Progressive taxation requires the rich to pay a higher share of their income in taxes than poor people. Most of us intuitively understand that the richest households benefit the most from the society built with our tax dollars and can afford to pay a larger share of their income to support public investments. But when one considers all the taxes that Americans pay, it turns out that our tax system overall is barely progressive. Having a sound understanding of who pays taxes and how much is a particularly relevant question now as the nation grapples with a health and economic crisis that is devastating lower-income families and requiring all levels of government to invest more in keeping individuals, families and communities afloat.

This year, the share of all taxes paid by the richest 1 percent of Americans (24.3 percent) will be just a bit higher than the share of all income going to this group (20.9 percent). The share of all taxes paid by the poorest fifth of Americans (2 percent) will be just a bit lower than the share of all income going to this group (2.8 percent).

ITEP generated these estimates using its tax model, which calculates different types of taxes using a dataset of representative taxpayers. In order to reflect the long-term state of our tax system, these figures do not take into account the recent economic downturn or the temporary tax provisions enacted to address it.

FIGURE 1

Some taxes we pay are quite progressive, including the federal personal income tax, corporate income tax, and estate tax.[1] But Americans pay other federal taxes that are not progressive. For example, everyone who works pays the Social Security payroll tax. This tax does not apply to investment income that most very wealthy families have, and it only applies to the first $137,700 of earnings a worker receives in 2020.

Americans also pay state and local taxes that are particularly regressive, meaning they capture a larger share of income from low- and middle-income families than from wealthy families. For example, state and local sales taxes are particularly regressive because poor families often must spend all their income buying necessities while wealthy families can save most of their income, shielding it from sales taxes.

When the effects of all these different taxes are taken together, it turns out that the tax system is not as progressive as many believe.

This is not to say that our tax system is not progressive at all. Americans’ total effective tax rate, that is the total amount of taxes paid as a percentage of income, does rise with income, as illustrated in Figure 2. But not as much as many Americans assume. As illustrated in Figure 2, those in the top 1 percent will pay a little more than a third of their income in taxes this year on average while those among the middle fifth of Americans will pay a bit more than a fourth of their income in taxes on average.

FIGURE 2

America’s Tax System Might Be Even Less Progressive

These figures may overstate the progressivity of the nation’s tax system for several reasons.

First, ITEP is not yet able to split out different income groups within the richest 1 percent. If we did, we might find that effective tax rates are surprisingly low for the very, very rich given that much of their income is capital gains and stock dividends, which are taxed at lower rates. Research by Emmanuel Saez and Gabriel Zucman finds that the very richest 400 taxpayers in the United States pay a lower effective tax rate than other groups.[2] While they use very different methods than ITEP, their conclusions are not surprising.

Second, calculating the fraction of income paid in taxes is just one way to measure effective tax rates and measure the progressivity of the nation’s tax system. To ascertain the extent to which taxes are higher for those with more ability to pay, it might make more sense to define effective tax rates as taxes paid as a share of taxpayers’ net worth.

Saez and Zucman estimated that in 2019, the wealthiest 0.1 percent households would pay 3.2 percent of their net worth in taxes while the bottom 99 percent of households ranked by wealth would pay 7.2 percent of their net worth in taxes.[3] In other words, when defining effective tax rates as taxes paid as a share of wealth, they find that the tax system is very regressive. This is unsurprising given that the concentration of wealth at the top is even more severe than the concentration of income at the top.[4]

How the 2017 Tax Law Made Our Tax System Less Progressive

The Tax Cuts and Jobs Act (TCJA), which was enacted by President Trump and his supporters in Congress at the end of 2017, made the nation’s tax system less progressive. TCJA cut federal taxes, and thus cut the total effective tax rate, for all income groups. This is illustrated in Figure 3, which compares the total effective tax rate for each group as it will be in 2020 versus what it would have been if TCJA had not been enacted.

However, the law particularly benefited the rich thanks to its provisions cutting personal income taxes for business owners, its cuts in the corporate income tax and its cut in the estate tax. As illustrated in Figure 4, the decline in effective tax rates for the richest 5 percent of taxpayers exceeded the decline for other income groups.

FIGURE 3

FIGURE 4

TCJA reduced the federal effective tax rate by 2.2 percentage points for the top 1 percent and by 2.6 for the next richest 4 percent. For all other income groups, TCJA reduced the federal effective rate by far less than 2 percentage points.

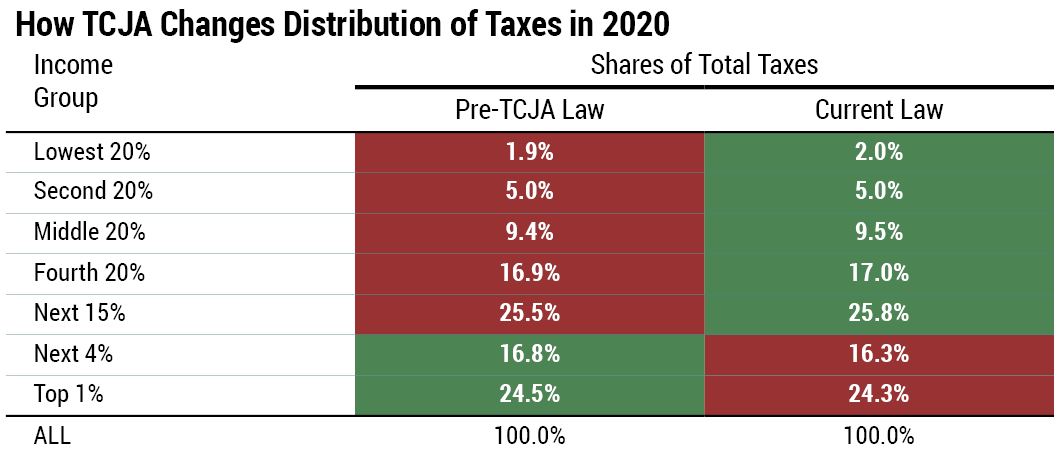

The share of total taxes paid by each income group was also affected by the 2017 law. Figure 5 shows that TCJA reduced the overall share of taxes paid by the richest 5 percent while increasing the share paid by other income groups.

FIGURE 5

Figure 5 provides the projected share of total federal, state, and local taxes paid by each income group under current law and an estimate of the share they would pay if TCJA had never been enacted. For each income group, the red-shaded figure is the scenario in which they pay a smaller share, and the green-shaded figure is the scenario in which they pay a larger share. Current law results in a smaller share paid by the richest 1 percent and the next richest 4 percent. All other groups pay a larger share of total taxes under current law compared to what they would pay under pre-TCJA law.

America’s Tax System Can Be Better

America’s tax system is moderately progressive and there are opportunities to make it still more progressive. State and local governments have many options to make their tax codes fairer. Congress has options to make the federal tax code more progressive, to offset the regressive impacts of state and local taxes.[5] Some of those options involve repealing provisions of TCJA, but others would address problems in the federal tax code that predated TCJA.[6]

[1] The federal personal income tax has a progressive rate structure and also provides low-wage working people with tax credits that are refundable, meaning they can result in negative income tax liability for certain low-income households. (These refundable credits are included in this analysis.) Corporate income taxes are paid directly by corporations. But like all taxes, corporate income taxes are ultimately borne by people. In this case the tax is borne mostly by the owners of corporate stocks and other business assets, which are mostly owned by well-off households. The estate tax applies only to the value of any estate exceeding $11,580,000 in 2020 (twice that amount for married couples) and consequently only affects the very wealthiest families.

[2] Steve Wamhoff, “Emmanuel Saez and Gabriel Zucman’s New Book Reminds Us that Tax Injustice Is a Choice,” Institute on Taxation and Economic Policy, October 15, 2019. https://itep.org/emmanuel-saez-and-gabriel-zucmans-new-book-reminds-us-that-tax-injustice-is-a-choice/

[3] Letter from Emmanuel Saez and Gabriel Zucman to Senator Elizabeth Warren, July 18, 2019. https://www.warren.senate.gov/imo/media/doc/saez-zucman-wealthtax.pdf

[4] Steve Wamhoff, “The U.S. Needs a Federal Wealth Tax,” Institute on Taxation and Economic Policy, January 23, 2019. https://itep.org/the-u-s-needs-a-federal-wealth-tax/

[5] Dylan Grundman, “Moving Toward More Equitable State Tax Systems,” Institute on Taxation and Economic Policy, January 9, 2019. https://itep.org/moving-toward-more-equitable-state-tax-systems/

[6] Steve Wamhoff, Matthew Gardner, “Progressive Revenue-Raising Options,” Institute on Taxation and Economic Policy, February 5, 2019. https://itep.org/progressive-revenue-raising-options/