Top 1 Percent’s share of the tax cut would grow from nearly one-third to one-half over 10 years

A national and 50-state distributional analysis of the House tax plan released late last week reveals that not only would the wealthiest 1 percent receive the greatest share of the total tax cut in year one, but their share would grow over time due to phase-ins of tax cuts that mostly benefit the rich and the eventual elimination or erosion in value of provisions that benefit low- and middle-income taxpayers.

Households in the top 1 percent of the income distribution collectively would receive nearly one-third (31 percent) of the tax cut in 2018, for an average cut of $48,580. Meanwhile, the middle-income quintile would receive an average tax cut of $750 and the poorest 20 percent would receive an average cut of $130.

But the 10-year outlook for the plan reveals that it would be even more generous to the top 1 percent in later years. By 2027, the top 1 percent of households’ collective share of the total tax cut would increase from 31 percent in year one to 48 percent by 2027, for an average cut of $64,720. Middle-income taxpayers’ average tax cut would erode to $460 from $750, and the poorest 20 percent’s average tax cut would decline to $110 from $130.

“A closer look at the details of this tax plan indicates that lawmakers are most serious about ensuring that they lower tax bills for the highest-earning households,” said Alan Essig, executive director of the Institute on Taxation and Economic Policy. For example, “the bill takes great care to fully eliminate the estate tax—which only the richest 0.2 percent of households pay—while phasing out a $300 tax credit that would benefit middle-income families. Further, low- and middle- class families likely will pay for these tax cuts that mostly benefit the highest earners through reduced investments in education, health care, infrastructure, scientific research, environmental protections, and other priorities.”

Part of the reason that the richest 1 percent would receive an even greater tax cut in later years is because the plan initially reduces the estate tax but repeals it by year 2024. The plan also includes a $300 non-child dependent credit in the first five years eliminates it in 2023. Further, due to how the plan accounts for inflation, tax benefits for taxpayers who earn their income from work would erode over time.

Following are significant findings from ITEP’s analysis:

- The richest 1 percent receive 31 percent of the entire value of the tax cut in year one and 48 percent of the value of the tax cut by 2027.

- The average value of the tax cut for the richest 1 percent in year one is $48,580, or 2.4 percent of their income, on average.

- The richest 1 percent not only receive the greatest share of the tax cut in terms of dollars, but also as a percentage of their income. For example, while the tax cut for the top 1 percent of households averages 2.4 percent of their income, the cut is just 0.9 percent of income for the poorest 20 percent on average and 1.4 percent of income for the middle-income quintile.

- The richest 1 percent is the only group for whom the value of the tax cut will grow over a decade. By 2027, the richest 1 percent of households are projected to have an average tax cut of $64,720 compared to $59,450 in year one. Meanwhile, the value of the tax cuts for other groups will shrink due to inflationary and other effects.

- The number of taxpayers who are subject to a tax hike is 8 percent in year one. But by 2027, the percent of taxpayers who would pay more would more than double to 18 percent.

To view the entire report, go to: http://itep.org/housetaxplan/

Additional ITEP research related to the House proposal include:

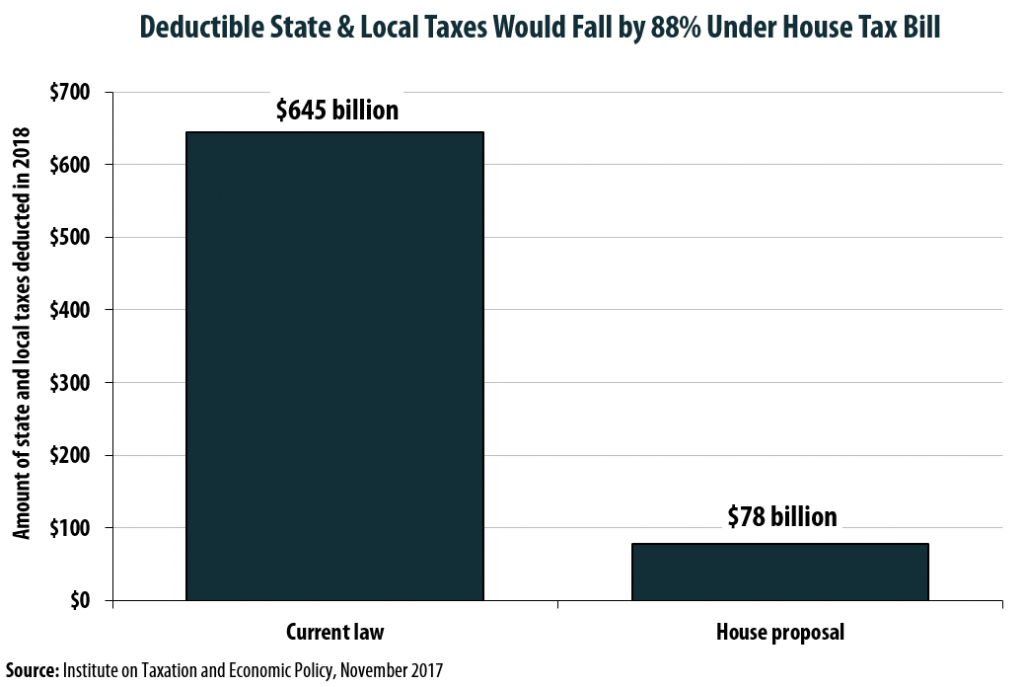

- House Plan Slashes SALT Deductions by 88 percent, Even with $10,000 Property Tax Deduction

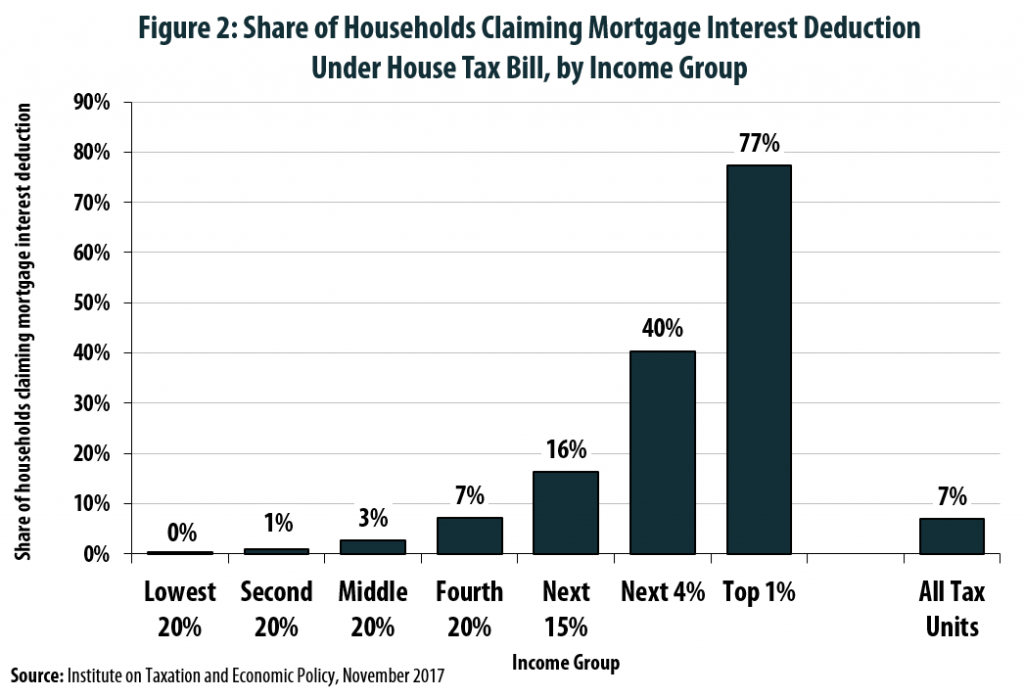

- Mortgage Interest Deduction Wiped Out for 7 in 10 Current Claimants Under House Tax Plan

- House Tax Bill Would Reserve Charitable Giving Subsidies for a Small Subset of Wealthier Households, https://itep.org/house-tax-bill-would-reserve-charitable-giving-subsidies-for-a-small-subset-of-wealthier-households/