Sen. Chris Van Hollen recently introduced the Working Americans’ Tax Cut Act (WATCA), which offers a generous middle-class tax cut paid for with a new tax on millionaires. He, along with most of the Democratic caucus in the Senate, is also a cosponsor of the American Family Act and the Tax Cut for Workers Act, bills that would expand the Child Tax Credit (CTC) and the Earned Income Tax Credit (EITC).

This analysis examines these three policies with the understanding that they do not include all the tax proposals that Sen. Van Hollen may support and are not a complete tax plan. Lawmakers will need to decide how much revenue to devote to the types of tax breaks provided under this legislation. This report takes no position on that question but rather provides estimates of the impacts on different income groups and on revenue.

A Progressive but Expensive Approach to Tax Reform

Combining the Working Americans’ Tax Cut Act (WATCA) with proposals to expand the Child Tax Credit (CTC) and Earned Income Tax Credit (EITC) would make our tax system more progressive by providing the biggest tax reductions to low-income people as a share of their income and reducing taxes for middle-income people, while raising taxes on the richest individuals and households.

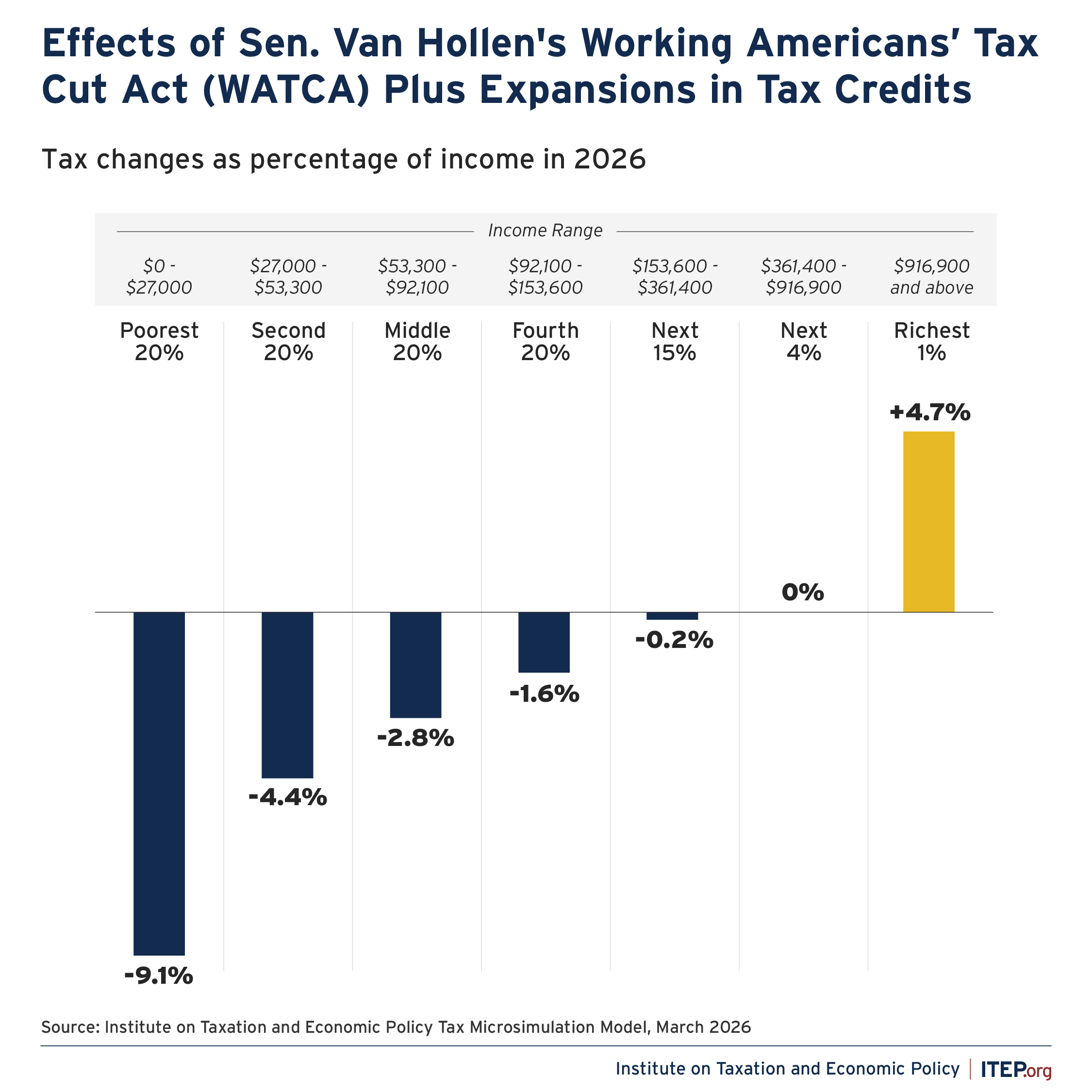

Figure 1

In 2026, the combination of the WATCA’s tax reduction plus the CTC and EITC expansions would provide an average tax break ranging from nearly $1,400 to about $2,000 for the bottom four quintiles of taxpayers (the bottom 80 percent of taxpayers). The richest 1 percent would pay higher taxes on average as a result of the millionaire surcharge included in the WATCA.

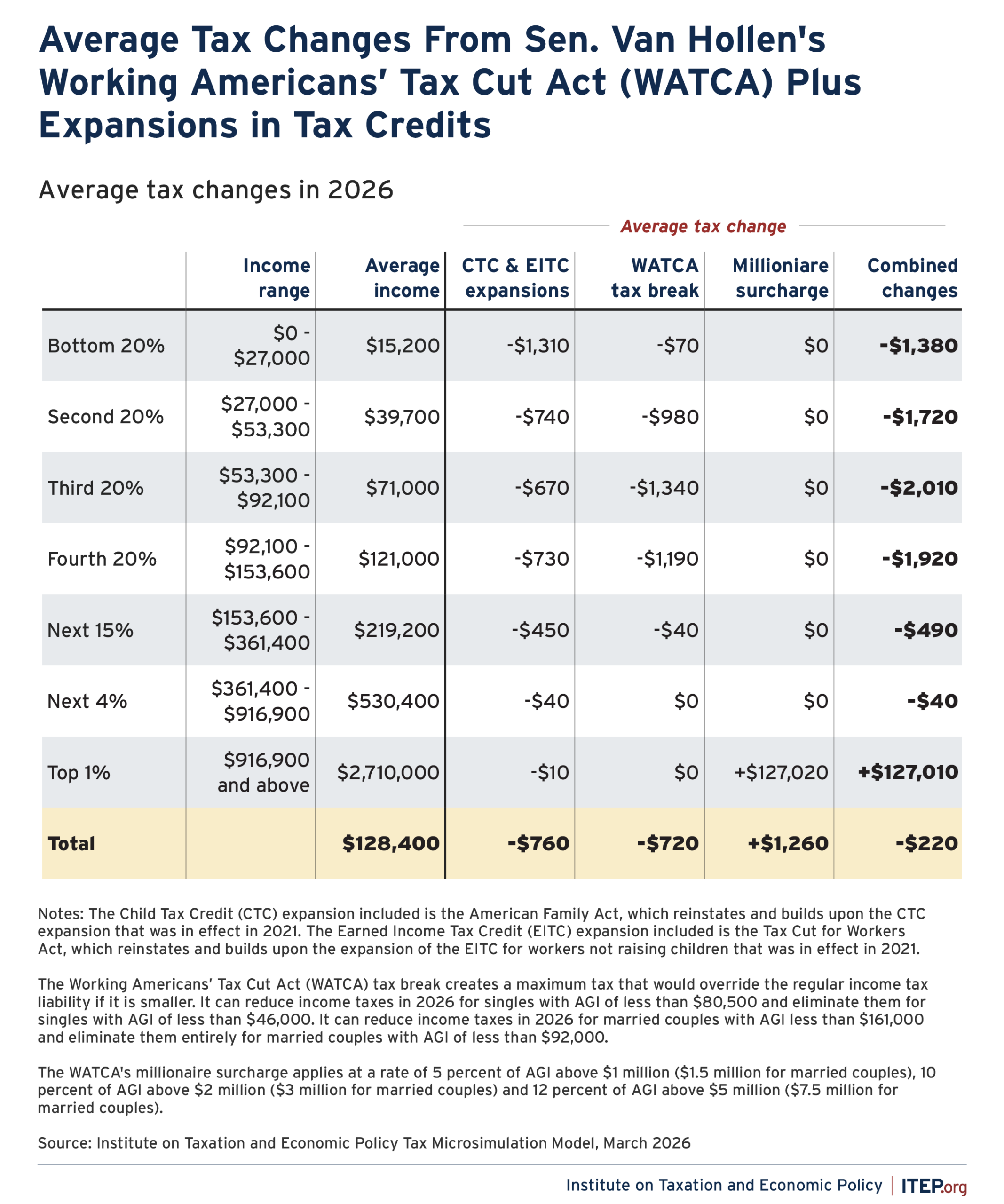

Figure 2

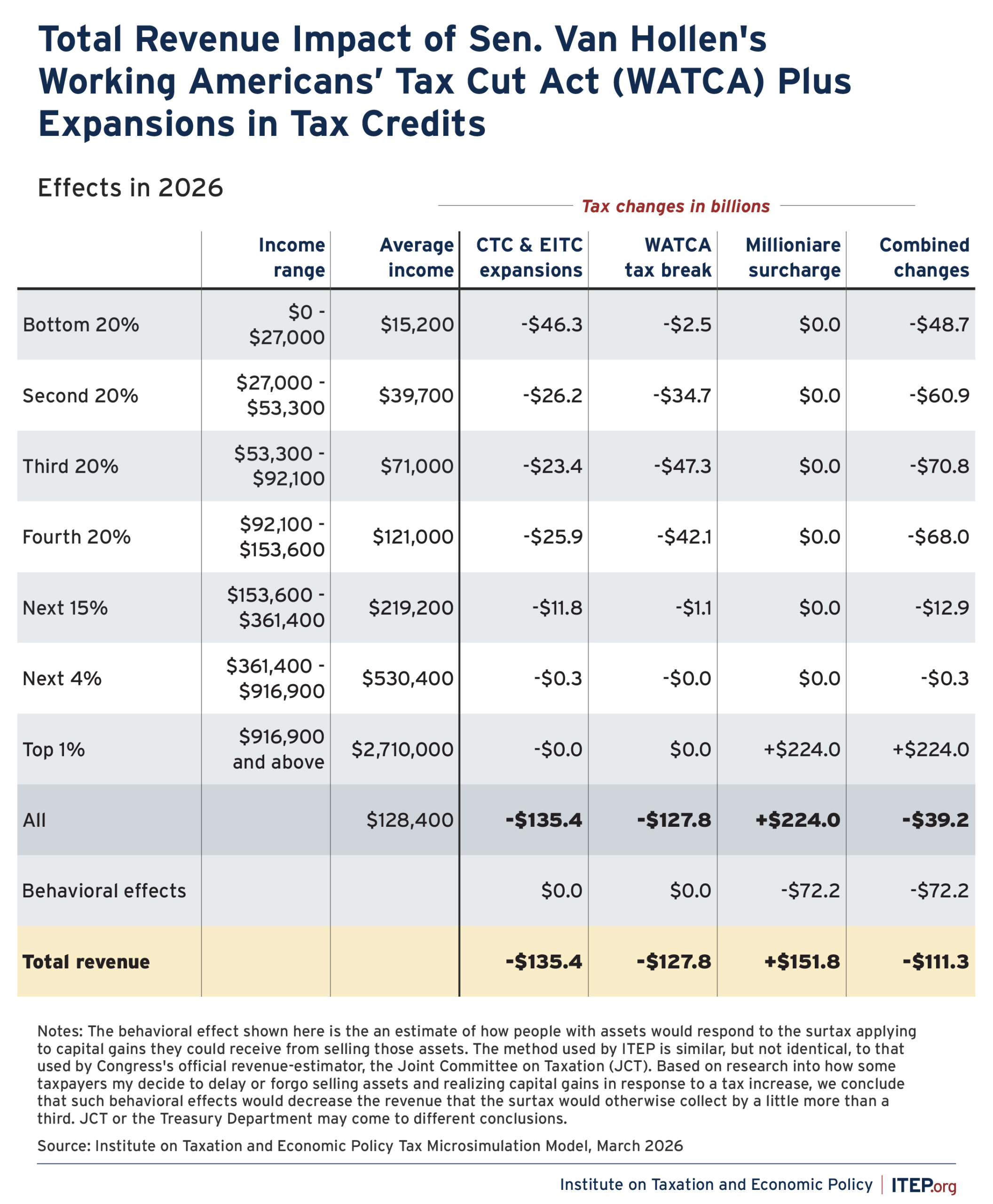

This overall plan would be progressive but would also reduce revenue by more than $100 billion a year.1

Figure 3

More Details

Working Americans’ Tax Cut Act (WATCA)

The WATCA makes two major changes to the federal tax code. First, it creates a maximum tax that would override income tax liability under the regular rules if it were smaller, providing a significant tax break to many middle-class households. Second, it would offset the costs of this tax break with a surcharge on adjusted gross income above $1 million.

The WATCA’s Tax Break

Taxpayers would pay whichever is less, a new maximum tax calculated under the WATCA, or the income tax calculated under existing rules. The maximum tax would have a significant “cost-of-living exemption,” which can also be thought of as the income threshold that tax filers would need to exceed to owe any income tax at all.

The cost-of-living exemption in 2026 would be $46,000 for singles, $64,400 for heads of households (who are mostly single parents), and $92,000 for married joint filers. The maximum tax is calculated as 25.5 percent of income beyond these amounts.

This provision would benefit relatively few people among the poorest 20 percent or richest 20 percent of Americans and would mainly benefit the middle 60 percent.

Many people among the poorest 20 percent would not benefit because their income tax liability is already zero, either because they earn less than the standard deduction they claim or because the Earned Income Tax Credit or Child Tax Credit eliminates their income tax liability.

Most high-income people would not benefit from this provision. The maximum tax would not be allowed for taxpayers whose income equals 175 percent or more of the exemption. This means that maximum tax would be unavailable in 2026 for taxpayers with income exceeding $80,500 in the case of singles, $112,700 in the case of heads of households, and $161,000 for married joint filers.2

The WATCA’s Millionaire Surcharge

The millionaire surcharge in the WATCA would have three rates that apply to adjusted gross income (AGI):

- 5 percent of AGI above $1.5 million for married joint filers and above $1 million for other taxpayers.

- 10 percent of AGI above AGI $3 million for married joint filers and above $2 million for other taxpayers.

- 12 percent of AGI above $7.5 million for married joint filers and above $5 million for other taxpayers.

American Family Act (AFA)

This provision would reinstate and build on the expansion of the Child Tax Credit (CTC) that was in effect for one year in 2021. It consists of two major changes.

First, for middle-class families the maximum credit per child would be increased from $2,200 under current law to $3,600 for children age 6 and older and it would be increased to $4,320 for children younger than 6. The AFA also includes a “baby bonus,” which effectively increases the maximum CTC for the first year of a child’s life to $6,360. (These amounts would be adjusted annually for inflation.) For well-off families, the maximum credit would remain $2,220 per child.

Second, the provision would remove the income restrictions that prevent poorer families from receiving the full credit amount. The credit is partitioned into two amounts, a non-refundable portion and a refundable portion. The non-refundable portion is the amount that families can use to directly offset their tax liability. The refundable portion is the amount that families can receive on top of their tax refund if they have little to no federal individual income tax liability.

Rules that restrict the refundable portion of the credit result in smaller total credits for families who have modest incomes – families who typically work and pay payroll taxes, excise taxes, tariffs, and many state and local taxes but do not earn enough to owe much or anything in federal income taxes. Under current law, 30 percent of children are too poor to receive the full CTC, and that percentage would be reduced to zero under the American Family Act.3

Tax Cut for Workers Act

This provision would expand the Earned Income Tax Credit (EITC) for low-income working people who do not have children living with them. Under current law, childless people are entitled only to a very small EITC of no more than about $660 in 2026, which would be increased to a maximum EITC of about $1,500 under this provision.

The EITC is a credit equal to a certain percentage of earnings up to a maximum amount of earnings. Under current law the credit percentage and the maximum earnings credited are both very low for childless workers, 7.65 percent and $8,680. (Hence the maximum EITC of about $660 for this group, which is 7.65 percent of $8,680.)

Under this provision, the credit rate for workers without children would double from 7.65 percent to 15.3 percent and the maximum earnings credited would increase also, bringing the maximum credit for these workers to about $1,500 in 2026.

Appendix

Endnotes

- 1. This calculation incorporates an assumption that, with respect to capital gains (profits from selling assets) taxpayers affected by the high-income surcharge will reduce their realizations (they will sell less in assets) to mitigate their tax increase. If Congress’s official revenue estimator, the Joint Committee on Taxation (JCT) does a revenue estimate of this proposal it might conclude that the surcharge will raise more or less than we calculate here if it makes a different assumption than ours regarding a behavioral response. It is likely, however, not to be dramatically different as the approach we use to estimate taxes on capital gains is similar to JCT’s. It is also possible that if this plan was enacted, it could include reforms that would prevent the wealthy from using various maneuvers to avoid the tax increase on their capital gains.

- 2. The ability to use the maximum tax calculation would not be “phased out” in the sense that many tax breaks are phased out gradually as income levels rise. The proposal is designed to make a traditional phaseout unnecessary because for most people (people claiming the standard deduction) the income level at which the maximum tax becomes unavailable is nearly the same income level at which they would pay less under the regular income tax rules anyway.

- 3. Joe Hughes, “The Child Tax Credit Leaves Out Millions of Children in 2026. There Are Better Alternatives,” Institute on Taxation and Economic Policy, March 10, 2026.