What Are Estate and Inheritance Taxes?

Estate and inheritance taxes are taxes on wealth passed on after someone’s death.

They are a common way for states to tax the inheritances of wealthy individuals. These taxes ensure that those very large estates help pay for public services like schools, hospitals, and parks.

While all 50 states once had estate taxes, only about one-third do today. They mainly affect wealthy people. Since other state and local taxes tend to be regressive, estate and inheritance taxes make tax systems fairer.

Who Pays Estate and Inheritance Taxes

Why Only a Small Share of Estates Pay These Taxes

State estate and inheritance taxes bring in billions of dollars annually for public services. Most of that comes from a relatively small number of very large estates. In fact, the overwhelming majority of estates, sometimes 99 percent or more, pay nothing at all. The reason states can raise so much money from a tax levied on so few households is that the households that are taxed are very, very wealthy. More than one in four dollars of wealth in the U.S. is held by the tiny fraction of households with net worth over $30 million. So, the tax generates a relatively large amount of revenue considering how few families are affected.

State estate and inheritance taxes bring in billions of dollars annually for public services. Most of that comes from a relatively small number of very large estates. In fact, the overwhelming majority of estates, sometimes 99 percent or more, pay nothing at all. The reason states can raise so much money from a tax levied on so few households is that the households that are taxed are very, very wealthy. More than one in four dollars of wealth in the U.S. is held by the tiny fraction of households with net worth over $30 million. So, the tax generates a relatively large amount of revenue considering how few families are affected.

How Estate and Inheritance Taxes Work

Estate Tax Exemptions and Thresholds

If an estate is worth less than a certain amount, it is automatically exempt. The exemption amount varies by state, from $1 million in Oregon up to $13 million in Connecticut in 2024. Larger estates are taxed only on the amount above the exemption. They can further reduce their tax with additional deductions for expenses, debts, and donations, and because the basic exemption is effectively doubled for married couples.

Estate Tax Rates and Deductions

After applying the exemption and deductions, a graduated tax rate — typically capped at 16 percent — is applied to the remaining value. Vanishingly few family farms and small businesses pay estate taxes because of the high exemption levels and deductions. The few that would still be subject to tax often owe little or nothing because of additional tax breaks targeted specifically at the wealthiest of small business and farm owners.

How Inheritance Taxes Differ from Estate Taxes

A few states have inheritance taxes, which work differently. Instead of the estate paying the tax before assets are distributed, the recipients (heirs) pay it. Rates and exemptions for inheritance taxes tend to be lower than for estate taxes, so more of the income is taxable, but at lower rates than under the estate tax. Rates and exemptions may also vary based on the relationship of the heir to the deceased.

For both inheritance and estate taxes, the tax is collected by the state where the decedent was living.

How changes in federal law have affected state estate taxes

The Federal “Pick-Up Credit” and Its Repeal

Fewer states have estate and inheritance taxes than in the past. The reason is that federal law has changed. Before 2001, every state had an estate tax based on a federal provision known as the “pick-up credit.” This credit allowed estates to reduce their federal tax bills by each dollar they paid in state tax. However, a series of federal tax changes starting in 2001 replaced the credit with a deduction. You can deduct your state estate tax from the total value of your estate, just as you can deduct donations and certain other items, but you no longer get a credit. Since many states’ estate taxes were tied explicitly to the credit, they were automatically repealed.

How States Responded to the Federal Estate Tax Changes

In the aftermath of the federal pick-up credit’s repeal, about one-third of states took steps to preserve their estate tax. This happened in two ways. Some states “decoupled” from the federal estate tax cut, effectively tying their own estate tax to the pick-up tax credit as it existed in 2001 prior to the repeal. Other states enacted their own separate taxes. Either approach avoided giving very wealthy families a new state tax break.

Although payers of state estate tax no longer receive a credit against their federal taxes paid, they can still claim it as a deduction. That means that, since the top federal estate tax rate is 40 percent, every dollar paid in state estate taxes results in up to 40-cent reduction in federal estate tax. In effect, the federal government subsidizes up to two-fifths of the revenue from state estate taxes.

Do Estate Taxes Cause Wealthy Residents to Leave?

At the time of federal credit repeal, some state policymakers expressed concern that preserving estate taxes would be counterproductive. They feared so many wealthy people would leave their state that it would wipe out gains from the tax. As it turns out, keeping the estate tax has paid off for states. Most ultra-rich households are remaining in state and paying the tax, so state revenues from estate and inheritance taxes are rising rather than falling.

Related Entries

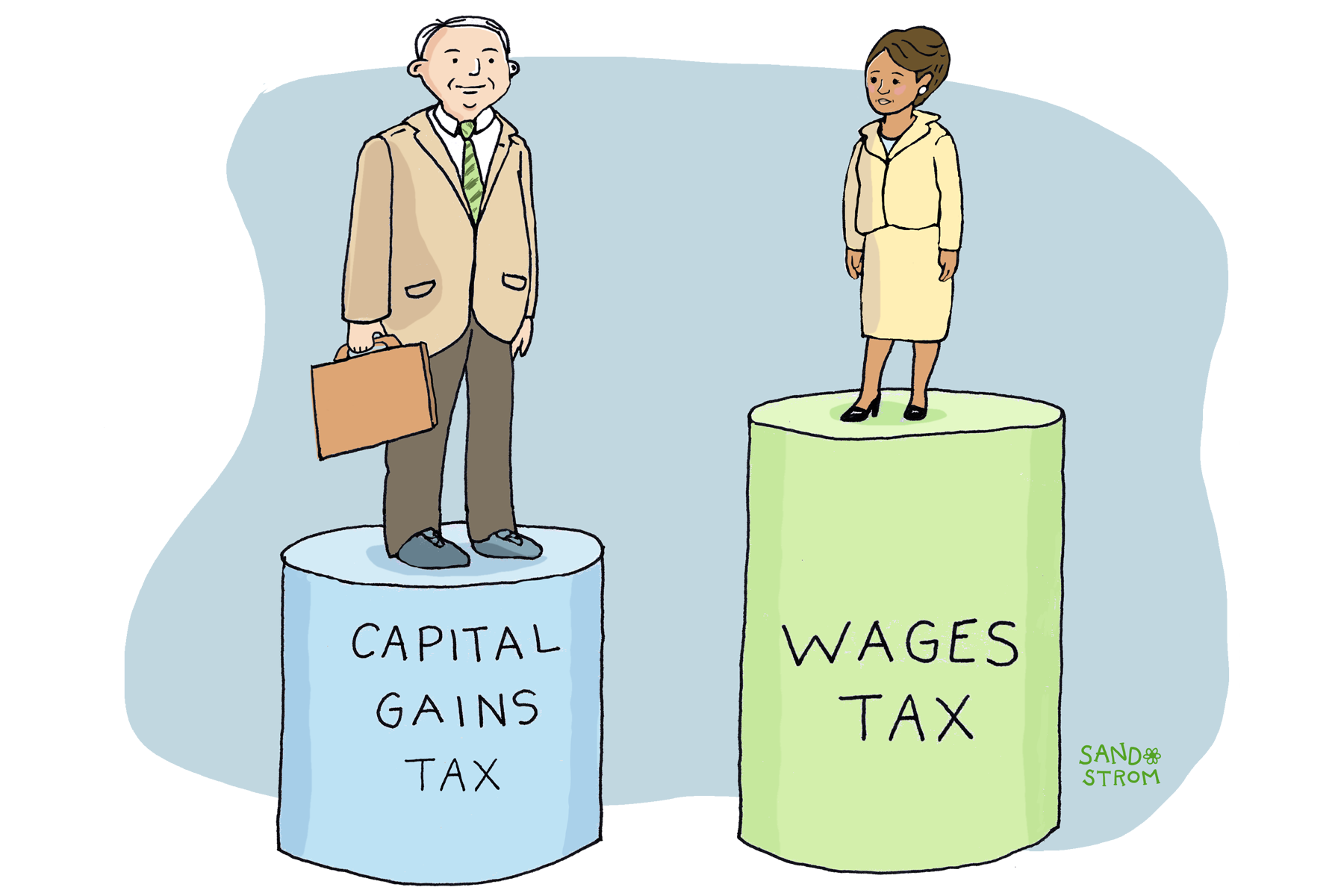

How Do States Tax Investment Income?

State personal income taxes apply not just to wages and salaries but also earnings on investments, like stocks and bonds. Most investments are held by wealthy people, so when states tax investment income at a lower rate than wages, high-income households pay tax at lower rates than middle-income households.

How Do State and Local Tax Policies Advance or Hinder Racial Justice?

State and local tax codes have the potential to either narrow or widen racial inequality created by historical and current injustices in public policy and in broader society. In general, tax codes that are more progressive across the economic spectrum do more to narrow racial inequality, while regressive tax policies exacerbate it.

Do State and Local Tax Cuts Fuel Growth?

Tax policy is an important economic tool but claims that tax changes will affect a state’s economy are often overstated. Such overstated claims are particularly common for taxes on wealthy individuals and profitable corporations, so careful assessment of such claims can help protect revenue streams and reduce regressivity.

Learn More

- Davis, Carl, Emma Sifre and Spandan Marasini (2022). “Extreme Wealth by State.” ITEP.

- McNichol, Elizabeth, and Samantha Waxman (2021). “State Taxes on Inherited Wealth.” Center on Budget & Policy Priorities.