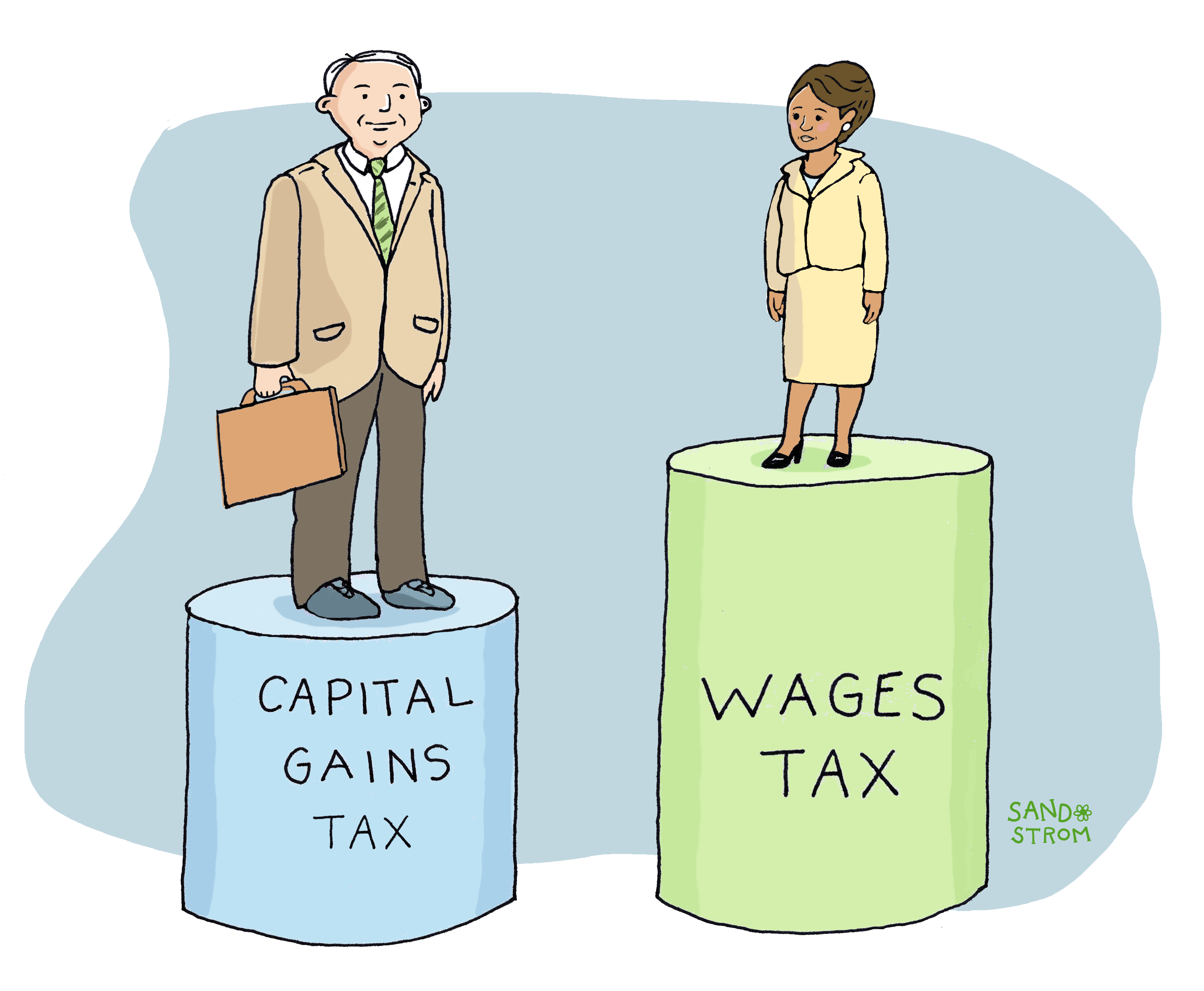

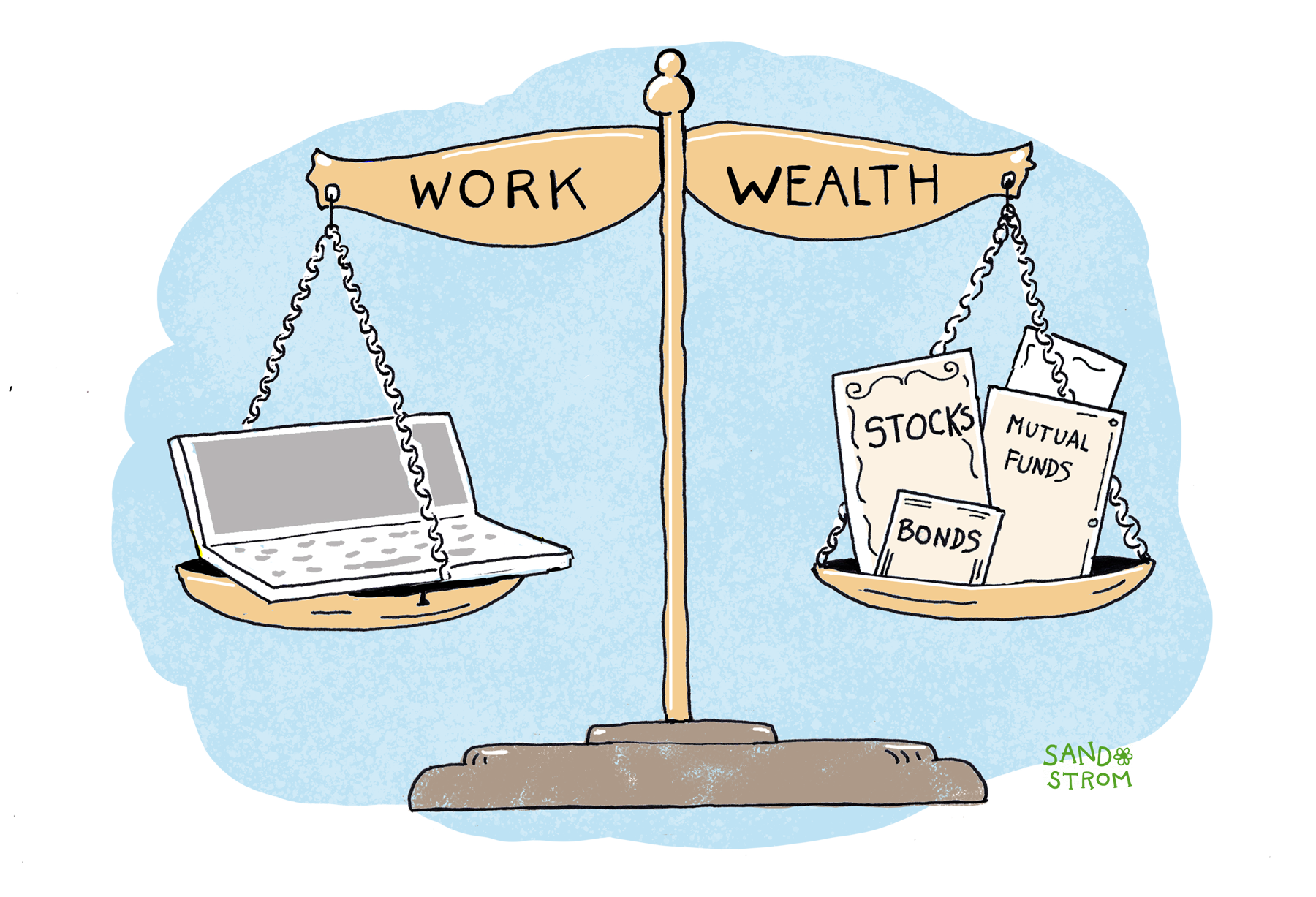

State personal income taxes apply not just to wages and salaries but also earnings on investments, like stocks and bonds.

Most investments are held by wealthy people, so when states tax investment income at a lower rate than wages, high-income households pay tax at lower rates than middle-income households. By contrast, states that strengthen taxation of investment income can raise substantial revenue while improving economic and racial equity of their tax code.

What Is Investment Income?

Investment income is income derived from assets rather than from wages and salaries.

What Counts as Investment Income?

- Capital gains, that is, profits from the sale of assets such as stocks, bonds, real estate, artwork, and antiques;

- Dividends distributed or allocated to shareholders;

- Interest payments on bank account balances, treasury and corporate bonds, certificates of deposit, and money market accounts;

- Rents derived from leasing real estate and other tangible property; and

- Royalties from allowing someone to use a copyright, patent, or mineral rights.

Investment income is considered a form of “passive income,” a term that also can also include the profits of a pass-through entity that some investors receive from businesses that they own but don’t actually work at.

A Lot of Income from Wealth is Untaxed or Undertaxed

In 2012, billionaire investor Warren Buffett famously disclosed he paid taxes at less than half the rate of his secretary. Subsequent research showed he wasn’t unique. Special tax breaks – both those enacted at the federal level and others added by states – cause investment income to be taxed less than income from wages, especially for the very wealthy.

For example, when the value of assets like stocks and bonds grows, economists consider that income. But federal tax law only applies when an asset is sold. If it is sold during the investor’s lifetime, the taxable capital gain is calculated as the difference between the original buying price (known as the basis) and the selling price. That means investors can defer tax for years or even decades. In the meantime, investors can benefit from the untaxed gains by borrowing against the investment. And they can invest the money they would have paid in taxes, yielding even more income.

In fact, if an investor holds onto an asset until death, the capital gain is never taxed. That’s because federal law provides for the basis to be reset (“stepped up”) to the current market value of the asset. The heir pays capital gains only on the growth above this stepped-up basis, completely erasing tax liability on the wealth gained between the date the original investor bought the asset and when they passed it on.

Capital gains deferral and stepped-up basis are two of the biggest federal tax breaks for investors, but there are others. For example, investors benefit from tax-deferred savings accounts, like Roth IRAs. Some wealthy investors have tens or even hundreds of millions of dollars that are growing in value tax-free in Roth IRAs. Special trust rules can also shield fortunes from taxation.

The result of these various tax breaks is that significant amounts of the profit that wealthy households earn from their investments goes untaxed under federal tax law.

Most states follow the federal tax rules, so these special rules for investors show up in state taxes too. And some states have additional breaks for investment income, such as lower rates, exemptions for income from dividends and capital gains, or tax breaks for wealthy retirees.

A more subtle way that states exempt investment income is by imposing payroll taxes to fund social insurance programs like unemployment insurance (UI) and family leave, or to generate general funds. These payroll taxes typically apply to earned income, but not to investment income.

Tax Breaks for Investment Income Favor Wealthy Households

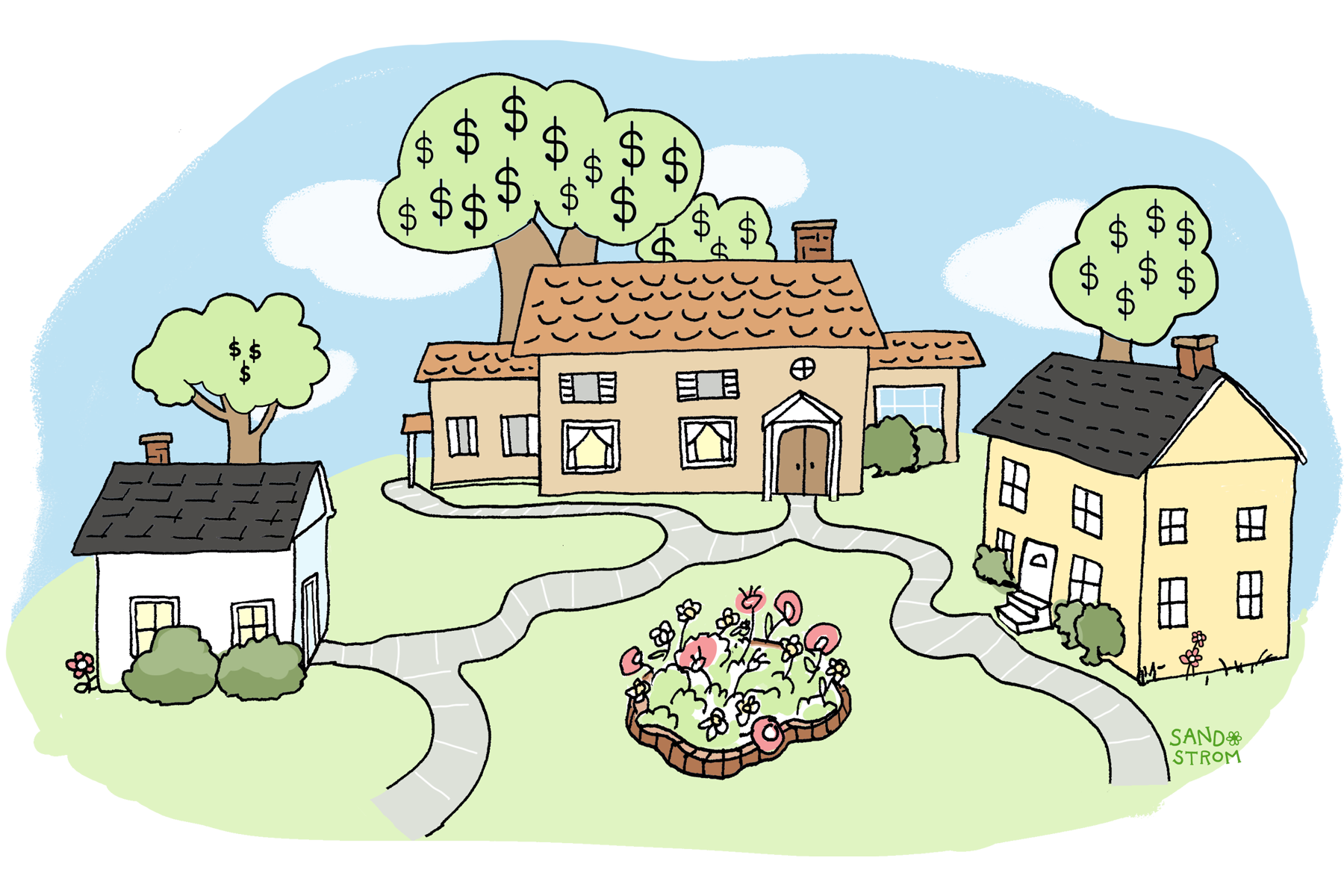

Tax breaks for investment income mostly benefit a small number of wealthy, overwhelmingly white households. In 2022, the richest 10 percent of U.S. households controlled 73 percent of the nation’s wealth, and the top 1 percent alone held 35 percent. Most of this wealth was held in the form of stocks, bonds, and other income-generating wealth. So when states under-tax investment income relative to wages, most of the benefits accrue to the wealthiest households.

Middle- and low-income households, including the great majority of white and Asian-American households and nearly all Black and Hispanic households, receive very little benefit from investment tax breaks. Black and Hispanic families, who respectively represent 14.2 and 9.6 percent of households, each own about 5 percent of real estate holdings, less than 2 percent of private business wealth, and about 1 percent of corporate equities and mutual fund shares.

How States Can Tax Investment Income More Fairly

States can avoid reinforcing federal tax preferences for investment income, achieve a better balance between investment and labor income, and raise new revenue for public services by targeting investment income. For example, Minnesota has a Net Investment Tax that applies only to passive income of high-income households, and Maryland has enacted a capital gains surcharge.

The various tax breaks for income from wealth at the state and federal level offer ample opportunities for more progressive taxation of income from wealth in states wishing to raise revenues while balancing tax fairness. Today’s tax break could be tomorrow’s revenue raiser.

Related Entries

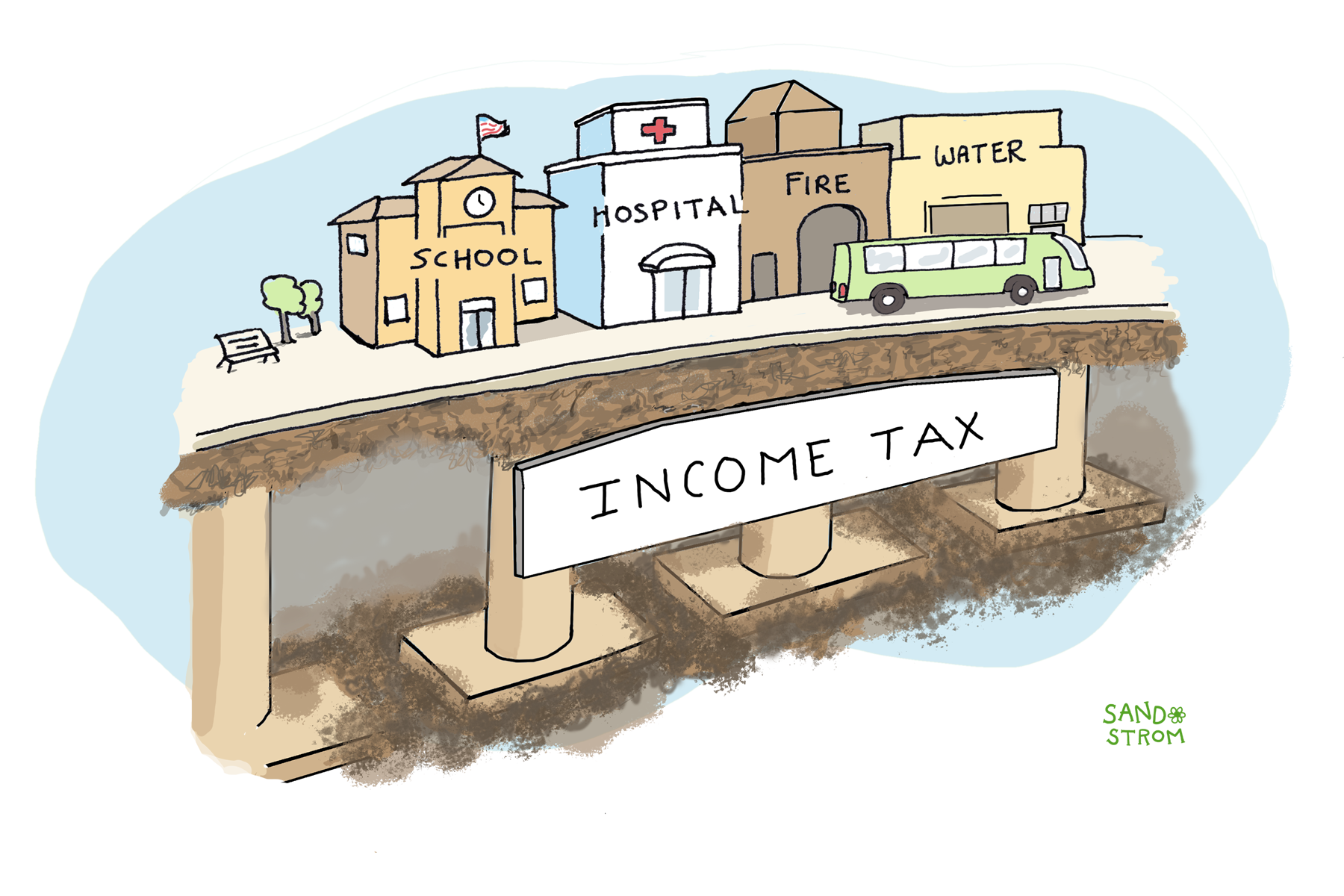

How Do State and Local Personal Income Taxes Work?

The personal income tax funds public education, health care, public safety, and other public services provided by state and local governments. If well-designed, it is the fairest major revenue source available to states.

How Do Estate and Inheritance Taxes Work?

Estate and inheritance taxes are taxes on wealth passed on after someone’s death. They are a common way for states to tax the inheritances of wealthy individuals. These taxes ensure that those very large estates help pay for public services like schools, hospitals, and parks.

How Do Real Property Taxes Work?

The great majority of property tax revenue is based on the value of land and buildings, but states also apply property taxes to certain business equipment, machinery, and supplies, and sometimes also to automobiles. Collectively these taxes are known as “personal property taxes.”

Learn More

- Davis, Carl, and Marco Guzman (2021). “State Income Taxes and Racial Equity: Narrowing Racial Income and Wealth Gaps with State Personal Income Taxes.” ITEP.

- Elliott, Justin, James Bandler and Patricia Callahan. “The Number of People With IRAs Worth $5 Million or More Has Tripled, Congress Says.” ProPublica, July 2021.

- Institute on Taxation and Economic Policy. Who Pays? A Distributional Analysis of the Tax Systems in All 50 States. Seventh Edition, 2024. National Economic Council. “The Buffett Rule: A Basic Principle of Tax Fairness.” April 2012.