Recent Work by ITEP

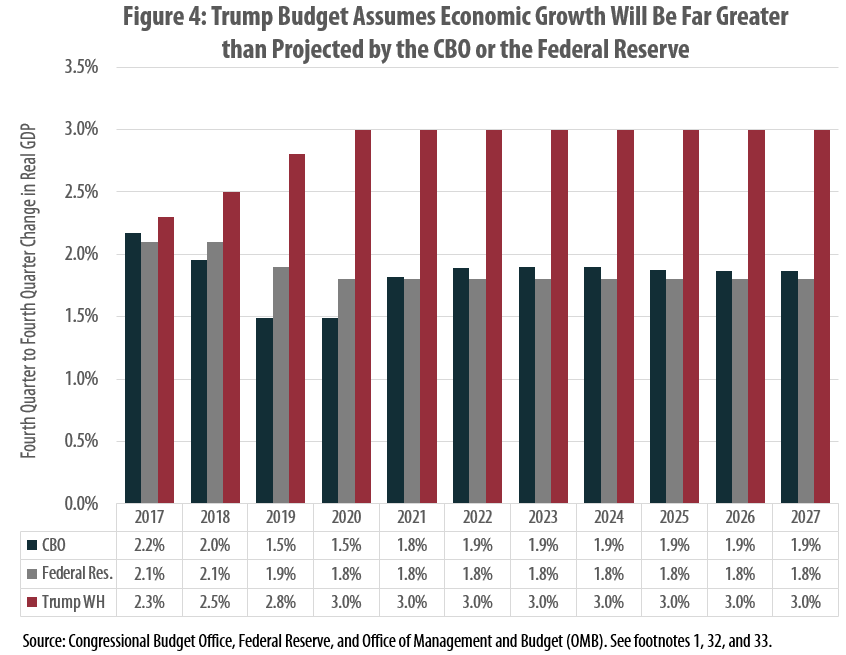

Trump Budget Uses Unrealistic Economic Forecast to Tee Up Tax Cuts

June 29, 2017 • By Carl Davis

The Trump Administration recently released its proposed budget for Fiscal Year 2018. The administration claims that its proposals would reduce the deficit in nearly every year over the next decade before eventually achieving a balanced budget in 2027, but the assumptions it uses to reach this conclusion are deeply flawed. This report explains these flaws and their consequences for the debate over major federal tax changes.

State Rundown 6/28: States Scramble to Finish Budgets Before July Deadlines

June 28, 2017 • By ITEP Staff

This week, several states attempt to wrap up their budget debates before new fiscal years (and holiday vacations) begin in July. Lawmakers reached at least short-term agreement on budgets in Alaska, New Hampshire, Rhode Island, and Vermont, but such resolution remains elusive in Connecticut, Delaware, Illinois, Maine, Pennsylvania, Washington, and Wisconsin.

Gas Taxes Will Rise in 7 States to Fund Transportation Improvements

June 28, 2017 • By Carl Davis

Summer gas prices are at their lowest level in twelve years, which makes right now a sensible time to ask drivers to pay a little more toward improving the transportation infrastructure they use every day. Seven states will be doing this on Saturday, July 1 when they raise their gasoline tax rates. At the same time, two states will be implementing small gas tax rate cuts.

Many state governments are struggling to repair and expand their transportation infrastructure because they are attempting to cover the rising cost of asphalt, machinery, and other construction materials with fixed-rate gasoline taxes that are rarely increased.

The flawed design of federal and state gasoline taxes has made it exceedingly difficult to raise adequate funds to maintain the nation’s transportation infrastructure. Thirty states and the federal government levy fixed-rate gas taxes where the tax rate does not change even when the cost of infrastructure materials rises or when drivers transition toward more fuel-efficient vehicles and pay less in gas tax. The federal government’s 18.4 cent gas tax, for example, has not increased in over twenty-three years. Likewise, nineteen states have waited a decade or more since last raising their own gas tax rates.

Senate Health Care Reform Bill Just as “Mean” as the House Version

June 26, 2017 • By Alan Essig

The Congressional Budget Office today released its score of the Senate Health Care proposal and the news is not good. It’s no wonder a narrow group of 13 lawmakers cobbled together the bill behind closed doors. Now that the measure has seen the light of day, we know that it epitomizes Robin Hood in reverse policies by snatching health coverage from 22 million people by 2026 (15 million in 2018) while showering tax cuts on the already wealthy.

Rather than being known for its pioneering pharmaceuticals, Mylan is increasingly becoming infamous for its pioneering tax avoidance strategies. In 2015, Mylan used an inversion to claim that it is now based in the Netherlands for tax purposes. It is a Dutch company only on paper because ownership of the company was mostly unchanged and it continues to operate largely out of the United States. This maneuver has allowed the company to avoid millions in taxes on its earnings in the U.S. and abroad. But that’s not the end of Mylan’s innovation when it comes to tax planning. A new…

Explaining our Analysis of Washington State’s Highly Regressive Tax Code

June 22, 2017 • By Carl Davis

Supporters of creating a local personal income tax in Seattle are rightly concerned about the lopsided nature of their state’s tax code. In a 50-state study titled Who Pays?, produced using our microsimulation tax model, we found that Washington State’s tax system is the most regressive in the nation.

West Virginia Lawmakers Settle on Imperfect Budget, Delay Tax Debate for Next Session

June 21, 2017 • By Aidan Davis

West Virginia’s roller coaster ride of a session is nearing its tumultuous end. In a press conference this morning, Gov. Jim Justice announced that he will let the legislature’s most recent budget bill become law without his signature.

State Rundown 6/21: Crunch Time for Many States with New Fiscal Year on Horizon

June 21, 2017 • By Meg Wiehe

This week several states rush to finalize their budget and tax debates before the start of most state fiscal years on July 1. West Virginia lawmakers considered tax increases as part of a balanced approach to closing the state’s budget gap but took a funding-cuts-only approach in the end. Delaware legislators face a similar choice, […]

ITEP in the News

CBS News: The One Big Beautiful Bill Act is 1 year old. Here are the winners and losers.

Yahoo News: Hawaii’s new ‘millionaire tax’ rivals top tax rate among other states

Lexington Herald-Leader: How are gas prices set in KY? From oil to the pump, here’s what to know

Wall Street Journal: Coke Takes on IRS With $20 Billion at Stake

Reuters: Hawaii Considers Gasoline Tax Suspension as Pump Prices Soar

ITEP Work in Action

Senator Chris Van Hollen: Van Hollen, Pettersen Lead Lawmakers in Introducing Legislation to Bring Transparency to Corporate Abuse of Tax Havens, Job Offshoring

Center on Budget and Policy Priorities: Missouri Tax Amendment Likely to Seriously Harm Services, Shift Taxes Onto Working Families

California Budget and Policy Center: Should Voters Approve Prop. 3? How Top Tax Rates Have Helped Californians

Migration Policy Institute: Rooted in the Valley: Immigrants in Napa County’s Communities and Economy

The Bell Policy Center: Colorado Ballot Guide 2026

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.