By Carl Davis and Mike Hegeman

The cannabis industry has come a long way since the first legal sale of adult-use cannabis eight years ago in Colorado. In 2021, the 11 states that allowed legal sales within their borders raised nearly $3 billion in cannabis excise tax revenue, an increase of 33 percent compared to a year earlier. While the tax remains a small part of state budgets, it’s beginning to eclipse other “sin taxes” that states have long had on the books. Most of the states that allowed cannabis sales last year raised more revenue from cannabis excise taxes than from alcohol excise taxes and profits (in the case of state-run liquor stores). In total, cannabis revenues outperformed alcohol by 20 percent by this measure.

Colorado stands out among this group with cannabis taxes raising seven times more than its excise taxes on alcohol. Not coincidentally, Colorado also has among the lowest alcohol tax rates in the nation. Alcohol excise taxes in Colorado are 2.7 cents per shot of liquor, 1.3 cents per glass of wine, or 1 cent per pint of beer and raised a combined total of $53 million last year. Colorado’s cannabis taxes are levied at higher rates per serving (a 5-milligram edible might incur around 16 cents of state tax, for example) and raised $396 million. While Colorado represents a relatively extreme case, low alcohol tax rates are the norm across much of the country as their real value has been eroded substantially by years of inflation and policy inaction.

But cannabis isn’t always the most lucrative “sin tax.” Last year, four of the 11 states that allowed for legal cannabis sales raised more revenue from alcohol. This includes Alaska, which has a higher alcohol tax rate than most states (15 cents per shot of liquor, for example), as well as three "control states” that generate profit directly at state-run liquor stores: Maine, Michigan, and Oregon. Moreover, because the alcohol industry is significantly larger than the legal cannabis industry, its overall tax contribution from general sales taxes, fees, various local taxes, and other levies surely surpasses that from cannabis. Nonetheless, it is remarkable that in the span of just a few years, the narrow “sin taxes” that states created to apply to cannabis purchases have managed to surpass the comparable taxes that have long applied to alcohol.

Both alcohol and cannabis revenues are usually overshadowed by tobacco which, for the time being, is the top “sin tax” revenue source in states. State-level excise taxes on tobacco range from 9 to 18 cents per cigarette in the states with legal cannabis sales discussed in this article. Across these states, tobacco excise taxes raised almost twice as much ($5.9 billion) as cannabis taxes. How much longer this pattern will hold is difficult to predict because cannabis and tobacco revenues are on very different trajectories.

In the wake of cannabis legalization, revenue has tended to start low but grow quickly as legal businesses ramp up production and sales. Tobacco tax revenue, on the other hand, is stagnating or declining in many states because tobacco usage is declining. The share of U.S. adults who smoke cigarettes has fallen by 40 percent in the span of just 15 years. Some recent increases in state tobacco taxes have helped to shore up tobacco tax revenues, but it remains clear that cannabis taxes are generally growing faster than tobacco taxes.

Already, the two states with the oldest and most developed legal cannabis markets have seen their cannabis tax haul surpass their tobacco tax revenues: cannabis revenue outperformed tobacco by 17 percent in Colorado and 44 percent in Washington State last year. The same may happen for other states. Nevada’s cannabis tax revenues, for example, are quickly approaching the revenue total raised through tobacco taxes.

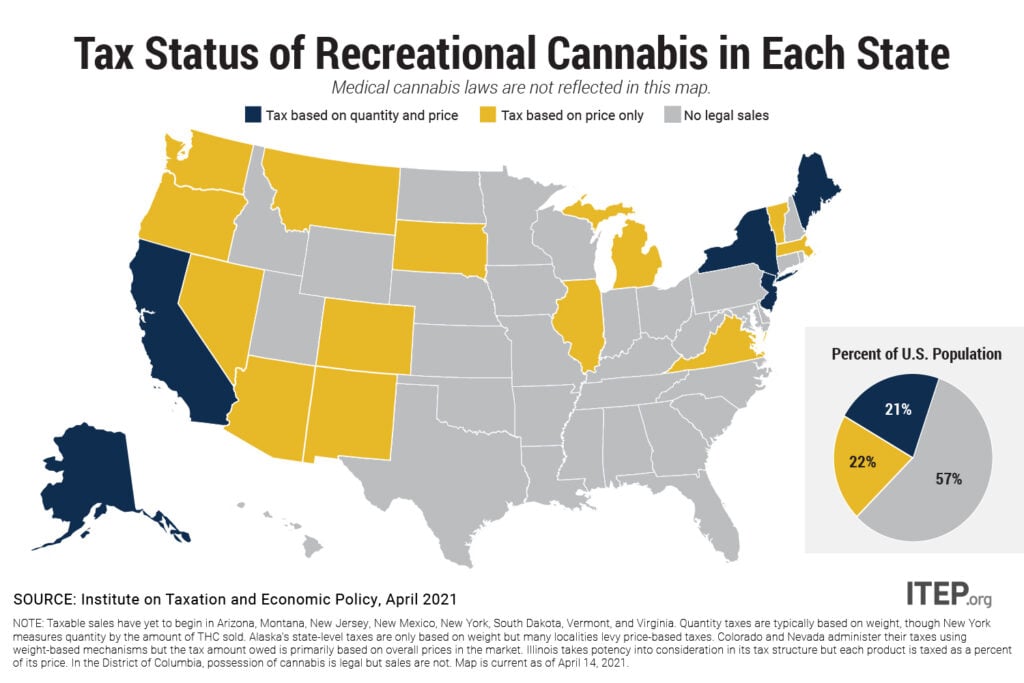

But while cannabis taxes have grown quickly in recent years, there are reasons to be concerned about the long-run trajectory of this revenue stream. For one thing, federal legalization has become almost inevitable as public support for legalization has reached a record high and the industry’s influence in Congress has grown. When legalization finally occurs—whenever that may be—the industry will undergo a major transformation as it gains long-awaited access to interstate commerce, banking services, and routine tax deductions that other businesses take for granted. Once multinational corporations can begin growing cannabis on an industrial scale and shipping it across state lines, a significant drop in cannabis prices is guaranteed. At that point, states that have chosen to build their cannabis structures exclusively around falling prices will find themselves facing revenue disappointment.

The good news is that states have straightforward options to prepare for this moment. Reworking cannabis taxes so that they apply to the quantity being purchased (e.g., taxing per ounce of flower or per milligram of intoxicant, for example), will allow for a more sustainable tax base than taxing at a percentage of a falling price. The other bit of good news is that states don’t need to look far for examples of quantity-based excise taxes. Every state in the nation already taxes alcohol and tobacco based on the quantity being purchased. Extending that approach to cannabis, as a few states have already done, is the logical next step.