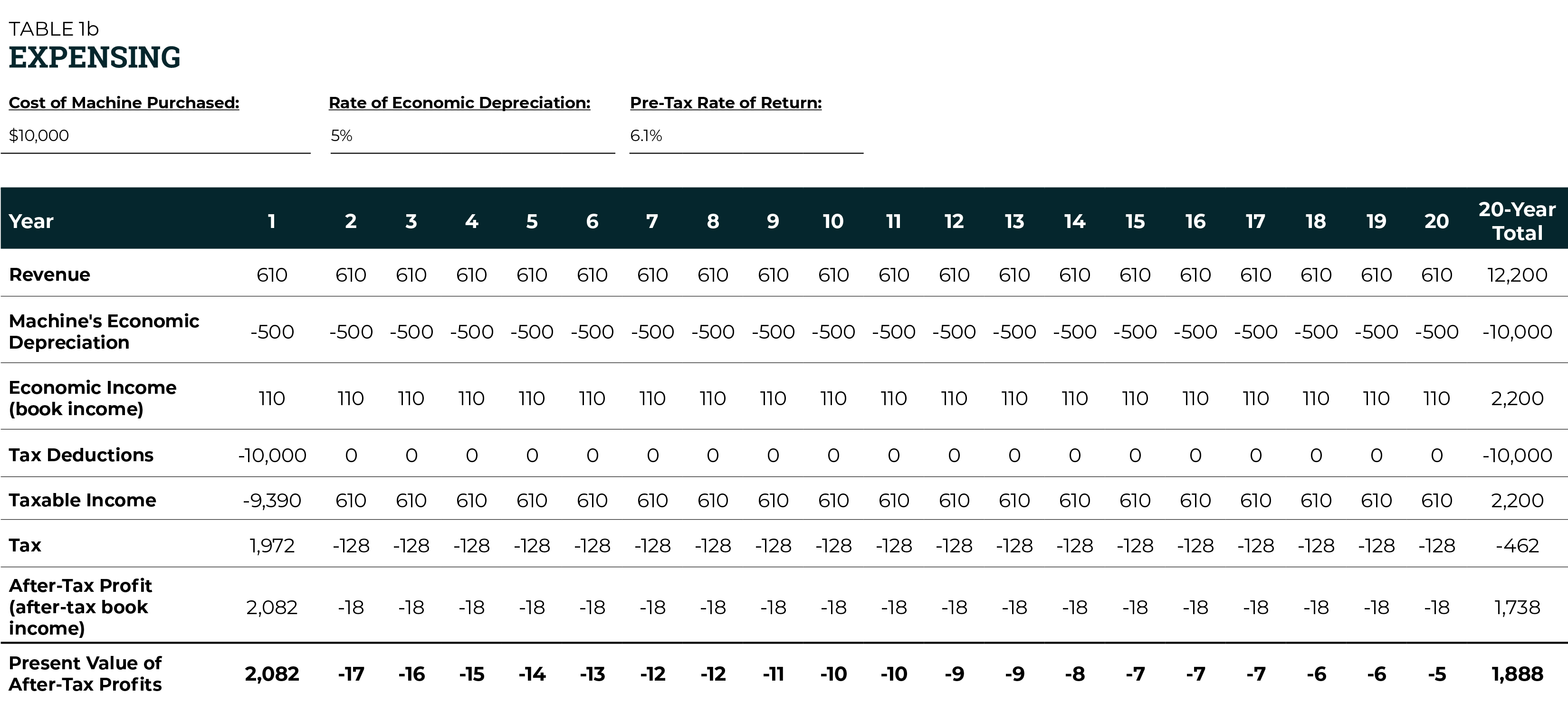

Now consider Table 1b, illustrating the same example but allowing for full “expensing,” which is the most accelerated depreciation possible. This means the company can deduct the full $10,000 cost of the machine in the first year.

Over the course of 20 years, the firm deducts the same amount for depreciation, $10,000, as in the previous example. As a result, the taxable income, tax and after-tax profits over the course of 20 years is the same in both examples.[3]

But the final line on both Tables 1a and 1b, which provides the “present value” of the after-tax profits, reveals the true difference between economic depreciation and full expensing. The present value is the value of future profits today. A dollar of profits next year is worth less than a dollar of profits this year, because a dollar of profits this year could be invested to generate more revenue. As already mentioned, the firm’s rate of return is 6.1 percent. After-tax profits generated today can be invested in more machines that will generate a 6.1 percent return each year. Calculations of present value can be complex, but for this purpose one can simply think of a dollar of after-tax profit generated in a given year as having 6.1 percent less value than a dollar of after-tax profit generated in the year before. In other words, a dollar in year two is worth roughly 93.9 percent of a dollar generated in year one.

The final line in both Tables 1a and 1b illustrates the present value of the after-tax profits in each year. (One can think of this as showing the value in year one of the profits generated in each of the 20 years.) Taking into account the “time value of money” in this way, we see that the investment generates an after-tax profit of $1,020 if economic depreciation applies and $1,888 if full expensing is allowed.

Accelerated depreciation shifts our tax system away from taxing income and towards taxing consumption, which effectively exempts income from investments. Income is either spent on consumption or it is saved and invested. If lawmakers start with an income tax but then exempt investment income, then they would tax only consumption. The full expensing provision in the new federal tax law takes a step in this direction by allowing certain investments to be tax-free.

Some economists favor expensing and other provisions that move us closer to a consumption tax because, they argue, this encourages businesses to invest more. They argue that an income tax places a double-tax on investment because, in the example above, income is taxed before it is used to purchase a machine to make widgets, and then the income generated by selling the widgets is also taxed.

Tax investment less and we will have more investment, they argue, growing the overall size of the economy. If the company in this example was unable to raise money by borrowing or issuing stock, it could face constraints on how much it can invest. By allowing the company to deduct the entire cost of the machine in the first year, expensing gives money back to the company that could then be used to buy a larger machine or buy additional equipment that would also generate revenue. Proponents therefore see this policy as one that increases private sector investment overall.

But this means that the government is able to invest less in the public goods and public services that the private sector does not adequately provide like defense, public safety, infrastructure, education, and health care, to name a few. (More details on the costs of accelerated depreciation are provided further on in this report.) Another problem is that consumption taxes are more regressive than income taxes. Poor families usually put all their income towards consumption (to purchase necessities) while high-income families are able to devote much of their income towards investments.

But even economists who generally favor consumption taxes should be able to see a problem with the approach to full expensing in TCJA. It is particularly problematic to have a tax system like ours that has some elements of both an income tax and a consumption tax. Allowing full expensing is consistent with a consumption tax. Allowing deductions for interest payments (and other business deductions) to calculate taxable income is consistent with an income tax. But allowing both provides businesses with tax treatment that is more generous than either a consumption tax or an income tax properly implemented. In other words, allowing both expensing and interest deductions can result in tax shelters.

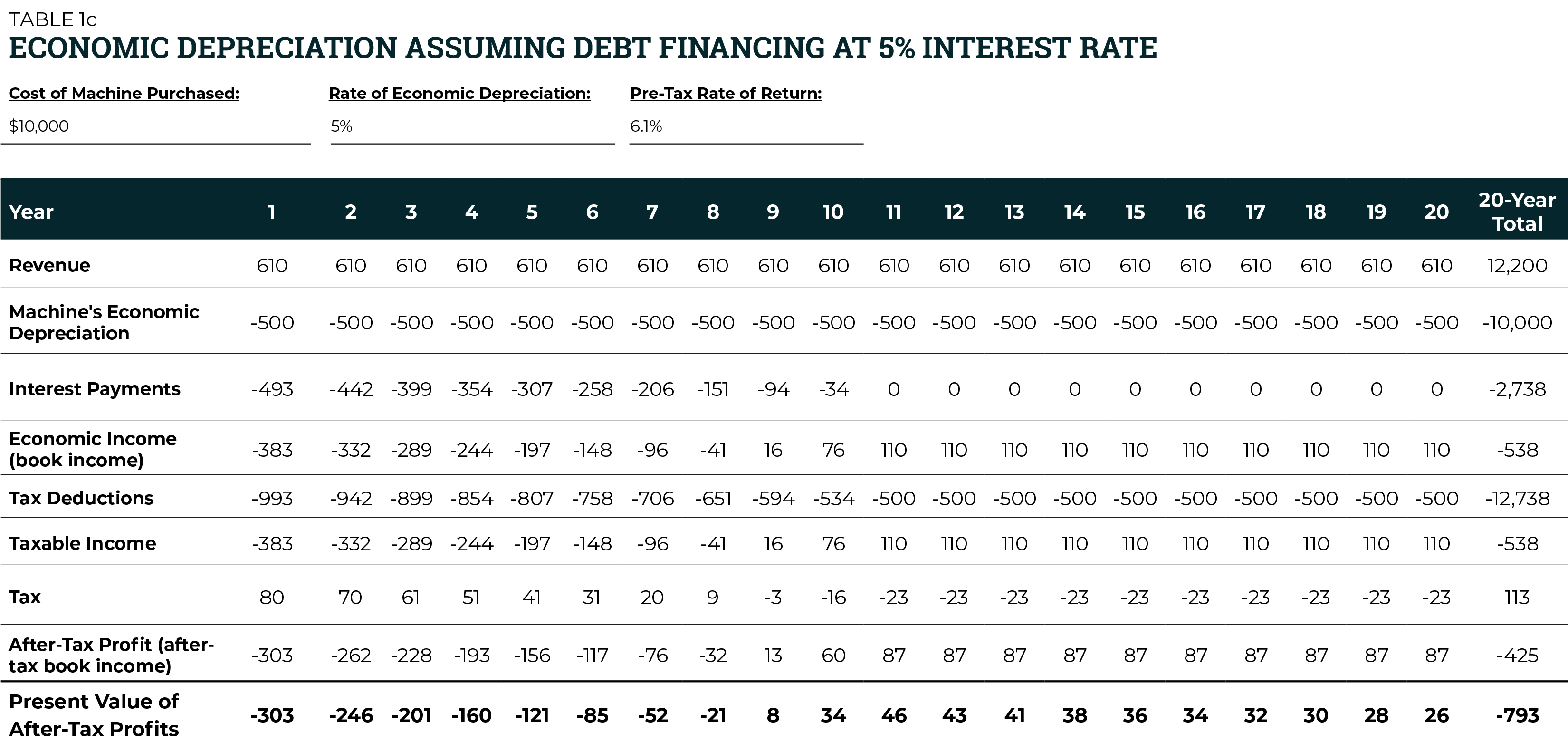

We can consider the above examples again but alter them to assume that the company borrows to purchase the machine.

Because our tax system generally taxes income (the increase in the net worth of the company), money borrowed by a company is not taxed because it does not increase the company’s net worth. A loan provides the company with $10,000 in additional cash, but it comes with a $10,000 debt, thus having no effect on its net worth. Receipt of the $10,000 loan is not counted as income, and repayment of the $10,000 is not deductible. However, interest payments on the debt do reduce the company’s net worth, so the income tax rules allow the business to deduct them. This is illustrated in Table 1c, which assumes the firm financed the purchase of the machine with a ten-year loan at an interest rate of 5 percent.

Table 1c assumes the company is subject to economic depreciation. In most respects, it is like Table 1a. The difference is that its pre-tax profits are reduced by interest payments for the first ten years (which in year one come to $493) and the tax deductions are increased by the same amount each year. Compared to the company that did not borrow, each year the pre-tax profits are reduced by interest payments while the company’s tax liability is reduced by a smaller amount (equal to the interest payment multiplied by the tax rate of 21 percent).

Table 1c shows that the company has, over the 20 years, a $425 loss on this investment. Adjusting for the time value of money makes the picture even worse. The present value of the profits and losses generated by the investment come to a 20-year loss of $793. In other words, the company should not buy this machine if it must borrow to finance the investment.

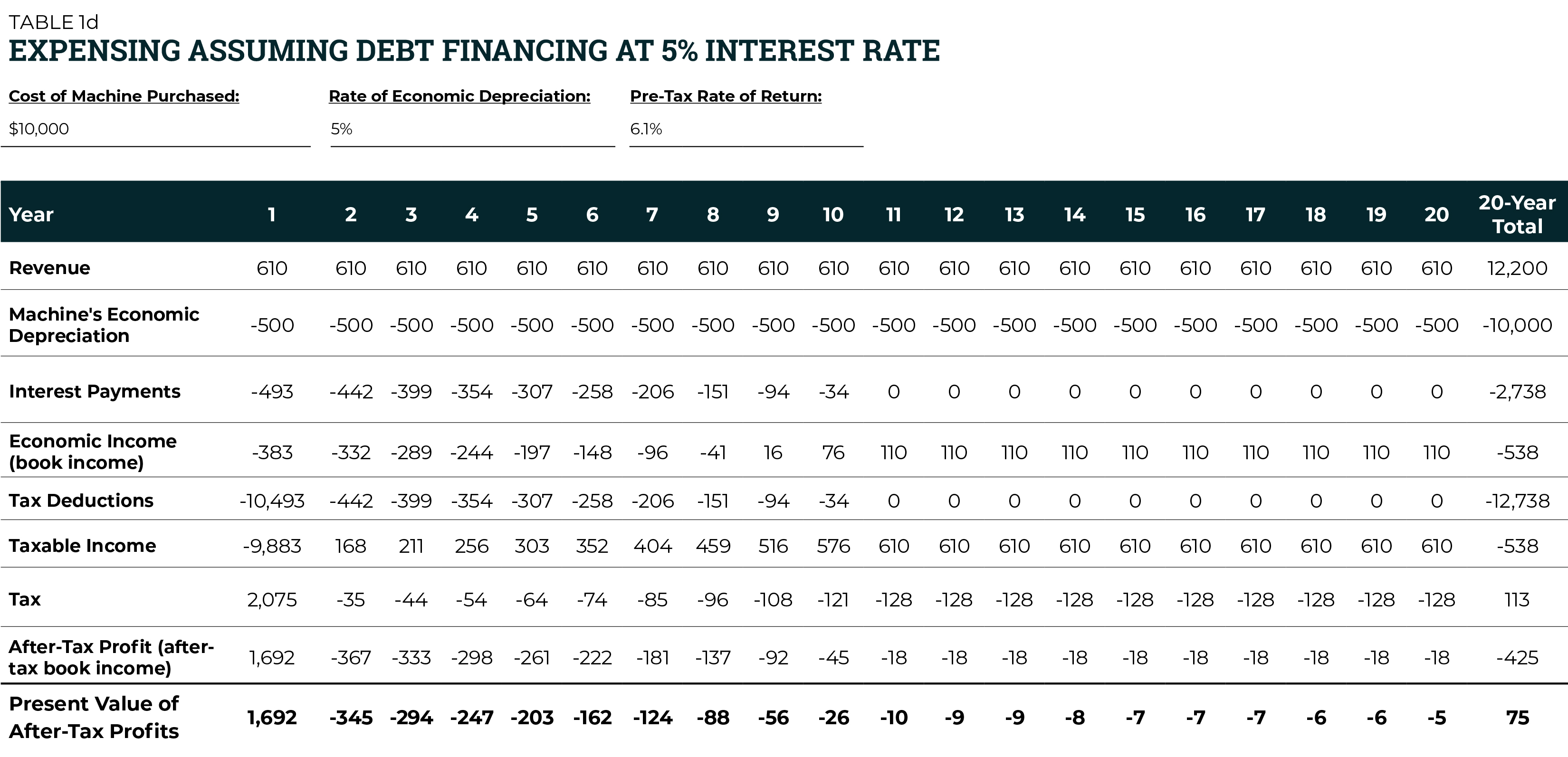

But if the company is allowed full expensing and is allowed to continue deducting interest payments, the investment suddenly becomes profitable, as illustrated in Table 1d.

In the example with full expensing and interest deductions, the company still suffers a net loss of $425 over the two decades, but adjusted for the time value of money, the picture is quite different. Over the 20 years, the present value of the after-tax profits outweigh the present value of the after-tax losses. The present value of the gains and losses over the two decades comes to an after-tax profit of $75.

An investment that would not otherwise be profitable becomes profitable only because of tax law. That is another way of saying the investment is a tax shelter. An investor could buy a machine that actually loses money in a business sense but generates an after-tax profit by exploiting the mismatch in the tax code’s treatment of investments and debt.

In this example, the company is not subject to consistent rules. Full expensing would make sense under a consumption tax, but interest deductions make sense under an income tax. Allowing both provides the company tax treatment that is more generous than either an income tax or a consumption tax properly implemented.[4]

The new federal tax law, the Tax Cuts and Jobs Act (TCJA), temporarily provides full expensing but also places new limits on interest deductions. Unfortunately, these limits would only reduce a fraction of the deductibility of interest.[5]

What Provisions Provide Accelerated Depreciation?

Under the default depreciation rules, most assets are subject to the Modified Accelerated Cost Recovery System (MACRS), which allows assets to be written off more quickly than they wear out and stop producing income.[6]

Under MACRS, tangible property used for business is generally depreciated over 3 to 20 years in the case of equipment. Residential buildings (like apartment buildings for rent) are depreciated over 27.5 years and non-residential buildings are depreciated over 39 years. Land is not depreciated because it does not wear out.

The depreciation breaks provided by MACRS have often been supplemented by additional breaks which were supposedly temporary, such as “bonus depreciation,” boosting the portion of equipment investment costs deducted in the first year, sometimes even to 100 percent (full “expensing”).

Despite Paul O’Neill’s statements that tax breaks never changed his decision-making as a businessman, the president he served under, George W. Bush, signed legislation in 2002 that provided bonus depreciation, ostensibly to stimulate the economy. Bonus depreciation was only allowed to expire for two years (2006 and 2007) since then. In every other year since 2002, Congress made this “temporary” break available.[7]

The TCJA expands accelerated depreciation yet further. From 2018 through 2022, the portion of equipment investment costs that can be deducted in the first year is set at 100 percent and then gradually declines each year after that until reverting to the permanent rules in 2027. The recovery periods for real estate (27.5 years for residential buildings and 39 years for non-residential buildings) were not changed.

Republican leaders in Congress have said that they hope to make permanent or extend the full expensing provision beyond 2022.

The Largest Depreciation Break Does Not Benefit Small Businesses

When President Bush and Congress provided bonus depreciation in 2002, and in all the subsequent legislation that extended and even expanded that tax break, it was not necessary to help small businesses.

Bonus depreciation (which has been temporarily expanded into 100 percent first-year depreciation or “expensing” under the TCJA) is provided under section 168(k) of the tax code. The benefit provided by section 168(k) has no limit based on the size of investments.

Any company that typical Americans would call a “small business” was already allowed to deduct the full costs of investments when they are made under a different provision, section 179. Section 179 is limited so that, in effect, it generally helps smaller companies.

Before TCJA was enacted, section 179 allowed a business that invested less than $2 million in a year to deduct 100 percent of the costs of up to $500,000 in investments in the year they are made. The new law increases those limits so that a firm with investments of less than $2.5 million in a year can deduct 100 percent of up to $1 million in investments in the year they are made.

The merits of section 179 are debatable, but one thing is clear: It does not benefit massive corporations like Boeing or General Electric. To put it another way, even if Congress does believe that depreciation breaks are helpful, it could provide them solely for smaller businesses through Section 179.

As illustrated by the figures in the next part of this report, section 179 costs just a fraction as much as the depreciation breaks for larger businesses.

Depreciation Breaks Are Expensive

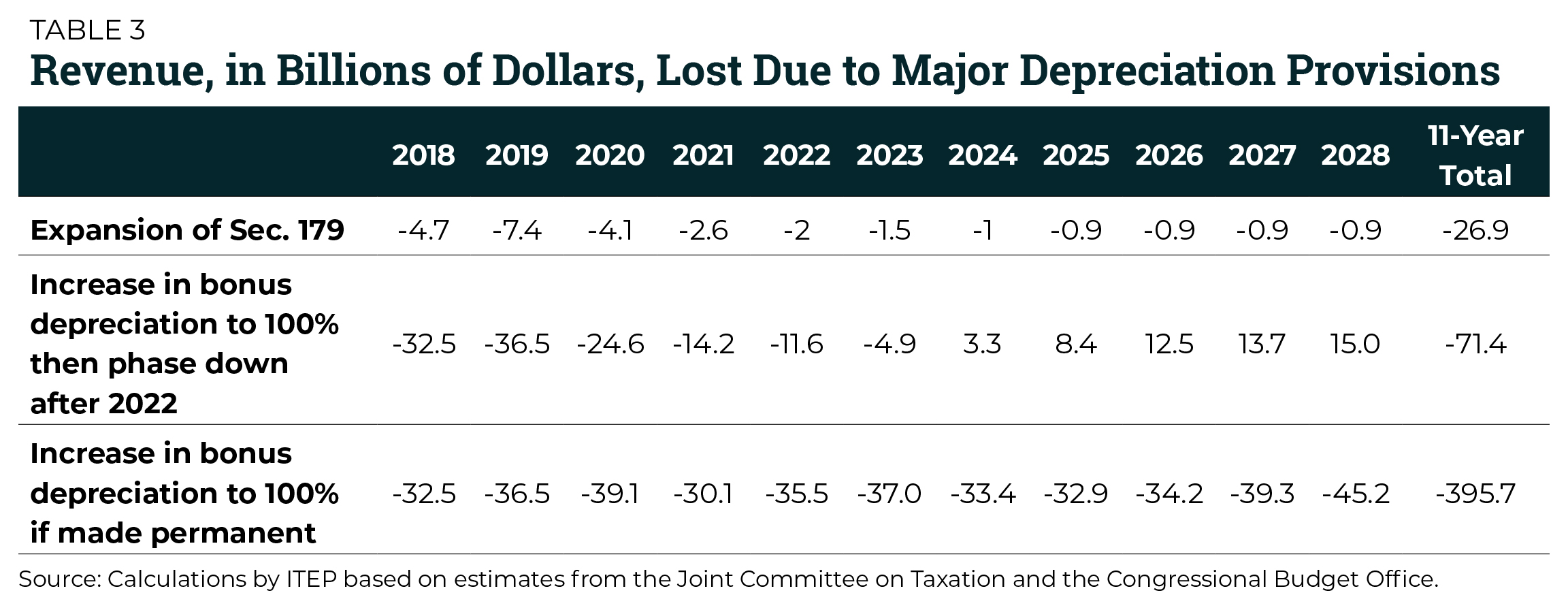

Congress’s official revenue-estimator, the Joint Committee on Taxation (JCT), has calculated that the revenue lost due to section 179 from 2017 through 2021 will total $65 billion while the revenue lost due to bonus depreciation and expensing for equipment under section 168(k) during that same period will come to $266 billion.

The figures in Table 2 are from JCT’s estimates of “tax expenditures,” which are subsidies provided through the tax code by provisions that deviate from the basic rules of the tax system. In this case, the basic rule is that the federal government taxes the income of businesses, which can be thought of as any increase in a company’s net worth. If depreciation for tax purposes matched economic depreciation (meaning the costs of capital investments would be deducted as those investments wear out and stop generating income), then there would be no tax subsidy for depreciation.

There was a time when even larger, more problematic depreciation tax breaks were allowed. Exceptionally generous rules were in effect in the early 1980s, creating an epidemic of tax shelters and tax avoidance that led to the Tax Reform Act of 1986. However, the less-wasteful depreciation system created by that act, the Modified Accelerated Cost Recovery System (MACRS), still allows assets to be written off more quickly than they wear out and stop producing income.

MACRS also includes what is called the Alternative Depreciation System (ADS) which more closely follows economic depreciation (more closely tracks the useful lives of assets). But MACRS only uses ADS in limited situations.

Because depreciation under ADS comes closer to matching economic depreciation, JCT considers any depreciation rules that are more generous than ADS, such as MACRS, section 179 and section 168(k), to be tax expenditures.

This suggests that Congress could eliminate accelerated depreciation by repealing MACRS and requiring all depreciation to be done under ADS. In 2011, JCT concluded that this could raise more than $700 billion over a decade.[8] An analysis from the U.S. Treasury Department found that this reform would raise less revenue each decade after enactment, so that the savings in the fourth decade would be just 60 percent of the savings in the first decade.[9] This serves as a warning to lawmakers about just how much of the revenue savings they could use to offset new spending or new tax cuts. But this reform would still raise significant revenue even in the long-term.

The budgetary savings would decline over time because depreciation breaks, to a degree, affect the timing of tax payments rather than the amount. If a business owner or corporation is allowed to deduct the cost of purchasing equipment sooner rather than later, that means tax payments will be lower in the near-term and higher in the long-term.

This timing element of depreciation tax breaks can make it difficult to understand their costs. For example, Table 3 illustrates the revenue loss resulting just from the changes that TCJA made to section 179 and to bonus depreciation. TCJA’s provision to expand bonus depreciation into 100 percent depreciation through 2022 was estimated by JCT to lose revenue for the first few years and then raise revenue in later years, as taxes that were deferred by businesses taking deductions earlier would finally come due. (The revenue gain is outweighed by the revenue loss in earlier years, resulting in a long-term net loss for the federal government.)

Table 3 also provides estimates of the costs of TCJA’s 100 percent depreciation (expensing) provision if it is extended beyond 2022. (These estimates combine JCT’s estimates of TCJA with projections from the Congressional Budget Office of the cost of extending the temporary expensing provision.) While the revenue loss may decline in future decades, it is nonetheless enormous.

The JCT and CBO figures do not show the full cost of these provisions in the sense that their estimates do not reflect the time value of money. Each dollar of deductions is worth more today than it would be if taken ten or twenty years in the future. This is the main reason businesses bother to use bonus depreciation.[10]

Evidence that Accelerated Depreciation Effectively Grows Our Economy Is Weak

While proponents claim that bonus depreciation would boost investment and thus economic growth, others are more skeptical. A report from the Congressional Research Service, summarizing efforts to quantify the impact of the provision, concludes that bonus depreciation “was a relatively ineffective tool for stimulating the U.S. economy during periods of weak or negative growth.”[11]

Proponents assert that accelerated depreciation increases investment. But Lily Batchelder points out that studies supporting this assertion may actually identify little more than timing shifts — businesses accelerate investments that were already planned, in order to take advantage of temporary depreciation breaks. She points out that when researchers examine the relationship between accelerated depreciation and permanent increases in investment, the results are mixed.[12]

In theory, temporary bonus depreciation provisions are supposed to at least provide this short-term effect, during the time businesses must take advantage of them before they expire. Permanent depreciation breaks are likely to have even less stimulative effect because businesses are in no rush to take advantage of them, as they do not expire.

Corporations Prefer Tax Breaks Investors Will Acknowledge

Why are depreciation breaks not more effective in encouraging investment that would not otherwise occur? Researchers have found a surprising answer. Jesse Edgerton of the National Bureau of Economic Research concluded in a 2012 paper that the financial accounting rules that determine what information is reported to the public (and thus to investors) ignore accelerated depreciation tax breaks, which in turn means that corporate managers have little incentive to pay attention to them.[13] Even if corporate managers can slash their company’s taxes dramatically by using depreciation breaks, they get no thanks from investors, who rely on information that makes no mention of these breaks.

It may seem difficult to believe that corporate managers ignore tax breaks that affect their bottom line. Don’t corporations act rationally to maximize profits? Aren’t investors sufficiently sophisticated to understand the taxes, and thus the after-tax profits, of companies? The answer to these questions is: Not always.

Lily Batchelder comes to the same conclusion. She explains that the problem has to do with the 10-K, the form that publicly traded corporations file annually with the Securities and Exchange Commission, which provides information so that investors and the rest of the public know how to evaluate the profitability of a given corporation. The information is presented in a way that encourages people to focus on a measure of tax liability that combines two very different concepts: “current taxes” which are paid in the year reported, and “deferred taxes,” which the corporation is obligated to pay but has not yet paid. Often these taxes are deferred through accelerated depreciation breaks, which allow a company to take deductions for the cost of equipment earlier than it otherwise would, resulting in lower taxes initially but higher taxes in the future.

Thinking of a company’s tax liability as including both its current taxes (taxes it actually paid in the year in question) and deferred taxes (taxes the company is supposed to pay someday) could make sense for certain accounting purposes. But it does not tell us what a company is paying in a given year, and it does not recognize the benefits the company receives from accelerated depreciation.

Batchelder points to survey data showing that if corporate managers consider taxes when making investment decisions or decisions about where to locate a facility, the vast majority of them focus on the statutory tax rate (which for corporations was 35 percent until TCJA reduced it to 21 percent) or they focus on the “book” tax rate, meaning the effective tax rate provided in the 10-K that combines “current” taxes (taxed paid in a given year) and deferred taxes (taxes not actually paid yet).

It would seem more rational for them to focus on the marginal tax rate, the fraction of each new dollar in profits that would be paid in taxes. But the survey data shows that just 13 percent focus on the marginal tax rate when making investment decisions and just 9 percent focus on marginal tax rates when deciding where to locate a facility.[14]

Batchelder begins her paper by saying that it “is motivated by conversations with dozens of CEOs, CFOs and tax directors of Fortune 100 companies during my time in government. When asked about their investment decision making processes, almost all of them said they account for taxes by focusing on the statutory (“headline”) tax rate or their financial accounting (“book”) tax rate—not something closer to the actual, discounted taxes that they expect to pay on returns on an investment.”

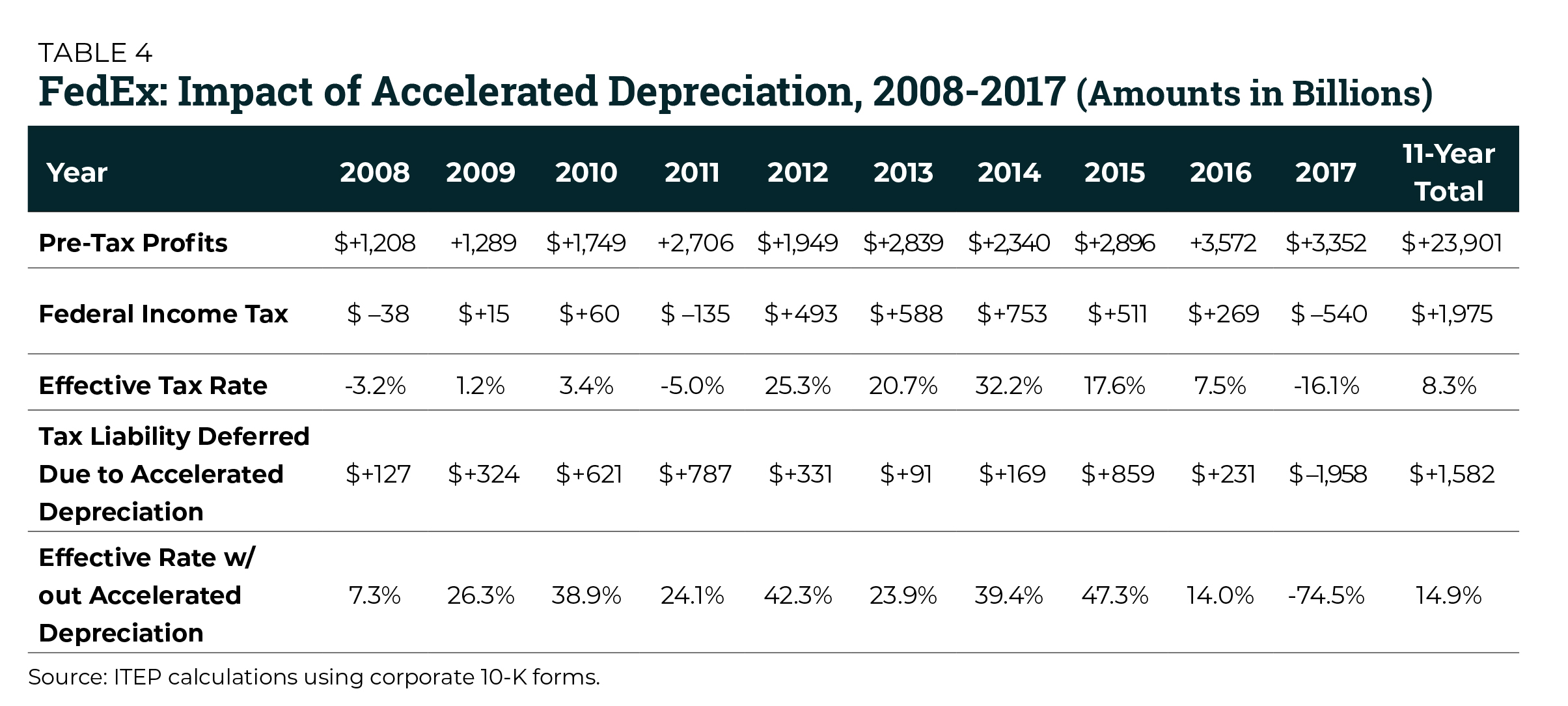

Indeed, corporate executives prefer lower tax rates, even when they are not paying taxes. In the summer of 2017, Congressional Republicans were struggling to figure out how to put together a tax plan that would lower the statutory corporate tax rate dramatically while also allowing full expensing. (One provision they hoped would replace some of the lost revenue, a border-adjusted tax, proved politically untenable.) The CEO of FedEx, Fred Smith, published his own tax reform plan to get past the logjam.[15] His plan kept the steep reduction in the statutory corporate tax rate but allowed expensing of just half of the costs of capital investments. When given the choice, the leadership of FedEx chose a lower statutory corporate tax rate over full expensing.

The real mystery is why the CEO of FedEx was promoting tax reform at all. The company was already paying very little in taxes. As illustrated in Table 4, FedEx reported about $2 billion in “current” federal corporate income taxes on roughly $24 billion of profits over the past decade in the 10-K forms it filed with the SEC. That comes to an effective tax rate of just 8.3 percent. One might think that the CEO of a company as large as FedEx would have better ways to spend his time than to promote reform of a tax that his company was already avoiding for the most part.[16]

But Fred Smith’s behavior makes a little more sense if investors give him no credit for using accelerated depreciation to avoid taxes. There are probably many different types of tax breaks that allowed FedEx to pay an effective tax rate that was much, much lower than the statutory tax rate of 35 percent in effect until 2018. One of those tax breaks was certainly accelerated depreciation.

Table 4 also illustrates the additional federal taxes FedEx would have paid each year if depreciation was not accelerated. It also shows that in this scenario, the company’s effective tax rate over the past decade would have been 14.9 percent. While this is not a particularly high tax rate, one can imagine corporate leaders trying to drive it down further. If investors do not appreciate how accelerated depreciation drives down the company’s tax rate, it makes sense that CEOs would prefer other types of tax breaks or a lower statutory tax rate instead.[17]

In the end, Congressional Republicans did not follow Smith’s suggestion. They provided both the dramatic reduction in the corporate tax rate and full expensing. The question of the law’s cost, to the extent that it was addressed at all, was given over to budget gimmicks. For example, the expensing provision was written as a temporary provision to help make the cost of the plan appear to stay below the target revenue cost Congress had set out for itself, even though supporters of the law have already stated that they would like to make the expensing provision permanent.

The Failure of Accelerated Depreciation

The entire theory behind accelerated deprecation provisions starts with the notion that corporate managers respond to these provisions in making their investment decisions. The evidence indicates that corporate managers actually pay little attention to these provisions but only claim these tax breaks for investments that they would have made anyway. As a result, hundreds of billions of dollars are lost each decade but there is little reason to believe that businesses have truly increased investment.

Even when these tax breaks are effective in changing the decisions of investors, it is not obvious that this is a good outcome. Accelerated depreciation is one of the ways that income from capital (mostly income of the rich) is taxed less than income from labor (more common among the non-rich). Also problematic is that these breaks can lead to tax shelters, investments that make no economic sense at all other than to take advantage of the mismatch between how our tax code treats investments and debt.

Congress can put an end to all of this. Instead of making the problem worse by extending the full expensing provision in TCJA beyond 2022, lawmakers should consider repealing it. They should go even further by repealing the permanent accelerated deprecation in our tax code, which they can accomplish by eliminating MACRS and requiring assets to be depreciated under ADS.

[1] The authors would like to thank Steven M. Rosenthal, Lily Batchelder, and David S. Miller for their comments and inspiration. Anything valuable in this report is due to them, any errors or misunderstandings are due to the authors.

[2] U.S. Senate Finance Committee Hearing to Consider the Nomination of Paul O’Neill, January 17, 2001. https://www.c-span.org/video/?c4686196/paul-oneill-tax-incentives

[3] In this example, the deduction of $10,000 in the first year allows the company to report a loss that year, which is assumed to generate tax savings because it can be used to offset other income of the company.

[4] For more explanation of this problem, see Deborah A. Geier, “Expensing and the Interest Deduction,” Tax Notes, September 17, 2007.

[5] For one thing, TCJA’s new limit on interest deductions does not bar companies using full expensing from deducting interest payments altogether. It limits those deductions to 30 percent of adjusted taxable income. Before 2022, the law defines adjusted taxable income as taxable income before interest, taxes, depreciation, and amortization are subtracted. From 2022 on, TCJA defines adjusted taxable income as a smaller number, which is taxable income before interest and taxes are subtracted (after depreciation and amortization are subtracted). This limit does not apply at all to companies with less than $25 million in gross revenue nor does it apply to some specific types of businesses (farms, real estate, certain types of energy).

[6] The Congressional Budget Office explains: “Most rates of depreciation in the tax code today were set in the Tax Reform Act of 1986 and, if the average rate of inflation since that time was 5.0 percent, they would approximate the rate of economic depreciation (the decline in an asset’s economic value, including the impact of inflation over time). The Congressional Budget Office estimates, however, that inflation over the next decade will average about 2.3 percent annually. That difference of nearly 3 percentage points means that, if those rates of depreciation stay the same, businesses will be able to deduct larger amounts of depreciation from taxable income—and thus have a lower tax liability—than they could if the deduction accurately measured economic depreciation.” See Congressional Budget Office, “Options for Reducing the Deficit: 2014 to 2023,” “Option 26: Extend the Period for Depreciating the Cost of Certain Investments,” November 13, 2013. https://www.cbo.gov/budget-options/2013/44848

[7] An explanation of this legislative history is provided by Gary Guenther, “The Section 179 and Section 168(k) Expensing Allowances: Current Law and Economic Effects,” Congressional Research Service, May 1, 2018. http://www.fas.org/sgp/crs/misc/RL31852.pdf

[8] Memorandum from Thomas A. Barthold, Director of the Joint Committee on Taxation, October 27, 2011. https://democrats-waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/media/pdf/112/JCTRevenueestimatesFinal.pdf

[9] See discussion in Chye-Ching Huang, Chuck Marr and Nathaniel Frentz, “Timing Gimicks Pose Threat to Fiscally Responsible Corporate Tax Reform,” January 13, 2014. https://www.cbpp.org/research/timing-gimmicks-pose-threat-to-fiscally-responsible-corporate-tax-reform?fa=view&id=3994

[10] On the other hand, it is possible that JCT and CBO somewhat overstate the revenue impacts. The next sections of this report explain that these provisions may not change business decisions but are claimed for investments that would have been made even in the absence of any such provisions. That would mean they have a significant revenue cost, but little or no effect on the economy. If JCT and CBO assumed that the amount of investment eligible for accelerated depreciation would increase significantly in response to these policies, they may have concluded that the revenue impacts were larger than is warranted.

[11] Guenther.

[12] Lily L. Batchelder, “Accounting for Behavioral Considerations in Business Tax Reform: The Case of Expensing,” draft, January 24, 2017, page 20. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2904885

[13] Jesse Edgerton, “Investment, Accounting, and the Salience of the Corporate Income Tax,” National Bureau of Economic Research, Working Paper 18472, October 2012. http://www.nber.org/papers/w18472

[14] Batchelder, page 17.

[15] Matthew Townsend, “Fed Up With Tax Stalemate, FedEx CEO Pushes Alternative Solution,” Bloomberg, June 27, 2017. https://www.bloomberg.com/news/articles/2017-06-27/fedex-ceo-pushes-alternative-tax-plan-after-washington-stalls

[16] Some observers debated whether technical issues with the 10-Ks made it difficult to rely on the current tax figure. But while the current tax number is rarely the exact amount companies end up paying to the IRS, the current tax measure does seem to closely track corporate taxes actually paid. In 2013, the General Accounting Office released a report using tax data to show how much profitable American corporations paid in taxes (as a group) and found that actual federal tax payments recorded in IRS data for a given year were very similar to the “current” federal taxes reported in the 10-Ks in the aggregate. See General Accounting Office, “Corporate Income Tax: Effective Tax Rates Can Differ Significantly from the Statutory Rate,” GAO-13-520, Jul 1, 2013. https://www.gao.gov/products/GAO-13-520

[17] Of course, the information available does not reveal the full impact of accelerated depreciation on FedEx. For one thing, the impact in any one year could be the net effect of accelerated depreciation from many previous years, in addition to accelerated depreciation for investments made in that particular year. Accelerated depreciation on investments will lead to tax reductions in some years and tax increases in later years when the deferred taxes come due, so that the estimated impact provided here is the sum of those effects each year. It shows that the net effect was to reduce FedEx’s taxes until 2017 when the previously deferred taxes coming due exceeded the new tax deferrals. The full expensing provision in TCJA will likely ensure that depreciation lowers the company’s taxes once again. The data available also do not tell us how FedEx benefits from deferring whatever tax it will pay. If we could imagine that FedEx only existed from 2008 through 2017, then we would see the total amount of taxes that the company paid over its lifetime and see how much it defers each year. The table would look something like the very simple examples provided earlier in this report. The ten-year total tax liability would be the same whether or not one takes into account deferral, but we would be able to calculate how much FedEx was able to boost the present value of its after-tax profits by deferring tax.