The Biden administration has already provided details on its corporate tax proposals and in the next couple of weeks is expected to propose tax changes for individuals. Meanwhile, congressional Democrats have some ideas of their own. What should we expect?

The Biden Campaign Tax Plan

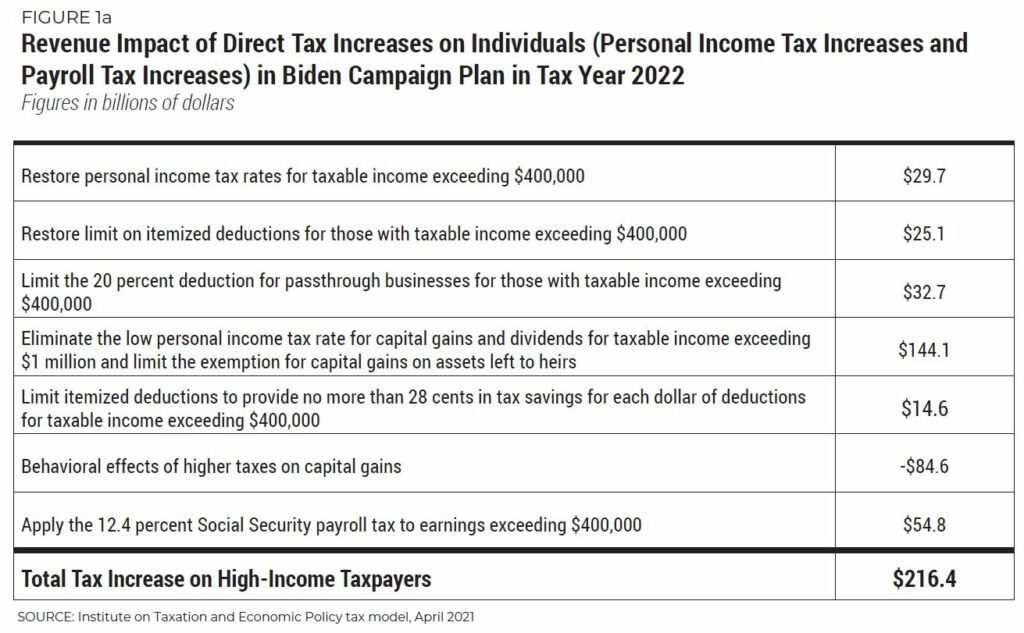

The best guide right now to the administration’s thinking is the tax increases for individuals that Biden proposed during his presidential campaign. Those proposals would only affect taxpayers with incomes of more than $400,000. Here are some basic findings from a newly updated analysis from ITEP.

- The personal income tax increases and payroll tax increase that Biden proposed on the campaign trail would affect 2 percent of taxpayers and raise $216 billion in tax year 2022.

- 97 percent of the combined personal income tax hikes and payroll tax hike would be paid by the richest 1 percent.

- The payroll tax increase in Biden’s campaign plan cannot be enacted through the reconciliation process that lawmakers may use to pass legislation.

- The personal income tax increases in Biden’s campaign plan on their own (without the payroll tax increase) would affect 1.9 percent of taxpayers and raise $162 billion in tax year 2022.

- 98 percent of the personal income tax hikes would be paid by the richest 1 percent.

ITEP’s analysis of Biden’s campaign plan has more details.

The Cap on Deductions for State and Local Taxes

The Trump tax law put a $10,000 cap on the amount of state and local taxes (SALT) taxpayers can deduct on their federal income tax returns.

While this policy seems to have been designed to target “blue states” with higher state and local taxes rather than for sound policy reasons, simply repealing the SALT cap, as some congressional Democrats have proposed, is problematic.

- If the tax proposals Biden offered during his campaign were amended to include repeal of the SALT cap, this would drain away around $100 billion of the revenue raised in tax year 2022.

- The richest 1 percent would receive more than 60 percent of the benefits of repealing the SALT cap, and the richest 5 percent would receive 85 percent of the benefits.

- Repealing the SALT cap combined with the Biden campaign proposals or in isolation essentially has the same revenue effects ($98 billion vs $101 billion) and essentially the same distributional effects.

- In every state and the District of Columbia, more than half of the benefits would go to the richest 5 percent of taxpayers.

- In all but four states, more than half of the benefits would go to the richest 1 percent.

Alternatives

There are potential alternatives that would raise as much or more than Biden proposes from those with incomes of more than $400,000 while also replacing the SALT cap with a different limit on tax breaks for the rich that does not target particular states.

- ITEP’s proposal for an alternative tax to replace the AMT and the SALT cap and only affect those with incomes of more than $400,000 would raise $317 billion in tax year 2022 compared to the $162 billion that Biden’s personal income tax proposals would raise that year.

- ITEP’s proposal would raise taxes on 1.5 percent of taxpayers in tax year 2022.

- This proposal would be simpler and raise more revenue than Biden’s campaign proposals but would be in keeping with his pledge to not raise taxes on anyone with income below $400,000.

ITEP’s report explaining this proposal has more details.

Other Tax Provisions for Individuals – the Child Tax Credit Expansion

While running for President, Biden proposed other tax changes for individuals besides tax hikes. For example, he proposed to expand the Child Tax Credit (CTC) in a way that was eventually enacted, for one year only, as part of the American Rescue Plan Act.

Some lawmakers propose to make the CTC expansion permanent or at least extend it beyond 2021.

- The CTC expansion removes the limits on refundability (a lower dollar cap on the refundable portion of the credit and a rule limiting the refundable portion to a percentage of earnings above a certain threshold). The limits on refundability prevent nearly all low-income families with children from receiving the full credit.

- The CTC expansion also increased the maximum credit from $2,000 per child to $3,000 for each child age 6 and older and $3,600 for each child younger than age 6.

- If Congress extends the CTC expansion or makes it permanent, roughly 90 percent of children in the United States would benefit in 2022.

Download ITEP’s national and state-by-state estimates of effects of CTC expansion in 2022.