House Republicans recently voted to rescind the green energy and electric vehicle tax credits that were enacted last Congress as part of the Inflation Reduction Act (IRA). By the logic that Republican lawmakers have used in the past to oppose Biden’s corporate tax increases, this would amount to a direct tax increase on energy and automotive companies and an indirect tax increase on their employees and consumers. This newfound willingness to raise taxes stands in contrast to the recent position of almost the entire House Republican Caucus.

Public subsidies delivered through the tax code are known as “tax expenditures” in budget parlance, and the GOP is absolutely right that efforts to lower the national debt should include a critical review of activities receiving public tax support. But the tax code is flush with wasteful giveaways to corporations and the wealthy, so it is odd that House Republicans have zeroed in on eliminating credits that are driving a rush to build new factories and energy facilities in the United States.

If Congress wants to reduce costly tax expenditures, they would do well to look at the advantageous treatment of capital gains, which costs the government hundreds of billions every year and contributes to rising inequalities. Or they could pare back the 20 percent deduction for pass-through businesses, which is purported to help small businesses but in reality often flows to billionaires. There’s also the benefit for companies to offshore profits to tax havens.

Reforming these wasteful expenditures would provide ample funding for Congress to invest in children and low-income workers by expanding the Child Tax Credit and Earned Income Tax Credit.

The House debt plan is a reversal on tax reform.

Most House Republicans—including Speaker Kevin McCarthy and Rep. Jason Smith, the chair of the House’s main tax committee—have signed a pledge to not raise taxes under any circumstances without enacting offsetting tax cuts. And recently, GOP House leaders stated that President Biden’s proposal to lower the deficit was a non-starter because it included tax increases on people making over $400,000. Congressional Republicans also argue that corporate tax increases are tax hikes for individuals at all income levels who could be, in theory, indirectly affected by corporate tax changes.

This rigid anti-tax stance has always been incongruous with their posture as a party concerned with balanced budgets. The basic arithmetic behind the federal budget shows that tax increases are needed to bring the deficit back toward historical averages. And data shows that the ratio of public debt in the economy would have been stable over the 21st century if not for continual tax cuts.

House Republicans insist they are not making a reversal on their anti-tax hike position by voting to rescind the IRA tax credits because, in their mind, those credits effectively amount to government spending.

In fact, many tax benefits amount to subsidization of activities that Congress has deemed worthy of public support. Undoubtedly, Congress should periodically review which activities are receiving subsidies through the tax code. The President has often cited ITEP’s finding that many highly profitable corporations pay effective tax rates close to zero due to the innumerable subsidies written into the tax code. Last fall, we asked why companies making frozen breakfast foods and casino games were lobbying Congress to extend research tax breaks. (GOP lawmakers have recently announced a new proposal to extend the frozen sausage and slot machine subsidy.)

Congress should reform tax expenditures, which largely benefit the wealthy.

Subsidies delivered through the tax code have a technical term, “tax expenditures.” Every two years, the Joint Committee on Taxation—Congress’s nonpartisan revenue scorekeeper—estimates the revenue cost of these provisions.

The benefits from tax expenditures are distributed varyingly across different subsets of taxpayers. The Child Tax Credit, for example, flows to low- and middle-income families with children. When Congress temporarily expanded that credit in 2021, child poverty was cut in half. On the other hand, the benefits for capital gains and dividends primarily flow to wealthy investors—including many from out of the country.

Some expenditures—like the IRA credits for green energy and electric vehicles—encourage domestic manufacturing. Other expenditures instead allow companies to pay lower rates on foreign profits, encouraging multinationals to offshore their business activities to tax havens.

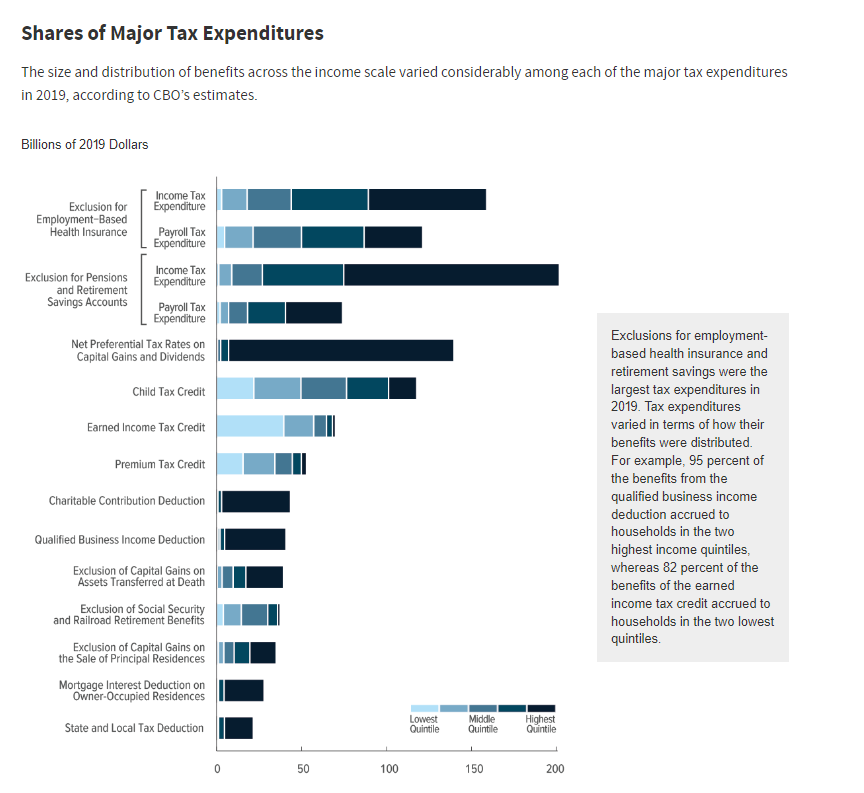

The Congressional Budget Office recently analyzed the effects of some of the largest federal tax expenditures in 2019 and found that taken as a group, they disproportionately favored the richest taxpayers. Seventy-five percent of the reduced capital gains rate and 50 percent of the pass-through business deduction went to the top 1 percent. The CBO report does not include corporate tax expenditures, which also largely benefit the richest taxpayers since the wealthy own much more corporate stock on average.

Image source: Congressional Budget Office

House Republicans were on the scent of a good idea when they started talking differently about tax expenditures. Unfortunately, their hunt fell short when they settled on simply repealing the IRA’s green credits. Reasonable people can debate whether to subsidize activities through the tax code. But at least these energy tax credits have a sensible goal and are driving domestic production, which cannot be said for many tax expenditures that are far more costly and which Congressional Republicans never question.