Recent Work by ITEP

Avocado Toast, iPhones, Billionairesplaining and the Trump Budget

May 30, 2017 • By Jenice Robinson

A couple weeks ago, a billionaire set the Internet ablaze when on 60 Minutes Australia he chided millennials to stop buying avocado toast and fancy coffee if they wanted to buy a home. The backlash was swift and deserved. Twenty- and early thirty-something people rightly took offense to the suggestion that they haven’t purchased homes […]

Besides Eviscerating the Safety Net, Trump Budget Would Put States in a Fiscal Bind

May 26, 2017 • By Misha Hill

There has been considerable discussion about the human impact of the Trump budget’s draconian cuts to what remains of the social safety net. A long-standing conservative talking point in response to such criticism is that states can pick up the tab when federal dollars disappear. But at a time when many states are facing budget shortfalls and the effect of federal tax reform is yet to be determined, it is outlandish to suggest that states are flush with cash to make up for federal spending reductions.

Congressional Hearing Highlights Problems with the Border Adjustment Tax

May 25, 2017 • By Richard Phillips

The debate over the so-called border adjustment tax (or BAT) took center stage this week when the House Ways and Means Committee held its first hearing on the topic. Despite strong support by the House Republican leadership and the Chairman of the Ways and Means Committee, Rep. Kevin Brady, the proposal faced an onslaught of criticism during the hearing from invited witnesses and members of both parties.

23 Million Uninsured Americans Is Too Great a Cost to Finance Tax Cuts for the Rich

May 24, 2017 • By Richard Phillips

The cost to give $1 trillion in tax cuts to the wealthy and corporations is 23 million uninsured Americans by 2026. This is the bottom-line take away from the much-awaited Congressional Budget Office (CBO) score of the American Health Care Act, which House Republicans rushed through the chamber and narrowly passed (217-213) in early May.

This week, Kansas lawmakers continued work on fixing the fiscal mess created by tax cuts in recent years, as legislators in Louisiana, Minnesota, Oklahoma, and West Virginia attempted to wrap up difficult budget negotiations before their sessions come to an end, and Delaware lawmakers advanced a corporate tax increase as one piece of a plan to close that state's budget shortfall. Our "what we're reading" section this week is also packed with articles about state and local effects of the Trump budget, new 50-state research on property taxes, and more.

Trump Budget Plan Would Eliminate Child Tax Credits for Working Families Due to Parents’ Immigration Status

May 23, 2017 • By Misha Hill

As ITEP has detailed, undocumented immigrants are taxpayers, contributing close to $12 billion a year in state and local taxes while also paying federal payroll, income, and excise taxes. In spite of these facts, Mick Mulvaney, President Trump’s budget director, has spread erroneous information to validate the administration’s cruel proposal to strip a proven anti-poverty benefit from undocumented immigrants and their children.

ITEP’s Commitment to Being a Voice for Low-, Moderate- and Middle-Income People in Tax Policy Debates

May 22, 2017 • By Alan Essig

A strong voice for working people in federal and state tax policy debates is absolutely critical. Sound, progressive tax policies make all the difference between high-quality educational systems or crowded classrooms with limited resources. They account for the difference between structurally sound roads and bridges or potholes and other crumbling infrastructure. At the federal level, good tax policy means raising enough revenue so the nation can adequately fund child care and early education, health care, food inspection, national parks, and a clean, safe environment among other things.

This week saw tax debates heat up in many states. Late-session discovered revenue shortfalls, for example, are creating friction in Delaware, New Jersey, and Oklahoma, while special sessions featuring tax debates continue in Louisiana, New Mexico, and West Virginia. Meanwhile the effort to revive Alaska's personal income tax has cooled off.

Tax Avoiding Companies Well Represented at Tax Reform Hearing

May 18, 2017 • By Richard Phillips

Today the House Ways and Means Committee will hold its first tax reform hearing of 2017, which marks the official opening of the tax reform debate in Congress. True tax reform, if the committee sought to achieve it, could create more jobs and ensure companies are paying their fair share by cracking down on the massive offshore tax avoidance that companies engage in. Unfortunately, the panel of witnesses for today’s hearing is largely made up of representatives of various major corporations that are beneficiaries of the loopholes in our current corporate tax laws. Given this, it seems likely that these…

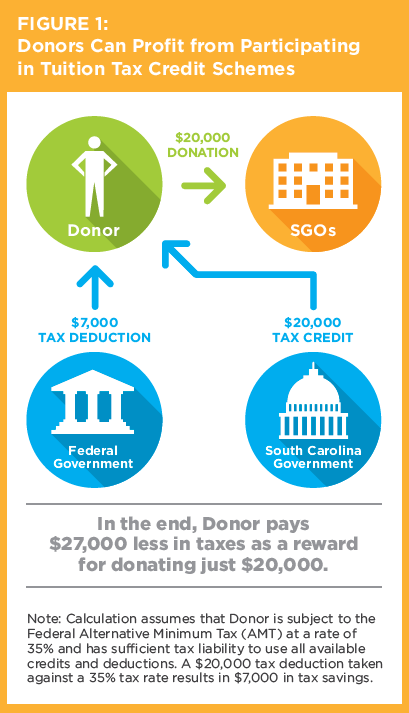

Investors and Corporations Would Profit from a Federal Private School Voucher Tax Credit

May 17, 2017 • By Carl Davis

A new report by the Institute on Taxation and Economic Policy (ITEP) and AASA, the School Superintendents Association, details how tax subsidies that funnel money toward private schools are being used as profitable tax shelters by high-income taxpayers. By exploiting interactions between federal and state tax law, high-income taxpayers in nine states are currently able […]

ITEP in the News

CBS News: The One Big Beautiful Bill Act is 1 year old. Here are the winners and losers.

Yahoo News: Hawaii’s new ‘millionaire tax’ rivals top tax rate among other states

Lexington Herald-Leader: How are gas prices set in KY? From oil to the pump, here’s what to know

Wall Street Journal: Coke Takes on IRS With $20 Billion at Stake

Reuters: Hawaii Considers Gasoline Tax Suspension as Pump Prices Soar

ITEP Work in Action

Senator Chris Van Hollen: Van Hollen, Pettersen Lead Lawmakers in Introducing Legislation to Bring Transparency to Corporate Abuse of Tax Havens, Job Offshoring

Center on Budget and Policy Priorities: Missouri Tax Amendment Likely to Seriously Harm Services, Shift Taxes Onto Working Families

California Budget and Policy Center: Should Voters Approve Prop. 3? How Top Tax Rates Have Helped Californians

Migration Policy Institute: Rooted in the Valley: Immigrants in Napa County’s Communities and Economy

The Bell Policy Center: Colorado Ballot Guide 2026

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.