Ahead of this year’s delayed Tax Day, our partners at Prosperity Now released a powerful report providing a comprehensive overview of many of the ways our federal tax system privileges wealth over work, while also lifting up several provisions which could serve as a template for improving progressivity within the tax code.

The report makes clear the connections between our federal tax code—which the report correctly describes as “riddled with systemic racism”—and a failure to curb growing inequality. ITEP is proud to have worked closely with Prosperity Now to prepare distributional estimates, including breakdowns of benefits and coverage by race and ethnicity* of several tax of the tax expenditures discussed, for the report.

The federal government spends roughly $634 billion a year through the tax code to build wealth via retirement savings, higher education, and homeownership. Yet many of those incentives are unavailable to working families. Additionally, Black and Hispanic taxpayers are overrepresented in the bottom 40 percent of tax filings by income, reflecting the impact of systemic racism on these families’ ability to accumulate wealth and on-going discrimination in the labor market. Several of these incentives primarily benefit the already wealthy, who are disproportionately white. For example, ITEP estimates that the top 20 percent of white households—that make up 15.8 percent of all tax returns—receive 59.1 percent of the benefits of the mortgage interest deduction (MID), one of the key federal spending policies that rewards homeownership. Poorly targeted programs like the MID are not just ineffective, they also exacerbate racial, ethnic, and gender gaps in wealth.

By contrast, the report duly recognizes the Earned Income Tax Credit (EITC) as an example of a tax policy that targets its benefits to low- and moderate-income taxpayers, as well as taxpayers of color. ITEP estimates that Black, Native American and/or Alaska Native, Native Hawaiian/other Pacific Islander and Hispanic households make up 24.9 percent of all tax returns but account for 40.1 percent of those claiming the EITC. Additionally, 83.5 percent of the EITC’s benefits go to those in the lowest 40 percent by income. In this way, the EITC is both well-targeted to reduce income inequality and racial and ethnic disparities.

The authors correctly call for reforms in the federal tax system to curb the ways our existing code privileges wealth and improve the targeting of the substantial amount of investment which occurs through the tax code to ensure all working families, including Black, Hispanic, Native and other people of color, are able to equitably access those incentives. It is worth noting that other rich nations wield their tax codes and spending policies as much more powerful tools for fighting inequality. It is a political choice that the U.S. does not do more to fight poverty and income inequality and push harder for racial justice using its tax code.

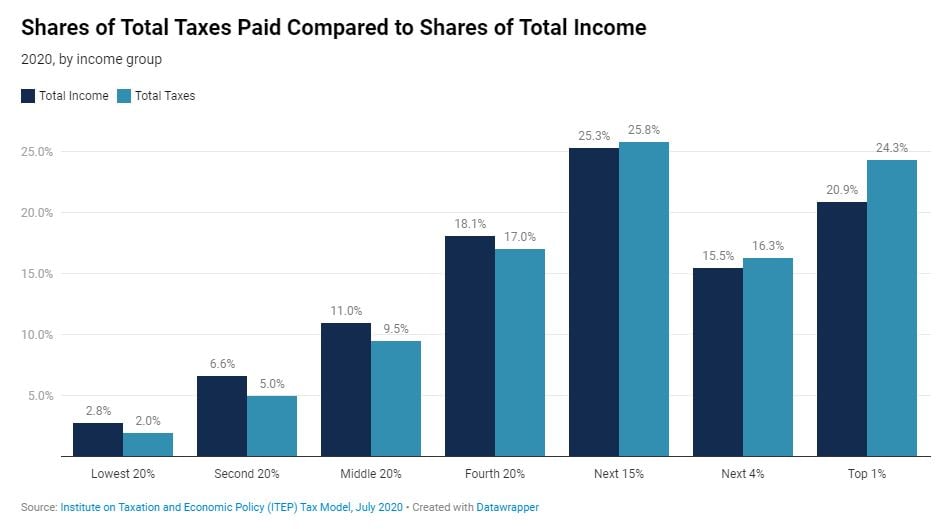

It’s also worth noting the nation’s combined local, state, and federal tax code is only marginally progressive as ITEP documents annually in our Who Pays Taxes in America? report. The passage of the Trump administration’s Tax Cuts and Jobs Act further tilted the playing field against working families. In 2020, 72 percent of its benefits will go to the highest 20 percent of tax filers by income. Because of existing racial inequalities, the TCJA’s regressive design will give white taxpayers in 79 percent of the law’s benefits in 2020, even though white taxpayers make up only 67 percent of all tax units. By contrast, Black taxpayers, who account for 10 percent of all tax units, will only receive 5 percent of the law’s benefits.

Demanding that our tax code be used more aggressively to reduce inequality and adequately fund public services in all communities is not just a tax policy issue, it is a racial justice issue. The ways in which our tax code privileges wealth over work exacerbate inequalities—both socioeconomic and racial—and are a missed opportunity to level the playing field. Lawmakers can and should build on existing progressive tax provisions to address inequality and eliminate provisions which excuse the richest households from contributing their fair share.

*We adapt a methodology rooted in methods used by the Tax Policy Center to achieve imputations within the context of ITEP’s microsimulation model. Forthcoming reports and resources will present additional applications of this exercise and provide supplementary documentation.