Congress is considering legislative changes that would increase federal corporate income taxes partly by closing or limiting the special breaks and loopholes that companies use to avoid taxes. The following explains flaws in the federal corporate income tax that Congress should address.

Corporate tax avoidance mainly benefits wealthy Americans and foreign investors who own most of the shares in American corporations. When corporations pay lower taxes, these shareholders receive larger dividends from their stocks and obtain larger gains when they sell their stocks.

It is reasonable for corporations (and, indirectly, their shareholders) to pay taxes to support the government investments that make their profits possible, such as the highways that facilitate the movement of goods and people, the education and health care systems that provide a productive workforce, the legal system and the protection of property, all of which are vital to commerce. Corporate tax avoidance allows wealthy and powerful individuals to reap enormous benefits from these investments without contributing their fair share to support them.

Current tax laws allow corporations to shift billions of dollars into offshore tax havens.

The nation’s current international corporate tax laws have significant loopholes allowing corporations to shift profits into offshore tax havens. Specifically, American corporations use accounting gimmicks to make profits earned in the United States or in other countries where they do business appear to be earned in tax havens, which are countries that have no corporate tax or a corporate tax with a very low rate and ample loopholes.

It is easy to demonstrate that this is happening. Figure 1 illustrates the profits that American corporations claimed to earn in 2018 through their offshore subsidiaries in 15 countries where these claims seem suspicious or, in some cases, impossible.

For example, in 2018 American corporations reported $97 billion in profits in Bermuda, a small island nation with a gross domestic product (GDP) of $7 billion that year. In other words, U.S. multinational corporations claimed to earn more than 13 times the GDP of Bermuda in Bermuda in 2018. These absurd numbers cannot be explained by large numbers of employees in Bermuda producing goods or providing services either. U.S.-based companies reported just 740 employees in Bermuda in 2018, meaning the average Bermudan worker would have produced an astounding $131 million in profit for their American employers if these corporate reports truly reflected reality.

All six of the top tax havens in 2018 were either British Overseas Territories or Crown Dependencies. Amazingly, American companies claimed to earn $204 billion in combined profits in these tiny jurisdictions, more than two and a half times as much as they earned in the United Kingdom. For reference, these jurisdictions had a combined GDP of $30 billion in 2018, compared to United Kingdom’s GDP of $2.9 trillion.[1]

Offshore profit-shifting by corporations was a problem under the old tax system and remains a problem under the system created by the 2017 Tax Cuts and Jobs Act (TCJA). Current rules do not tax offshore profits of American corporations unless they exceed a 10 percent return on tangible investments (like machinery and equipment) they hold offshore.[2] When offshore profits are taxed, they are effectively subject to a tax rate of 10.5 percent, which is half the 21 percent rate that the United States imposes on domestic profits. Yet another problem is that rules are applied to each corporation’s profits on a global basis, rather than a per-country basis, which makes it easier for companies to use the excess taxes they pay in one country to offset the U.S. taxes they would otherwise pay on profits in tax havens.

The United States collects relatively little in corporate income taxes.

Before Congress reduced the statutory corporate tax rate from 35 percent to 21 percent as part of the TCJA, corporate spokespersons often complained that the statutory rate was higher than that of many other countries. But even then, American corporations paid an effective tax rate (taxes as a share of profits) that was far lower than they admitted.

Offshore profit-shifting was a reason for this, but not the only one. Prior to the 2017 tax law and after, American businesses have benefited from a slew of tax provisions that reduce their effective tax rate. Depreciation breaks, stock option deductions, research and investment credits, and more allow corporations to substantially reduce their taxable income or to directly reduce their taxes owed. A 2014 study of international tax rate measures from the Congressional Research Service found that, while the United States had a higher top statutory corporate tax rate than many of its peers, the rate that corporations paid was in line with that of other large, competitive economies.[3]

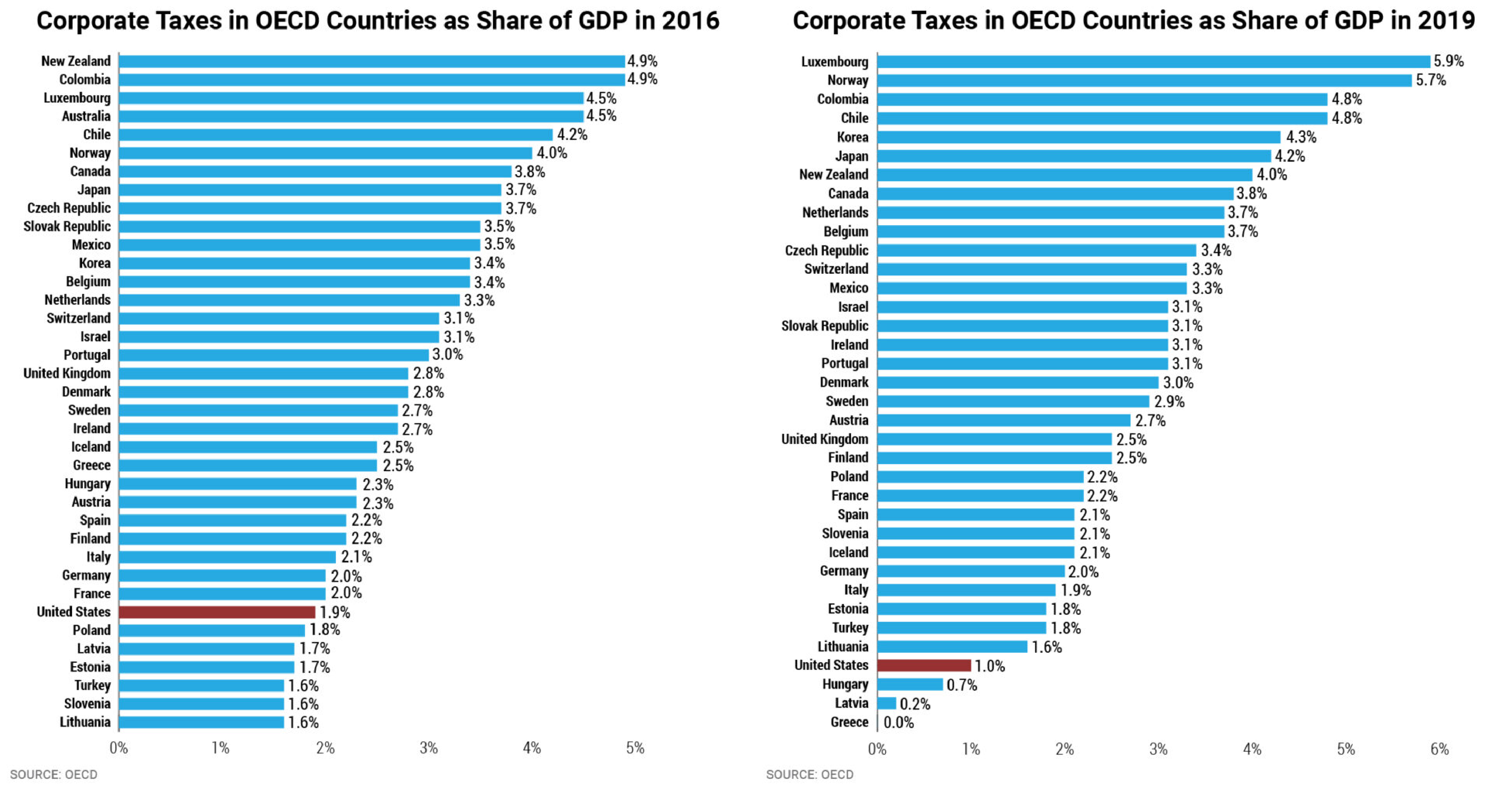

Another way to compare the tax liabilities of corporations from one country to the next is to examine corporate tax revenues as a share of economic output. Given that a significant portion of the world’s largest corporations are based in the United States and supposedly had a burdensome corporate tax rate prior to the TCJA, one might expect the United States to have had a much higher ratio of corporate tax revenue to economic output than its peers. In fact, the opposite is true, as illustrated in Figure 3.

Figure 3: Corporate Taxes as a Share of Gross Domestic Product

Corporate taxes accounted for just 1.9 percent of GDP in 2016, the seventh lowest among OECD countries and lowest of all major economies. Post-TCJA, that rate has fallen even lower. In 2019, corporate taxes comprised just 1 percent of GDP, with only Hungary, Latvia, and Greece having lower rates among OECD countries.

Many U.S. corporations avoid all or most of the federal corporate income tax.

Some corporations entirely avoid the corporate income tax. In April, ITEP published a report identifying 55 corporations that were profitable in the United States in 2020 but did not pay any current federal income taxes that year. This finding caused widespread outrage and has been cited multiple times by President Biden and multiple members of Congress.

But the corporate tax avoidance that occurred in 2020 was not unusual. In July, ITEP published another report identifying 39 corporations that were profitable in each year from 2018 through 2020 (the first three years that the TCJA was in effect) and paid no federal income tax on average over those three years.

As illustrated in Figure 4 below, these 39 corporations collectively had a federal income tax liability of negative $4.2 billion during that period, meaning they collectively received $4.2 billion in refunds from the IRS for taxes paid in previous years.

The federal statutory income tax rate for corporations established in the TCJA is 21 percent. But many corporations clearly pay nothing, and most pay far less than 21 percent of their profits in federal income taxes.

ITEP’s July report identified 73 corporations that were profitable each year from 2018 through 2020 but paid an effective federal income tax rate that was greater than zero, but less than half of the statutory tax rate of 21 percent. These 73 corporations include many household names such as Amazon, Bank of America, Deere, Domino’s Pizza, Etsy, General Motors, Honeywell, Molson Coors, Motorola, Netflix, Nike, Verizon, Walt Disney, Whirlpool and Xerox—which all paid effective federal income tax rates in the single digits.

As illustrated in Figure 4, these 73 corporations collectively paid an effective federal income tax rate of just 5.3 percent on $430 billion of profits during those years.

President Biden’s proposals will not make U.S. corporations less competitive.

There is no evidence that our pre-TCJA corporate tax system made American corporations uncompetitive, and there is no evidence that the TCJA made them more competitive.

The United States accounts for just over 4 percent of the world’s population and a quarter of global GDP, but American corporations account for 40 percent of the market value and a third of the sales of the Forbes Global 2000, which is an annual list that measures the largest businesses in the world based on sales, profits, assets, and market value. These figures were essentially the same in 2017, before the TCJA was enacted, and in 2020, as illustrated in Figure 5 below.[4]

The data show that prior to the TCJA’s reduction in corporate tax rates, U.S. corporations had a massive competitive advantage in the global economy. That advantage remains virtually unchanged, even though the TCJA was ostensibly supposed to make American companies more competitive. If anything, President Biden’s overall tax and investment plan would make our economy more competitive because it includes infrastructure improvements and other investments that will make it easier for companies to produce profits in the United States.

In 2017, Professor Kim Clausing (now Treasury Deputy Assistant Secretary for Tax Analysis) argued that elements other than tax competitiveness were equally important in attracting investment from multi-national corporations.[5] Income per capita, a well-educated workforce, good governance, and access to market were all significant factors for attracting large, successful businesses. President Biden’s tax and investment plan would further increase the competitiveness of American companies by using desperately needed revenues to increase income for workers, invest in education, improve infrastructure, and protect natural resources.

U.S. multinational corporations will pay lower effective tax rates than competitors from abroad even if Congress raises taxes.

Even if higher taxes made corporations less competitive, the United States is nowhere near reaching the point where that could happen.

According to Congress’s official revenue-estimators at the Joint Committee on Taxation (JCT), the average effective U.S. federal income tax rate paid by American corporations in 2018 was 7.8 percent. Their worldwide effective income tax rate, which includes taxes paid to the United States and to other countries, was 8.8 percent. Multinational corporations based in the countries that are among the nation’s top ten trading partners paid a much higher average effective rate, 18.1 percent.

An analysis published by Reuters finds that even if all of President Biden’s tax proposals are enacted, American multinational corporations will still pay effective rates that are lower than foreign companies they compete with.

President Biden’s tax plan will solve many problems with federal corporate income tax.

The Biden administration has proposed to increase federal corporate income tax revenue in several ways.

First, the administration proposes to raise the statutory corporate tax rate from 21 percent to 28 percent (well below the 35 percent rate that applied before the TCJA was enacted).

Second, and most importantly, the administration proposes to change the rules that currently tax the foreign profits of American corporations more lightly than their domestic profits.

For example, the President’s plan would repeal the rule exempting offshore profits up to an amount equaling a 10 percent return on foreign investment. This means that all foreign profits of American corporations would be subject to U.S. taxes if they are not taxed by foreign governments.

The federal income tax rate on the offshore profits of American corporations would be 21 percent rather than the 10.5 percent that applies today. This would narrow (but not fully eliminate) the gap between rates for domestic profits and offshore profits. Companies would still receive credits against their U.S. federal income taxes for income taxes they pay to foreign governments, to prevent double taxation.

With these changes in place, corporations would no longer benefit from accounting gimmicks that make their profits appear to be earned in countries that impose little or no tax liability on them. The total taxes paid on offshore profits (including U.S. taxes and foreign taxes) will always come to at least 21 percent.

The rules would be applied to each corporation’s profits on a per-country, rather than a global basis, meaning companies could no longer use the excess taxes they pay in one country to offset the U.S. taxes they otherwise pay on profits in tax havens.

Third, the President’s plan would limit tax breaks for domestic corporate profits, albeit indirectly. The President does not propose to directly change provisions related to accelerated depreciation, stock options and other domestic tax breaks. But he would limit their effect with a minimum tax equal to 15 percent of corporations’ “book” income, meaning the profits they report to the public and to investors. Corporations would pay whichever is more, their tax liability under the regular corporate tax rules or 15 percent of their book profits.

Congress should not pass up this opportunity

Corporations use special breaks and loopholes to avoid paying taxes that support the society that makes their profits possible. Some avoid paying a dime in taxes despite earning millions or billions in profits. They claim to earn profits in small European and Caribbean nations with few consumers or employees, then argue that their tax bills should be slashed even lower for the United States to remain competitive.

The Tax Cuts and Jobs Act failed to fix these problems and in some ways made the situation worse. Congress now has a historic opportunity to fix the problems created in 2017 and to go even further to make sure that corporations are paying their slice of the bill.

[1] These territories are valued as tax havens for low tax rates, low transparency, amenability to income shifting, and ties to the British legal and financial systems. Profiles of each country's scope for tax abuse are compiled annually in the Tax Justice Network's Corporate Tax Haven Index. https://cthi.taxjustice.net/en/cthi/profiles

[2] In other words, under TCJA, an American corporation generally does not pay U.S. federal income taxes on offshore profits if those profits equal less than a tenth of the amount the company has invested in tangible assets (assets like machines, factories, office buildings) offshore. If a U.S. multinational has invested $10 billion in tangible assets offshore and in a given year generates $2 billion through its offshore subsidiaries, just $1 billion of that amount will be subject to U.S. federal income taxes. (And that $1 billion will be taxed at half of the rate that applies to domestic U.S. profits.)

[3] Jane G. Gravelle, ”International Corporate Tax Rate Comparisons and Policy Implications,” Congressional Research Service, January 6, 2014. https://crsreports.congress.gov/product/pdf/R/R41743

[4] 2017 data is reported in the 2018 edition of the Forbes Global 2000. 2020 data is reported in the 2021 edition of the Forbes Global 2000.

[5] Clausing, Kimberly A., “Does Tax Drive the Headquarters Locations of the World's Biggest Companies?” August 14, 2018. https://unctad.org/system/files/official-document/diae2018d4a4.pdf